Indonesia Energy Profile: Reorienting Energy Production To Meet Domestic Demand – Analysis

By EIA

Indonesia, with a population of 253 million people in 2014, is the most populous country in Southeast Asia and the fourth most populous country in the world, behind China, India, and the United States.1 Formerly a net oil exporter in the Organization of the Petroleum Exporting Countries (OPEC) for several decades, Indonesia now struggles to attract sufficient investment to meet growing domestic energy consumption because of inadequate infrastructure and a complex regulatory environment. Indonesia encompasses more than 17,000 islands, presenting geographical challenges in matching energy supply in the eastern provinces with demand centers in Java and Sumatra. Also, urbanization and demand in other areas of the country are rising at a faster pace than energy infrastructure development.

After suspending its OPEC membership seven years ago, Indonesia is scheduled to rejoin the cartel by 2016 as the country attempts to secure more crude oil supplies for its swiftly rising demand and greater investment from Middle Eastern members in its downstream infrastructure projects. Despite Indonesia’s energy struggles, it was the world’s largest exporter of coal by weight and the fifth-largest exporter of liquid natural gas (LNG) in 2014. As Indonesia seeks to meet its energy export obligations and earn revenues through international market sales, the country is also trying to meet energy demand at home.

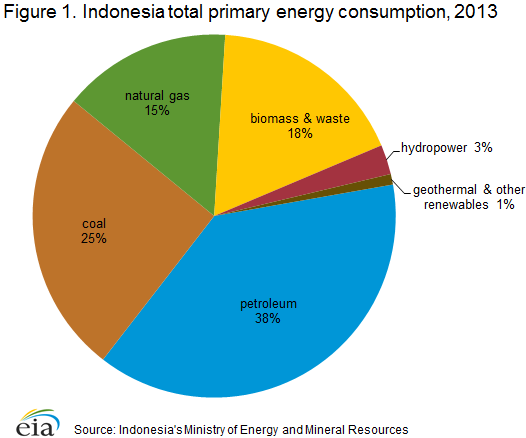

Indonesia’s total primary energy consumption grew by 43% between 2003 and 2013, according to the Indonesian government. The country’s petroleum share, although decreasing, continues to account for the highest portion of Indonesia’s energy mix at 38% in 2013 (Figure 1). In the past decade, coal consumption more than doubled, surpassing natural gas consumption and becoming the second most consumed fossil fuel as Indonesia turned to less expensive sources of indigenous fuels.2 Indonesia intends to reduce its reliance on petroleum in its energy consumption portfolio to a 25% maximum share while raising the coal and natural gas portions to at least 30% and 22%, respectively, by 2025.3

Indonesia is also a significant consumer of traditional biomass and waste in its residential sector, particularly in the more remote areas that lack connection to the country’s energy transmission networks. In 2013, biomass and waste (which includes firewood and charcoal) consisted of nearly 18% of total primary energy consumption, although its share has declined over the past several years.4 As Indonesia industrializes and expands its electricity and transportation sectors, the country is using more fossil fuels, particularly coal and oil products. Indonesia also plans to leverage the country’s vast renewable sources of hydroelectricity, geothermal, solar, and biomass and waste, to generate electricity for domestic consumption.

Indonesia’s total energy demand is closely linked to the country’s economic expansion. According to World Bank data, Indonesia sustained relatively strong economic performance throughout the global recession, with an average gross domestic product (GDP) growth rate of more than 6% per year between 2007 and 2012, with the exception of 2009 when GDP growth dropped to 4.6%. However, GDP growth started declining after 2012 and fell to 5% in 2014 as a result of weaker demand from trade partners, lower exports, lower commodity prices, and a tighter monetary policy following the government’s decision to raise interest rates substantially between mid-2013 and late 2014.5

Indonesia’s energy sector continues to influence the economy to a large degree, although the decline in oil and natural gas production during the past few years has lowered its impact. Oil and natural gas alone constituted 15% of merchandise exports in 2014, a decline from 23% in 2000.6 In addition, revenues from the oil and gas sector, which historically accounted for about 20% of total state revenues, fell below 20% after 2008 and were less than 12% in 2014, despite high oil prices during most of the year.7 The significant drop in global crude oil prices, which started in June 2014, is expected to reduce Indonesia’s oil and gas revenues by at least one-third in 2015.8 A combination of healthy growth, some market reforms, higher hydrocarbon prices, and a stable government encouraged rapid investment, particularly in the commodity sector until around 2010. Factors that have greatly hindered foreign investment in the past few years include more technically challenging oil and natural gas plays, rising domestic energy demand and accompanying limitations on exports, higher taxes on exploration and production, and lengthier processes to procure and renew contracts.

Despite the government’s emphasis on more private sector involvement in infrastructure expansion, many infrastructure projects continue to be delayed, because regulatory challenges and uncertainties have reduced predictability for foreign investors.

Indonesia’s recently elected government under President Joko Widodo is attempting several energy sector reforms to address the country’s regulatory burdens and lack of legal transparency and to attract much-needed foreign investment for its more capital-intensive and technically challenging energy projects. President Widodo’s new reforms attempt to address corruption and informal markets, streamline the regulatory process for investors, make domestic prices more competitive with international markets, and reduce upstream oil and natural gas costs for investors. However, Indonesia’s energy security policy of retaining more of its hydrocarbon production for domestic use and maintaining local content requirements will continue to hamper investment from international companies.

Petroleum and other liquids

Indonesia’s declining oil production and rising domestic demand resulted in the country’s exit from OPEC in 2009 and higher levels of petroleum imports to meet demand. Indonesia is scheduled to rejoin OPEC in December 2015.

After oil was first discovered in 1885 in northern Sumatra, the hydrocarbon sector became an important part of Indonesia’s economy. Indonesia produced 911,000 barrels per day (b/d) of petroleum and other liquids in 2014, ranking as the 22nd-largest oil producer in the world in 2014 and accounting for about 1% of world production. Although Indonesia’s petroleum and other liquids production has declined over the past two decades, the country continues to export crude oil and condensates within the region. Indonesia is also located along a strategic maritime transit route, the Strait of Malacca, which serves much of East Asia with oil imports from the Middle East.

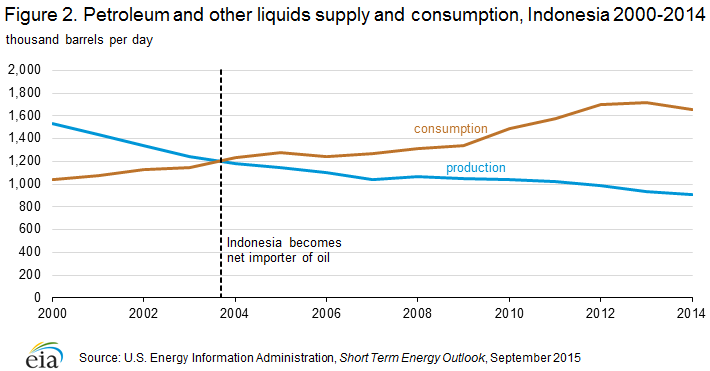

Indonesia is scheduled to rejoin OPEC in December 2015, after suspending its membership in January 2009. Indonesia originally joined OPEC in 1962. The 2009 exit was prompted by growing internal demand for energy, declining production (most notably in mature fields), and limited investment to increase capacity. Indonesia had become a net oil importer by 2004 after domestic demand outstripped production, which has been on a general decline since 1991 (Figure 2). Indonesia claims that rejoining OPEC will strengthen its cooperation with oil-producing countries, provide greater access to crude oil supplies, and allow the country to be a link between energy producers and consumers. Indonesia currently buys crude oil and oil products through third-parties or traders and wants direct access to long-term crude oil supply contracts through negotiations made between national oil companies.9 These crude oil imports are needed to meet expected refining capacity additions from proposed upgrades and expansions slated to come online within the next decade. Indonesia also hopes to attract more infrastructure investment by OPEC members for its upstream and downstream energy infrastructure projects. OPEC notified Indonesia that it plans to accept the country’s request to re-activate its membership with the organization as a full member at the next OPEC meeting in December 2015.10 Indonesia currently imports crude oil and refined products to meet domestic demand.

Sector organization

International oil companies, particularly Chevron and Total, dominate Indonesia’s upstream oil sector. State-owned energy company Pertamina must balance its needs as a corporation against its mandate as a national oil company to meet domestic demand.

