The State Of The Eurozone Monetary Union – Analysis

By VoxEU.org

The Eurozone crisis continues to take centre stage. This column discusses how deep the EZ crisis is, how long it will last, and what should be the policy priorities. A number of findings emerge. First, the difference in labour market performance between the US and the Eurozone is one of degree but not of kind. Second, the economic consequences of the sovereign debt crisis will be mostly gone by 2018, but the political crisis will continue. Third, enforcing fiscal rules via political arm twisting is a recipe for disaster. Market discipline must instead be brought back, but without financial fragmentation. Limited and conditional Eurobonds are the best way to do so.

By Thomas Philippon*

Unemployment in the US vs the Eurozone

I first compare labour market dynamics inside the Eurozone with those inside the US (for a broader discussion of macro-financial stability, see Lane 2015). The US is a well-functioning currency area, but there is significant heterogeneity in credit and house price dynamics. This makes the US a relevant control group, as argued in Martin and Philippon (2014).

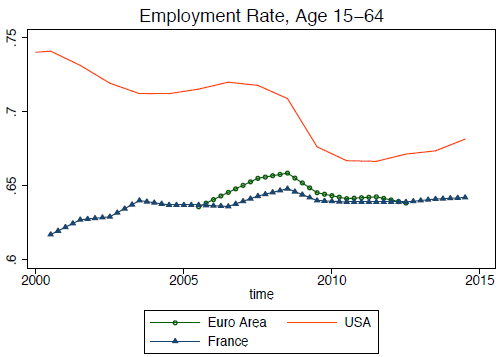

The unemployment rate is the most widely discussed statistic, but if we want to think about inefficiencies in the labour market it is more relevant to look at the rate of employment, the number of people working divided by the population that could be working. Figure 1 shows the employment rates of all individuals aged 15 to 64 in the US, the Eurozone, and France. Availability is limited for the Eurozone data and France provides a useful benchmark since it is always close to the median of the Eurozone.

Differences between Europe and the US appear smaller when we consider employment rates instead of unemployment rates. The drop in employment in the US is severe and long lasting and the recovery is weak, unlike with the unemployment series, suggesting that workers may have become discouraged. The decline in US employment also pre-dates the 2008 recession, as discussed in Moffitt (2012), suggesting structural, not cyclical issues. In Europe, on the other hand, employment rates have declined less, although they started from a lower level on average. Many European countries’ employment rates appear to be on an improving trend, often as a result of structural reforms, such as pension reforms.

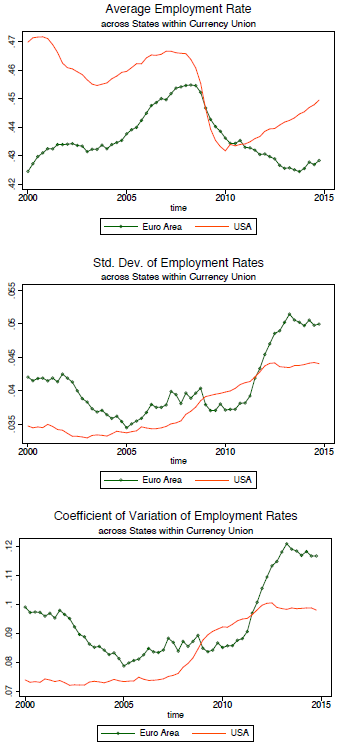

Figure 2 presents total employment rates without controlling for differences in the age structure of the population. The top panel shows the average (unweighted) employment rate across states and countries. The middle panel shows the standard deviation and the bottom panel the coefficient of variation (the standard deviation divided by the mean). We observe a more persistent slump and more dispersion in the Eurozone than in the US, but these differences are smaller than with unemployment rates. In particular, the coefficient of variation increases significantly in the US as well. To paraphrase Darwin, I conclude that the difference in labour market performance between the US and the Eurozone, significant as it is, is one of degree and not of kind.

A tale of three crises: Finance, economics, and politics

The European crisis is in fact the sum of three crises, unfolding over different time frames. These differences confuse the commentators and lead to widely misleading predictions such as “now that the acute financial crisis is over, surely the economies will rebound”, or “now that unemployment rates are finally falling, surely the worst is over”.

- The financial crisis is violent and short-lived.

Looking at 10-year government yields in the Eurozone, the sovereign debt panic starts in 2010 and peaks in 2012; by 2014 it is essentially over.

- The economic crisis is much slower than the financial crisis.

