Iran Energy Profile: Holds Some Of World’s Largest Deposits Of Proved Oil And Natural Gas Reserves – Analysis

By EIA

Iran holds some of the world’s largest deposits of proved oil and natural gas reserves, ranking as the world’s fourth-largest and second-largest reserve holder of oil and natural gas, respectively. Iran also ranks among the world’s top 10 oil producers and top 5 natural gas producers. Iran produced almost 4.7 million barrels per day (b/d) of petroleum and other liquids in 2017 and an estimated 7.2 trillion cubic feet (Tcf) of dry natural gas in 2017.[1]

The Strait of Hormuz, off the southeastern coast of Iran, is an important route for oil exports from Iran and other Persian Gulf countries. At its narrowest point, the Strait of Hormuz is 21 miles wide, yet an estimated 18.5 million b/d of crude oil and refined products flowed through it in 2016 (nearly 30% of all seaborne-traded oil and almost 20% of total oil produced globally). Liquefied natural gas (LNG) volumes also flow through the Strait of Hormuz. Approximately 3.7 Tcf of LNG was transported from Qatar via the Strait of Hormuz in 2016, accounting for more than 30% of global LNG trade.

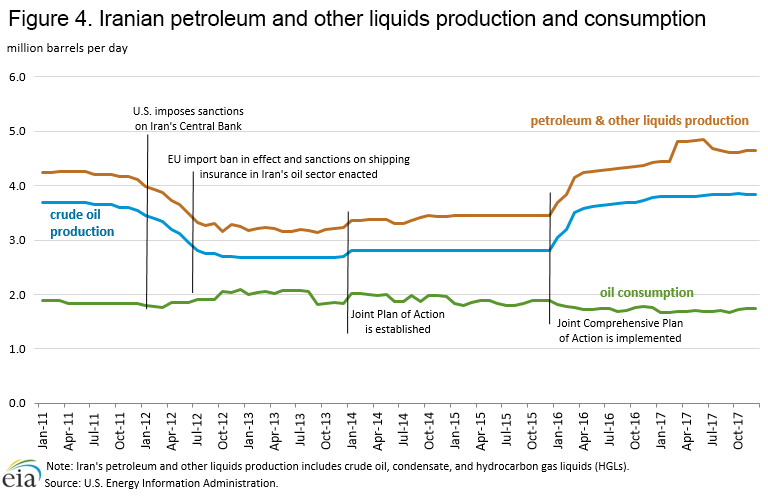

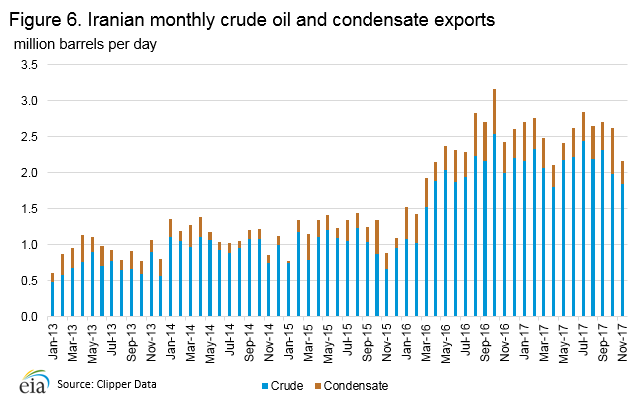

Despite Iran’s abundant reserves, crude oil production stagnated and even declined between 2012 and 2016 as nuclear-related international sanctions that targeted Iran’s oil exports hindered progress across Iran’s energy sector, which affected upstream investment in both oil and natural gas projects. At the end of 2011, the United States and the European Union (EU) imposed sanctions as a result of Iran’s nuclear activities, which went into effect in mid-2012. These sanctions targeted the Iranian energy sector and impeded Iran’s ability to sell oil, resulting in a near 1.0-million b/d drop in crude oil and condensate exports in 2012 compared with the previous year. Since the oil sector and banking sanctions were lifted, as outlined in the Joint Comprehensive Plan of Action (JCPOA) in January 2016, Iranian crude oil and condensate production and exports have risen to pre-2012 levels.

Iran’s oil and natural gas export revenue was $33.6 billion in Fiscal Year (FY) 2015-2016, according to the International Monetary Fund (IMF), having decreased nearly 40% from $55.4 billion in FY 2014-2015. EIA estimates that Iran’s oil net export revenues totaled $36 billion in 2016. The sudden drop was the result of continued depressed export volumes and lower crude oil prices, which combined resulted in low total export revenue. In FY 2016-2017, oil and natural gas export revenue was estimated to have risen to $57.4 billion as crude oil export volumes rose following the implementation of the JCPOA.[2] Most of the export revenues come from crude oil and condensate exports because Iran exports only a small volume of natural gas. Iran consumes most of the natural gas it produces.

Iranian development of its natural gas resources continues and has picked up pace following the implementation of the JCPOA. However, production growth had been slower than expected because sanctions targeting Iran’s nuclear activities between 2012 and 2016 also affected natural gas development as a result of lack of foreign investment and technology. Iran’s natural gas activities are centered on the South Pars natural gas field, located offshore in the Persian Gulf, which holds roughly 40% of Iran’s proved natural gas reserves.[3] The field is being developed mainly by Iranian companies.

Total primary energy consumption

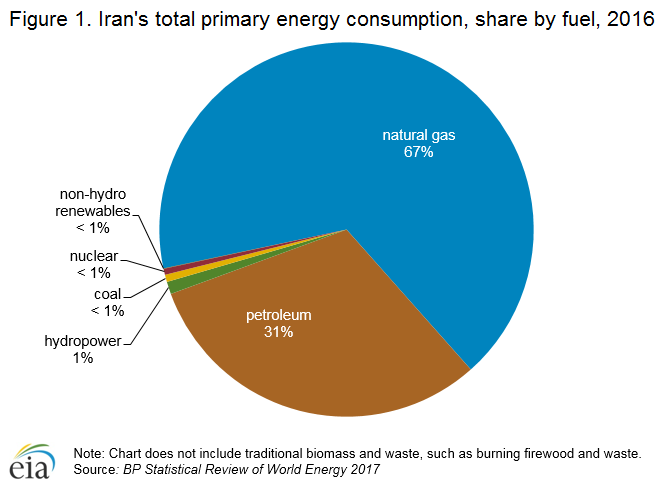

Iran consumed more than 270 million tons oil equivalent of primary energy in 2016.[4] Natural gas and oil accounted for almost all (98%) of Iran’s total primary energy consumption, with marginal contributions from hydropower, coal, nuclear, and non-hydro power renewables. Iran’s primary energy consumption has grown rapidly over the past decade and continued to grow even when economic growth was depressed and when nuclear-related sanctions were in place. In fact, between 2006 and 2016, Iran’s primary energy consumption expanded by about 40%. To better control domestic demand growth and reduce the budgetary exposure to high subsidy costs, the Iranian government implemented energy subsidy reform, which resulted in increasing domestic prices for domestic petroleum, natural gas, and electricity between 2010 and 2014.

