Tethered To The US Financial System – Analysis

US interest-rate hikes put the Turkish lira and the currencies of other emerging economies in peril, and the United States may not be a good role model.

By Will Hickey*

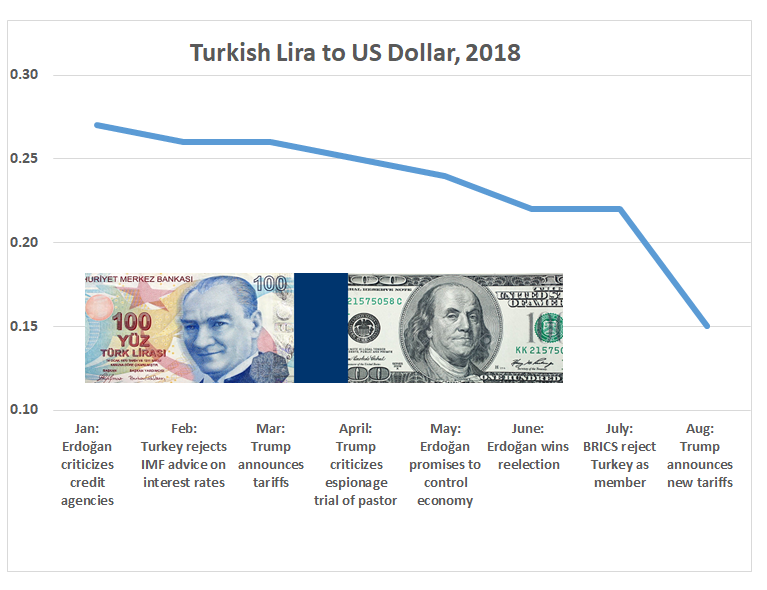

The lira has collapsed after Turkey borrowed foreign currency, namely US dollars, at low interest rates to fund increasing economic expansion. Such borrowing, an example of what Berkeley economist Barry Eichengreen has called “original sin,” works fine until conditions derail economic patterns – in Turkey’s case, the US Federal Reserve increasing interest rates. As of this writing, the currencies of not only Turkey, but also Argentina, India and Indonesia continue on a volatile slope, pointing largely downward due to US rate increases.

Pundits are quick to point out that Turkey’s currency woes are not spreading, yet other countries do confront similar challenges. More so, fund managers reduce exposure to all emerging market assets as a matter of course, as one bad apple can spoil the whole basket: Emerging economies must raise interest rates, contain domestic debt, rein in inflation and more.

Economists must consider the social ramifications of what they preach. Turkey has many features of so-called vibrant economies: an entrepreneurial mindset, a youthful population with a median age of 30, social media usage, internet penetration greater than 50 percent, and an export-oriented mindset along with a Blue Oceans strategy. Turks are also a large part of new business formation and innovation in Europe, with more than 4 million in Germany and 1 million in France, doing the jobs many Europeans don’t want to do. Further, Turkey has absorbed the brunt of refugees from Syria, sheltering more than 3 million, and helped refugees from as far away as Myanmar. Overall, Turks display what economist John Maynard Keynes called “animal spirits,” engaging in investment even during times of uncertainty. Not being an EU member, not being shackled to stifling Brussels dictates, may be a blessing in disguise for Turkey.

Still, Turkey has problems, some unpalatable for Western analysts. Foremost, Turkey shares borders with conflict-ridden Syria, Iran and Iraq, not to mention a thriving Kurdish insurrection in Anatolia. Easy foreign money has created a false housing boom that enriched a few while many Turks struggle economically. An increasingly authoritarian leader disrupts freedom of the press and speech and blocks social media. Turkey’s conflicts with the Kurds, about 20 percent of the country’s population, has led to accusations of human rights violations. Even so, when the dollar is removed from the equation, Turkey has much to offer investors over the long term, perhaps even more than some developed Western countries with plateaued markets.