International oil companies (IOCs) in the Indonesian oil market include Chevron, Total, ConocoPhillips, ExxonMobil, and BP. Chevron is the largest oil producer in Indonesia, accounting for about 40% of the country’s crude oil production in 2014.11 PT Pertamina (Pertamina), Indonesia’s state-owned integrated energy supply company, accounted for approximately 30% of domestic crude oil production in 2014, according to company data, making the national oil company (NOC) the second-largest oil producer, Other IOCs involved in developing Indonesia’s oil reserves are Total, ConocoPhillips, and ExxonMobil. NOCs, such as the China National Offshore Oil Corporation (CNOOC), PetroChina, and South Korea’s KNOC, also hold upstream assets.12

In addition to its upstream activities, Pertamina operates nearly all of Indonesia’s refinery capacity, procures crude oil and product imports, and supplies petroleum products to the domestic market. Pertamina’s monopoly in the retail market ended in 2004, but the company continued to be the sole distributor for subsidized fuels until early 2010. Pertamina must balance its own needs as a corporation to increase export profits with its mandate as a national oil company charged with meeting domestic demand.

The Indonesian Ministry of Energy and Mineral Resources is responsible for entering into production sharing contracts (PSCs) with interested oil companies. Indonesia’s 2001 Oil and Gas Law significantly restructured Indonesia’s upstream oil and natural gas sector, transferring the upstream regulatory role from Pertamina to BPMigas, a state-owned legal entity that was tasked with managing and implementing PSCs. Although Pertamina continues to be wholly state-owned, the 2001 law also established it as a limited liability corporation in 2003.

SKK Migas, a special task force that is operating until the government amends the 2001 Oil and Gas Law, is tasked with managing and implementing PSCs, determining sellers of government shares of oil and gas, and increasing oil and gas production for domestic demand. The President of Indonesia is ultimately responsible for formulating oil and gas regulatory policy, while parliament provides oversight and consent. Following a corruption case within SKK Migas and arrest of its former chairman in late-2013, the entity lost the right to market the country’s unused oil and gas designated for domestic use within Indonesia. The government transferred exclusive domestic marketing rights to state-owned Pertamina. One of the new government’s proposed reforms is to convert SKK Migas into a state-owned enterprise.13

Exploration and production

Oil production in Indonesia continued to decline in 2014 as there were no major new production projects to offset declines at older fields. Aging infrastructure and fields suggest the country will struggle to meet production targets in the short term.

Indonesia possessed 3.7 billion barrels of proved crude oil reserves at the end of 2014, down from 4 billion barrels two years earlier, according to Oil & Gas Journal (OGJ).14 According to the Indonesian Petroleum Association, replacement of oil reserves had dropped to 47% in 2013 as a result of declining investment in oil exploration, especially in deepwater blocks.15 Petroleum and other liquids (or total liquid fuels) production declined from a high of nearly 1.7 million barrels per day (b/d) in 1991 to an estimated 911,000 b/d in 2014. Crude oil and lease condensate production made up about 790,000 b/d of this total, a level below the government’s revised 2014 target of 818,000 b/d reported in the state budget.

The government’s annual crude oil and lease condensate production target, which has not been reached each year since 2009, is 825,000 b/d for 2015, revised down from an original goal of 900,000 b/d.16 Several factors put downward pressure on Indonesia’s oil output each year, including: licensing approvals at the regional level of government, land acquisition and permit issues, oil theft in the South Sumatra region, aging oil fields and infrastructure, and insufficient investment in unexplored reserves. Indonesia’s two oldest, largest producing fields are Duri and Minas, both located on the eastern coast of Sumatra. Chevron, the operator, has employed enhanced oil recovery (EOR) techniques in both fields to try sustaining output. However, production from these fields continues to decline.

The government expects new production from the Cepu and Ketapang blocks, located in East Java, to peak at the end of 2015. Industry analysts believe this major project could offset some of the declines from mature fields.17 Indonesia also set the 2016 production target between 830,000 b/d and 850,000 b/d as the large Banyu Urip field in the Cepu block is expected to reach its full production and enhanced recovery efforts are likely to stem production declines from mature fields. Banyu Urip is currently the only producing field in the Cepu PSC, which is located in the East Java Basin and is estimated to hold 600 million barrels of recoverable reserves. Banyu Urip reached a production level of about 80,000 b/d by August 2015.18 The partners (ExxonMobil, Pertamina, and local governments) expect Cepu to reach a peak capacity of 205,000 b/d in 2016 and to settle at a plateau production of 165,000 b/d for the following two years.19

Pertamina now faces the combined challenges of stemming oil production declines and meeting domestic demand. Much of the reserves remaining under Pertamina’s control are from mature fields and require enhanced oil recovery (EOR) techniques, currently beyond the technological scope of domestic firms, or the development of basic infrastructure in remote areas of the country (mainly in the eastern region). Partly because of an uncertain regulatory atmosphere and government measures to support local companies, foreign investment in extracting these reserves remains limited. In addition, Indonesia’s domestic operations have been limited by disputes with IOCs operating within Indonesia. Under current regulation, Domestic Market Obligations (DMOs) require that a minimum 25% of oil production be made available to the Indonesian market. This production floor is part of Indonesia’s policy to offset its rising oil imports and serve its domestic needs.

Deepwater exploration and production activity is focused in the Kutei Basin (off the coast of Kalimantan), Western Papua, and the Bonaparte Basin (adjacent to Australia in the Arafura Sea). Chevron, Eni, Niko Resources, Statoil, Total, and Hess are the firms most active in Indonesia’s deepwater field development. Chevron is the largest operator in these areas, managing five of the eight deepwater fields currently in development. Currently, technical and commercial success rates have not spurred further development in these areas.

In an attempt to attract investment for exploration and production, at the beginning of 2015, Indonesia’s Ministry of Finance exempted oil and natural gas exploration activities from the land and building taxes as a means of increasing future supply. This tax has negatively impacted exploration efforts in the country since 2010.20 Indonesia began offering significantly greater shares (35% for oil and up to 40% for natural gas) of production to energy firms awarded any new contracts. Western market analysts still consider the upstream investment environment to be risky, and licensing rounds from the past four years have not attracted as much foreign investment as anticipated. However, the government held another bidding round for 11 conventional and unconventional oil and gas blocks in August 2015 and plans to hold a tender in 2016 for another 21 blocks to attract more investment.21

Refining

Indonesia’s refinery output primarily serves the growing domestic market, although current refining capacity is insufficient to meet demand growth.

Indonesia’s total refinery capacity was an estimated 1.1 million b/d at the beginning of 2015, at six major refineries and a few smaller facilities. The overall utilization rate of these refineries was less than 90% in 2014 (Table 1).22 Pertamina expanded the non-crude capacity of its Cilacap refinery in 2015. The two largest refineries have the capability to process imported sour crude oil, but the other refineries are not as complex.23 Indonesia’s swiftly rising oil demand has put pressure on the government to upgrade its refining capacity to reduce its reliance on more expensive imported oil products. Indonesia is also seeking to enhance refining capabilities to process higher octane gasoline and fuels that meet Euro IV emissions specifications for reduced sulfur content in vehicles.

Indonesia’s petroleum consumption reached nearly 1.7 million b/d in 2014, and refinery output met only about 55% of the consumption of domestic oil products, according to FACTS Global Energy (FGE).24 Oil product imports met the remaining demand. Current refining capacity is insufficient to meet demand growth because there has been a lack of government financial incentives to stimulate foreign investment in the sector. Since the construction of the Balongan refinery in 1994, no new refineries have been built in Indonesia.