Management of oil and natural gas sectors

The state-owned National Iranian Oil Company is responsible for all upstream oil and natural gas projects. The Iranian constitution prohibits foreign or private ownership of natural resources. However, international oil companies can now participate in the exploration and development phases through the Iranian petroleum contract, a relatively new model for its upstream oil and natural gas fiscal regime.

The Supreme Energy Council, which was established in July 2001 and is chaired by the president of Iran oversees the energy sector. The council is composed of the Ministers of Petroleum, Economy, Trade, Agriculture, and Mines and Industry, among others. Under the supervision of the Ministry of Petroleum, state-owned companies dominate the activities in the oil and natural gas upstream and downstream sectors, along with Iran’s petrochemical industry. The three key state-owned enterprises are the National Iranian Oil Company (NIOC), the National Iranian Gas Company (NIGC), National Oil Refining and Distribution Company (NIORDC), and the National Petrochemical Company (NPC).

| Company | Responsibility |

|---|---|

| National Iranian Oil Company (NIOC) | NIOC controls oil and natural gas upstream activities through its eleven subsidiaries. |

| National Iranian Gas Company (NIGC) | NIGC controls natural gas downstream activities. The company’s objective is to process, deliver, and distribute natural gas for domestic use. NIGC operates through several subsidiaries. |

| National Iranian Oil Refining and Distribution Company (NIORDC) | NIORDC is responsible for all refining and distribution activities related to crude oil and petroleum products, including construction of refining and storage facilities, oil pipelines, and operations of gasoline stations. NIORDC conducts these operations through its four major subsidiaries. |

| National Petrochemical Company (NPC) | NPC manages Iran’s petrochemical industry, including operations of several petrochemical complexes, through its subsidiaries. |

| Source: U.S. Energy Information Administration, Facts Global Energy, Arab Oil & Gas Directory, and NIOC | |

Foreign investment

In an effort to attract much-needed foreign investment and technology in its oil and natural gas sector, the Iranian government implemented the Iranian petroleum contract that allows international oil companies to participate in all phases of upstream projects. The new fiscal regime was approved in 2016 and offers more attractive terms than the previously available buyback contracts.

The Iranian constitution prohibits foreign or private ownership of natural resources, and prior to late 2016, the government only permitted buyback contracts, which allowed international oil companies (IOCs) to enter exploration and development contracts through an Iranian subsidiary. A buyback contract is similar to a service contract and requires the contractor (or an IOC) to invest its own capital and expertise to develop oil and natural gas fields. After the field was developed and production started, the project’s operatorship reverted to NIOC or to the relevant subsidiary. The IOC did not get equity rights to the oil and natural gas fields. NIOC used revenue from the sale of oil and natural gas to pay back the capital costs to the IOC. The annual repayment rates to the IOC were based on a predetermined percentage of the field’s production and rate of return. According to Facts Global Energy (FGE), the rate of return on buyback contracts ranged between 12% and 17%, and the payback period was between five and seven years. [5]

In late 2016, Iranian parliament approved and the government implemented the new oil contract model called the Iranian (or Integrated) Petroleum Contract (IPC). The main purpose of this new framework is to attract foreign investment and technology to spur development of upstream oil and natural gas projects. The new contract terms are a hybrid of those in buyback contracts and production sharing agreements (PSA). The IPC encompasses exploration, development, and production phases, along with the possibility to extend into enhanced oil recovery (EOR) phases. The contract term is set at a maximum of 20 years, with the possibility to extend the term by 5 years for EOR projects. The IPC retains the previous local content requirement of 51% of the value of work, and the foreign investor is required to submit plans for knowledge and technology development transfer as part of its annual operational financial plan.[6]

International sanctions have affected Iran’s energy sector by limiting the foreign investment, technology, and expertise needed to expand capacity at oil and natural gas fields and to reverse declines at mature oil fields. Iran has had to depend mainly on local companies to develop oil and natural gas fields in recent years. Although the IPC was intended to reverse this trend, Iran has had limited success in attracting IOCs to its oil and natural gas upstream.

Thus far, there were only two finalized contract under the IPC. The first one was the July 2017 agreement with French major Total and China National Petroleum Corporation (CNPC) to develop Phase 11 of the South Pars field. The development will not produce any crude oil but is expected to produce about 80,000 b/d of condensate.[7] More recently, Russian state-controlled Zarubezhneft signed oil development contracts under the IPC, with reportedly Rosneft, Lukoil, Gazprom Neft, and Tatneft all considering upstream agreements with Iran. The latest agreement was signed in mid-March 2018 between Zarubezhneft, NIOC, and Dana Energy to develop West Paydar and Abadan onshore fields near Iraq. The ten-year contract calls for improved recovery rates and increased production from the fields to 48,000 b/d.

Oil sector

Reserves

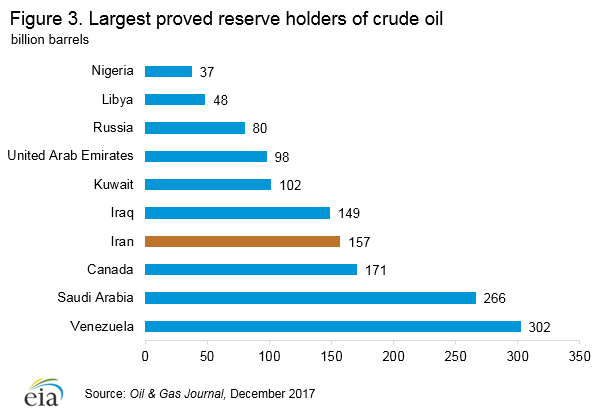

Iran holds almost 10% of the world’s crude oil reserves and about 13% of OPEC reserves. More than 70% of Iran’s crude oil reserves are located onshore, with the remainder mostly located offshore in the Persian Gulf.

