Global Trade Needs More Supply Diversity, Not Less – Analysis

By Davide Malacrino, Adil Mohommad and Andrea F. Presbitero

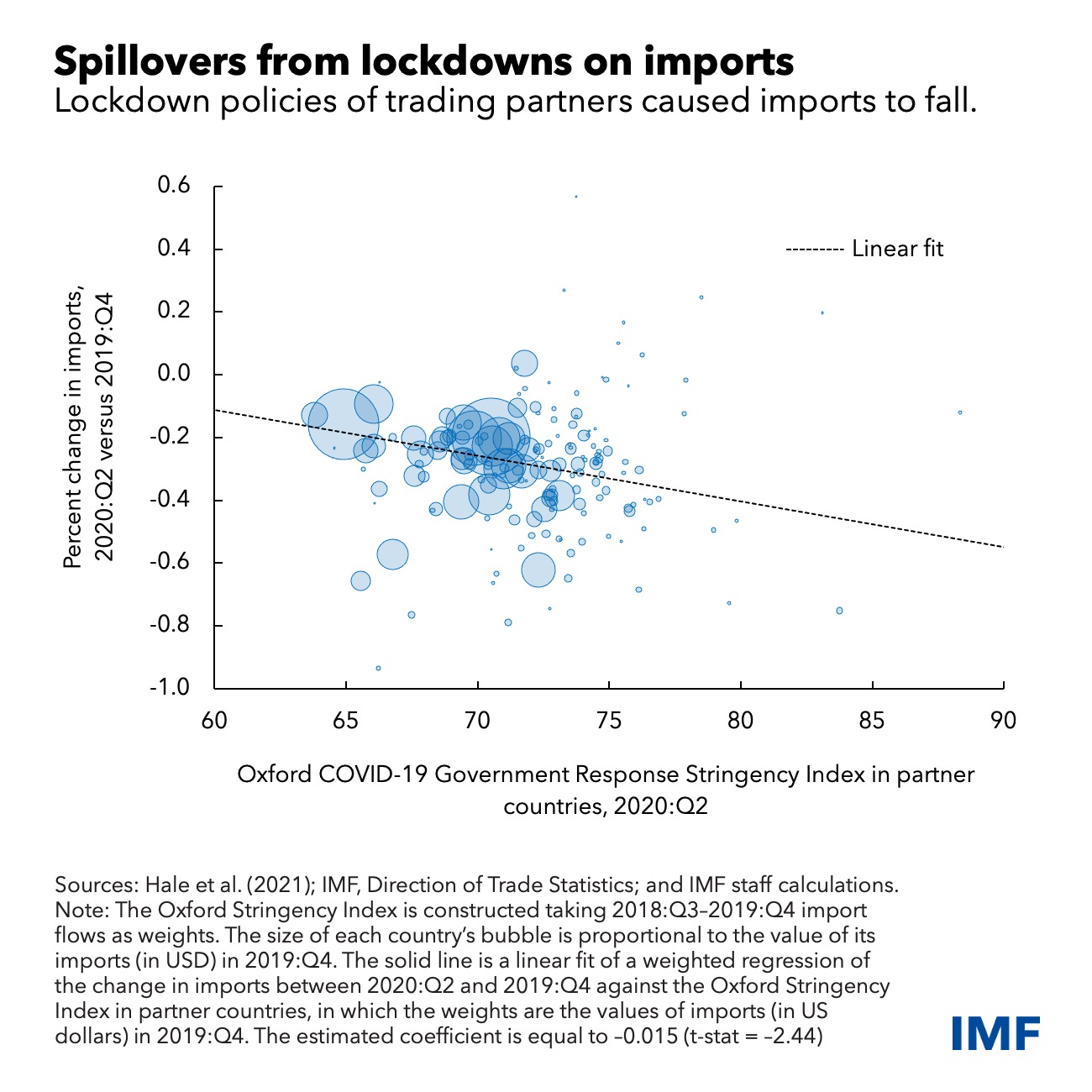

Countries with trade partners that implemented more stringent lockdowns had a sharper drop in imports. Though trade flows have adjusted, more diversified global value chains could help lessen the impact of future shocks.

The demand and supply shocks unleashed by the pandemic were expected to lead to a dramatic collapse in trade, but international commerce has proven more resilient than during previous global crises.

While goods trade fell sharply in the second quarter of 2020, it bounced back to pre-pandemic levels later in the year. The decline for services in 2020 (such as tourism) was worse, and has recovered more slowly, given persistent restrictions to contain infection in some countries.

International spillovers

Factors specific to the pandemic help explain these trade patterns.

First, goods imports were larger in 2020 than would be predicted by demand (and relative prices) alone, more so in countries with stringent lockdowns or severe outbreaks.

Second, lockdowns had significant—if unintended—international spillovers. Countries with trade partners that implemented more stringent lockdowns experienced larger declines in imports of goods. Trade partner lockdowns accounted, on average, for up to 60 percent of the decline in imports in the first half of 2020. These impacts were larger in industries that rely heavily on global value chains, and are further downstream in the production process (such as electronics).