Pertamina unveiled its Refinery Development Master Plan to boost total refinery capacity to almost 1.7 million b/d and signed several agreements to partner with international oil companies. The NOC will team with Saudi Aramco on the Dumai, Cilacap, and Balongan refineries, with Sinopec on the Plaju refinery, and with Japan’s JX Nippon Oil on the Balikpapan refinery. Pertamina expects final investment decisions on the projects will occur in 2017 and the upgrades to be complete around 2022. Indonesia also announced plans to build four new refineries, each with capacities of 300,000 b/d through public-private partnerships.25 These capacity additions will require Indonesia to seek more crude oil imports while the gap between the country’s crude oil and condensate output and demand widens.

| Refinery | Operator | Location | Capacity (b/d) |

|---|---|---|---|

| Cilacap | Pertamina | Central Java | 324,000 |

| Balikpapan | Pertamina | East Kalimantan | 242,000 |

| Dumai /Sei Pakning | Pertamina | Central Sumatra | 158,000 |

| Balongan | Pertamina | West Java | 116,000 |

| Plaju/Musi | Pertamina | South Sumatra | 113,000 |

| Tuban (condensate splitter) | TPPI | East Java | 93,000 |

| Cepu | Migas | Central Java | 3,600 |

| Bojonegoro | Tri Wahana Universal (TWU) | East Java | 5,600 |

| Total | 1,055,200 | ||

| Sources: FACTS Global Energy, International Energy Agency, OGJ, company websites | |||

Consumption and distribution

A strong economy, population growth, and state subsidies for fuels have worked together to push domestic oil demand beyond domestic supply. Fuel subsidies have cost the government at least 7% of its annual budget since 2005, pressuring the government to reduce fuel subsidy spending.

A strong economy, population growth, and continued state subsidies for fuels worked together to push domestic oil demand beyond supply. Domestic petroleum consumption totaled about 1.7 million b/d in 2014, steadily rising from 1.3 million b/d in 2007, resulting in higher net imports over the past several years.

In 2014, gasoline and gasoil made up the bulk of demand, each accounting for 37%, according to FGE. Petroleum use declined in the power and industry sectors while it increased in the transportation and household sectors. Indonesian gasoline demand has grown by 79% since 2005, and gasoil demand has grown by 9% over the same time period. Liquefied petroleum gas (LPG) use has increased in the past decade because of government subsidization and price regulation, especially in the residential sector. Liquefied petroleum demand, which made up 10% of oil products demand in 2014, has grown five-fold between 2005 and 2014.26

Fuel subsidies have cost the government from 7% and 27% of its annual public expenditures between 2005 and 2014. High international oil prices before the second half of 2014 and increasing fuel imports made energy subsidies expensive, weighing heavily on Indonesia’s budget. In 2014, the government overshot its budgeted amount by 17% after spending $20 billion on fuel subsidies, according to Indonesia’s Ministry of Finance data.27 To curb oil imports, reduce pressure on the government budget, and free up more capital for infrastructure projects, Indonesian President Widodo took advantage of the lower-price oil environment since June 2014 to drastically reduce government fuel subsidies over the past year. In November 2014, the government reduced gasoline and diesel subsidies by more than 30%, and in January 2015, it eliminated the subsidy on gasoline and introduced a fixed subsidy for diesel at below-market prices.

Trade

Indonesia’s rising domestic demand and waning oil production in the past few years led to increased import levels of both crude oil and petroleum products.

Indonesia has no international oil pipelines and few domestic pipelines, making maritime trade vital. Most petroleum trade is in the form of imports, chiefly motor gasoline and diesel for Indonesia’s transport sector. The country exports a small amount of fuel oil. The country both imports and exports crude oil and is a net crude oil importer as a result of the regional imbalances and growing domestic demand for crude oil use in refineries and for power generation.

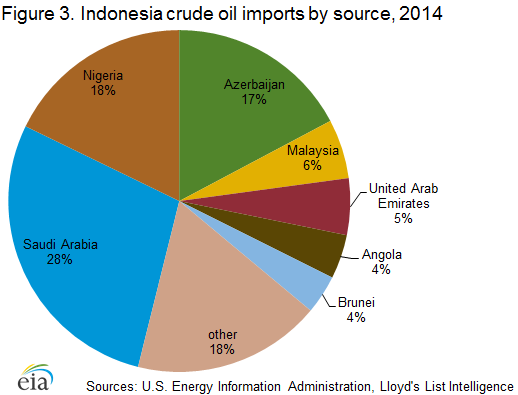

In 2014, Indonesia imported more than 441,000 b/d of crude oil and lease condensate, according to the Analysis of Petroleum Exports (APEX) tanker tracking service of Lloyd’s List Intelligence.28 About 28% of Indonesia’s crude oil imports came from Saudi Arabia (Figure 3). Other significant suppliers included Nigeria (18%), Azerbaijan (17%), Malaysia (6%), United Arab Emirates (5%), Brunei (4%), and Angola (4%).

Indonesia’s net oil product imports remain relatively high as a result of insufficient refining capacity to process the growing demand for oil products. The country’s net oil product imports in 2014 were 592,000 b/d, according to FGE.29 Oil product imports consisted primarily of gasoline (53% of total imports), gasoil for transport and power generation, LPG for residential use, and jet fuel. Pertamina is responsible for purchasing Indonesia’s subsidized gasoline, RON 88 specification gasoline, which currently makes up the largest share of the country’s gasoline demand. Japanese demand for Indonesian fuel oil, which increased after the Fukushima nuclear accident in 2011, subsided in 2013 as Japan increased natural gas and coal imports.

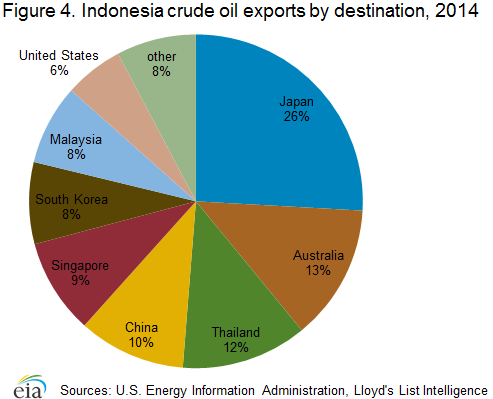

Indonesia continues to export crude oil and condensates even though the country has turned into a net importer of total oil, partly because of a desire to maintain market access and oil revenues. In addition, regional imbalance in the archipelago between oil production and demand centers encourages both imports and exports. In 2014, APEX tanker data estimated Indonesian crude oil exports were roughly 381,000 b/d, primarily to regional buyers (Figure 4).

Natural gas

Natural gas production has increased by more than 11% between 2000 and 2013. While Indonesia continues to be a major exporter of natural gas, domestic consumption growth has increased at a faster pace than production, leaving less natural gas for exports.

Indonesia possessed 103.4 trillion cubic feet (Tcf) of proved natural gas reserves in 2015, down slightly from 104.7 Tcf in 2013, according to OGJ. The country’s proved natural gas reserves are the 13th largest in the world, and the second largest in the Asia-Pacific region, after China, using OGJ data.30 Although Indonesia has a much better reserve replacement for natural gas than for oil, the country is also struggling to replace natural gas reserves at the same rate they are being used. The ratio has dropped to about 90% in 2014 from 127% in 2012.31 The country continues to be a major exporter of pipeline and liquefied natural gas (LNG). At the same time, domestic demand for natural gas has doubled since 2005. The government began constructing new LNG receiving terminals and natural gas transmission pipelines to address domestic gas needs, although this is likely to reduce the natural gas available for export.

Sector organization

The regulatory structure that shapes Indonesia’s upstream oil sector also forms the basis for the natural gas sector. Pertamina accounted for 13% of natural gas production in 2013 through subsidiary Pertamina Gas, according to IHS Energy. IOCs such as Total, Inpex, ConocoPhillips, and ExxonMobil dominate the upstream gas sector. Total, ConocoPhillips, and BP produced more than 50% of gross natural gas in the country in 2013.32 Other upstream investors in Indonesia’s gas sector include various Chinese national oil companies, other international oil and gas companies, and local Indonesian energy firms. State-owned utilities, Perusahaan Gas Negara (PGN) and Pertagas, and a private Indonesian company, TGI, operate all of Indonesia’s transmission activities, while PGN has a monopoly over the distribution lines.33

Exploration and production

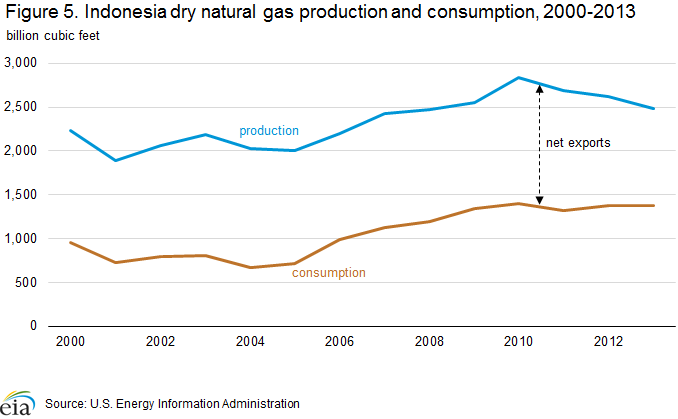

EIA estimates Indonesia produced 2.5 Tcf of dry natural gas in 2013, mostly from offshore fields not associated with crude oil production. In recent years, companies have shifted attention to newer, underexplored offshore areas, particularly in the eastern regions of the country (Figure 5). Production of natural gas grew at an annual rate of about 2.4% from 2000 to 2010 and reached a peak of 2.8 Bcf in 2010 with the commissioning of the Tangguh LNG project. However, production fell by an annual average of 4.4% between 2011 and 2013. The country has struggled to attract foreign investment in more technically challenging and deepwater fields, and exploration has slowed as a result of regulatory hurdles and a lack of fiscal incentives for IOCs. Despite the decrease in production, Indonesia’s 2013 natural gas production was the 12th largest in the world.