Iran holds almost 10% of the world’s crude oil reserves and about 13% of OPEC reserves. More than 70% of Iran’s crude oil reserves are located onshore, with the remainder mostly located offshore in the Persian Gulf.

According to the Oil & Gas Journal, as of January 2018, Iran has an estimated 157 billion barrels of proved crude oil reserves, representing almost 10% of the world’s crude oil reserves and about 13% of reserves held by the Organization of the Petroleum Exporting Countries (OPEC).[8] Most Iranian reserves are located onshore (about 71%), with the Khuzestan Basin containing roughly 80% of total onshore reserves.[9] Iran also has 0.5 billion barrels of proved and probable reserves in the Caspian Sea, but to date very limited upstream activity has occurred in Iran’s portion of the Caspian Sea. Iran also shares a number of onshore and offshore fields with neighboring countries, including Iraq, Qatar, Kuwait, and Saudi Arabia.

Exploration and production

Iran produced 4.7 million b/d of petroleum and other liquids in 2017, of which 3.8 million b/d was crude oil and the remainder was condensate and hydrocarbon gas liquids. Iran’s crude oil production has recovered since the implementation of the JCPOA.

Iran is one of the founding members of the Organization of the Petroleum Exporting Countries (OPEC), which was established in 1960. Since the 1970s, Iran’s oil production has varied greatly. Iran’s production averaged more than 5.5 million b/d of oil in 1976 and 1977, with production topping 6.0 million b/d for most of the period. Since the 1979 revolution, however, a combination of war, limited investment, sanctions, and a high rate of natural decline in production of Iran’s mature oil fields has prevented a return to those production levels.

Sanctions related to Iran’s nuclear activities imposed in late 2011 and mid-2012 led to a precipitous decrease in Iranian production in 2013, with production falling to 2.7 million b/d. These sanctions targeted Iran’s petroleum exports and imports, prohibited large-scale investment in the country’s oil and natural gas sector, and cut off Iran’s access to European and U.S. sources for financial transactions. Further sanctions were implemented against institutions targeting the Central Bank of Iran, while the EU imposed an embargo on Iranian oil and banned European Protection and Indemnity Clubs (P&I Clubs) from providing Iranian oil tankers with insurance and reinsurance. Before this round of sanctions, Iran was the second-largest producer in OPEC, but the country has since been overtaken by Iraq.

Sanctions related to Iran’s nuclear activities imposed in late 2011 and mid-2012 led to a precipitous decrease in Iranian production in 2013, with production falling to 2.7 million b/d. These sanctions targeted Iran’s petroleum exports and imports, prohibited large-scale investment in the country’s oil and natural gas sector, and cut off Iran’s access to European and U.S. sources for financial transactions. Further sanctions were implemented against institutions targeting the Central Bank of Iran, while the EU imposed an embargo on Iranian oil and banned European Protection and Indemnity Clubs (P&I Clubs) from providing Iranian oil tankers with insurance and reinsurance. Before this round of sanctions, Iran was the second-largest producer in OPEC, but the country has since been overtaken by Iraq.

Following the implementation of the JCPOA in January 2016 and Iran’s renewed ability to export oil to Europe, Iranian exports immediately rose, and, as a result, Iranian crude oil production once again exceeded pre-2012 levels. In 2017, Iran produced nearly 4.7 million b/d of petroleum and other liquids, of which 3.8 million b/d was crude oil and the remainder was condensate and hydrocarbon gas liquids (HGL). Iranian total liquids production rose in 2017 relative to 2016 by 0.5 million b/d, supported by continued increases in exports.

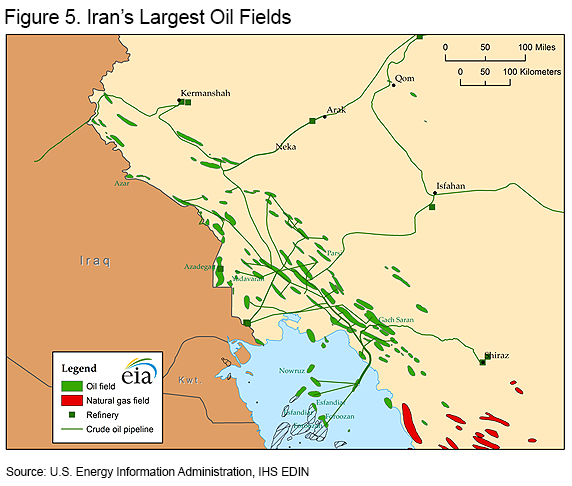

Crude oil streams and oil fieldsMost of Iran’s crude oil production comes from the country’s southwestern onshore fields, where Iran Heavy and Iran Light grades are produced. This area accounts for about 85% of Iran’s total crude oil production capacity.[10] Iran Heavy is a medium-heavy, high-sulfur crude oil (29.3° API, 2.29% sulfur) and is sourced from some of Iran’s largest oil fields, including the Gachasaran, Marun, Ahwaz, and Bangestan. Iran Light is similar in quality to Arab Light, with 33° API and 1.58% sulfur content. Iran Light is produced at several onshore fields in the Khuzestan province, but two-thirds of the Iran Light volume comes from three fields, Ahwaz, Karanj, and Aghajari.[11] All of these fields are decades old and have large decline rates. Sustaining production capacity will require EOR techniques, including the injection of natural gas into oil reservoirs to boost recovery rates.

In addition to its Heavy and Light grades, Iran also produces Azadegan, Doroud, Foroozan, Lavan Blend, Soroush/Norouz, and Sirri. Azadegan is a relatively new stream, with production about totaling 0.2 million b/d in 2017 from the Azadegan oil field (called Majnoon on the Iraqi side). Azadegan’s plateau production is expected to reach 0.65 million b/d.

In tandem with the development of the giant South Pars natural gas field, Iran has also increased condensate output, which averaged 0.6 million b/d in 2017. Additional phases of the South Pars development will result in increasing growth in condensate output in the coming years.

