Back From The Brink: Policy Reform And Debt Relief In Greece – Analysis

By VoxEU.org

Economists continue to debate whether – and to what extent – Greek debts should be relieved. This column takes through the details of Greek debt, what relief options are open to Greece, and what the likely consequences of relief might be for all parties. Yet again, there are no easy choices – but that doesn’t mean economists and policymakers shouldn’t try.

By William R. Cline*

In the first half of 2015 the populist and confrontational policies of the new Syriza government destabilised the Greek economy, climaxing in the closure of the banks and a referendum rejecting the terms of a financial rescue package offered by the Eurozone partners. But facing the alternative of Grexit, Tsipras, in July, tentatively agreed to a new support programme with conditions at least as demanding as those rejected in the referendum. The new agreement did raise the possibility of debt relief through longer maturities, but explicitly ruled out a haircut on debt principal (Euro Summit 2015). On August 14, 2015, Eurozone finance ministers agreed with Greece on the new support program for €86 billion. The IMF indicated it would only participate if the Eurozone grants Greece debt relief.1

In evaluating the new situation, it is important to recognise that the headline debt figure overstates the true burden of Greek debt. Because most of the debt is owed to official sector partners at concessional interest rates, the interest burden is much lower than would usually be associated with the same gross debt. Under the Fund’s own criterion for sustainability in these circumstances (ratio of gross financing needs to GDP), Greek debt should remain within an acceptable range at least through 2030.2 It is questionable to base debt relief policy on problems that might or might not materialise beyond such a distant horizon. Moreover, most of the projected sharp increase in debt could be avoided by carrying out bank recapitalisation directly from the European Stability Mechanism (ESM) to the banks, rather than through the Greek government as an intermediary.

There is still an important potential role for using interest rate relief, for two purposes. First, if fiscal balances fall below target because of lower than expected growth (rather than policy slippage), a portion of interest otherwise accruing could be forgiven to avoid the need for additional fiscal tightening and its recession-aggravating consequences. Second, because Greek unemployment is at depression levels (26%), special employment programmes would seem appropriate, and forgiving a portion of the interest due could provide a significant source of funding for this purpose.

Framing issues

Some have suggested that it is only fair that Eurozone partners forgive some of the debt, because the official loans mainly went to finance the dash to safety by Eurozone banks previously exposed in Greece.3 However, Eurozone banks only retrieved about €70 billion, about one-third of the official sector support.4

Critics also argue that the Troika (the European Commission, the ECB, and the IMF) contributed to Greece’s depression by calling for too much austerity (see Stiglitz 2015). The fiscal adjustment was indeed large. The cyclically adjusted primary (non-interest) fiscal balance swung from -13.2% of GDP in 2009 to +5.3% in 2014, twice or more times the tightening in Portugal (9.5%), Spain (8.2%), and Ireland (7.2%). But Greece had no fiscal space to adjust more slowly, because it was cut off from financial markets, and official sector support was already stretched to the limits. Some might say that Eurozone support has been too stingy because it forced Greece to adjust too much too fast. Yet support from partner countries amounted to about 110% of Greek GDP, three to four times as much as provided to Ireland (27%) or Portugal (32%). In comparison, US support committed to Mexico in its 1994-95 peso crisis was much smaller (5% of Mexican GDP) and shorter-term.

The adjustment needed to be large because public spending had gotten so far out of hand. Real primary spending per capita had surged by 54% from 2000 to 2009, far more than in Portugal (22%) or Italy (16%); and primary spending relative to GDP had risen from 40% of GDP in 2003-06 to 49.3% in 2009. Nor would less adjustment have paid for itself through more revenue induced by higher growth. Even at the upper bound of the IMF’s upward-revised multipliers (1.7), smaller spending cuts would not have boosted GDP and revenue by enough to pay for themselves. Much of the adjustment occurred in 2010-11, moreover, when sovereign risk spreads were soaring and would have risen even more in the absence of fiscal adjustment efforts.

A final broad policy issue is why it would make any sense to pile an additional €86 billion (about 40% of GDP) in new official claims on top of debt that the IMF already considers unsustainably high. The answer is that most of the new support package will go to amortise existing debt, recapitalise banks and thereby acquire assets, or pay arrears and build up deposits, so the rise in net debt will be only about €10-15 billion (Cline 2015: 5).