Indonesia’s largest natural gas fields are located in the Aceh region of South Sumatra and East Kalimantan. The Mahakam block, located offshore East Kalimantan and operated by Total since 1967, currently accounts for roughly one-fourth of Indonesia’s dry natural gas production and is a key supplier to the Bontang LNG plant.34 As part of Indonesia’s initiative to provide more upstream development opportunities to local firms, the government decided to transfer the ownership and operatorship of the Mahakam block to Pertamina once the production sharing contract expires in 2017. Total and its partner Inpex of Japan each currently hold a 50% equity share, and the government decided that the IOCs can keep a 30% stake in the block.35

Chevron is developing several deepwater fields offshore East Kalimantan in the Kutei Basin that are expected to produce a maximum of 450 billion cubic feet per year (Bcf/y) of natural gas and 58,000 b/d of liquid condensates. The first phase is expected to begin operations in 2016. The project, collectively known as the Indonesian Deepwater Development (IDD), contains three production sharing contracts covering five fields and will be developed over two phases. The fields are expected to supply the Bontang LNG terminal and to meet domestic demand. The majority of the project’s production is expected from the Gendalo and Gehem fields (the second phase), which has been delayed until 2020 as Chevron tries to extend the term length of the PSC and to secure customers.36

In recent years, some companies have shifted their attention toward less explored parts of the country. Pertamina, Malaysia’s Petronas, Thailand’s PTTEP, Chevron, Japan’s Inpex, ConocoPhillips, and Premier Oil are key producers in the West Natuna Basin (Blocks A and B) within the South China Sea. These companies have been producing from these fields since the late 1990s and exporting some of the natural gas through pipelines to Singapore. As of mid-2015, the Indonesian government and project partners (Pertamina, ExxonMobil, France’s Total SA, and PTTEP) had not reached a finalized PSC for the East Natuna block (formerly known as the Natuna D Alpha block). The PSC has been delayed several times since 2011, and the block is technically challenging to develop as a result of its large carbon dioxide concentrations (estimated at more than 70%). Its proved reserves of 46 Tcf are massive and one of the largest in the region.37 For several years, Indonesia has faced military disputes with China over competing claims to the waters off Natuna Island, located in the northern region of Indonesia. China claims some area around Natuna, as part of its “nine dash line“, which overlaps Indonesia’s exclusive economic zone. These territorial disputes, high exploration costs, and current low oil prices could further postpone exploration and development of gas resources in East Natuna.

The Bintuni Bay, located in West Papua, and the Central Sulawesi region are emerging as important new offshore natural gas resource areas. In the area near West Papua, BP oversees proved reserves of 14.4 Tcf that produce gas feedstock for the Tangguh liquefaction facility that began operations in 2009.38 The Arafura Sea in eastern Indonesia is mostly underexplored and contains the Abadi gas field, estimated to have reserves between 10 and 14 Tcf.39 This field is being developed to feed the Abadi floating LNG terminal now slated to come online in 2022, three years later than expected.

Increasing domestic demand for natural gas continues to reduce Indonesia’s capacity for exports, and the country might not be able to meet its external obligations. Moreover, Indonesia’s geography presents a challenge to resource development and makes the switch to natural gas for domestic consumption more difficult. The nation’s most prolific blocks of natural gas reserves are located far from its major demand markets, and regulatory uncertainty has delayed the investment needed for exploration. Several IOCs have requested 20-year extensions from Indonesia’s government for many PSCs as a result of the long process for obtaining licenses and exploration of these deepwater areas. Foreign upstream investment in PSC areas declined in recent years, and the number of signed PSCs signed dropped from 25 new oil and natural gas contracts in 2012 to 7 in 2014.40 Also, certain companies have relinquished their interest in some exploration and production contracts after failing to discover economically viable reserves or have scaled back on capital expenditures in deepwater exploration plays as a result of much lower oil prices.

Natural gas associated with oil production is often flared when there is no infrastructure in place to make use of the gas. Indonesia ranked 13th in global natural gas flaring in 2012, according to the Global Gas Flaring Reduction Partnership (GGFR).41 According to Indonesian statistics, natural gas flaring rose after 2010 even though production declined overall. Indonesia’s lack of adequate natural gas pipelines and infrastructure and its insufficient regulatory oversight have contributed to rising levels of gas flaring.

Coal bed methane and shale gas

Indonesia’s government promotes exploration for coal bed methane (CBM) and shale gas, in addition to conventional crude oil and natural gas. The Ministry of Energy and Mineral Resources estimates that the country has CBM reserves of 453 Tcf based on preliminary studies. In 2008, the Indonesian government started awarding CBM blocks in the South and Central Sumatra basins on Sumatra Island and in the Kutei and Barito basins in East Kalimantan. The CBM production rate in 2014 was less than 1 Bcf/y, substantially lower than the government’s original target for 2015 production (183 Bcf/y). Production levels have been lower than anticipated because of regulatory hurdles, environmental issues, and limited demand. As a result, Indonesia substantially lowered its 2015 CBM production target to about 3 Bcf/y.42

There is currently no shale gas production in Indonesia, but policymakers are interested in exploring the country’s shale oil and shale gas potential. In April 2012, the Indonesian government initiated four shale gas study projects and expects commercial shale gas production to begin by 2020. As of August 2015, Indonesia had held two bidding rounds for unconventional oil and gas blocks and had awarded several shale gas PSCs over the past two years for onshore fields in North Sumatra and South Sumatra. EIA estimates that Indonesia possesses 46 Tcf of total recoverable shale gas resources in South and Central Sumatra, East Kalimantan, and the eastern province of Bintuni. A major challenge to the growth of the shale industry is the cost of exploration in Indonesia. This cost is estimated to be as much as four times the drilling cost in North America because the deposits are deeper than those in the United States. The lack of sufficient natural gas distribution networks is also a hindrance to any large-scale shale gas development. Indonesia forecasts that its shale gas will commence production by 2018.43

Consumption and distribution

Natural gas production in Indonesia initially was exported, but the country’s declining oil production led producers to shift increasing gas volumes toward domestic consumption. In 2013, Indonesia consumed almost 1.4 Bcf of natural gas, or slightly more than half of its total dry gas production. The industrial sector and the power sector account for the largest portions of domestic consumption (54% and 24%, respectively, in 2013). Demand from the industrial sector is likely to expand as a result of much lower Asian natural gas spot prices compared to 2014, and new regasification capacity allowing the country to supplement its indigenous production with imports. The country’s power sector is also expected to consume more natural gas as the government plans to add 13 GW of gas-fired capacity by 2020 and replace relatively expensive diesel-fired power. However, coal still remains the dominant and more economic fuel in the power sector and is likely to be prioritized over natural gas. Indonesia’s Ministry of Energy and Mineral Resources stipulates that gas supply must be allocated to the needs of enhanced oil recovery, the fertilizer industry, and the power sector before any other sectors.44

Pursuant to a Domestic Market Obligation (DMO) stipulated in Indonesia’s government regulations, 25% of natural gas produced from production-sharing contracts in Indonesia must supply the domestic market. The government has imposed larger obligations in recent specific contracts. For example, the planned Donggi-Senoro LNG received government approval only after the developers designated 25%-30% of the output explicitly for domestic consumption.