Upstream projectsIran’s plans to expand its production capacity and crude oil output in the medium term are ambitious and will require international funding, expertise, and technology. The plans are centered on the development of the Azadegan, Yadavaran, Yaran, and South Pars oil layer, as well as a number of other fields, including the Caspian Sea resources. NIOC plans to sign new upstream contracts under the IPC scheme in the second half of 2018 and in 2019 for additional phases that will increase production of Azadegan, Yadavaran, Yaran, and South Pars oil layer. Azadegan produced less than 0.2 million b/d in 2017 and is forecast to reach plateau production of 0.75 million b/d (including both the North and South Azadegan projects).

Yadaravan is also producing crude oil, with production reaching 0.1 million b/d in the fourth quarter of 2017. Additional development will increase output to more than 0.3 million b/d when it reaches plateau production.

| Project | Developer | Plateau output (000 b/d) |

Est. plateau year |

|---|---|---|---|

| Azadegan (North and South) | CNPC and NIOC | 750 | post 2020 |

| Yadavaran phase 2 | Sinopec | 95 | 2019-20 |

| Yadavaran phase 3 | Sinopec | 120 | post 2020 |

| South Yaran | NIOC | 100 | 2018 |

| South Pars Oil Layer | NIOC | 150 | 2018 |

| Crude oil production at the Yadavaran, South Azadegan, and South Pars (oil layer) fields is currently below their plateau levels. CNPC is China National Petroleum Corporation. Sinopec is China Petroleum & Chemical Corporation. Source: Facts Global Energy, Energy Intelligence |

|||

Crude oil and condensate exports

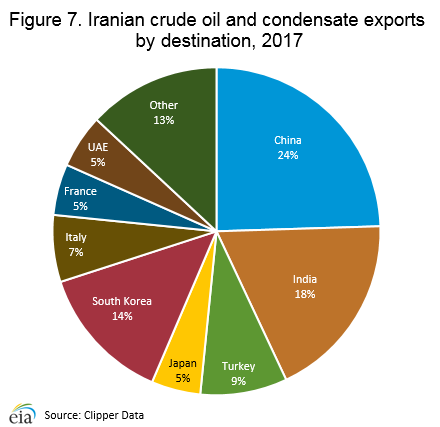

Iran’s exports of crude oil and condensate increased sharply in 2016 and averaged more than 2.5 million b/d in 2017. The largest buyers of Iranian crude oil and condensates in 2017 were China, India, Turkey, and South Korea. Iran’s main oil customers have not changed significantly since the implementation of the JCPOA.

According to EIA estimates based on tanker-tracking data reported by Clipper Data, Iran’s crude oil and condensate exports averaged 2.5 million b/d in 2017, about 0.2 million b/d higher than the 2016 average. China and India accounted for about 43% of all Iranian exports in 2017, and Turkey and South Korea took substantial volumes during the year.

Iran resumed its crude oil exports to Europe in 2016 following the implementation of the JCPOA. Before the 2011 and 2012 sanctions, European refiners had been purchasing and processing Iranian crude oil, but they stopped their imports in early 2012. In 2016 and 2017, a number of European countries resumed their purchases of Iranian oil, including Croatia, France, Greece, Italy, Malta, Netherlands, Poland, and Spain.

Iran resumed its crude oil exports to Europe in 2016 following the implementation of the JCPOA. Before the 2011 and 2012 sanctions, European refiners had been purchasing and processing Iranian crude oil, but they stopped their imports in early 2012. In 2016 and 2017, a number of European countries resumed their purchases of Iranian oil, including Croatia, France, Greece, Italy, Malta, Netherlands, Poland, and Spain.

In addition to crude oil and condensate, Iran also exports petroleum products. According to Facts Global Energy (FGE), Iran has a supply surplus for all petroleum products except gasoline. Iran’s exports of petroleum products averaged 507,000 b/d in 2017, with LPG and fuel oil accounting for about 83% of total petroleum product exports. Iran’s petroleum product exports declined in 2017 compared with exports of 587,000 b/d (including small volumes of gasoline exports) in 2016. Most of the petroleum product exports went to Asia.[12]

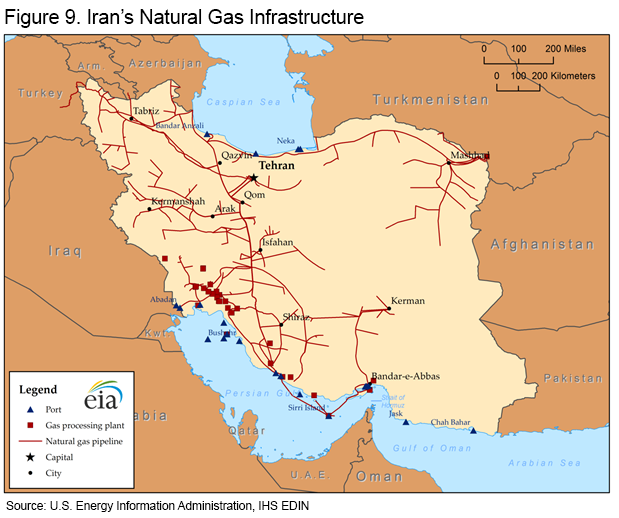

Oil terminals The terminals at Kharg, Lavan, and Sirri Islands, located in the Persian Gulf, handle almost all of Iran’s crude oil exports. Iran also has two small crude oil terminals at Cyrus and Bahregansar, one terminal along the Caspian Sea, and other terminals that handle mostly refined product exports and imports. Condensate from the South Pars natural gas field is exported from the Assaluyeh terminal.

The terminals at Kharg, Lavan, and Sirri Islands, located in the Persian Gulf, handle almost all of Iran’s crude oil exports. Iran also has two small crude oil terminals at Cyrus and Bahregansar, one terminal along the Caspian Sea, and other terminals that handle mostly refined product exports and imports. Condensate from the South Pars natural gas field is exported from the Assaluyeh terminal.

