ISIS And Oil: Iraq’s Perfect Storm – Analysis

By Published by the Foreign Policy Research Institute

By Frank R. Gunter*

(FPRI) — The combination of the ISIS insurgency and low oil prices are producing an economic shock unprecedented in Iraq’s troubled history. The ongoing conflict will require a sharp rise in security expenditures at the same time that government oil export revenues are collapsing, forcing the government into deficit spending. This deficit spending, combined with a loss in reserves from the Central Bank of Iraq, calls into question the much-vaunted stability of the Iraqi dinar.

In the eleven years since the U.S.-led invasion overthrew Saddam Hussein, Iraq has faced brutal conflict and sharp drops in oil prices but – until mid-2014 – never both at the same time. Following the destruction of the Golden Mosque, Iraq descended into what many analysts saw as a full-fledged civil war in 2006-7. However, not only was a large proportion of Iraqi security expenses paid for by the United States but also world oil prices rose sharply. Combined with a gradual increase in oil export volume, this resulted in a substantial growth in government revenues. And when oil prices collapsed in 2009, the level of violence and associated expenses was the lowest since before the 2003 invasion. The recent combination of an acceleration in violence and an oil price collapse is unprecedented.

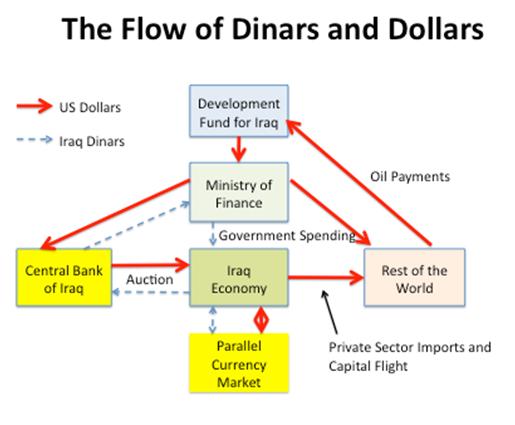

Dollar Flows in Iraq

The flow of dinars and dollars within Iraq is critical to dealing with the ongoing crisis and yet little understood even within the country. The figure below illustrates the pattern of these flows. As is well known, the primary source of government revenues – over 95% – is from oil exports. For over a decade, the dollars earned from these exports have been paid into the Development Fund for Iraq (DFI), which is held by the Federal Reserve Bank of New York. The primary reason for having oil export payments paid to the DFI rather than directly to Iraq’s Ministry of Finance (MoF) is to avoid confiscation of these funds by foreign courts in settlement of Saddam-era lawsuits.

Upon request, dollars from Iraq’s oil exports are transferred from the DFI to the MoF. At this point, a divergence occurs. Over half – about 60% in 2013 – of the dollars flow out again to the rest of the world as payments for government imports, debt service, and miscellaneous transactions. The remaining dollars are sold to the Central Bank of Iraq (CBI) for dinars at a rate of 1166 Iraqi Dinars per US Dollar. The MoF then uses these dinars to pay for the Government of Iraq (GoI) expenditures in the Iraq economy such as salaries, pensions, social safety net, security, etc. The dollars accumulated by the CBI through these dinar sales are, of course, the nation’s international reserves.

However, many of these dollars immediately flow out again. The CBI holds daily auctions to provide dollars to the Iraq economy. Financial institutions buy dollars from the CBI in order to provide them to individuals and organizations that want dollars as a more secure savings asset, to facilitate domestic transactions, to purchase legal and illegal imports, and for capital flight. This demand for dollars is quite large. For example, during the first 14 auction days of December 2014, CBI dollar sales totaled $2.25 billion. Those Iraq individuals or organizations that are forbidden by the CBI to directly access the currency auction must purchase dollars at a premium in the parallel currency market. On December 18, 2014, the exchange rate in the parallel market was 1199 Iraqi Dinars per US Dollar – about 3% higher than at the CBI auction.

In every year but one over the last decade, the inflow of dollars to the CBI from the MoF exceeded the outflow of dollars through currency auctions resulting in an increase in the country’s international reserves. For example, in 2013 the MoF sold about $55 billion to the CBI while about $53 billion flowed out again through the currency auctions resulting in about a $2 billion increase in international reserves. The large increase in international reserves since 2004 has been the major support for the country’s enviable exchange rate stability. However, the results for 2014 were grim.