State-owned Perusahaan Gas Negara (PGN) controls the midstream gas market and the transmission market, operating more than 3,800 miles of natural gas transmission and distribution pipelines.45 However, domestic distribution infrastructure is almost non existent outside of Java and North Sumatra. PGN began operating the South Sumatra-West Java pipeline in 2008, providing an important link between the gas-producing region of South Sumatra and the densely populated market of West Java. The Grissik-Duri pipeline is another important domestic transmission pipeline, as it provides natural gas to Chevron’s Duri oil field for its steam flooding and for power generation activities in the regional market.

Natural gas pipeline exports

Although the majority of Indonesia’s natural gas exports are transported as LNG, Indonesia sends about a fourth of its gas exports to Singapore and Malaysia through two pipeline connections: one from its offshore fields in the West Natuna Sea and the other from the Grissik gas processing plant in South Sumatra. In 2014, Indonesia exported about 336 billion cubic feet per year (Bcf/y) via pipeline (30% of its total exports), with more than 230 Bcf/y sent to Singapore.46 These pipelines deliver gas to Singapore under two long-term contracts, both set to expire by 2024. However, SKK Migas reported that Singapore plans to end natural gas purchases from Indonesia’s pipeline exports once these contracts expire.47 This reduction in exports should allow Indonesia to keep more supply for domestic use in the next few years.

Liquefied natural gas

Indonesia was the fifth-largest LNG exporter in 2014, following Qatar, Malaysia, Australia, and Nigeria. Expected growth in natural gas demand led the government to pursue policies that secure domestic natural gas supplies for the local market.

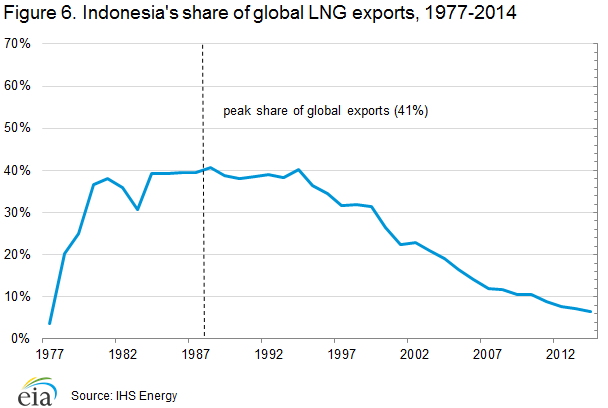

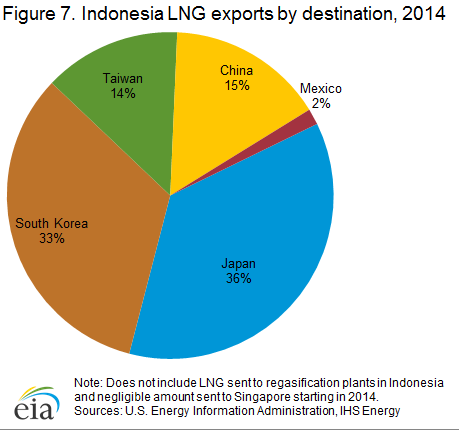

After accounting for more than a third of global LNG exports in the 1990s, Indonesia’s share of the global market now is less than 7%. In 2014, Indonesia exported approximately 762 Bcf of LNG, down from 816 Bcf in 2013, according to IHS Energy (Figure 6).48 Mostly a regional supplier to South Korea, Japan, Taiwan, and China, Indonesia has lost market share in recent years to other LNG producers including Qatar, Malaysia, Australia, and Nigeria (Figure 7). Indonesia was the world’s fifth-largest exporter of liquefied natural gas (LNG) in 2014. Indonesian LNG exports to Japan fell by more than 50% from 2010 to 2014, as export contracts with Japan expired and Indonesia diversified its markets.49

Indonesia began shipping LNG between its liquefaction facilities and the country’s first regasification terminal in 2012. The government has sought to meet the increasing gas demand by raising the country’s regasification capacity, which reached 412 Bcf by the start of 2015 (Table 3). Indonesia has plans to import LNG from other countries by 2018. Indonesia signed its first two gas import contracts with Cheniere Energy (United States) to receive a total of 72 Bcf/y of LNG for 20 years starting in 2018 from the company’s planned Corpus Christi liquefaction terminal, located in the Gulf Coast of the United States.50

The shift to being a natural gas importer is emblematic of the country’s decreasing natural gas production in recent years and increasing domestic demand. Although the country still exports significant quantities of LNG, export volumes have fallen by 44% since 1999, and internal economic growth has stimulated higher levels of natural gas consumption.51

Indonesia has three liquefaction plants with a combined operating production capacity of 1.3 trillion cubic feet per year (Tcf/y) (Table 2).52 A lack of sufficient gas reserve additions in the Arun field in North Sumatra resulted in declining LNG exports from the former Arun liquefaction plant in recent years. Pertamina converted the facility to a regasification terminal in late 2014. The Donggi-Senoro LNG terminal, located in Central Sulawesi, is the newest plant, and it was commissioned in mid-2015. At least 25% of the new capacity coming online in Indonesia is slated to supply the domestic market.53

The government intends for the current regasification facilities to serve the domestic electricity plants and industrial customers in Java and Sumatra (Table 3). Most of the country’s proposed regasification capacity is located in Java. In the eastern regions of the country, where there is a small but growing demand for natural gas, Pertamina and PLN (Indonesia’s state electricity firm) announced plans to develop several small mini-LNG terminals with a total capacity of less than 50 Bcf/y.

| Project name | Owners | Peak output (Bcf/y) | Target start year |

|---|---|---|---|

| Existing LNG terminals | |||

| Nusantara FSRU1 | Pertamina 60%, PGN 40% | 182 | Operational |

| Lampung FSRU | PGN | 86 | Operational |

| Arun LNG | Pertamina 70%, Aceh regional government 30% | 144 | Operational |

| Planned projects | |||

| Tangguh LNG expansion | Petronas | 182; 1 train | 2019 |

| Abadi Floating LNG2 | Shell 35%, Inpex 65% | 120; 1 train | 2022 |

| 1 A train is an independent unit for liquefaction and purification. 2 A floating terminal is one above an offshore gas field that produces, liquefies, stores, and transfers natural gas. Sources: IHS Global Insight, FACTS Global Energy, International Energy Agency, company websites |

|||

| Project name | Owners | Peak output (Bcf/y) | Target start year |

|---|---|---|---|

| Existing LNG terminals | |||

| Bontang | Pertamina | 811; 6 trains1 | Operational |

| Tangguh | BP 37%, CNOOC 14%, Japanese companies 46%, Talisman Energy 3% | 365; 2 trains | Operational |

| Donggi-Senoro | Mitsubishi 45%, Pertamina 29%, KOGAS 15%, Medco 11% | 98; 1 trains | Operational |

| Projects under construction | |||

| Sengkang LNG | Energy World Corporation | 48 | Q4 2015 |

| Planned projects | |||

| Cilacap FSRU | Pertamina | 38 | 2017 |

| Cilamaya FSRU | Pertamina | 24 | 2018 |

| Baten /Bonjonegara LNG | Pertamina | 182 | 2019 |

| Tanjung Benoa LNG | Pertamina | 19 | 2016 |

| 1 Floating Storage Regasification Unit that receives and converts the LNG offshore. Sources: IHS Global Insight, FACTS Global Energy, International Energy Agency, company websites |

|||

Coal

Indonesia exports nearly 80% of its coal production, making the country the world’s largest exporter of coal by weight.

Indonesia plays an important role in world coal markets, particularly as a regional supplier to Asian markets. It has been the largest exporter of thermal coal, typically used in power plants, for several years. In 2011, it overtook Australia as the world’s largest exporter of coal by weight. In 2014, Indonesia was the world’s largest exporter of thermal coal, with nearly 80% of production leaving the country.54 However, declining international coal prices since 2011 and the drop in global demand, particularly from China, have negatively impacted Indonesia’s coal production and revenues since 2013.

Sector organization

Indonesia’s Ministry of Energy and Mineral Resources oversees the coal sector and sets the country’s thermal coal reference price. The government passed the 2009 Law on Mineral and Coal Mining No.4 to stimulate development of the domestic mineral processing industry and to increase foreign investment in the mining sector. The law introduced more transparent and standardized tenders and licenses for mining blocks. Also, the regulation decentralized the licensing process, allowing local governments to approve licenses for smaller mines. This regulation allowed easier access to smaller mining operations in Indonesia to produce and send coal to the growing export markets in the region.