Kharg Island, the largest export terminal in Iran, is located in the northeastern part of the Persian Gulf. Most of Iran’s crude oil exports are sent via Kharg, which includes a main terminal and a four-berth sea island (three of which are operational). The terminal processes all onshore production (the Iranian Heavy and Iranian Light Blends) and offshore production from the Foroozan field (the Foroozan Blend). NIOC has reportedly upgraded the terminal to handle a maximum capacity of 7 million b/d.[13]

Lavan Island mostly handles exports of the Lavan Blend sourced from offshore fields. Lavan is Iran’s highest-quality export grade (35.2° API, 1.59% sulfur) and one of Iran’s smallest streams, with production volume of about 115,000 b/d in 2017. Lavan’s storage capacity is 5.5 million barrels and has a loading capacity of 200,000 b/d.[14]

Sirri Island serves as a loading port for the medium-gravity, high-sulfur Sirri Blend that is produced in the offshore fields. Its storage capacity is 4.5 million barrels.[15]

Neka is Iran’s Caspian Sea port, which was built in 2003 to receive crude oil imports from the Caspian-region producers under swap agreements. The port’s loading capacity is about 150,000 b/d, but trade press reporting suggests that only about 50,000 b/d of oil flows through Neka. The terminal is used to facilitate swap agreements with Azerbaijan, Kazakhstan, and Turkmenistan. Under these agreements, Iran receives crude oil at its Caspian Sea port of Neka, which is processed in the Tehran and Tabriz refineries. In return, Iran exports the same amount of crude oil from Kharg Island.[16]

Assaluyeh terminal is where Iran’s South Pars condensate is loaded for exports, mainly to China, India, Japan, South Korea, and the United Arab Emirates. In addition to condensate, the port also loads LPG, sulfur, and petrochemical products.[17]

The export terminals Bandar Mahshahr and Abadan (also known as Bandar Imam Khomeini) near the Abadan refinery are used to export refined product from the Abadan refinery. Bandar Abbas, located near the northern end of the Strait of Hormuz, is Iran’s main fuel oil export terminal.

Consumption and downstream

Iran is the second-largest oil-consuming country in the Middle East after Saudi Arabia. While Iran has become self-sufficient in meeting domestic demand for most petroleum products, it continues to rely on some gasoline import volumes. Current plans include construction of new refineries and upgrades to existing refineries to increase gasoline production.

Iran is the second-largest oil-consuming country in the Middle East after Saudi Arabia. While Iran has become self-sufficient in meeting domestic demand for most petroleum products, it continues to rely on some gasoline import volumes. Current plans include construction of new refineries and upgrades to existing refineries to increase gasoline production.

Iran is the second-largest oil-consuming country in the Middle East, after Saudi Arabia. Iranian domestic oil consumption is mainly diesel, gasoline, and fuel oil. Oil consumption averaged 1.7 million b/d in 2017, falling slightly compared with the 2016 level. Almost all of Iran’s product consumption was met with domestically refined product, but Iran continues to rely on relatively small volumes of gasoline imports. In 2017, Iran’s only petroleum product import was an estimated 80,000 b/d of gasoline, which accounted for roughly 16% of Iran’s gasoline consumption during the year.[18]

In the past, Iran had limited domestic oil refining capacity and was dependent on imports of refined products, especially gasoline, to meet domestic demand. In response to international sanctions and the resulting difficulty in purchasing refined products, Iran expanded its domestic refining capacity. As of December 2017, Iran’s total crude oil distillation capacity was slightly more than 2.2 million b/d, according to FGE.[19]

| Refinery | Crude distillation capacity (thousand b/d) |

|---|---|

| Abadan | 400 |

| Isfahan | 375 |

| Bandar Abbas | 330 |

| Tehran | 250 |

| Arak | 250 |

| Borzuyeh | 120 |

| Tabriz | 110 |

| Shiraz | 60 |

| Lavan | 60 |

| BooAli Sina | 34 |

| Kermanshah | 22 |

| Aras 2 | 10 |

| Booshehr | 10 |

| Aras 1 | 5 |

| Yazd | 3 |

| Total | 2,159 |

| Source: Facts Global Energy, December 2017 | |

PipelinesIran has an extensive domestic oil pipeline network including 19 crude oil and product pipelines ranging in length from 93 miles to 525 miles. Iran’s longest pipeline is the product line that runs between Rey and Mashahad. It transports oil between Ahavaz and Rey and supplies feedstock to the Tehran, Arak, and Tabriz refineries. In addition, a new 36-inch condensate pipeline (Assaluyeh-Bandar Abbas) ships feedstock from Assaluyeh to the new PGS refinery.[20]

Iran’s future plans include construction of three additional petroleum product pipelines, including a new line that will transport gasoline throughout Iran from the Persian Gulf Star (PGS) refinery.

Natural gas sector

Reserves

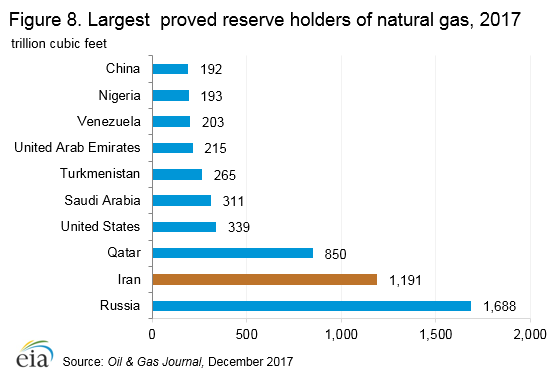

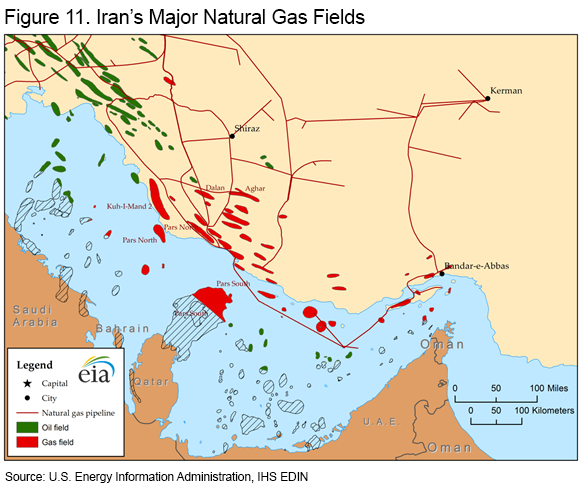

Iran is the second-largest proved natural gas reserve holder in the world behind Russia. Iran holds 17% of the world’s proved natural gas reserves and more than one-third of OPEC’s reserves. Iran’s largest natural gas field, South Pars, is estimated to hold almost 40% of Iran’s natural gas reserves.