Debt projections

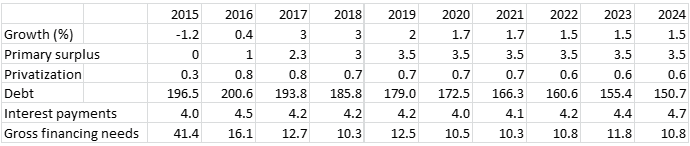

The European Debt Simulation Model that I developed (Cline 2014) provides a basis for projecting Greek debt under the new support programme. Table 1 shows the baseline assumptions for growth, primary fiscal balance, privatisation receipts, and three debt-burden ratios to GDP – gross debt, interest payments, and gross financing needs.5 Growth is far weaker in 2015-16 than expected one year ago (an average of -0.4% instead of 3.3%), as is the decade average for the primary surplus (1.5% instead of 2.8%, see Table 1 and IMF 2014). The baseline assumes €25 billion in bank recapitalisation added to public debt.

Even though debt reaches a peak of 201% of GDP, the interest burden is an average of only 4.2% of GDP in 2015-20 and 4.4% in 2021-24. The reason is that debt owed to the European Financial Stability Facility and European Stability Mechanism pays a low interest rate averaging 1.6% in 2015-20 and 2.6% in 2021-24 (see IMF 2015a: 2).

In comparison, the average interest burden for Portugal in 2015-20 is projected at 4.3% (IMF 2015c). Yet Portugal’s debt is on a much lower path, easing from 126% of GDP in 2015 to 121% by 2020, rather than the much higher path of 200% easing to 150% in Greece. So the debt to GDP ratio substantially overstates the debt burden for Greece.

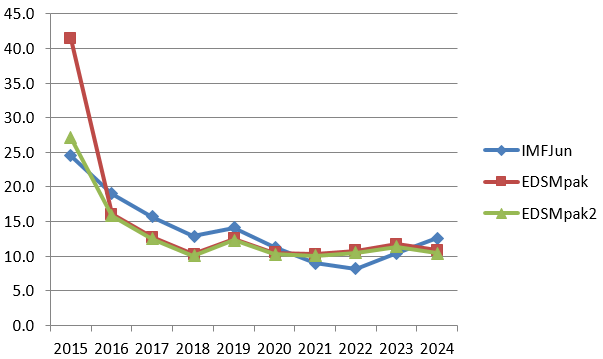

Similarly, except for the first year when there is a bulge because of the bank recapitalisation, the gross financing needs ratio lies comfortably in or (mostly) below the 15-20% acceptable range identified by the IMF. So again these projections confirm the diagnosis that for the coming decade at least, there is not a critical problem of over-indebtedness.

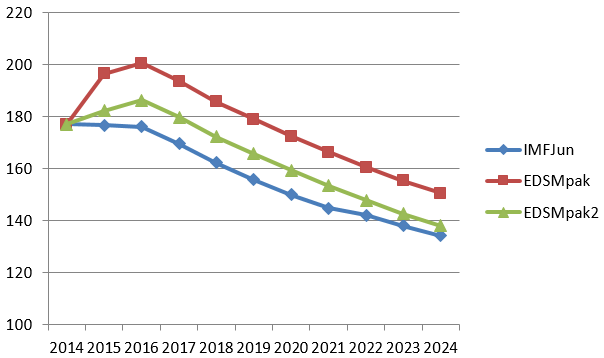

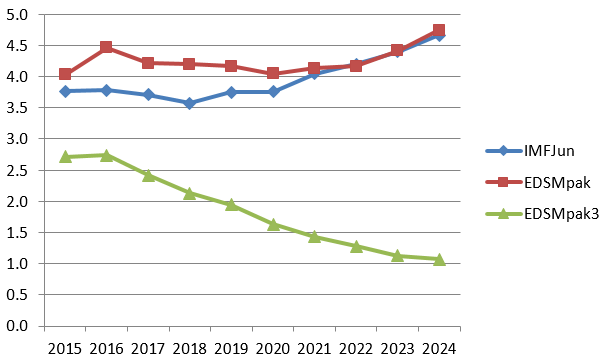

Figures 1 through 3 show these same three ratios for the baseline (‘EDSMpak’ for package) alongside alternative projections and scenarios. All three figures show the June 2015 IMF baseline for comparison. Figures 1 and 3 also show a scenario in which bank recapitalisation is handled outside of sovereign debt (‘EDSMpak2’). Figure 2 shows a scenario in which all interest on debt owed to the Eurozone partners (but not ECB) is forgiven for this decade, as a gauge of debt relief potential (‘EDSMpak3’).

Figures 1 and 3 strongly suggest that the optics of the Greek debt burden would be much improved if the €25 billion in bank recapitalisation were handled directly by the ESM and the banks rather than passing through the sovereign.6 For its part, Figure 2 strongly suggests considerable scope for debt relief through forgiving interest on the Eurozone partner claims. If there were a complete interest holiday for the full decade, the ratio of interest payments to GDP would be down to only 1% of GDP by 2024.

Debt relief?