Indonesia is seeking to retain greater revenues from its coal mining industry. In early 2012, the government declared that all foreign investors must sell a majority of existing mine equity to local investors by the 10th year of production.55 The government is also considering raising royalty rates paid by a third of Indonesia’s mining operation permit holders. The rate increase was postponed in mid-2015 because many smaller mines were cutting production and closing operations as they struggled with negative cash flows.56 Other policy changes under discussion are to ban exports of low-calorific value coal (coal that has undergone minimal processing) and increase the calorific value of coal. Although the coal upgrade technology is lacking and expensive which would pose challenges for small and medium-sized coal producers.

In response to the increasing coal demand in the domestic market, Indonesia imposed a domestic market obligation on large coal producers in 2010, establishing caps each year for the amount of coal that must be allocated for domestic sales. According to IHS Energy, the 2013 domestic market obligation cap was set at 82 million short tons, which was about 18% of total coal production. The primary beneficiary of this policy is the electric power sector, as the government seeks to improve electrification rates in the country. The government aims to boost the country’s coal-fired capacity over the next five years through its latest electricity expansion program and intends to increase DMO requirements from 20% to 25% of total production.57

PT Bumi Resources is Indonesia’s largest mining company and coal producer, with an output of 88 million short tons in 2013. PT Kaltim Prima Coal (KPC), a subsidiary of PT Bumi Resources, a large Indonesian mining company, owns one of the largest coal mines in the world. PT Adaro is the second-largest coal producer, responsible for nearly 60 million short tons of coal in 2013. Other major producers in the country include PT Kideco Jaya, PT Indotambang Raya Megah, and PT Berau. The top five producers in Indonesia accounted for more than 45% of coal production in 2013.58

Exploration and production

Indonesia’s coal production, mostly bituminous and sub-bituminous, has climbed sharply over the past decade.

According to Indonesia’s government, the country had 34.6 billion short tons of recoverable coal at the beginning of 2013, located primarily in South Sumatra, East Kalimantan, and South Kalimantan.59 Indonesian coal is primarily bituminous or sub-bituminous in rank, and the country produces a small amount of lignite used by the power sector. Approximately two-thirds of Indonesia’s coal production comes from East Kalimantan.60

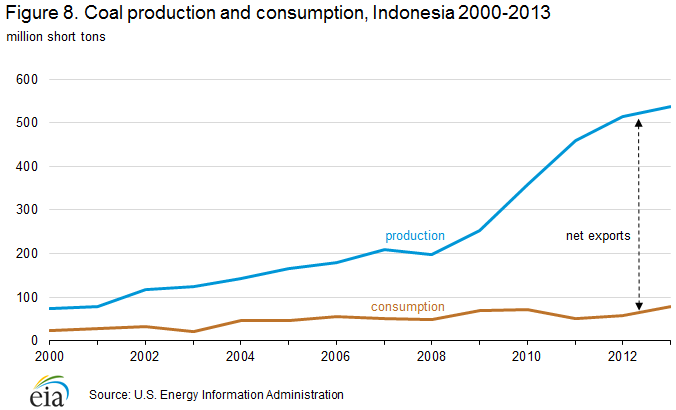

Coal production quadrupled over the past decade from 125 million short tons in 2003 to 538 million short tons in 2013. This increase was the result of a sharp growth in demand particularly in Asia, where coal had a competitive advantage over higher-priced oil and natural gas (Figure 8). According to the Indonesian Coal Mining Association, supply began to decline in 2014 as international coal prices continued to drop, which resulted in financial losses for small operations.61

According to the International Energy Agency, about 77 million short tons of coal were produced illegally from small mining operations in 2013.62 To ensure more transparency and reduce illegal economic gain, the government has proposed limiting exports from 14 ports.63 Also, in October 2014, Indonesia began requiring exporting licenses to further manage state revenues paid through royalties and taxes and to manage the amount of exports that leave the country.64

Consumption

Indonesia’s government encourages the use of coal in the power sector because of the relatively abundant domestic supply. Coal use also reduces the use of expensive diesel and fuel oil.

Indonesia’s coal consumption grew to 79 million short tons in 2013. The electricity sector is the largest source of domestic coal consumption. Power plants accounted for about 70% of total coal sales in recent years, while the remainder was used in industries.65 Electricity sector demand for coal is expected to increase in the next few years as a result of additions to coal-fired generation capacity.

Unlike many other countries, Indonesia’s government encourages increased use of coal in the power sector, because of the relatively abundant domestic supply. Coal use also reduces the use of expensive diesel and fuel oil to generate electricity. Although coal consumption has grown significantly in the past decade, most production has been exported. To guarantee sufficient domestic supply, the Indonesian government sets a DMO each year based on projected demand.

Trade

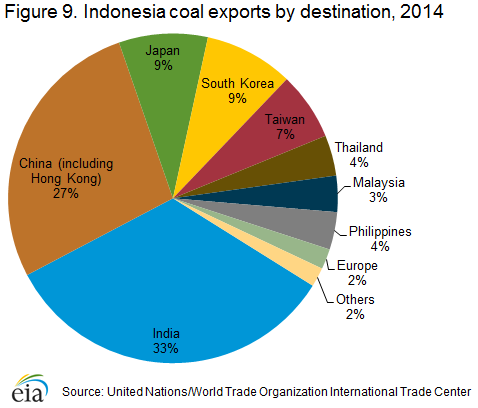

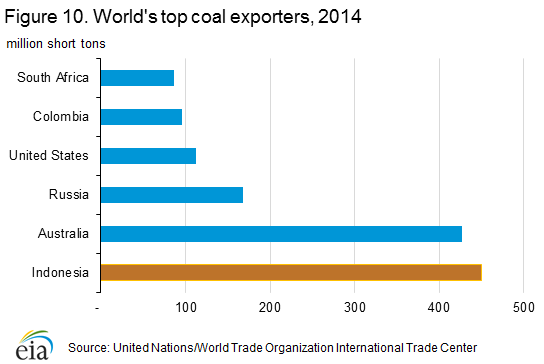

In 2014, Indonesia exported about 450 million short tons of coal, making it the world’s largest exporter of coal by weight, according to the International Trade Center (Figure 10). Exports declined in 2014 from a high of 467 million short tons in 2013. Indonesia has become increasingly important as a source for Chinese coal imports over the past few years. According to Indonesia’s Coal Mining Association, exports declined slightly in 2014 as Indonesia’s smaller mines ceased operations following declining global coal prices and falling revenues. In addition, China’s coal imports fell as its industrial manufacturing sector slowed and as stricter environmental standards were imposed on lower quality coal. Indonesia’s coal exports primarily serve Asian markets, with about 85% of total coal exports sent to China, Japan, South Korea, India, and Taiwan (Figure 9). In 2014, India became the largest importer of Indonesian coal, surpassing China.66

Electricity

Electricity

Although Indonesia’s electricity generating capacity doubled in the past decade, the country has a low electrification ratio compared to countries with similar income levels. In 2014, about 84% of Indonesia’s population had access to electricity compared to less than 68% in 2010, according to state-owned electric utility Perusahaan Listrik Negara (PLN).67 Indonesia’s 2014 National Energy Policy aims to nearly complete the electrification of the country by 2020. Eastern Indonesia lags behind the western area of the country, with some provinces such as Papua only providing electricity to 43% of its population.68 Because capacity growth has not kept pace with electricity demand growth, grid-connected areas have also suffered from power shortages. Inadequate supporting infrastructure, difficulty obtaining land-use permits, subsidized tariffs, and an uncertain regulatory environment all contribute to insufficient generation.

Sector organization

PLN is the most significant company in Indonesia’s electric power sector. It owned and operated about 70% of the country’s generating capacity through its subsidiaries as of 2014 and maintains an effective monopoly over distribution activities.69 Although the most recent 2009 Electricity Law ends PLN’s distribution monopoly, regulations are not in place to enforce this law.

The government regulates consumer electricity prices below market levels, forcing PLN to accept losses. To ameliorate the effect of this policy on the state’s vertically integrated utility, Indonesia raised prices in 2013 by 15%.70 This move was also intended to reduce government subsidies to PLN. In lieu of subsidies, the government has sought to raise tariffs in the power sector to provide price security to PLN and to private investors. Also, feed-in tariffs exist for geothermal, solar, and waste-to-energy power.

