Central Banks In A Shifting World – Presentation

By Vitor Gaspar

1. Introduction

It is such a pleasure to participate in the ECB Forum on Central Banking and discuss the paper by Evi Papa on Fiscal Rules and Macroeconomic Stabilization in the Euro Area. The paper reviews relevant theoretical and empirical literature and, at the end, examines the Next Generation EU program. The paper is well-written, and it covers a vast landscape. If offers much to learn and to think about.

In my discussion, I will focus on policy. I will argue that it is useful to adopt a broad perspective that considers politics, finance and fiscal policy as fundamentally inter-twined. Interactions between monetary and fiscal policy are better understood in such broad context. I will move on to give a very quick overview of the evolution of ideas and perspectives about macroeconomics that impacted monetary unification in Europe. I will give examples of how experience forced re-thinking. I will go on documenting recent fiscal policy developments, prospects and risks.

Finally, I will comment on Next Generation EU. In doing so, I will make a strong case for public investment in smart and green technologies. I will identify implementation challenges and highlight the importance of public infrastructure governance, transparency and accountability.

2. Politics, Financial Integration and Fiscal Policy

Milton Friedman argued we are subject to the tyranny of the status quo. “Only a crisis – real or perceived – produces real change.”[1] Interestingly, much earlier, Jean Monnet articulated a similar thought, specifically aimed at European integration: “Europe will be made in crises. It will become the sum of the responses to those crises.”[2] Coming even closer to the theme of this session fiscal crises have provoked political revolutions. That was the case for England in 1688 and for France and the US in 1789. Fiscal crises have often changed the distribution of political power within multilayered government structures. The political relevance of fiscal crises is emphasized by Thomas Sargent in many contributions.[3]

In the 1990s, when the launch of the euro area was being prepared, the dominant framework to think about macroeconomic policies had a Real Business Cycle (RBC) core, complemented with elements inspired by Keynesian macroeconomics. The framework was labelled New Keynesian[4] or New Neoclassical Synthesis[5]. Goodfriend and King (2001) put the framework to work as it applied to policymaking in the euro area. They presented their work at the first ECB central banking conference.

For my purposes I want to emphasize the following: first, monetary policy should focus on maintaining price stability. By keeping to a stable price level path, monetary policy is also neutral policy. That is, it keeps economic activity in line with potential output or, in other words, it keeps the output gap at zero. Second, with complete and perfectly integrated financial markets, a small open economy can get full insurance, against idiosyncratic shocks, at fair terms. Third, given that monetary policy would smooth the business cycle, in response to demand disturbances, for the euro area and financial markets would provide insurance against idiosyncratic risks, fiscal policy should focus making sure that public finances support resilient, smart, sustainable and inclusive growth.

The Delors Report (1989) had already pointed to important qualifications. Specifically, while it noted that “markets can exert a disciplinary influence on profligate governments,” it warned than market discipline was subject to important limitations: “Rather than leading to a gradual adaptation of borrowing costs, market views of the creditworthiness of official borrowers tend to change abruptly and result in the closure of access to market financing. Market forces might either be too slow and weak or too sudden and disruptive.”[6] The Report concluded that binding rules were necessary. Such rules would favor financial stability. Independence of monetary policy, in turn, called for the exclusion of direct central bank financing by Treasuries. Such constraints were reflected in the Maastricht Treaty and lie at the roots of European fiscal rules.

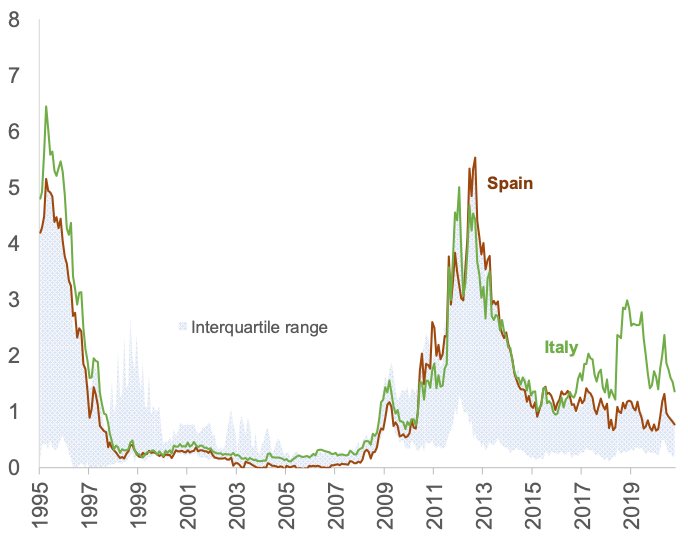

Figure 1: Euro Area Spreads (10-year bonds, Jan. 1995–Oct. 2020)

Sources: Thomson Reuters Datastream, Bloomberg, Haver Analytics, Global Financial Data and International Financial Statistics

Notes: Spreads are against Germany.