Turkey has been among the world’s biggest booming economies during the past 15 years. No country can fake economic growth for 15 years. Turkey’s President Recep Tayyip Erdoğan faces market pressures, and issues such as tension with Washington over an imprisoned US pastor, tit-for-tat tariffs or a religious leader hiding out in the United States are sideshows, distracting from Turkey’s economic complexities.

Surrender to the US dollar is often the only game in town for many emerging economies. Currencies ultimately are linked to the dollar, and even the euro, pound and Japanese yen are kept “range-bound” by their respective central banks – meaning that they fluctuate within a band. For example, the Korean won rarely deviates below 1000 or above 1200 won per dollar to protect the export industry from instability. This is similar with other Asian currencies, such as the Singapore dollar, ranging from $1.30 to 1.50 per US dollar.

However, the US economy depends on a mind-boggling national debt overhang, approaching $22 trillion, and a widening current account trade deficit – with more imports than exports to most countries, not just China. Also, the country has an overheated housing market, growing public indebtedness of mandatory entitlements of Social Security and Medicare, not to mention an overextended military policing much of the world on borrowed money.

However, the US economy depends on a mind-boggling national debt overhang, approaching $22 trillion, and a widening current account trade deficit – with more imports than exports to most countries, not just China. Also, the country has an overheated housing market, growing public indebtedness of mandatory entitlements of Social Security and Medicare, not to mention an overextended military policing much of the world on borrowed money.

Other countries being told to reform their economies have similar problems. By using the US dollar as a borrowing currency, other countries also import US economic policy. But the United States, as the world’s largest economy with a reserve currency, can resist adopting others’ policies.

Orthodox economic wisdom suggests that the United States can continue to run large trade deficits as it has the potential to “grow” itself out of debt with innovation, productivity and its status accounting for 60 percent of global currency reserves. Other countries do not have these advantages. Other economies are advised to rely on dollar pegs and fixed exchange rate such as the Hong Kong/US dollar or outright dollarization of an economy as in Ecuador. These arguments are growing old as the United States confronts its own social and political problems including inequality, automation replacing jobs, subsidies and the debt burden.

Other countries exhibiting dollar fatigue are in the same boat as Turkey and should not be judged on dollar scarcity alone. Venezuela has a politically tested population lean and hungry for change. Iran wants to develop its fossil fuel deposits and has cheap, youthful labor. India has a huge market potential ripe for expansion. Russia has vast tracts of land in need of development to feed other booming populations, including those in nearby China. Indonesia, an island nation, offers significant infrastructure and development opportunities, and Argentina has vast natural and agrarian resources.

The global economy should not rise and fall based on one apex factor of dollarization, not when the dollar is flawed. Countries will seek alternatives. such as Zimbabwe with “dollar bonds,” or Venezuela and Russia with cryptocurrency backed by oil – though for the latter, the response is mostly to vast oil exports, crude oil priced in dollars worldwide and US sanctions.

In the information age, entrepreneurship and innovation are increasingly becoming real currency, more so than any devalued fiat money, with nothing behind it in many cases except a printing press. Logically, countries may then ask if it is necessary to continue borrowing in foreign currencies and instead seek domestic advantages via restructured institutions.

In the 21st century, societies must consider what they can offer and how these opportunities can be monetized. Emerging economies want to free themselves from hanging on every US Federal Reserve interest hike or inflation worry. Countries must start restructuring their own economies to utilize and institutionalize these advantages. For all countries, in particular those seeking to escape the middle-income trap such as Turkey, China, Argentina and Indonesia, upgrading their labor markets to promote domestic demand and value-added activity, as opposed to dependence on raw commodity exports or low value-added manufactured goods, is a consistent theme.

There is no free lunch. Reliance on US dollars to kick domestic problems down the road can quickly turn into a double edged sword in a world of rising US rates. Just ask Turkey.

*Will Hickey is a Visiting ASEAN Professor with Guangdong University of Foreign Studies, Canton, China. He is also author of Energy and Human Resource Development in Developing Countries: Towards Effective Localization, Macmillan, 2017.