Could Hong Kong After Merger With Shenzhen Help China’s One Belt One Road Thrive? – Analysis

According to the International Monetary Fund (IMF) June 2016 research report “Neoliberalism: Oversold?” which was described as “a political bombshell … that caused a near-panic among advocates of free market policies” by the Foreign Policy analyst Rick Rowden [Note 1], what ‘capital account liberalization’ brings to developing countries is “the pervasiveness of booms and busts” rather than growth. “In addition to raising the odds of a crash, financial openness has distributional effects, appreciably raising inequality……. There is now strong evidence that inequality can significantly lower both the level and sustainability of growth” [Note 2].

As China happens to be in the middle of the capital account liberalization process with a view of making its Renminbi (RMB or China Yuan) freely convertible in the international FX market, Beijing would probably adopt a new growth strategy with reference to such an IMF conclusion. In fact, Beijing is facing a new headache after Brexit because its previous plan of using London, alongside with Hong Kong (a special administrative region in China), as another major offshore clearing center for RMB may not work out as expected, were the secessions of Scotland and Northern Ireland from the United Kingdom to materialize. To find a Plan B, several Chinese scholars have immediately called for the removal of this clearing center from London to Frankfurt or Brussels. However, the long term future of European Union (EU) and Euro are also in danger of deformation or even disintegration amid the rampant emergence of localism, racism and protectionism.

On the other hand, the One Belt One Road (OBOR) framework can be regarded as formally in shape after China has reached the “16+1” agreement with almost all the Eastern European nations [Note 3]. For the buildup of this Silk Road economic zone which encompasses 65 countries across Asia, Europe and Africa, China has to shoulder tremendous funding provision in the coming 50-70 years. Given the gigantic size of debts, intensive stress of risks and lengthy period of generating investment return, Beijing may have no choice but to maintain the control over the ‘capital account’ of international payment until after 2100 so as to prevent the RMB exchange rate from being tortured by the never-ending volatility abroad, thus hindering its development.

If Beijing realizes that the RMB cannot be freely convertible by the end of the 21st century, one of the options available would be to at least triple Hong Kong dollar’s (HKD, a freely convertible currency) circulation volume and speed up its velocity to suffice the necessary financial flexibility and capacity required for China’s efforts in making RMB a major transaction currency second (now the world’s 5th with 1.76% of SWIFT global financial settlement data) to the USD, and tuning the OBOR zone’s economic growth in a stable manner.

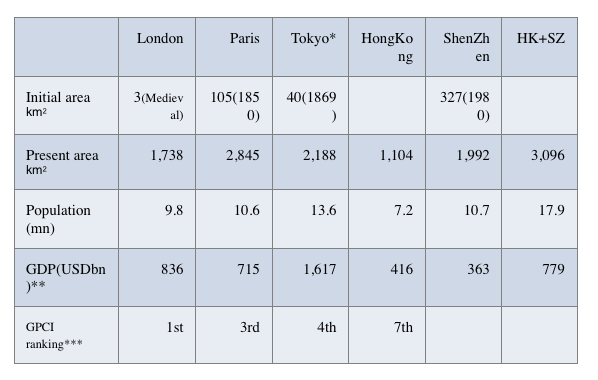

Given the immense scale of the OBOR trade zone, HK’s present economic size is too small (only half of London and a quarter of Tokyo, see the table below), usable land is too little (compared to the wide plain river bank of London and Paris), and human talents are not diversified enough. To overcome these issues, Beijing has to imitate the historical territorial expansion of many other metropolises by merging Hong Kong with its neighboring city Shenzhen to become a special economic zone (HK+SZ).

Data: Wikipedia *1st July 1943 city of Tokyo merged with Tokyo Prefecture to become Tokyo Metropolis ; **GDP (USDbn): Brookings Institution 2014 est PPP-adjusted (listed in Wikipedia) ; ***GPCI: Global Power City Index 2015 ; http://www.mori-m-foundation.or.jp/pdf/GPCI2015_en.pdf

Data: Wikipedia *1st July 1943 city of Tokyo merged with Tokyo Prefecture to become Tokyo Metropolis ; **GDP (USDbn): Brookings Institution 2014 est PPP-adjusted (listed in Wikipedia) ; ***GPCI: Global Power City Index 2015 ; http://www.mori-m-foundation.or.jp/pdf/GPCI2015_en.pdf

The mode of the HK+SZ merger can take reference from the 1991-2000 reunification of Germany and Berlin which cost a total of 2 trillion Deutsche Mark, as well as the reunion of Vietnam and Yemen.

Some of the key arrangements include [1] relocating the London Metals Exchange (which is already a subsidiary of the HK Stock Exchange) to HK; [2] using favorable conditions to encourage banks of Eastern European, African, Middle Eastern and Shanghai Co-operation Organization countries to open branch offices in the low rent SZ districts, and HSBC and Standard Chartered Group to register back in HK; [3] merging the HK and SZ Stock Exchanges and adopting regulations compatible with the EU’s MiFID rules; [4] inducing the OBOR enterprises to raise funds via HKEx listing or issuing bonds here, be them Islamic or in RMB or HKD.

The major benefit of this HK+SZ merger is that, without the need to rely on a politically and financially unstable European FX clearing center for a not-fully-convertible RMB which may become the dominant settlement currency for the trades (Current Account) within the OBOR zone, all the developing countries’ enterprises can enter directly into the sizable HK stock and bond markets to raise the necessary non-USD funds (Capital Account-PIs and Loans) for their domestic primary and secondary productions as well as infrastructural construction. It could greatly ease their present problems of borrowing capital funds from the USD markets and also shelter their domestic economic activities by staying away from the volatile FX market in the West (e.g. Asian financial crisis 1997-8).

While the Western financial institutions are fond of high frequency trading or big shorts, peoples in the developing countries simply want to improve their daily livelihood by, for example, having a clean toilet at home. Given the IMF’s admission of Neoliberal economic policies’ weaknesses, developing countries including China, Brazil, India, Kenya, Sri Lanka and alike would have a legitimate justification to resist the Western pressure to opening the Capital Account, thus paving their own way of cultivating economic growth with a stable currency.

From the Realists’ perspective, the Third World’s diminishing dependency on USD and the Western economies would undeniably threaten the United States’ superpower status. The U.S. could of course bypass the IMF to prevent this from happening by, say, tightening its ‘Contain China’ policy to trigger a OBOR miscarriage. However, the question is: are we going to have a world war (of hate) as what Francois Holland, Donald Trump and Larry Kudlow have been suggesting [Note 4]?

This article first appeared at FPIF with the title as “IMF Disavows Neoliberalism”

[Note 1] Foreign Policy, “The IMF confronts its N-word”, July 6, 2016. http://foreignpolicy.com/2016/07/06/the-imf-confronts-its-n-word-neoliberalism/

[Note 2] IMF, “Neoliberalism: Oversold?”, June 2016. https://www.imf.org/external/pubs/ft/fandd/2016/06/pdf/ostry.pdf

[Note 3] OSW, “China on Central-Eastern Europe: ‘16+1’ as seen from Beijing”, April 14, 2015. http://www.osw.waw.pl/en/publikacje/osw-commentary/2015-04-14/china-central-eastern-europe-161-seen-beijing

[Note 4] CNBC, “Kudlow on Trump’s two homers: Pence and a promise for a declaration of war”, July 16, 2016. http://www.cnbc.com/2016/07/16/trumps-two-homers-pence-and-a-promise-for-a-declaration-of-war.html