3. Debt, Deficits and Public Finance Risks

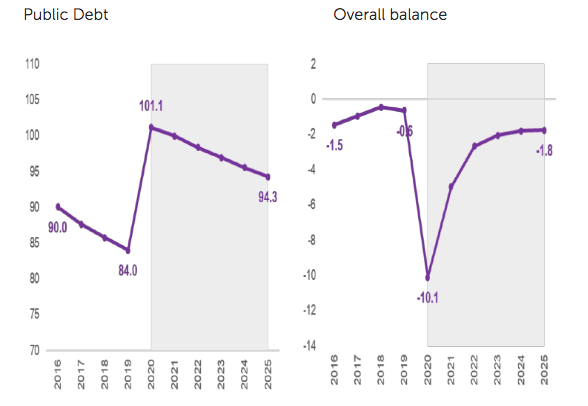

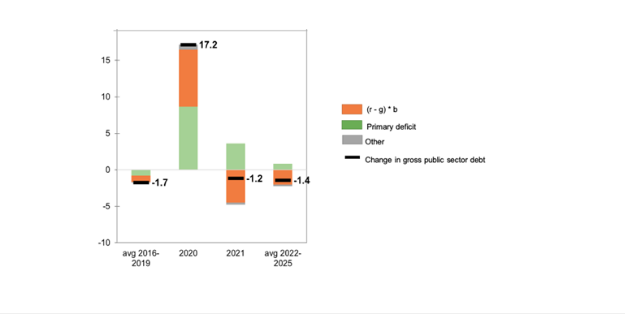

Prior to the pandemic, public debt in the Euro Area was declining at an average of 1.7 percentage points of GDP per year over 2016-19. In 2020, this ratio will jump by an unprecedented amount – 17 percentage points – to 101 percent of GDP. This is illustrated in Figure 2.

Figure 2: Euro Area Public Debt and Fiscal Balance (2016–2025, in percent of GDP)

Sources: IMF Fiscal Monitor and WEO.

As shown in Figure 3, the major increase in the primary deficit and the sharp contraction in economic activity are the main drivers of this jump up in debt. The IMF baseline scenario, based on information at end-September 2020, considered that after such exceptional development, the public debt to GDP in the Euro Area would resume its downward trajectory, albeit at a slower pace than before. This downward path is explained by negative interest-growth differentials and gradual reduction in the primary deficit.

Figure 3: Euro Area Public Debt and Fiscal Balance (2016–2025, in percent GDP)

Sources: IMF Fiscal Monitor, WEO, and IMF staff calculations.

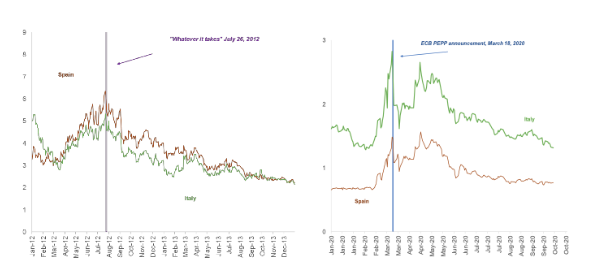

Figure 4 illustrates a number of important points. First, monetary policy matters a lot for fiscal policy. The figure gives two examples. July 26, 2012, “whatever it takes” and March 18, 2020, the announcement of the PEPP. In both cases the response of bond yields – and yield differentials – was quick and sizeable. Second, the divergence in bond yields in the period of the fiscal crises in the euro area was associated with persistent divergence in fiscal policies and economic results. Financing conditions also diverged for private corporations based in different member states. Clearly the single financial market fragmented under stress. Fiscal policy was strongly pro-cyclical in the countries hit by sharply rising sovereign yields, so their economies suffered a double blow from higher borrowing costs and fiscal contraction. This leads to the final point: the performance of the euro area member states from the start of the GFC is far from stellar. The best performers delivered over the period on par with the US. The laggards fell way behind. These phenomena created political challenges within and between countries. Divergences will likely persist and may even increase with COVID 19.

Figure 4: Euro Area Spreads (10-year bonds, Jan. 2008–Oct. 2020)

Sources: Thomson Reuters Datastream, Bloomberg, Haver Analytics, Global Financial Data and International Financial Statistics.

Notes: Spreads are against Germany.