We have seen earlier (Figure 2) that employment rates have barely begun to recover. What this means is that the worst in terms of employment is likely to happen after the end of the financial panic.

- The political crisis is slower still.

Guiso et al. (2015) show that trust towards the EU has continuously declined from 2010 to 2013, and that the trend is unlikely to be reversed any time soon. This means that the worst distrust towards the EZ is likely to happen when the economic recovery is under way. It is not during the economic crisis that the political crisis is the most acute, but after.

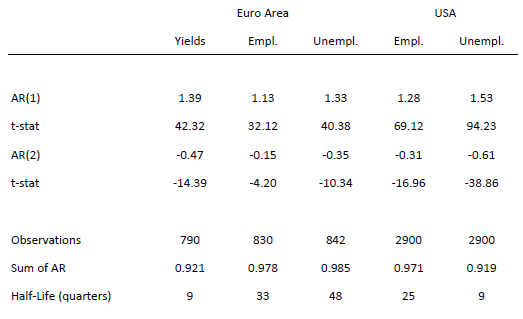

A quantitative analysis of the persistence of the shocks, in Table 1, shows that the half-life of government bond spreads is of about two years (9 quarters). If a country experiences an increase of its rate of 100 basis points relative to the Eurozone average, then two years later we expect a spread of about 50 basis points. For the employment rate, however, the half-life is about eight years (33 quarters). Economic distress is much more persistent than financial distress. A formal test of the persistence of political shocks is hampered by data availability, but the data presented by Guiso et al. (2015) makes it clear that they are even more persistent than economic shocks.

This simple analysis suggests that the economic consequences of the sovereign debt crisis will persist until 2018, and that the political consequences will persist longer.

The Greek debacle

Greek people have suffered tremendously and the country is left with massive unemployment and a crushing debt overhang. As terrible as Greece’s depression might be, the right question to ask is: How much could we have avoided with better policies? The answer depends on how far back we start.

- During the boom: reckless policies.

If we go back to the pre-crisis period, we find that most of the Greek drama would have been avoided with sensible policies. In Martin and Philippon (2014) we quantify the causes of the crises across the Eurozone and we find that Greece was (mostly) brought down by reckless government spending during the boom years. In that sense, and since Greece is a democracy, one can argue that it is first and foremost responsible for its own demise.

But we – governments, households, investors – all make mistakes, and this is why policymakers have devised mechanisms (such as debt restructuring) to deal with the consequences of these mistakes. A more directly relevant question is then: How badly was the Greek crisis handled? Or in other words, starting from 2009/2010, how much better could the Greek situation have been?

- After 2009: only bad options.

The first thing to recognise is that, given how unbalanced the Greek economy was in 2009/2010, a major recession was inevitable. As Blanchard (2015) explains, “[h]ad Greece been left on its own, it would have been simply unable to borrow. Even if it had fully defaulted on its debt … it would have had to cut its budget deficit by 10% of GDP from one day to the next. These would have led to … much higher social cost than under the programs.”

But policy mistakes also made the situation. Some observers advocated an early debt restructuring, coupled with strong fiscal consolidation, but the perceived risk of contagion made it impossible to implement. Eventually, in 2012, Greece’s debt was reduced by approximately €100 billion. This was unfortunately too late – much of the macroeconomic damage was done.

Since an early restructuring was prevented by fears of contagion (legitimate or misguided, this is beside the point), I have argued (see Philippon 2015) that it is not fair to ask Greece to pay for the consequences of the delay. If one accepts this idea, then it follows that one should consider an alternative history – with an earlier debt restructuring – as a benchmark for Greece’s debt negotiation.

When I simulate the path of the Greek economy assuming an ‘early debt relief scenario’, I find that it is significantly better than the actual path in terms of GDP, employment, and debt dynamics. Based on these calculations, I argued that it would be fair to lower Greece’s target for primary surplus by at least 1.5%.

- The 2015 tragedy.

The word ‘tragedy’ has been over-used to talk about Greece’s economic disaster. I do not use it to describe what happened between 2009 and 2013. Mistakes were made, but it is far from obvious that there were better alternatives available in real time.

What happened in 2015, however, does have a tragic flavour. The Greek people were led to believe that they could get a better deal if only they elected a different government. Instead, they got a worse deal, in all respects.

The first six months of the new Greek government, following the elections of January 2015, were a complete disaster.

- In 2014, the real GDP of Greece grew for the first time since 2007, by 0.8%. Greece managed to issue bonds at 3.5%.

- Unemployment was falling and GDP was forecast to grow by 2.5% in 2015.