Because of political disputes, Iraq never passed a 2014 budget. Instead, government expenditures in 2014 were based on an arguably unconstitutional extrapolation of the 2013 budget. And the Government of Iraq (GoI) has continuously delayed even a partial accounting of 2014 revenues and expenditures. However, recent data from the International Monetary Fund support the view that Iraq’s fiscal and monetary situation is deteriorating. At the same time that oil export earnings are declining, GoI security-related dollar imports have increased dramatically. One effect has been on fiscal reserves held at the DFI, which have fallen from almost $18 billion at the end of 2012, and $6.5 billion at the end of 2013, to about $4 billion at the end of November 2014 (IMF Press Release 14/560, 9 December 2014). Equally worrisome is the drop in the country’s international reserves.

From $77 billion at the end of 2013, the international reserves held by the CBI fell to about $67 billion at the end of November 2014. This is only the second year-over-year fall in international reserves in the last decade. In the absence of reliable data from the GoI, there are two possibilities. Either there has been a decrease in MoF sales of dollars to the CBI and/or a substantial increase in dollar auction sales to financial institutions. However, through November 2014, auction sales of dollars by the CBI have totaled about $47.4 billion, which is roughly in line with 2013 dollar sales. Therefore, the cause of the drop in Iraq’s international reserves is more likely a result of the collapse in oil export revenues combined with increasing security-related dollar expenditures by the Iraqi government and, possibly, accelerating capital flight. Thus in 2015, Iraq not only faces a fiscal crisis from falling oil export revenues but also a monetary crisis because of the loss of international reserves. The fiscal crisis might be best understood by distinguishing between the “break even” price of oil and the “crisis” price of oil.

Break Even and Crisis Prices

Despite the fact that the country’s 2015 fiscal year starts this month, the crucial assumptions underlying the budget are uncertain. Over the last several months, no sooner has the GoI announced a planning price for oil for the 2015 budget then world prices have fallen below this level. The most recent announcement on December 25th was for a $102.5 billion budget based on an annual average oil price of $60 per barrel resulting in a large deficit (Gulf Research Center, December 25, 2014). Expenditures of $102.5 billion in 2015 means that the GoI expects to spend almost $22 billion less than its actual expenditures in 2013! Where will the cuts occur? The drop in oil prices to similar levels in 2009 provides insight into both the reactions of the GoI and the effects on the Iraqi economy.

In 2009, as total revenues decreased by about 33%, salary and pension expenditures increased by about the same percentage. This necessitated sharp cuts in the other major expenditure categories, safety net transfers and public investment, in order to reduce expenditures. The remaining deficit was financed through the sale of GoI treasury bills and the MoF “clawing back” unspent government funds from the state owned banks. The economic effects of the draconian cuts in public investment were severe and long-lasting. Since public investment accounts for over 90% of Iraq’s fixed capital formation, the cuts in the investment budget caused most economic development activities to grind to a stop. Work on improving roads, increasing electricity generation, opening schools and clinics, increasing access to clean water, and so on was abandoned until oil prices finally recovered in 2010. And when the projects were eventually restarted, it was often discovered that previous work had to be completely redone due to looting, vandalism, environmental damage, or planned revisions. By some estimates, it was not until 2011 that public investment returned to the levels achieved at the end of 2008.

Of course, if 2015 oil prices turn out to be higher than expected, the GoI might be able to restore some of the cuts. However, rather than have the reader chase daily changes in oil price predictions, it might be more useful to consider the implications of two oil prices: the break-even price and the crisis price.

Assuming oil exports of about 3.3 million barrels per day, Iraq needs an oil price of about $80 a barrel in order to break-even and to be able to pay for its sharply reduced 2015 expenditures without running a budget deficit. An oil price this high would provide sufficient revenues to pay not only for current expenditures and security costs but also for essential infrastructure investment. Since world oil prices are already less than $60, it is extremely unlikely that Iraq will be able to break-even in 2015. But at what price of oil will the required reductions in GoI expenditures become politically destabilizing?