The government is seeking to stimulate foreign investment in the power sector by mandating PLN to offer guaranteed power purchase agreements (PPAs) for independent power producers (IPPs) as part of its supply portfolio. The government projects that IPPs will construct nearly 60% of the power capacity in the latest government program to add 35,000 megawatts (MW) of power by 2019.71

Generation

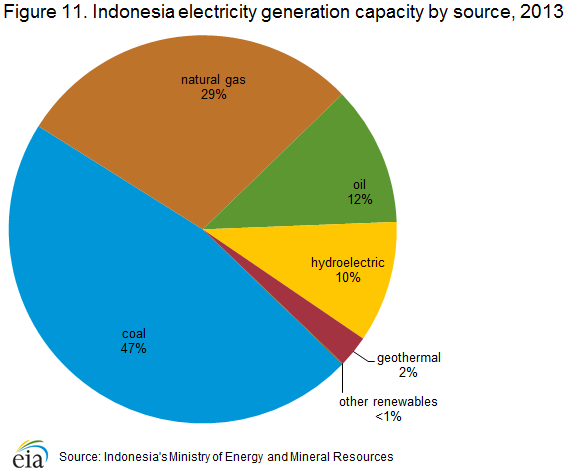

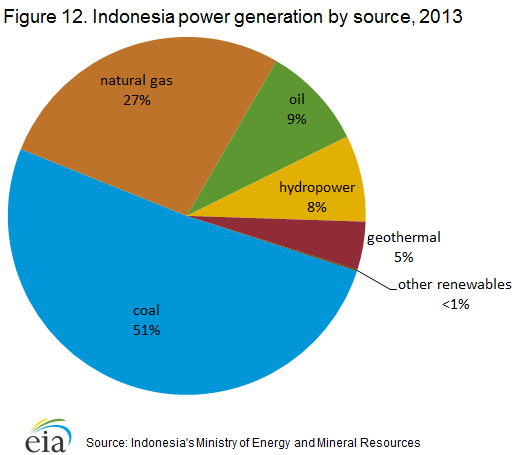

Indonesia had an estimated 51 gigawatts (GW) of installed capacity and generated 229 billion kilowatthours (kWh) in 2013, according to Indonesia’s Ministry of Energy and Mineral Resources and PLN data (Figure 11).72 In 2013, about 88% of the power generation came from fossil fuel sources, with the rest coming from hydroelectric (8%) and geothermal (5%) (Figure 12). Coal accounted for slightly more than half of the power generated from fossil fuels. Oil-fired generation has declined along with Indonesia’s oil production.

In its latest energy policy established 2014, the Indonesian government set a national goal that 100% of households will have electricity by 2020. To address the capacity shortage and alleviate bottlenecks in more developed areas in Java, the policymakers embarked on a fast-track plan in 2006, designed to accelerate power plant development. Phase one of this plan includes 10 GW of new coal-based generation. After delays of this project from its original completion date of 2010, the country has added 8.1 GW of coal-fired capacity in this phase and plans to complete the first-phase additions by 2015, according to PLN.73 The second phase of nearly 18 GW of capacity additions include cleaner energy sources such as natural gas, geothermal, hydroelectricity, and other renewables, although coal-fired generation capacity still makes up more than 60% of this phase. According to PLN, this additional capacity is planned to come online by 2022, although the second phase has also encountered project delays. In mid-2015, President Jokowi Widodo announced an ambitious electric capacity target to install 35 GW through 2019, about 20 GW from coal-fired capacity, 13 GW from natural gas-fired plants, and 3.7 GW from renewable sources (primarily hydroelectricity and geothermal resources).74

Indonesia’s primary power consumers are residential (42% market share), industrial (33%), and commercial (18%).

Geothermal and other renewables

Plans to increase the use of total renewable energy (including hydropower) to 19% of the total energy portfolio by 2019 and to a minimum of 23% by 2025 depend heavily on developing the country’s geothermal and hydropower resources.75 The Ministry of Energy and Mineral Resources has estimated that Indonesia has a potential 29 GW of geothermal capacity, only 5% of which has currently been developed.76 One impediment to development has been the definition of geothermal development as a mining activity, which restricted new projects in conservation areas. Indonesia passed a new Geothermal Law in 2014 that eliminated this regulation for geothermal development. The law also attempts to raise investment in geothermal projects by making the price more closely match developments costs. Also, the law limits the permitting process to review only by the central government and alleviates land acquisition issues by providing benefits for the local populations.77

Indonesia’s power sector is notable for significant levels of geothermal power. Indonesia is the third-largest geothermal energy generator in the world, behind the United States and the Philippines. Indonesia added about 540 megawatts (MW) of geothermal capacity in the decade leading up to 2013, bringing its installed electric capacity to more than 1.3 GW. Indonesia’s current geothermal plants are scattered around Java, North Sumatra, and North Sulawesi and make up less than 3% of total installed generation capacity.78 To promote geothermal development, the country’s fast-track electrification plan calls for an additional 5 GW of geothermal capacity by 2022, to be operated primarily by IPPs and private companies.79 The new government’s 35 GW Electricity Program, launched in mid-2015, includes 1.2 GW of additional geothermal capacity by 2019. The government signed a cooperation agreement with New Zealand in 2012 for joint development of geothermal energy projects.80 PT Medco Power Indonesia plans to commission the 330-MW Sarulla power plant, which will be the world’s largest geothermal plant by 2018.81

Hydropower consisted of about 10% of the total generation capacity in 2013, and there has been little growth from this energy source in the past decade. Indonesia plans to develop several mini-hydropower plants, adding about 2 GW of capacity by 2019.82 Indonesia has a small but growing electricity capacity of other renewables such as solar, wind, and biomass energy. The government strongly supports investment in these plants, particularly in more remote areas, to further increase the country’s electrification rate.

Notes:

- Data presented in the text are the most recent available as of October 7, 2015.

- Data are EIA estimates unless otherwise noted.

Endnotes:

1The World Bank, Data: Indonesia (Accessed July 2015).

2Indonesia’s Ministry of Energy and Mineral Resources, 2014 Handbook of Energy & Economic Statistics of Indonesia, pages 10-11 and 20-21.

3PricewaterhouseCoopers, “2014 Negative Investment List – the end of an era for the oilfield service sector,” page 3; and International Energy Agency, “Energy Supply Security 2014 – Indonesia,” page 7 and Policies and Measures: National Energy Policy (Government Regulation No. 79/2014).

4Indonesia’s Ministry of Energy and Mineral Resources, 2014 Handbook of Energy & Economic Statistics of Indonesia, pages 10-11 and 20-21.

5World Bank data: GDP growth (accessed August 2015).

6Newsbase AsianOil, “Indonesia looks to OPEC for economic panacea,” May 13, 2015 and Jakarta Post, “Energy and Economic Growth,” July 15, 2010.

7PricewaterhouseCoopers, “Oil and Gas in Indonesia Investment and Taxation Guide 2014,” May 2014, page 13.

8Reuters, “Hit to Indonesia’s oil and gas revenue threatens deficit, crude output,” April 30, 2015.

9Platts McGraw Hill Financial, “Indonesia eyes OPEC crude in push to replace third-party supplies,” June 16, 2015.

10Newsbase, AsianOil, “Indonesia looks to OPEC for economic panacea,” May 13, 2015, pages 3-4 and Reuters, “OPEC says Indonesia to rejoin oil group after 7-year break,” September 8, 2015.

11Chevron Indonesia (website accessed July 2015).

12Indonesia Investments, “Indonesian Companies: Pertamina,”; and Pertamina Annual Report 2014; and PricewaterhouseCoopers, “Oil and Gas in Indonesia Investment and Taxation Guide 2014,” May 2014, page 11.

13Katadat, “Discussion of SKK Migas’ Fate narrowed to be Special State-owned Firm ,” July 29, 2015.

14Oil & Gas Journal, “Worldwide Look at Reserves and Production, December 1, 2014.

15The Jakarta Post, “Energy crisis: Needs urgent action now,” September 18, 2014.

16Newsbase, AsianOil, “Indonesia’s oil production tops 800,000 bpd in April,” April 15, 2014, page 7; and Indonesia-Investments, “Crude Oil Production Indonesia: Difficult to Meet 2014 Oil Lifting Target,” August 8, 2014.

17Newsbase AsianOil, Indonesia sets 2016 oil gas production targets,” June 17, 2015, page 12.