Iran is the second-largest proved natural gas reserve holder in the world behind Russia. Iran holds 17% of the world’s proved natural gas reserves and more than one-third of OPEC’s reserves. Iran’s largest natural gas field, South Pars, is estimated to hold almost 40% of Iran’s natural gas reserves.

According to Oil & Gas Journal, as of December 2017, Iran’s estimated proved natural gas reserves were 1,191 trillion cubic feet (Tcf), second only to Russia. Iran holds 17% of the world’s proved natural gas reserves and more than one-third of OPEC’s reserves.[21] Iran has a high success rate of natural gas exploration, which is estimated at 79% compared to the world average success rate of 30% to 35%, according to FGE.[22] Finding new natural gas reserves in Iran is not a high priority because the country contains large amounts of undeveloped known reserves.

Iran’s largest natural gas field is South Pars, a non-associated gas field located offshore in the Persian Gulf. South Pars is part of a larger gas structure that straddles the territorial water of Iran and Qatar called the North Field in Qatar. South Pars reserves account for almost 40% of Iran’s total natural gas reserves.[23] Other major natural gas fields in Iran include Kish, North Pars, Sardar-e-Jangal, Forouz-B, Aghar, Golshan, and Kangan. These fields and others also hold large amounts of condensate reserves. About 80% of Iran’s natural gas reserves are non-associated, according to FGE.

Production

Iran is the world’s third-largest dry natural gas producer after the United States and Russia. Iran’s natural gas prospects have improved with the commencement of production in the South Pars field, with additional phases expected to come online in the coming years.

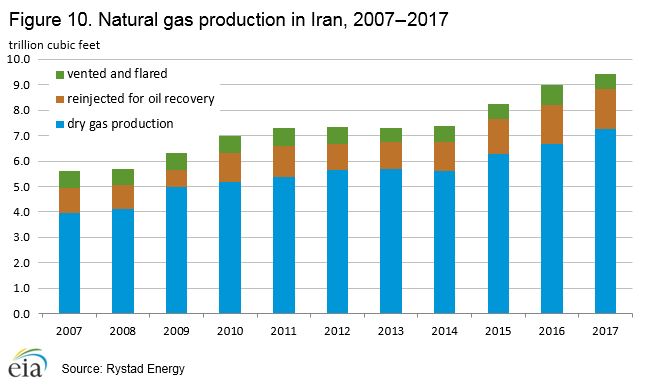

Iran’s gross natural gas production totaled nearly 9.5 Tcf in 2017, of which 7.3 Tcf was dry natural gas, rising almost 9% compared with 2016, according to Rystad Energy. Roughly 1.6 Tcf of the total was reinjected into oil wells to enhance oil recovery,[24] which plays a central role in Iran’s oil production. Iran’s use of natural gas in enhanced oil recovery (EOR) has increased 56% between 2007 and 2017. As natural gas production increases, the use of natural gas for EOR is expected to continue to rise. Use of EOR will be key to stemming declines in Iran’s brownfields, which have relatively high natural decline rates.

In addition to the natural gas used for EOR, Iran vented and/or flared approximately 0.6 Tcf of gas in 2017.[25] Natural gas is flared when no infrastructure exists to capture and transport gas associated with oil production. Iran was the second-largest source country of flared natural gas in 2017, behind only Iraq.

In addition to the natural gas used for EOR, Iran vented and/or flared approximately 0.6 Tcf of gas in 2017.[25] Natural gas is flared when no infrastructure exists to capture and transport gas associated with oil production. Iran was the second-largest source country of flared natural gas in 2017, behind only Iraq.

With 7.3 Tcf of dry natural gas produced in 2017, Iran was the world’s third-largest producer after the United States and Russia. South Pars is Iran’s largest field by production volume, with approximately 55% of Iran’s production originating from this field. FGE projects that when fully developed, South Pars volumes will account for more than 70% of Iran’s total production. In addition to South Pars, other major sources of Iran’s natural gas production include the Tabnak, Nar, Kangan, Homan, and Shanoul fields.

Most of the natural gas produced is consumed domestically, with Iran’s consumption averaging at an estimated 6.9 Tcf in 2017.[26] In 2016 (the latest available data), Iran was the world’s fourth-largest consumer of natural gas after the United States, Russia, and China.[27] The largest share of natural gas use domestically in 2016 was in the electric power sector (32%), followed by the residential and commercial sector (29%) and the industrial sector (27%). Natural gas use for electric power generation has grown in recent years as Iran replaced crude oil and fuel oil with natural gas for electricity generation.[28]

South Pars Natural Gas Field

Natural gas production from South Pars is critical to meet increasing domestic consumption and Iran’s plans and obligations for exports. The development plan includes 24 phases, of which 18 are already operational.

The most significant energy development project in Iran, the South Pars field, accounted for about 55% of Iran’s natural gas production in 2016. It holds almost 40% of Iran’s total proved natural gas reserves.[29] Discovered in 1990 and located 62 miles offshore in the Persian Gulf, South Pars has a 24-phase development plan, with 18 phases already operational, although not all of these phases have reached maximum production capacity. Currently, five phases are under development and one phase just began its development. Each of the 24 phases has a combination of natural gas with condensate and/or hydrocarbon gas liquids (HGL). The project is managed by Pars Oil & Gas Company (POGC), a subsidiary of NIOC. According to FGE, development of the South Pars gas field has so far required $71 billion in investment, with an additional $20 billion needed to complete the remaining phases.