- Thanks to erratic and irresponsible policies, growth forecasts have been revised down to 0.5% and unemployment will be significantly higher than it would have been.

The tragedy comes from the clash between the economic and political dynamics described earlier.

Grexit might have made sense in 2008, but not in 2015. From 2005 to 2009, Greece accumulated a current-account deficit of 57.6% of GDP. Closing that gap required an increase in exports and a decrease in imports, which is difficult and painful to achieve without devaluation. So one could reasonably argue that an exit followed by a massive default and devaluation made sense at that time. But in 2015, the adjustment was done, painful as it was, and bygones should be bygones. A sensible policy would have been to focus on improving the economy going forward.

The 2015 elections and the ensuing negotiations, however, had nothing to do with economics. It was pure political theatre on both sides. Mr Tsipras won the elections and successfully destroyed his political opponents, inside and outside Syriza, becoming the only politician left standing and assured to head the country for at least a few more years. His tenure as prime minister has so far been a failure. On the other side, there was a clear desire in Germany to punish the new Greek government and teach a lesson to other populist movements in Europe. There are good reasons to fight populism and demagogy in Europe, but the idea that this is best done by imposing humiliating conditions in a Troika programme sounds particularly wrong-headed to me.

Concluding remarks and the way forward

What I take away from the previous sections is:

- On one hand, the structural problems of the Eurozone are more severe than the ones facing the US, but that the differences are not nearly as large as what is commonly argued.

- On the other hand, political risk and distrust (in a broad sense) will persist for a long time.

They will not dissipate simply because unemployment comes down. It is, therefore, important to plan for several years of political instability.

So what should be done?

- Keep cool and continue building the banking union

Firstly, policymakers need to keep a cool head. This might sound obvious but the hysterical discussions surrounding the Greek crisis show that there is no lack of stupid ideas and bad policy advice. I find most annoying the ‘Eurozone is not an optimal currency area’ arguments that repeat commonplace ideas without providing any actual insight.

The interesting question is: What does it take to have a stable currency area? In my view, the traditional approach missed the most important piece –the banking union. Forget labour mobility, a common language, or even a federal budget.1 A banking union is the one piece of financial architecture that should have been built before the crisis. Véron (2007) asked in 2007 whether Europe was ready for a banking crisis. How many others saw that critical point? Thankfully the banking union is under way and should be supplemented by a capital market union (Véron and Wolf 2015).

- Reforming the Eurozone.

The Greek crisis has exposed deep flaws in the functioning of the Eurozone. It needs to become more accountable, more transparent, and more efficient.

A possible solution is to merge the position of ECFIN commissioner with that of president of the Eurozone. At the same time, the enforcement of fiscal discipline should be entrusted to an independent division within ECFIN. We also need a Eurozone chamber within the European parliament where EZ issues would be discussed and where the President of the Eurozone would be confirmed and heard on a regular basis.

- More markets, less politics.

The externalities that exist in a currency union create the need for strict fiscal discipline among member states. The difficult issue is how to impose this discipline effectively. Bénassy-Quéré (2015) explains clearly how the logic of the Maastricht treaty proved faulty, and the Greek debacle shows that we should not rely on finance ministers to impose discipline on each other. The political dynamics are simply too destructive.

Imposing mechanical balanced-budget rules like in the US is not an option since we do not have a federal budget or a common pool of safe sovereign debt. Countries need to retain some fiscal discretion simply because there is no fiscal discretion anywhere else in the system.

We need instead to bring back market discipline. It would have been much better for everyone if the markets had told the Greek government that their economic plans made no sense, instead of other finance ministers. Markets are neither stable nor particularly smart, and they impose discipline too late and too abruptly.

- Markets, however, have one fundamental advantage over politicians – they punish but they do not humiliate.

Traders vote with their feet, they do not want to teach lessons, they do not seek revenge. One can complain that markets forget too quickly, but in this case I would argue that this is a critical advantage.

The fundamental challenge, then, is to revive market discipline without creating the risk of sudden stops (Merler and Pisani-Ferry 2012). This is why we need to reopen the eurobonds debate.

- Eurobonds, or at least Eurobills.

Eurobonds were widely discussed in 2010 and 2011 but they were not implemented, probably because they were not the right choice as a crisis management tool.

The combination of ESM and OMT did the job. But the lively debates that took place at the time were nonetheless insightful.2 Here is a quick summary of what most participants agreed on:

- A currency union needs a shared safe asset.

