US Refineries Running At Record High Throughputs – Analysis

By EIA

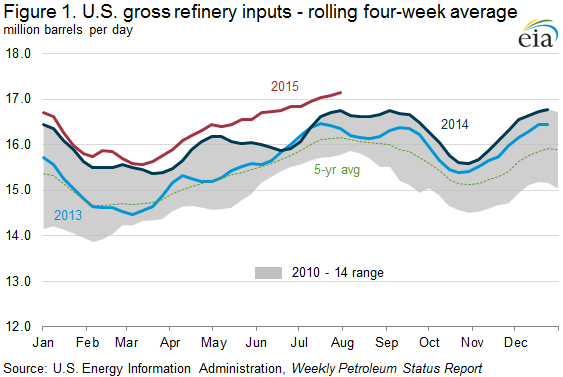

Gross inputs to U.S. refineries exceeded 17 million barrels per day (b/d) in each of the past four weeks, a level that had not previously been reached or exceeded in any given week since EIA began publishing the data in 1990. The rolling four-week average of U.S. gross refinery inputs has been above the five-year range every week so far this year (Figure 1).

The record high gross inputs reflect both higher refinery capacity and higher utilization rates. Lower crude oil prices and strong demand for petroleum products, primarily gasoline, both in the United States and globally have led to favorable margins that encourage refinery investment and high refinery runs.

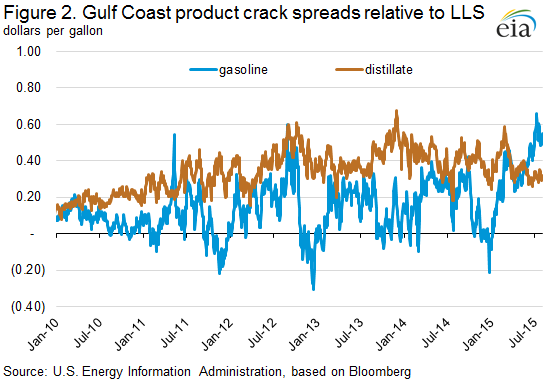

Gulf Coast refinery margins are currently supported by high gasoline crack spreads that reached a peak of 66 cents per gallon (gal) on July 8, a level not reached since September 2008 (Figure 2). For the past several years, distillate crack spreads have consistently exceeded those for gasoline, but since May this trend has reversed. From 2011 to 2014, distillate crack spreads (calculated using Gulf Coast spot prices for Light Louisiana Sweet crude oil, conventional gasoline, and ultra-low sulfur distillate) averaged a 24 cents/gal premium over gasoline crack spreads, but that premium has fallen to an average 2 cents/gal so far this year. Since May 20, Gulf Coast gasoline crack spreads have averaged 17 cents/gal higher than distillate crack spreads. Higher demand for gasoline is supporting these margins. Total U.S. motor gasoline product supplied is up 2.9% through the first five months of 2015, and trade press reports indicate that demand is also higher in Europe and India so far this year compared with 2014.

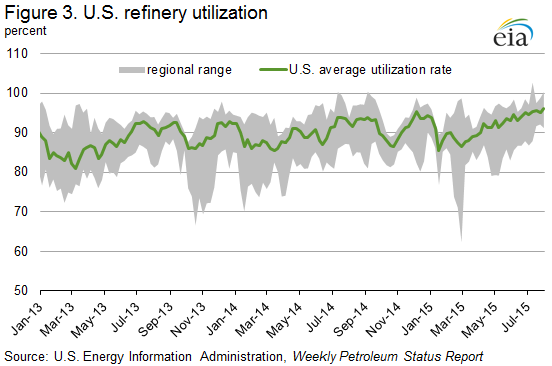

Favorable margins leading to high refinery runs are not limited to the Gulf Coast region. Since early April, U.S. refinery utilization (gross inputs divided by operable calendar day capacity) has consistently been above 90%, driven largely by elevated runs at Gulf Coast and Midwest refineries (Figure 3). During that time, East Coast and Rocky Mountain utilization has also been high, only dipping below 90% in five weeks and two weeks, respectively.

Despite the ongoing unplanned outage at ExxonMobil’s Torrance, California, refinery, utilization on the West Coast exceeded 90% for the past three weeks, marking the second, third, and fourth times that all five regions have recorded refinery utilization rates above 90% for the same week since EIA began publishing weekly utilization data in 2010. These high utilization rates combined with increased U.S. refinery capacity (18.0 million b/d as of January 1, 2015) have led to record high gross inputs. Monthly data on utilization rates go back further, and the last time all regions exceeded 90% in the same month happened in September 2006.

U.S. refinery runs tend to peak in the second and third quarters of the year when demand is greater because of increased driving in the summer. In its July Short-Term Energy Outlook (STEO), EIA estimates that refinery runs will average 16.7 million b/d from April through September and then dip slightly in the fourth quarter to 16.2 million b/d before falling further to 15.8 million b/d in first-quarter 2016. Following the winter period of lower demand and refinery maintenance, STEO expects U.S. refinery runs will reach new highs next summer, averaging 16.9 million b/d in third-quarter 2016.

U.S. average gasoline and diesel fuel prices decrease

The U.S. average retail price for regular gasoline decreased six cents from last week to $2.69 per gallon as of August 3, 2015, down 83 cents from the same time last year. The West Coast and Midwest prices both decreased seven cents per gallon, to $3.48 per gallon and $2.52 per gallon, respectively. The East Coast and Gulf Coast prices each declined five cents, to $2.58 per gallon and $2.39 per gallon, respectively. The Rocky Mountain price decreased three cents to $2.83 per gallon.

The U.S. average diesel fuel price declined six cents from the prior week to $2.67 per gallon, $1.19 less than the same time last year. The Gulf Coast price decreased eight cents to $2.54 per gallon. The Midwest price declined six cents to $2.56 per gallon. The Rocky Mountain and West Coast prices both fell five cents, to $2.69 per gallon and $2.91 per gallon, respectively. The East Coast price was down four cents to $2.77 per gallon.

Propane inventories gain

U.S. propane stocks increased by 0.9 million barrels last week to 90.4 million barrels as of July 31, 2015, 21.9 million barrels (32.0%) higher than a year ago. Midwest inventories increased by 0.7 million barrels and Gulf Coast inventories increased by 0.2 million barrels. Rocky Mountain/West Coast inventories increased by 0.1 million barrels while East Coast inventories remained unchanged. Propylene non-fuel-use inventories represented 5.3% of total propane inventories.