| Phase | Natural gas capacity (Bcf/d) |

Condensate capacity (b/d) |

Start-up year |

|---|---|---|---|

| 1 | 1 | 40,000 | 2004 |

| 2 | 2 | 80,000 | 2003 |

| 3 | |||

| 4 | 2 | 80,000 | 2005 |

| 5 | |||

| 6 | 3.7 | 120,000 | 2008 |

| 7 | |||

| 8 | |||

| 9 | 2 | 80,000 | 2019 |

| 10 | |||

| 11 | 2 | 80,000 | 2022 |

| 12 | 3 | 110,000 | 2014 |

| 13 | 2 | 75,000 | 2018 |

| 14 | 2 | 75,000 | 2018 |

| 15 | 2 | 75,000 | 2015 |

| 16 | |||

| 17 | 2 | 75,000 | 2016 |

| 18 | |||

| 19 | 2 | 75,000 | 2017 |

| 20 | 2 | 75,000 | 2017 |

| 21 | |||

| 22 | 2 | 77,000 | 2018 |

| 23 | |||

| 24 | |||

| Total | 30 | 1,117,000 | |

| Source: Facts Global Energy, December 2017 | |||

Imports and exports

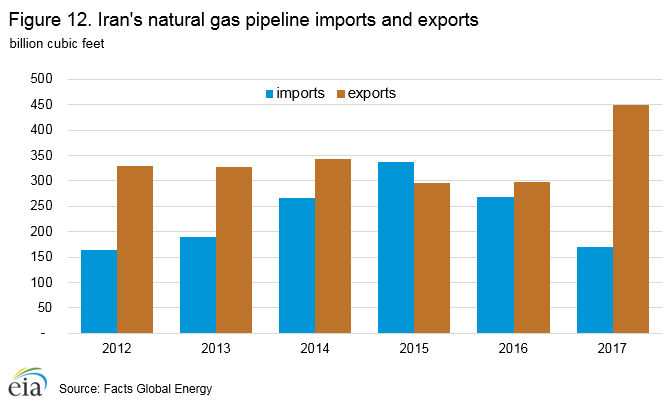

Iran trades relatively small volumes of natural gas regionally via pipelines. In 2017, all of Iran’s imports came from Turkmenistan, and more than 73% of Iran’s exports went to Turkey. Iran does not have the infrastructure in place to export or import liquefied natural gas (LNG).

Iran accounts for about 1% of global natural gas pipeline trade and is not yet a significant natural gas exporter. In 2017, Iran exported about 450 Bcf and imported 170 Bcf of natural gas via pipelines. Iran relies on imports particularly during winter months when residential space-heating demand peaks during colder weather. Iran does not have the infrastructure to export or import liquefied natural gas (LNG). Although Iran’s aspirations to build a liquefaction facility date back to the 1970s, the country has yet to build one. In past years, the NIOC started construction projects to build an LNG export plant, but most of the work has been halted. The lack of technology and foreign investment, stemming from decades-old international sanctions, made obtaining financing and purchasing necessary technology impossible. Inability to construct a large-scale LNG project has led to a change in strategy. Iran is now working on plans to construct small- and medium-sized LNG plants, including the Kangan LNG project, which would have 2 million tons per year (mmtpa) of liquefaction capacity, and the acquisition of a Caribbean floating LNG (FLNG) terminal. Purchase of the Caribbean FLNG is subject to U.S. sanctions.

Iran exports natural gas via pipeline to Turkey, Armenia, Azerbaijan, and Iraq, and it receives imports from Turkmenistan. Total exports averaged 1.2 Bcf per day of natural gas in 2017, of which about 73% was destined for Turkey. Iran’s natural gas exports to Armenia averaged 36 MMcf per day in 2017, for which Iran received electric power. Iran and Armenia trade natural gas and electric power via a 20-year swap contract. [30]

Iran began exporting natural gas to Iraq in June 2017 to fuel electric power plants near Baghdad, including the Al-Besmaya, Al-Quds, Al-Mansuriyah, and Al-Sadr stations. Annual natural gas exports to Iraq averaged 132 MMcf per day in 2017, but these volumes likely will rise as new gas-fired generation capacity comes online in Iraq. In addition to volumes to the Baghdad-area power plants, Iran also plans to ship natural gas to Basrah sometime in late 2018.

Iran’s imports of natural gas from Turkmenistan began in 1997 in response to lack of domestic infrastructure that would deliver natural gas from the south to the major consuming centers in northern Iran. Turkmenistan’s natural gas volumes filled this critical gap for years, especially during winter months. Iran’s imports of Turkmenistan’s natural gas peaked in 2015 at 0.9 Bcf per day, but they have since fallen to 0.5 Bcf per day. The decrease is partly the result of contractual disputes between Iran and Turkmenistan, which have at times resulted in a complete cessation of gas trade between the two countries. In January 2017, Turkmenistan halted gas exports to Iran over a reported non-payment for deliveries. In response, Iran built a pipeline between the city of Damghan and Neka in the north, reducing the need for Turkmen natural gas.

Iran’s imports of natural gas from Turkmenistan began in 1997 in response to lack of domestic infrastructure that would deliver natural gas from the south to the major consuming centers in northern Iran. Turkmenistan’s natural gas volumes filled this critical gap for years, especially during winter months. Iran’s imports of Turkmenistan’s natural gas peaked in 2015 at 0.9 Bcf per day, but they have since fallen to 0.5 Bcf per day. The decrease is partly the result of contractual disputes between Iran and Turkmenistan, which have at times resulted in a complete cessation of gas trade between the two countries. In January 2017, Turkmenistan halted gas exports to Iran over a reported non-payment for deliveries. In response, Iran built a pipeline between the city of Damghan and Neka in the north, reducing the need for Turkmen natural gas.

In the past, Iran received natural gas imports from Azerbaijan, but these imports ceased completely in October 2016. Iran and Azerbaijan traded natural gas under a gas swap contract, where Iran delivered natural gas to Azerbaijan’s Nakhchivan province, and in return, Iran received volumes from Azerbaijan via the Astara pipeline connections.

Proposed regional pipelinesIran has the potential to become an important natural gas supplier to its region and has established agreements with some of its neighboring countries to export natural gas via planned regional pipelines. However, several challenges related to Iran’s natural gas sector remain that may complicate volumes expected from these projects. Some of these challenges include: Iran’s growth in natural gas demand; Iran’s reliance on domestic natural gas to augment oil recovery by reinjecting it into oil wells; international sanctions that have hindered Iran’s access to technology and foreign investment; and some disagreements between Iran and potential buyers over natural gas prices.

Iran-Oman Pipeline: In March 2014, Iran and Oman agreed to form a joint venture that would deliver more than 1 Bcf per day of Iranian natural gas to Oman. Some of the Iranian gas volumes were planned to be exported as LNG from Oman. However, Oman’s development of its domestic natural gas resources, including tight gas development projects, has removed some of the need to import natural gas from Iran. The project would require a new pipeline (half of which would be subsea). Thus far, little progress has been made on its construction.

