US Inflation Slows Further In July CPI – Analysis

By Dean Baker

It appears that inflation is continuing to decelerate in spite of an unemployment rate that is at a 16-year low. The overall and core CPI both rose 0.1 percent in July. This brings the rate of increase over the last 12 months in both measures respectively to 1.7 percent, well below the Fed’s 2.0 percent, as measured by the PCE, which translates into roughly a 2.2 percent CPI inflation rate.

Perhaps even more important than the level is the direction of change. The rate of inflation appears to be slowing. Taking the average price level over the last three months (May, June, and July) compared with the prior three months (February, March, and April), the annual rate of inflation in the core index has been just 0.7 percent. Even this modest increase is driven entirely by rising rents. If shelter costs are pulled out of the core index, it has been dropping at a 0.7 percent annual rate over the last three months compared with the prior three.

There is even some good news on rental costs. It appears that the rate of increase in rents is now slowing. The year-over-year increase for the owners’ equivalent rent (OER) component had been as high as 3.6 percent back in December. It is down to 3.2 percent for July and the annualized rate comparing the last three months with the prior three months is just 2.7 percent. (The OER is a better measure of actual housing costs because the rent proper index also includes some utilities.)

Inflation in almost all other components remains well contained. The price of medical care services increased by 0.3 percent in July and is up 2.3 percent for the last year. College tuition costs rose by just 0.1 percent in July and are up by 2.0 percent over the last year.

An exception is medical care commodities, which were up 1.0 percent in July and are now up by 3.7 percent over the last year. This is being driven by higher prices for prescription drugs, the index for which rose 1.3 percent in July and is now up by 4.2 percent over its year-ago level.

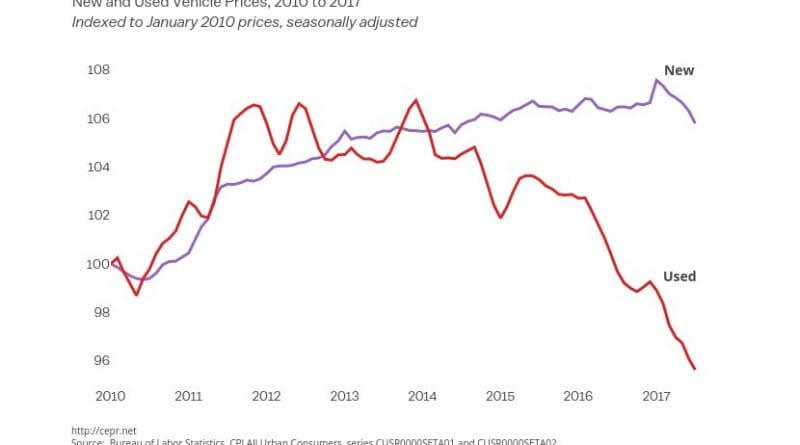

One area of notable price declines is used and new vehicles. The price of both fell by 0.5 percent in July. Over the last year, new vehicle prices are down 0.6 percent, while used vehicle prices have fallen by 4.1 percent. A big part of this story is a glut on the used car market due to the repossession of large numbers of cars sold on subprime loans. This depresses prices in the used car market, which then puts downward pressure on prices in the new car market.

Since the start of 2010, new vehicle prices have risen at less than a 1.0 percent annual rate, while used car prices have fallen by more than 4.0 percent. It’s worth noting the new vehicle index may not reflect actual sales prices. The Bureau of Labor Statistics (BLS) incorporates quality adjustments in its measurements. This means that its index for vehicle prices may be flat or declining, even if the price of a new car in 2017 is higher than the price in 2016. If people don’t perceive the quality improvements in the same way as BLS, they could still think car prices are rising.

This is one reason why concerns over a deflationary spiral are silly. Deflation could mean modest increases in the price of most goods, coupled with substantial quality improvements. It’s hard to envision the economy collapsing because the quality of goods and services is improving more rapidly.

In addition to the CPI report released today, yesterday’s report on the Producer Price Index also gives no indication of accelerating inflation. The overall final demand index fell 0.1 percent in July, while the core index excluding food, energy, and trade were flat for the month. Both indexes are up 1.9 percent over the last year. The intermediate goods index fell 0.1 percent, while the core intermediate goods index fell 0.3 percent.

In short, the July data suggest that inflation is likely slowing from its rate earlier in 2017. It is certainly not increasing.