That safe asset should not be the bonds of one particular member because this could trigger episodes of sudden stops and flight to safety. The price of a safe asset should increase in bad times, providing cheap funding to its issuers precisely when it is most needed.

- A shared safe asset would be very useful for banking regulation and for the conduct of monetary policy.

The banking aspect is particularly important in my opinion. Banking supervision cannot continue to treat all sovereign debt as risk free. On the other hand, it would make no sense for the Eurozone to simply give up its safe assets. The solution is to treat individual sovereign debt as risky and to introduce new safe assets at the same time.

- Avoiding moral hazard is a priority but we should recognise that moral hazard is already present in the current system and we should look for an improvement, not a first-best solution.

I would also argue that providing some insurance (as in the form of eurobonds quotas) is likely to reduce moral hazard by making the no-bailout option more credible. There will always be a bailout option, pretending otherwise is foolish. But we can minimise the set of circumstances where bailouts take place.

I view the blue/red bond proposal of Delpla and von Weizsäcker (2010) as the most elegant solution. Had Europe implemented a banking union together with the Delpla and von Weizsacker proposal, there would not have been a crisis at all. After the crisis, however, the legacy debt makes the transition a lot more difficult. A less ambitious proposal is to introduce eurobills, as proposed by Hellwig and Philippon (2011). The idea is to mutualise the short end of the yield curve – to avoid fragmentation of the money markets – but not the long end – to maintain market discipline. That same logic that was later applied to the OMT, and it worked exactly as predicted. I would therefore propose the introduction of eurobills together with the gradual strengthening of the no-bail-out clause by adjusting the prudential requirements on sovereign debt. In the long run, we would move to a blue/red debt market where markets would help enforce fiscal discipline.

About the author:

* Thomas Philippon, Professor of Finance, Stern School of Business, NYU and CEPR Research Affiliate

References:

Bénassy-Quéré, A (2015), “Maastricht flaws and remedies”, Note du CAE (English version), forthcoming.

Blanchard, O (2015), “Greece: Past critiques and the path forward”, iMF direct blog.

Bofinger, P, L Feld, W Franz, C Schmidt, and B Weder di Mauro (2010), “European redemption pact”, VoxEU.org, 9 November.

Brunnermeier, M, L Garicano, P Lane, M Pagano, R Reis, T Santos, M Pagano, D Thesmar, S Van Nieuwerburgh, and D Vayanos (2011), “ESBies:A realistic reform of Europe’s financial architecture”, VoxEU.org, 25 October.

Corsetti, G, L Feld, P Lane, L Reichlin, H Rey, D Vayanos, and B W di Mauro (2015), A new start for the Eurozone: Dealing with debt, Monitoring the Eurozone 1, CEPR.

Delpla, J and J von Weizsäcker (2010), “The blue bond proposal,” Bruegel policy brief, May.

Guiso, L, P Sapienza, and L Zingales (2015, April), “Monnet’s error?” EIEF Working Paper.

Hellwig, C and T Philippon (2011), “Eurobills, not Eurobonds”, VoxEU.org, 2 December.

Lane, P (2015), “Macro-financial stability under EMU”, CEPR Discussion Paper 10776.

Martin, P and T Philippon (2014), “Inspecting the mechanism: Leverage and the great recession in the Eurozone”, Working Paper NYU.

Merler, S and J Pisani-Ferry (2012), “Sudden stops in the Eurozone”, Bruegel Policy Contribution.

Moffitt, R A (2012), “The reversal of the employment-population ratio in the 2000s: Facts and explanations”, Brookings Papers on Economic Activity 1, 201–264.

Philippon, T. (2015), “Fair debt relief for Greece: New calculations,” VoxEU.org, 10 February .

Véron, N (2007), “Is Europe ready for a major banking crisis?” Policy brief, Bruegel, August.

Véron, N and G Wolf (2015), “Capital markets union: a vision for the long term”, Bruegel Policy Contribution, April.

Yagan, D (2014), “Moving to opportunity? Migratory insurance over the great recession”, manuscript January.

Footnotes:

1 For the US, Yagan (2014) finds that despite migration flows that were in principle large enough to provide full insurance, migration has provided only 7% insurance; the 2006 residents of the average local area have borne 93% of the area’s idiosyncratic labour demand shock during the Great Recession.

2 Four proposals were discussed in details: Delpla and von Weizsäcker (2010), Bofinger et al. (2010), Brunnermeier et al. (2011), and Hellwig and Philippon (2011). See also Corsetti et al. (2015).