Iran-Pakistan Pipeline: Construction of one leg on the Iranian side of the pipeline is complete, but construction on the Pakistani side has been repeatedly delayed and has yet to start. In 2009, when the agreement was signed, Pakistan agreed to import 750 MMcf per day of natural gas, and the trade was supposed to commence in December 2014. Given the lack of progress on the Pakistani side, this project is not likely to materialize.[31]

Iran-UAE Gas Contract: Although the Iranian natural gas pipeline system is connected to the United Arab Emirates (UAE), Iran has so far refused to sell its natural gas to UAE. Iran and the UAE had signed an initial agreement to trade natural gas on a 20-year term, with Iran shipping natural gas produced at the Salman field to the city of Sharjah. However, after repeated cancellations, the contract has been referred for international arbitration.

Electricity sector

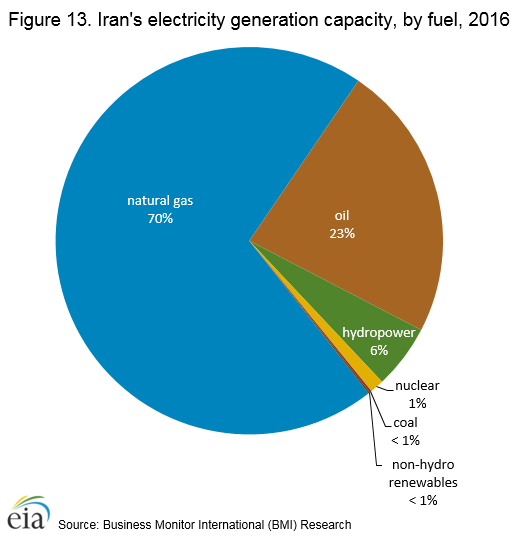

Natural gas is Iran’s primary fuel source to generate electricity, accounting for 70% of total generation in 2016. With the projected demand growth, Iran will have to expand generation capacity in the coming years. However, state control of electricity prices at depressed levels will make expanding capacity challenging.

In 2016, Iran generated almost 276 billion kilowatthours (kWh) of electricity, of which 93% was from fossil-fuel sources.[32] Natural gas is the largest source of fuel for electricity generation in Iran, accounting for 70% of total generation. Hydropower, nuclear, and nonhydro power renewables make up the remaining fuel sources used to generate electricity in Iran.

In 2016, Iran generated almost 276 billion kilowatthours (kWh) of electricity, of which 93% was from fossil-fuel sources.[32] Natural gas is the largest source of fuel for electricity generation in Iran, accounting for 70% of total generation. Hydropower, nuclear, and nonhydro power renewables make up the remaining fuel sources used to generate electricity in Iran.

The Iranian government has ambitious plans to expand electric power generation capacity, including natural gas-fired, renewable, and nuclear-fired facilities. Natural gas-fired generation likely will continue to play an important role in the electric power sector in Iran, and a number of natural gas-fired projects are in various stages of completions.

Iran’s ambitious plans also extend to nuclear-fired electric power generation. The government plans to construct additional units to the Bushehr facility, Iran’s only nuclear power plant. Currently, Bushehr has 1,000 MW of capacity. These two additional units would potentially commence operations in 2028 at the earliest. Bushehr became fully operational in late 2013.[33] Construction at the power plant originally began in the mid-1970s, but the project was repeatedly delayed by the Iranian Revolution, the Iran-Iraq war, and then by problems associated with the Russian consortium that was awarded the construction contract. The Iranian government took control of the plant’s management in late 2013, about the same time the nuclear power plant began producing commercial power.[34]

The Iranian government also plans to add 5 GW of new nonhydro power renewable capacity by 2020. According to Business Monitor International, Iran has adopted a feed-in tariff to offer a fixed rate for renewable projects in an effort to promote these types of projects.

Notes:

- Data presented in the text are the most recent available as of April 9, 2018.

- Data are EIA estimates unless otherwise noted.

Endnotes:

2. International Monetary Fund Article IV Consultation, Islamic Republic of Iran (February 2017), IMF Country Report No. 17/62, page 4.

3. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017 (December 2017), page 37.

4. BP Statistical Review of World Energy 2016 (June 2017)

5. Facts Global Energy, Iran’s Oil and Gas Annual Report 2014 (December 19, 2014), page 12.

6. Herbert Smith Freehills, The New Iranian Petroleum Contract (August 2016).

7. Middle East Economic Survey, “OPEC’s 2017 Output The Second Highest on Record; What Does 2018 Hold?” (January 12, 2018).

8. Oil & Gas Journal, Worldwide look at reserves and production (December 2017).

9. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017 (December 2017).

10. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017 (December 2017).

11. Energy Intelligence, World Crude Oil Data – Iran (accessed January 2018).

12. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017 (December 2017).

13. Energy Intelligence, World Crude Oil Data – Iran (accessed January 2018).

14. Energy Intelligence, World Crude Oil Data – Iran (accessed January 2018).

15. Energy Intelligence, World Crude Oil Data – Iran (accessed January 2018).

16. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017 (December 2017).

17. Energy Intelligence, World Crude Oil Data – Iran (accessed January 2018).

18. Facts Global Energy, Iran Oil and Gas Monthly January 2017, Data File (February 2018).

19. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017, (December 2017).

20. Ibid.

21. Oil & Gas Journal, Worldwide look at reserves and production, (December 2017).

22. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017, (December 2017).

23. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017, (December 2017).

24. Gas production data: Rystad Energy UCube (January 2018 update)

25. Ibid

26. Facts Global Energy, Iran Oil and Gas Monthly January 2017, Data File (February 2018).

27. BP Statistical Review of World Energy 2016 (June 2017)

28. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017, (December 2017).

29. Facts Global Energy, Iran’s Oil and Gas Annual Report 2017, (December 2017).

30. Facts Global Energy, Iran Oil and Gas Monthly January 2017, Data File (February 2018).

31. Facts Global Energy, Iran’s Oil and Gas Annual Report 2016, (December 2017).

32. Business Monitor International (BMI) Research, Iran Power Report Q1 2018.

33. Business Monitor International (BMI) Research, Iran Power Report Q2 2015, (March 2015), page 33.

34. Business Monitor International (BMI) Research, Iran Power Report Q2 2015, (March 2015), page 17.