Trump’s Final Gamble: From Chinagate To Hybrid Wars – Analysis

The disastrous failure of the Trump administration to contain COVID-19 will result in catastrophic second quarter data. As a result, Trump is risking his re-election on domestic unrest, fatal geopolitics and a global depression.

The cold reality is that the Trump administration learned about the virus already on January 3, when CDC Director Dr. Robert R. Redfield informed Secretary of Health Alex Azar that China had discovered a new coronavirus. Yet no mobilization was initiated until toward late March (see my report here):

Indeed, the Trump White House missed three opportunities to contain the virus outbreak; in January (between CDC alert and WHO’s international emergency), the first quarter (between the WHO emergency and the pandemic alert) and the second quarter (since social distancing began 6-8 weeks late and inadequately).

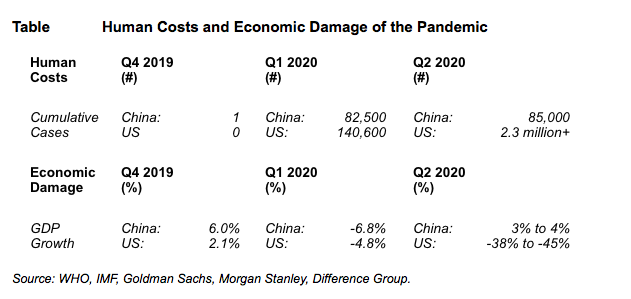

Instead of virus mobilization in early January, a long debate began within the White House over “what to tell to the American public,” while Azar and Secretary of State Mike Pompeo began repeated attacks against China. The consequent economic carnage is evident in the second quarter free-fall (Table).

At the end of June, the US is likely to have more than 2.3 million cumulative cases and over 130,000 deaths. In the first quarter, US annual GDP growth contracted (-4.8%) but the real carnage will ensue with the second quarter plunge (-38% to -45%), as I projected in April and major US investment banks have warned. The Atlanta Fed’s model expects a -52% plunge, however.

To survive its pandemic and economic failures, the Trump White House has initiated a series of measures in a hybrid war against China. In the absence of timely countervailing actions, these measures have potential to undermine global economic prospects in the short term and the promise of the Asian Century over time.

Southeast Asia will not remain immune to such headwinds.

From Chinagate to hybrid China Wars

As the Trump White House has targeted China as a its re-election scapegoat, the early victims include US-Sino high-level bilateral dialogue, trade and investment relations, US treasuries, military relations and destabilization in East Asia.

High-Level Dialogues. Undermining decades of US-Sino bilateral progress, President Trump has let US-Sino high-level economic, law enforcement and cultural dialogues freeze since fall 2017; the diplomatic and security dialogue since fall 2018.

Trade. Trade tensions are re-escalating. After the Phase-I deal, China is obliged to buy $200 billion in additional US imports over two years on top of pre-trade war purchase levels. The truce would require 18% annual import growth from the US, which is challenging to China amid Trump protectionism and dire global prospects.

Investment. Before the trade wars, US investment to China averaged $15 billion per year, whereas Chinese investment in the US soared to $45 billion. US investment to China has persisted, but Chinese investment in the US has been forced to plunge to $5 billion. Thanks to Trump decoupling, over a decade of progress has been reversed. Nevertheless, seven of ten US companies do not plan to leave China.

Treasuries. For years, Beijing invested much of its foreign exchange reserves in US assets, particularly US Treasury securities. In another low-probability but high-impact re-election scenario, Republicans are threatening Beijing with unilateral $1.1 trillion debt cancellation, while Democrats hope to de-list Chinese companies from US markets. As a result, Beijing is diversifying investments away from the US, while pumping over $1.4 trillion into the tech sector over to 2025.

Military Relations. Despite political differences, US-China military exchanges used to feature high-level visits, exchanges between defense officials, and functional interactions. According to Pentagon, these engagements have fallen by two-thirds in the Trump era, while bilateral tensions are rapidly escalating in South and East China Sea. Whether accidental or provoked, a conflict is a matter of time.

Special Administrative Regions. Destabilization efforts in Chinese mainland’s proximity have escalated dramatically since 2017.

- Taiwan. Unlike previous administrations, the White House, in cooperation with Taiwan’s president Tsai Ing-wen, seeks to undermine decades of “One China” policies. If the past “strategic ambiguity” gives way to force, the geopolitical impact could destabilize East Asia.

- Hong Kong. According to Washington, “pro-democracy forces” are threatened in Hong Kong. According to Beijing, cooperation between the White House, Congress, and Tsai government is fueled by a quest for “color revolution.” As Senate Intelligence Committee chair, radical-right Sen. Marco Rubio (R-FL) hopes to exploit the Hong Kong Human Rights and Democracy Act for regime change in China as he has in Iran, Russia, Venezuela and elsewhere.

- Macau. Financier of the Trump campaign and Republican conservatives, billionaire casino magnate Sheldon Adelson allowed the CIA to use of his Macau properties for US espionage in the early 2010s. More recently, his Sands Corp. played a critical role in an apparent spying operation targeting Julian Assange, when the CIA came under the control of Mike Pompeo, another Adelson ally.

- Tibet. Before Trump’s Hong Kong declaration,US lawmaker Scott Perry (R-PA), a retired Pennsylvania Army National Guard Brigadier General, has introduced a bill to recognize Tibet as a sovereign country.

From pandemic geopolitics to US debt crisis

In 2003, the Bush administration began its Iraq War under a pretext, presumably to achieve a domino-effect democracy across the Middle East. The consequent nightmare led to still another ‘forever war’ in the region, in which the costs soared to $3 trillion, as estimated by economist Joseph Stiglitz.

Barely two decades later, the Trump administration has initiated what in Beijing looks like a nascent hybrid war to win re-election. The economic costs of complacency, which are misplaced on China and WHO, are estimated at $9 trillion; that’s three times the costs of the Iraq War.

These tragic losses could pale with the imminent new policy mistakes. In what I have termed a Great Power Conflicts scenario, lingering pandemic risks would result in intense trade and technology wars, “hot” geopolitical conflicts and a long, multi-year global depression. This is the current path of the Trump White House, which is predicated on leveraging US economy to the hilt.

US debt has soared to $26 trillion that puts US debt-to-GDP ratio to 120% (at par with that of Italy amid its debt crisis in 2011-12), which the White House and the Fed will soon have to further increase.

Due to the central role of US in the world economy, such economic leverage – coupled with the human costs of the pandemic and deadly geopolitics – is pushing global prospects toward the edge of global depression.

This is a short version of a commentary published by China-US Focus on June 5, 2020.