18International Energy Agency, Oil Market Report, “Indonesian comeback?,” June 11, 2015, page 27; The Jakarta Post, “Banyu Urip ramps up output to 75,000 bopd,” April 9, 2015; Rigzone, “Indonesia Plans to Offer 21 Oil, Gas Blocks for Tender in 2016,” September 3, 2015.

19Newsbase AsianOil, “Indonesia’s import dependency drives OPEC bid,” June 24, 2015.

20Jakarta Post, “Tax bill killing drive to find new reserves in Indonesia,” July 22, 2015.

21Reuters, “Indonesia increases investor share for oil, gas blocks amid low oil prices,” September 11, 2015.

22FGE, Asia Pacific Databook 2: Refinery Configuration & Construction, pages 49-51; FGE Asia Pacific Databook 3: Oil Product Balances, page 29.

23International Energy Agency, Energy Supply Security 2014: Indonesia, page 11; and Jakarta Post, “Bid for cleaner fuel blocked by Pertamina,” August 22, 2015.

24FGE, Asia Pacific Databook 3: Oil Product Balances, page 32.

25Platts McGraw Hill Financial, “Indonesia’s Pertamina signs agreements on refinery upgrades,” December 10, 2014; and Platts McGraw Hill Financial, “Indonesia eyes crude oil imports from Iran amid refining expansion plans,” May 28, 2015; and Jakarta Post, “Oman set to develop new oil refinery complex in Riau,” May 29, 2015.

26FACTS Global Energy, Asia Pacific Databook 3, Spring 2015, page 32.

27International Institute for Sustainable Development (IISD), A Citizen’s Guide to Energy Subsidies in Indonesia, page 5 and IISD, Indonesia Energy Subsidy Review, Issue 1, Volume 2, March 2015, page 4.

28Lloyd’s Intelligence List, APEX tanker tracking database (accessed August 2015).

29FGE, Asia Pacific Databook 3: Spring 2015, page 32.

30Oil & Gas Journal, Worldwide Look at Reserves and Production, December 1, 2014. Note: Australian government claims a much higher commercial reserve capacity than OGJ reports placing Indonesia as the third-largest for reserves in the Asia-Pacific region.

31McKinsey & Company, “Ten ideas to reshape Indonesia’s energy sector,” September 2014, page 4; and The Jakarta Post, “Energy crisis: Needs urgent action now,” September 18, 2014.

32IHS Energy, Indonesia Market Profile, May 28, 2015, pages 15-16.

33International Energy Agency, Energy Supply Security 2014: Indonesia, pages 20-21.

34IHS Energy, “Indonesia: The fate of Mahakam and implications for Pertamina,” December 3, 2014, page 2.

35Newsbase AsianOil, “Indonesia says Total, Inpex can retain 30% Mahakam stake,” June 24, 2015.

36Platts McGraw Hill Financial, “Indonesian gas project delays,” March 25, 2015; and Chevron website: Indonesia (accessed September 2015).

37Jakarta Post, “Govt looks to approve East Natuna bid,” August 14, 2013; Platts McGraw Hill Financial, “Pertamina seeks 50-year PSC for East Natuna gas block,” May 8, 2012.

38IHS Energy, “Tangguh LNG Liquefaction Profile,” March 13, 2015, page 4.

39IHS Energy, “Abadi LNG Liquefaction Profile,” November 4, 2014, page 22.

40Rigzone, “Indonesia plans to offer more oil, gas blocks for bidding this year,” May 25, 2015.

41World Bank Global Gas Flaring Reduction Partnership (GGFR) (accessed September 2015).

42Jakarta Post, “CBM could redraft Indonesia’s energy charts,” April 21, 2014; PricewaterhouseCoopers, “Oil and Gas in Indonesia Investment and Taxation Guide 2014,” page 12; Indonesia Investments, “Coalbed Methane Production in Indonesia Far from Successful,” March 2014.

43Shale Gas International, “Indonesia signs four contracts for unconventional oil and gas exploration,” May 27, 2015.

44International Energy Agency, “Energy Supply Security 2014: Indonesia,” page 20.

45PT PGN Annual Report 2014, page 125.

46BP Statistical Review of World Energy 2015.

47Antara News, “Singapore to stop gas imports via pipelines from Indonesia,” January 29, 2014 and IHS Energy, “Singapore Market Profile,” June 8, 2015, page 15.

48IHS Energy, “Annual LNG Trade,” May 7, 2015.

49IHS Energy, “Annual LNG Trade Data,” May 7, 2015 and BP Statistical Review of World Energy 2015.

50Platts McGraw Hill Financial, “Indonesia’s Pertamina secures more US LNG as it prepares for gas shortage,” July 2, 2014.

51IHS Energy, “Annual LNG Trade Data,” May 7, 2015.

52IHS Energy, “Liquefaction Database,” May 27, 2015.

53IHS Energy, “Tangguh LNG Liquefaction Project Profile,” 2015, page 6; and Jakarta Post, “Donggi-Senoro LNG plant ready for operation,” May 12, 2015 and IHS Energy, “Donggi Senoro LNG Liquefaction Project Profile,” January 22, 2015.

54Energy Information Administration; Indonesia’s Ministry of Energy and Natural Resources, 2014 Handbook of Energy & Economic Statistics of Indonesia, page 63, and UN/WTO International Trade Center database.

55The Globe and Mail, “Indonesia limits foreign ownership of mines,” September 6, 2012.

56IEA, Medium-Term Coal Market Report 2014, page 90; and Indonesia Investments, “Government of Indonesia Postpones the Coal Royalty Hike,” July 23, 2015.

57IHS Energy, Indonesia Coal Profile, March 2015, pages 4 and 8; and Oxford Business Group, “Lower commodities prices and regulations pressuring Indonesia’s coal industry, 2015.

58EIA estimates using IHS Energy, Indonesia Coal Profile, March 2015, page 12.

59Indonesia’s Ministry of Energy and Natural Resources, 2014 Handbook of Energy & Economic Statistics of Indonesia, page 62.

60International Energy Agency, Medium-Term Coal Market Report 2014, page 32-33, 90.

61Indonesia Investments, “Coal Mining Update Indonesia: Coal Production to Fall in 2015,” April 29, 2015.

62International Energy Agency, Medium-Term Coal Market Report 2014, page 90.

63Indonesia Coal Mining Association, “To prevent the illegal export of coal, 14 coal port in Kalimantan and Sumatra will be renovated,” July 2, 2014.

64Indonesia Investments, “Indonesia Coal Update: Export, Production and New License System,” October 13, 2014.

65IHS Energy, Indonesia Coal Profile, March 2015, page 9

66UN/WTO International Trade Center database (accessed September 2015).

67PT PLN Annual Report 2014, page 8.

68Tempo.co, “Govt’ Targets 99 Percent Electrification Rate,” January 21, 2015.

69International Energy Agency, “Energy Supply Security 2014: Indonesia,” page 28.

70International Energy Agency, “Energy Supply Security 2014: Indonesia,” page 27.

71The Jakarta Post, “PLN to spend $22.5 billion on power plants,” November 4, 2014.

72PLN Annual Report 2014, page 16.

73PLN Annual Report 2014, page 110.

74Tempo.co, “Jokowi to Launch 35,000 MW Electricity Program,” May 4, 2015.

75PricewaterhouseCoopers, “2014 Negative Investment List – the end of an era for the oilfield service sector,” page 3; and International Energy Agency, “Energy Supply Security 2014 – Indonesia,” page 7; and CleanTechnica, “Indonesia Sets 19% Renewable Energy Target For 2019,” June 11, 2015.

76PLN 2014 Handbook of Energy and Economic Statistics of Indonesia, page 97.

77The Jakarta Post, “Legal barrier to geothermal development removed,” August 27, 2014.

78Ministry of Energy and Mineral Resources, 2014 Handbook of Energy and Economic Statistics of Indonesia, page 86.

79Ministry of Energy and Mineral Resources, 2014 Handbook of Energy and Economic Statistics of Indonesia, page 86 and 112-113.

80New Zealand Herald, “Indonesia provides geothermal opportunity,” April 16, 2012.

81PR Newswire, “The 330 MW Sarulla Geothermal Power Project in Indonesia Signed Project Agreements,” April 4, 2013.

82Tempo.co, “Jokowi to Launch 35,000 MW Electricity Program,” May 4, 2015.