High public debt levels are not the most immediate risk in the Euro Area. Policymakers should not withdraw fiscal support prematurely, as highlighted by Alfred Kammer, in his recent press, briefing during the IMF Annual Meetings (https://www.imf.org/en/News/Articles/2020/10/21/tr102120-transcript-of-october-2020-european-department-press-briefing), the (policy) mistakes made in the aftermath of the GFC should be avoided. Of course, in the world of Goodfriend and King (2001) this would not be a problem because monetary policy would offset the effects on aggregate demand of withdrawing of fiscal support.

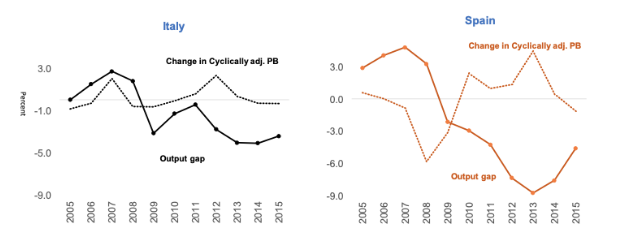

Euro Area policy patterns in the aftermath of the GFC, and their intimate relation with financial market conditions, can be illustrated with the cases of Italy and Spain. Figure 5 shows both of these countries tightened their fiscal stance (as measured by changes in the cyclically adjusted primary balance, as a ratio to potential output) in the middle of economic recessions.

Figure 5: Fiscal Stance and Output Gap

Sources: IMF Fiscal Monitor, WEO, and staff estimates.

Notes: Output gap as percent of potential GDP. Cyclically adjusted primary balance, in percent of potential GDP.

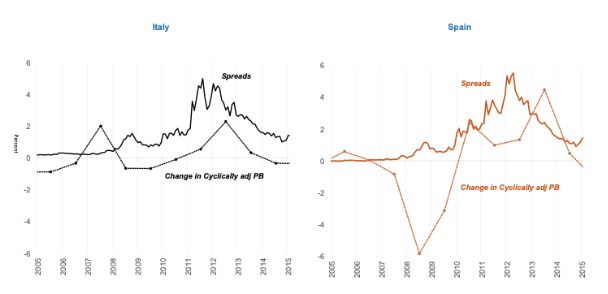

As I mentioned, the procyclicality of fiscal policy coincided with fragmentation in financial markets. One of its manifestations, illustrated in Figure 6, was a rapid widening of sovereign debt spreads. Vicious cycles involving increasingly costly access to finance and reduced space to confront the recession ensued. It is important to note that, more generally, fiscal policy was pro-cyclical in many other countries, in the euro area, including Germany itself.

Figure 6: Fiscal Stance and 10-year Bond Spreads

Sources: Thomson Reuters Datastream, Bloomberg, Haver Analytics, Global Financial Data, International Financial Statistics, CEPR, WEO, and IMF staff estimates.

Notes: Spreads are averaged by month and reported in the chart using monthly frequency. Spreads are against Germany. Cyclically adjusted primary balance, in percent of potential in fiscal year GDP, and is annual frequency.

Turning back to the present, I have presented above the debt and deficit projections under the IMF’s baseline scenario. But the WEO also considers alternative scenarios. It discusses possible risks. Unfortunately, some risks have already materialized. On the upside, growth has overperformed expectations in the third quarter of 2020. But recent weeks have been associated with a second wave of COVID 19 in Europe. Partial lockdowns have been adopted in many places. Government fiscal responses to support livelihoods will result in substantial further increases in deficits and debts. Economic activity and employment will also be adversely affected.

The medium-term horizon is thus subject to particularly acute uncertainties.

4. The Case for Public Investment and the Next Generation EU

The October 2020 Fiscal Monitor (FM) makes the case for public investment. The relevant macroeconomic context includes very low interest rates, high precautionary savings, weak private investment and a gradual erosion of the public capital stock over time.

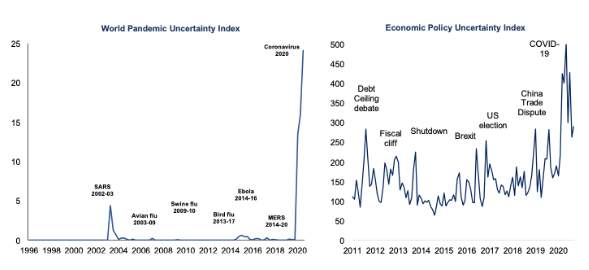

But the novel argument in the FM relates to uncertainty. The FM shows that investment multipliers are particularly high when macroeconomic uncertainty is elevated—as it is now.

