US Core CPI, Excluding Shelter, Fell 0.1 Percent In April – Analysis

By Dean Baker

The April Consumer Price Index (CPI) shows no evidence of accelerating inflation, in spite of the 18-year low in unemployment. The overall CPI rose 0.2 percent for the month, while the core index rose just 0.1 percent. Over the last year, the two indexes are up 2.5 percent and 2.1 percent, respectively.

Even this modest inflation is largely attributable to rising housing costs. The shelter index was up 0.3 percent in the month and was up 3.4 percent over the last year. A core index that also excludes shelter actually fell by 0.1 percent in April and is up by just 1.2 percent over the last year.

There are two important points about how housing costs drive inflation. First, this is not a classic wage–price spiral type of inflation. While the overall inflation rates remain low (even including shelter costs), insofar as shelter is a leading factor in pushing them higher, the rise in shelter costs is not due in any important way to rising wages and construction costs.

Second, virtually all analysts agree that the problem of higher housing costs is overwhelmingly due to limited land and building restrictions in desirable metropolitan areas. These factors are not going to be changed by the Federal Reserve Board’s interest rate policies. While the Fed views higher interest rates as a tool against inflation, the impact is likely to go the wrong way in the case of rents. By making it more expensive to build, higher rates are likely to worsen housing shortages in the most desirable markets.

The other point is that because the rapid rise in housing costs is primarily due to a limited number of metropolitan areas with overheated markets, there are large differences in the rate of inflation seen in different areas. For example, while the national CPI rose 2.5 percent over the last year, it rose just 1.9 percent in the New York metropolitan area and 1.4 percent in the Philadelphia metro area. By contrast, it rose 3.5 percent in the Miami metro area and 4.0 percent in the Los Angeles area. A worker seeing a 2.6 percent increase in hourly pay over the last year is coming out ahead in New York and Philadelphia, but falling badly behind in Miami and Los Angeles.

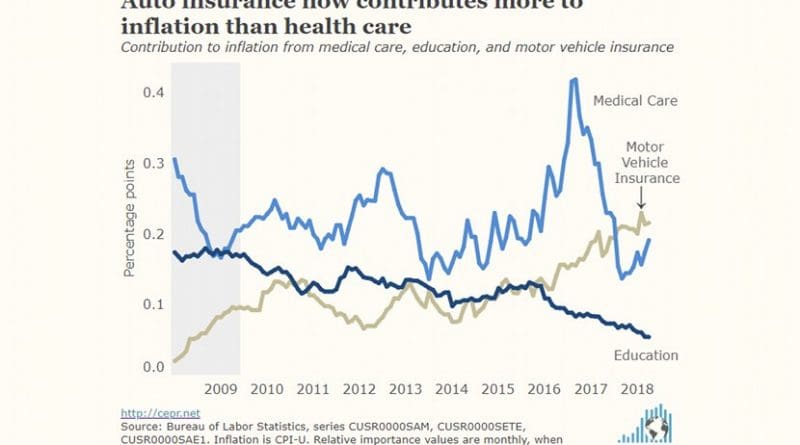

Outside of shelter, there is really no evidence of inflationary pressures elsewhere in the core. Inflation in the health care and insurance sectors, traditional problem areas, remains under control. The medical care index rose just 0.1 percent in April and is up just 2.2 percent over the last year. Education costs also rose 0.2 percent in April and up 1.8 percent over the last year.

Even motor vehicle insurance costs, which have surpassed both education and medical care as a contributor to inflation, may be coming under control. They fell by 0.2 percent in April, although they are still up by 9.0 percent over the last year.

Inflation in other major components is negligible or negative. New vehicle prices fell 0.5 percent in April, while used car and truck prices fell 1.6 percent. For the year, prices are down in these categories by 1.6 percent and 0.9 percent, respectively. Apparel prices rose by 0.3 percent, bringing the increase over the last year to 0.8 percent. Airline fares fell 2.7 percent in April and are down 6.9 percent over the last year.

Two areas where costs are rising are legal services — flat in April, but up 4.3 percent for the last year — and financial services, the price of which rose 4.6 percent last month, bringing the increase for the last year to 6.5 percent. Perhaps this is attributable to the policies pursued by the new leadership at the Consumer Financial Protection Bureau.

The overall picture in April remains the same as in prior months. The only place where there is notable evidence of inflationary pressures is in housing. Outside of housing, inflation in the core index is virtually nonexistent. Energy prices, which have risen 7.9 percent over the last year, are the only other potential problem on the horizon.