The Story Of Stagnant Wage Growth – OpEd

By Dean Baker

This recovery has not been great for workers. They have seen modest real wage gains over the last five years, but these gains have not come close to making up the ground lost in the recession and the first years of the recovery.

Nonetheless, real wages have been growing for most of the last five years. The last month has been an exception to this pattern, not because nominal wages have grown less, but because we had a large jump in energy prices, which has depressed real wage growth. Here’s picture for the last five years.

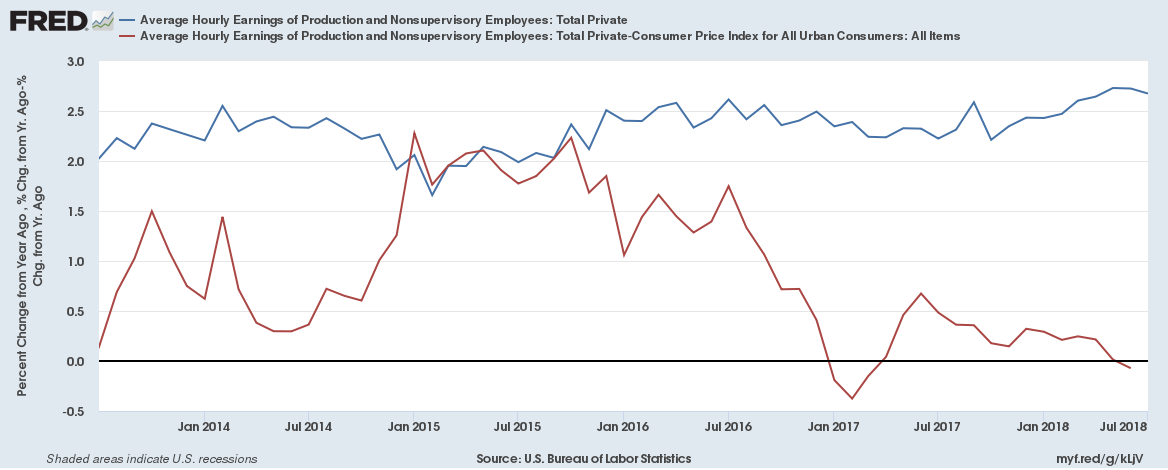

As can be seen, there is a very modest acceleration in the rate of average hourly wage growth over this period from just over 2.0 percent in the middle of 2013 to 2.7 percent in the most recent data. Real wage growth, which is the difference between the rate of wage growth and the rate of inflation, as measured by the Consumer Price Index, has mostly been positive, with the exception of a few months at the end of 2016 and beginning of 2017 and last month.

As can be seen, there is a very modest acceleration in the rate of average hourly wage growth over this period from just over 2.0 percent in the middle of 2013 to 2.7 percent in the most recent data. Real wage growth, which is the difference between the rate of wage growth and the rate of inflation, as measured by the Consumer Price Index, has mostly been positive, with the exception of a few months at the end of 2016 and beginning of 2017 and last month.

The explanation for the much larger variation in the real wage than the nominal wage is the variation in the rate of inflation over this period which is in turn overwhelmingly a function of changes in world oil prices. A sharp drop in world oil prices in 2014 translated into much lower energy prices for consumers in the United States. This meant very low, and even negative inflation rates, in 2015. The result was a much more rapid rate of real wage growth.

World oil prices have partially rebounded in the last two years, going from lows near $40 a barrel to current levels that are near $70. This has added to the inflation rate, pushing down real wage growth, and actually leading to short periods of negative growth.

The issue here is not that nominal wages have stopped growing, it is just that changes in world energy prices had led to a temporary drag on real wage growth, just as they provided a temporary boost to real wage growth in 2015.

This story is worth pointing out in the context of recent comments about real wages stagnating. This is true, but the cause is the rise in world oil prices, not something bad that happened to the labor market.

The folks who want to blame Trump for stagnant wages are off the mark, unless they think he is responsible for the rise in world oil prices. If the argument is that the tax cuts have not led to more rapid wage growth, this is true, but we really should not have expected to see much effect just yet. The tax cut story is that it will lead to more investment, which will in turn lead to higher productivity. Higher productivity will in turn lead to higher wages.

The key in this story is investment. And so far, there is nothing to show here, indicating that the tax cuts are only paying off for shareholders, not workers.

Anyhow, the point is that it’s a bit silly to blame slower real wage growth on Trump. I’m not about to become a Trumper, but the guy does 1000 things every day for which he should be chased out of office. Let’s focus on the real items, we don’t have to make stuff up.

This column originally appeared on Dean Baker’s blog: Beat the Press.