Figure 7: Uncertainty Indices

Sources: Barrero and Bloom (2020)

Notes: Data are from the World Uncertainty Index’s website’s World Pandemic Uncertainty Index (WPUI) which measures discussions about pandemics at the global and country level in the Economist Intelligence Unit (see Ahir, Bloom and Furceri, 2020). Monthly values for Economic Policy Uncertainty (EPU) index from www.policyuncertainty.com. See Baker, Bloom, and Davis (2016) for details of EPU index construction.

Public investment can also support the transformation of our economies going forward. Investment in health and education, in digital and green infrastructure can connect people, improve economy-wide productivity, and improve resilience to climate change and future pandemics.

Overall, fiscal policy can provide a bridge to smart, resilient, green, and inclusive growth. Interestingly, the literature reviewed by Pappa (2020) is much less favorable.

Why is that? COVID 19 is associated with very large macroeconomic uncertainty captured in the FM by the dispersion of economic forecasts. Altig et al. (2020) and Barrero and Bloom (2020) present a wide variety of measures of uncertainty. Figure 7 reproduces two of their examples: uncertainty about COVID 19 and uncertainty about economic policy. They show that uncertainty is elevated for a wide variety of uncertainty metrics. Furthermore, COVID 19 will be enduring for a while which means that the traditional concerns with time-to-build are less relevant than usual.

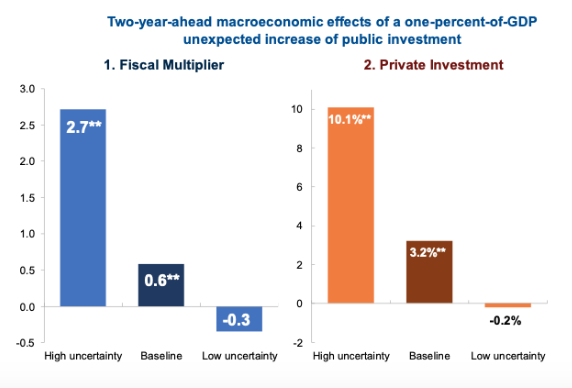

The new evidence in the FM shows that during times of high uncertainty the multiplier associated to public investment is four times larger than in the “baseline”. This happens because public investment can buttress private investors’ confidence and induce them to invest. That is so, in part, because it signals the government’s commitment to sustainable growth. Public investment projects can also stimulate private investment more directly. For example, investments in digital communications, electrification, or transportation infrastructure create new private investment opportunities directly through the creation of opportunities for value-added goods and / or services.

But good governance of public investment is crucial. The Next Generation EU identifies important priorities (e.g. green investment). But implementation is crucial.

The FM finds that the cost of an individual project can increase by as much as 10 to 15 percentage points just because it is undertaken in a period of heightened public investment effort. Cost increases tend to be higher and project delays longer if projects are approved and undertaken in these periods. Fast increases in public investment are also associated with increased vulnerabilities to corruption. More generally, improving the governance of project selection and management is important, because there is scope to improve the efficiency of infrastructure on average. All these themes are covered in a book on infrastructure governance (“Well Spent”) recently published by the IMF.[7]

Figure 8: Fiscal Multipliers

Sources: IMF staff estimates.

Notes: Panel 1: two-year ahead fiscal multipliers of public investment. Panel 2: semi-elasticity of private investment to public investment. **stands for statistically significant coefficient at two standard deviations confidence interval.

*About the author: Vitor Gaspar, a Portuguese national, has been Director of the Fiscal Affairs Department of the International Monetary Fund since 2014. Prior to joining the IMF, he was a Special Adviser at Banco de Portugal. He served as Minister of State and Finance of Portugal during 2011–13. He also held a number of positions in European institutions. Notably, he was director general of research at the European Central Bank from 1998–2004.

Source: IMF, remarks by Vitor Gaspar at ECB Forum on Central Banking 2020

References

Attig, D., Baker, S., Barrero, J. M., Bloom, N., Bunn, P., Chen, S., Davis, S. J., Leather, J., Meyer, B., Mihaylov, E., Mizen, P., Parker, N., Renault, T., Smietanka, P., Thwaites, G. (2020), “Economic Uncertainty Before and During the COVID-19 Pandemic,” Journal of Public Economics, Vol 191.

Barrero, J. and Bloom, N. (2020), “Economic Uncertainty and the Recovery,” Federal Reserve Bank of Kansas City, Economic Policy Symposium.

__________ and Davis, S., (2020), “COVID-19 Is Also a Reallocation Shock,” Becker Friedman Institute, Working Paper, No. 2020-59.

Clarida, R., Galim, J., and Gerler, M. (1999), “The Science of Monetary Policy: A New Keynesian Perspective,” Journal of Economic Literature, 37, pp. 1661-1707.