That depends on the crisis price of oil. The crisis price is the lowest oil price that will allow the GoI to pay salaries and pensions, purchase the necessary supplies for the police and army, maintain a minimum social safety net, pay interest on its debts, pay war reparations, and continue the absolute minimum infrastructure maintenance and construction to allow a steady increase in the volume of oil exports. If the world price of oil falls below the crisis price for an extended period of time and other revenue sources are not available, then the necessary expenditure cuts can be expected to be politically destabilizing. In 2009, this crisis price was an estimated $50 a barrel. Therefore, while the world price of oil in 2009 was below Iraq’s break-even price, it was above the crisis price.

However, in 2015, the crisis price of oil is expected to be much higher. Not only has there been a steady increase in government salaries and pensions since 2009, but also the GoI expects to sharply increase its security expenditures to fight ISIS. As a result, the 2015 crisis price of oil is an estimated $70 a barrel. Since world oil prices are expected to remain below the crisis price in 2015, the GoI faces a difficult challenge – either find another source of revenue, borrow the needed funds, or make politically unacceptable cuts in salaries or pensions. The latter option can be expected to lead to widespread political protests by government employees and retirees as well as threats of a government shutdown.

If world oil prices average $60 per barrel in 2015, then the GoI needs at least an additional $12 billion to fund its minimal crisis budget and an additional $12 billion – $24 billion in total – to rise to the break even point. While its international and domestic options to raise these funds are limited, the GoI has a high probability of funding its crisis budget. However, the GoI faces a much lower probability of being able to fund its 2015 break-even budget.

Options for international lending are limited. Government to government loans from the United States and other countries involved in the current war on ISIS are likely to face strong opposition in Washington and other world capitals. It will be argued – with an element of truth – that Iraq’s budget problems are mostly self-inflicted, the result of GoI mismanagement and corruption. In addition, it will be pointed out that the U.S. and other states have already forgiven 80% or more of their Iraqi debt and that these countries have spending needs at home. Iraq’s regional neighbors such as the UAE and Kuwait – who generally did not participate in the loan forgiveness program – are facing their own budget challenges resulting from the collapse in oil prices. However, it is likely that the GoI will be able to borrow several billion dollars. In addition, it appears that Kuwait has agreed to a one-year suspension of war reparations. These reparations were imposed under an agreement with the UN, where Iraq agreed to pay Kuwait 5% of its gross earnings from oil exports to compensate for the damages incurred during the Iraq invasion of Kuwait in 1990. With a world price of $60 a barrel, a one-years suspension will free up about $3.6 billion.

There are at least five other sources of funds to meet the fiscal deficit. First, the GoI can readily access the funds held at the Development Fund on Iraq that were an estimated $4 billion at the end of November 2014. Second, in 2009, the GoI was able to transfer about $7.7 billion from state-owned banks back to the MoF. These funds represented amounts that had been budgeted but not yet spent. In view of the constraints on spending in 2014, it is unlikely that more than several billion can be clawed back from state-owned banks in 2015. Third, the GoI could attempt to borrow domestically although the amount raised would probably be less than $1 billion. While there have been several bond issues since 2003, demand for such instruments is limited especially since there is no liquid secondary market for government debt. Fourth, although the country has an income tax system, tax revenues in previous years have been de minimis. It is unlikely that increasing the tax rate will raise substantial revenues in 2015. Finally, and most controversially, it has been proposed that the MoF obtain part of the country’s $67 billion in international reserves by encouraging/forcing the CBI to buy dollar denominated bonds from the MoF. Until a few years ago, it was believed that the CBI could resist such GoI pressure to monetize its debt, but former Prime Minister Nouri al-Maliki was able to remove the head of the CBI without the approval of the National Council of Representatives and replace him with a Maliki loyalist. This event severely undermined the perceived independence of the CBI.

Adding together these various sources of funds, the GoI should be able to raise or borrow enough to pay not only for its crisis budget in 2015 but also move part of the way towards its break-even budget. However, if sub-$60 per barrel oil prices continue into 2016, then the GoI will face an even wider budget gap while having exhausted its borrowing options. It may be impossible for the GoI to even pay for its crisis budget in 2016. But a more immediate challenge than the future price of oil is the increasing stress in early 2015 on the Iraqi exchange rate.