Rather than focusing on amortisation and risk of replacement of low-interest official debt by high-interest private debt after 2030, the concern of the IMF (2015b), it could be more useful to focus debt relief on contingent compensation already in the present decade in the event that fiscal balances deteriorate from the planned path because of lower than expected GDP growth. For example, if growth turned out to be 2% in 2017 instead of 3%, revenue would be lower by 0.4% of GDP (Cline 2015: 10). This amount could be compensated by forgiving about one-fifth of interest due on Eurozone claims (excluding ECB).

A parallel line of interest relief could forgive part of the interest as a means of financing employment-intensive public works programmes. If such programmes paid a wage of 90% of the minimum wage, allocating one-fourth of the interest due to Eurozone partners (or about €1 billion annually) would suffice to hire 135,000 workers, about 11% of the total number currently unemployed (Cline 2015: 11).

As for the capacity to meet gross financing needs by 2030 and after, in principle the ESM partners could commit to evaluation of the need for further stretch-outs of maturities (and reductions in interest rates) for that period closer to the event.

IMF participation?

Support from the IMF bears a penalty interest rate of 300 basis points above the basic IMF lending rate (SDR rate, now only 5 basis points, plus 100 basis points), because loans to Greece greatly exceed the country’s IMF quota and are at long maturities. It would therefore be desirable for the Eurozone to provide almost all of the new lending rather than relying on substantial additional support from the IMF.7 However, IMF monitoring would help ensure proper policy design and performance, supplementing monitoring by the European Commission. For this purpose it would make sense for the Fund to limit further Extended Fund Facility support to a modest amount such as €1 billion, thereby shifting onto the Eurozone most of the additional gross disbursements that otherwise might have been expected from the IMF.8

About the author:

* William R. Cline, Senior fellow, Peterson Institute for International Economics

References:

Cline, W R (2014), “Managing the Eurozone Debt Crisis”, Washington: Peterson Institute for International Economics.

Cline, W R (2015), “From Populist Destabilization to Reform and Possible Debt Relief in Greece”, Policy Brief PB15-12, Washington: Peterson Institute for International Economics, August.

Consensus Economics (2015), Consensus Forecasts, London, 13 July.

Euro Summit (2015), “Euro Summit Statement”, Brussels, 12 July, Brussels.

European Commission (2015), “Greece—Request for Stability Support in the Form of an ESM Loan”, 10 July, Directorate General, Economic and Financial Affairs, Brussels.

IMF (2013), “Staff Guidance Note for Public Debt Sustainability Analysis in Market-Access Countries” 9 May, Washington.

IMF (2014), “Greece: Fifth Review Under the Extended Fund Facility”, Country Report 14/151, June, Washington.

IMF (2015a), “Greece: Preliminary Draft Debt Sustainability Analysis”, Country Report 15/165, 26 June, Washington.

IMF (2015b), “Greece: An Update of IMF Staff’s Preliminary Public Debt Sustainability Analysis”, Country Report 15/186, 14 July, Washington.

IMF (2015c), “World Economic Outlook Database April 2015”, Washington.

Stiglitz, J E (2015) “Greece, the Sacrificial Lamb,” The New York Times, 25 July.

Summers, L (2015), “Greece is Europe’s failed state in waiting”, Financial Times, 20 June.

Wagstyl, S (2015) “Merkel goes on offensive to quell revolt over €86 billion Greek bailout”, Financial Times, 17 August.

Footnotes:

1 The Fund’s participation may not be decided until October (Wagstyl 2015).

2 Earlier IMF work had identified 15% of GDP as sustainable for emerging market economies, and 20% as sustainable for advanced economies (IMF 2013).

3 Larry Summers has suggested that “the vast majority” of support went for this purpose (Summers 2015).

4 This estimate and others in this article are set forth in Cline (2015).

5 Growth, primary surplus, and privatisation projections are based on IMF (2015a), European Commission (2015), and Consensus Economics (2015). The August 14 agreement placed the primary surplus moderately higher in 2015-18 (at 1, 2, 3, and 3.5% of GDP, respectively), but noted the targets “will be discussed… in light of recent economic developments”. See “Greece: Prior Actions”, available at http://www.wsj.com/public/resources/documents/GreekProposals070915.pdf.

6 This ‘debt’ is largely an optical illusion, because it would involve acquiring a corresponding asset in the major banks. The government already owns 40% of their weighted market capitalisation, and with the additional recapitalisation this ownership would rise to 90%. But the simple headline debt ratio does not deduct the value of this additional acquired asset.

7 The effective interest rate on IMF support is 3.7%; as noted, through 2020 the average rate is only 1.6% for ESM support.

8 Amounting to about €20 billion (Cline 2015: 15).