Dabla-Norris, E. (ed.) (2019), Debt and Entanglements Between the Wars, International Monetary Fund, Washington.

Delors, J., (1989), Report on Economic and Monetary Union in the European Community, Committee for the Study of Economic and Monetary Union.

Friedman, M., (1962), Capitalism and Freedom, (preface to the second edition, 1982) The University of Chicago Press.

Gali, J., (2015), Monetary Policy, Inflation and the Business Cycle: an Introduction to the New Keynesian Framework, Second Edition, Princeton University Press.

Garcia Herrero, A., Gaspar, V., Hoogduin, L., Morgan, J., and Winkler, B. (eds.), (2001), The Case for Price Stability, in Why Price Stability?, First ECB Central Banking Conference, European Central Bank.

Goodfriend, M. and Kinf, R., (1997), “The New Neoclassical Synthesis and the Role of Monetary Policy,” NBER Macroeconomics Annual, pp. 231-83., MIT Press.

International Monetary Fund (2020), Fiscal Monitor: Policies for the Recovery, Washington. https://www.imf.org/en/publications/fm/issues/2020/09/30/october-2020-fiscal-monitor.

Lamfalussy, A., (2000), Financial Crises in Emerging Markets, p.163, Yale University Press.

Monnet, J., Memoires, “L’Europe se fera dans les crises et elle sera la somme des solutions apportées à ces crises.” (translation by Vitor Gaspar).

Pappa, E., (2020), Fiscal Rules, Policy and Macroeconomic Stabilization in the Euro Area, ECB Central Banking Conference.

Sargent, T., (2013), Rational Expectations and Inflation, Third Edition, Princeton University Press.

Sargent, T., (2019), Foreword in Debt and Entanglements Between the Wars, International Monetary Fund.

Schwartz, G., Fouad, M., Hansen, T., and Verdier, G. (eds.), (2020), Well Spent: How Strong Infrastructure Governance Can End Waste in Public Investment, International Monetary Fund.

Woodford, M., (2003), Interest and Prices: Foundations of a Theory of Monetary Policy, Princeton University Press.

.

[1] Milton Friedman, 1962, Capitalism and Freedom, The University of Chicago Press, Chicago. Preface to the second edition, 1982.

[2] Jean Monnet, Memoires, “L’Europe se fera dans les crises et elle sera la somme des solutions apportées à ces crises.” (translation by Vitor Gaspar).

[3] See, for example, Foreword in Era Dabla-Norris (ed.), 2019, Debt and Entanglements Between the Wars, International Monetary Fund, Washington. See also Thomas Sargent, 2013, Rational Expectations and Inflation, Third Edition, Princeton University Press, Princeton.

[4] See, for example, Richard Clarida, Jordi Gali and Mark Gertler, 1999, The Science of Monetary Policy: A New Keynesian Perspective, Journal of Economic Literature, 37, 1661-1707. See also Michael Woodford, 2003, Interest and Prices: Foundations of a Theory of Monetary Policy, Princeton, Princeton University Press and Jordi Gali, 2015, Monetary Policy, Inflation and the Business Cycle: an Introduction to the New Keynesian Framework, 2nd edition, Princeton: Princeton University Press.

[5] Marvin Goodfriend and Robert King, 1997, The New Neoclassical Synthesis and the Role of Monetary Policy, NBER Macroeconomics Annual 1997, 231- 283. Cambridge MA: MIT Press and 2001, The Case for Price Stability, in Alicia Garcia Herrero, Vitor Gaspar, Lex Hoogduin, Julian Morgan and Bernhard Winkler (eds.), Why Price Stability?, First ECB Central Banking Conference, Frankfurt am Main: European Central Bank, June 2001.

[6] I believe that this description of the functioning of financial markets is due to Alexander Lamfalussy. Hehas confirmed as much in private conversation. In a separate context he wrote: “Financial fragility or, more precisely, periods of financial exuberance followed by episodes of financial distress have been integral to the working of market economies since times immemorial. Bubbles in asset prices have rarely deflated slowly; soft landings have been the exception, sharp declines the rule. Similarly, only on rare occasions has excessive indebtedness of firms or governments been absorbed gently; more frequently the indebtedness has led to outright financial crises, with severe implications for the real economy.” Reproduced from Alexander Lamfalussy, 2000, Financial Crises in Emerging Markets, page 163, New Haven: Yale University Press.

[7] Gerd Schwartz et al. (eds.), Well Spent: How Strong Infrastructure Governance can end waste in Public Investment, International Monetary Fund.