Exchange Rate Options

A great source of pride for the CBI has been its ability to maintain a relatively stable exchange rate despite intense conflict in 2006-7. In fact, the CBI actually allowed a 20% appreciation of the dinar during this period. However, as discussed above, CBI reserves are falling as a result of lower dollar sales to the CBI by the MoF combined with large auctions of dollars by the CBI to financial institutions. In addition, there is the possibility that the GoI will attempt to relieve its current fiscal crisis by encouraging or forcing the CBI to buy GoI dollar denominated bonds. This would replace liquid assets in the CBI accounts with illiquid assets, GoI bonds. If either or both of these events occur, then there will be a loss of confidence in the ability of the CBI to maintain the current exchange rate of 1166 Iraqi Dinars per US Dollar. Anticipating a depreciation of the dinar, speculation against this currency can be expected to increase. The CBI and GoI have few options to curb this speculation and prevent a loss of the nominal anchor of the Iraqi economy – its stable exchange rate.

One possibility is to further restrict access to the daily currency auctions. This was the primary policy response when the exchange rate came under attack in February 2012. Buyers of dollars were required to be registered and provide documentation for the precise purpose of the dollar purchases. Further restricting access can be expected to lead to a widening gap between the official exchange rate of 1166 Iraqi Dinars per US Dollar and the rate in the parallel currency market. An expansion of a dual exchange rate system can be expected to increase corruption as institutions use their political influence to gain access to the more favorable currency auction rates. In addition, by restricting access to dollars for less favored groups – primarily in the private sector – it can be expected that there will be a further slowdown in the growth of the country’s non-oil economy, exacerbating the economic crisis.

A more cynical or possibly realistic policy response to the loss of the country’s international reserves would be a sharp pre-emptive depreciation of the Iraqi dinar. This would not only lead to an increase in import prices and a decrease in the prices of non-oil exports boosting domestic production but also reduce – at least temporarily – speculative pressure on the dinar. The experience of countries in similar situations over the last several decades show that if the depreciation option is chosen, then it is better is to depreciate sooner rather than later and by a larger rather than smaller amount. One view is that the GoI should immediately announce a return to the pre-2006 exchange rate of about 1470 Iraqi Dinars per US Dollar – roughly a 25% depreciation. However, with a new government, it is unlikely that there will be an aggressive dinar depreciation. Typically, governments wait until a crisis brought about by a substantial loss of reserves occurs before depreciating their currency. And there is the fear that without fundamental changes in the Iraqi economy, any depreciation will only be the first of many.

A more long-term solution to the country’s loss of reserves and accompanying exchange rate crisis would be a return to using a currency board such as the one that provided Iraq with a stable exchange rate during the tumultuous period of 1930-49. Unlike the CBI, the former Iraq currency board guaranteed full dollar convertibility of dinar notes and coins only. This immunized the currency board from the speculative attacks that are often the downfall of fixed exchange rates such as Iraq’s. However, the adoption of an orthodox currency board can be expected to face serious political opposition since it would reduce the GoI’s ability to divert financial resources in order to favor particular economic sectors or to benefit friends of government officials.

Iraq’s Perfect Storm

The combination of falling world oil prices and the ISIS conflict has resulted in the most serious fiscal and exchange rate challenges since the 2003 invasion. It is tempting for the new government of Prime Minister Haidar al-Abadi to seek only limited modifications of fiscal and exchange rate policies so as not to run the risk of further destabilizing an already complex situation. And if low – sub-$100 a barrel – oil prices are a temporary phenomenon with higher oil prices returning in 2016, then this limited strategy should work. However, if deceased oil demand from the BRIC countries combined with an increased oil supply driven by both the fracking revolution in the United States and Saudi Arabian attempts to rein in the world oil market, then Iraq may face several years of oil prices substantially below $100 a barrel. It should be noted that, even after adjusting for inflation, the world recently experienced two decades, 1985-2005, of sub-$60 a barrel oil. A future of low oil prices will require difficult and, to a great extent, irrevocable decisions about both fiscal and exchange rate policies. Rich countries with long histories of stable government can afford to make stupid decisions. Iraq cannot.

About the author:

*Frank R. Gunter, a Senior Fellow in the Foreign Policy Research Institute’s Program on the Middle East, is a Professor of Economics at Lehigh University in Bethlehem, Pennsylvania.

Source:

This article was published by FPRI