The effects were short-lived, however, suggesting that global supply chains were resilient. And remote work also lessened the trade spillovers from lockdowns.

Even so, disruptions wrought by the pandemic led to calls for more domestic production of goods (reshoring). Our latest World Economic Outlook shows that dismantling global value chains is not the answer—more diversification, not less, improves resilience.

Global value chains adapted

Trade data affirm this. By mid-2020, Asian countries, which were hit early by COVID-19 but then managed to contain it (just when many European countries imposed severe mobility restrictions) saw an increase in their market share of GVC-related products of 4.6 percentage points in Europe, and 2.3 percentage points in North America. These gains were large and quick by historical standards but as countries adjusted to the pandemic, they’ve partially unwound, suggesting that the changes were likely temporary.

Though global value chains have adjusted, some industries such as automobiles have faced large supply disruptions, pointing to the need to enhance resilience. We analyze two options for building supply chain resilience: diversifying inputs across countries, and greater substitutability of inputs.

Boosting trade resilience

We simulated the effects of disruptions in a global economic model and compared outcomes under higher levels of diversification, or higher substitutability (how easily a producer can switch inputs from a supplier in one country to another). We considered two scenarios: supply disruption in a single, large, input supplier country; and supply shocks to multiple nations.

Our analysis shows that diversification significantly reduces global economic losses in response to supply disruptions. Following a sizable (25 percent) labor supply contraction in a single, large global supplier, gross domestic product for the average economy falls by 0.8 percent under the baseline. In the high-diversification scenario, this decline is reduced by almost half.

Higher diversification also reduces volatility when multiple countries are hit by supply shocks. We estimate that the volatility of economic growth in the average country is reduced by around 5 percent in this scenario. Diversification offers little protection, however, when a major disruption hits all economies at the same time, like the first four months of the pandemic.

Countries can diversify by sourcing more intermediate inputs from abroad. Currently there is a significant “home bias” in the sourcing of such supplies. Firms in the Western Hemisphere, for example, source 82 percent of their intermediates domestically. Re-shoring of production would thus lower diversification further.

Substitutability can be achieved in two ways: through greater flexibility in production, such as when electric vehicle maker Tesla Inc. rewrote software to enable its cars to use alternative semiconductors in response to the semiconductor shortage; or by standardizing inputs internationally. For example, General Motors Co. recently announced that it is working with semiconductor suppliers to reduce the number of unique chips that it uses by 95 percent, down to just three families of microcontrollers. This standardization would replace a host of chips, eliminating the costs of substituting between them.

Considering again the scenario of a 25 percent labor supply contraction in a large global supplier of intermediate inputs, we find that with greater substitutability, GDP losses in all countries (other than the source country) are reduced by about four-fifths.

Policy implications

Ensuring equitable access to vaccines and treatments remains the first policy priority. Recent targeted lockdowns in China are a reminder that pandemic-related restrictions continue to have an impact far beyond the affected country. It is in the self-interest of all countries, including those with high vaccination rates to end the acute phase of the pandemic everywhere.

Amid rising concerns regarding global economic fragmentation and “friendshoring” following the war in Ukraine, our analysis also shows that greater diversification and substitutability in inputs can enhance resilience. While corporate decisions will predominantly shape the future resilience of global value chains, government policies can help by providing a supportive environment and lowering the costs.

One obvious area is improved infrastructure. The pandemic has shown that infrastructure investments in certain areas are critical to mitigate supply disruptions related to trade logistics. For example, upgrading and modernizing port infrastructure on key global shipping routes would help reduce global chokepoints. Better digital infrastructure to facilitate telework can also help mitigate spillovers to other countries.

Governments can also help to make information more widely available, so firms can make more strategic decisions. For example, automobile manufacturers on average conduct business directly with about 250 Tier1 suppliers, but this number rises to 18,000 suppliers in the full value chain. Improving access to information on inter-firm transactions and supply chain networks, by for example, digitalizing firms’ document filings, such as tax returns, can be helpful, especially for smaller firms with fewer resources.

Finally, reducing trade costs can help diversify inputs. There is room to reduce non-tariff barriers, which would give a significant medium-term economic boost, especially in emerging markets and low-income developing countries. In addition, reducing trade policy uncertainty, and providing an open and stable, rules-based trade policy regime, can support greater diversification.

— This article, based on Chapter 4 of the April 2022 World Economic Outlook, “Global Trade and Value Chains During the Pandemic,” includes research by Galen Sher and Ting Lan, under the guidance of Shekhar Aiyar, and support from Shan Chen, Bryan Zou, Youyou Huang, and Ilse Peirtsegaele. The analysis was concluded in early 2022, prior to Russia’s invasion of Ukraine, and does not focus on the implications of the war for global trade and value chains.

*About the authors:

- Davide Malacrino is an Economist in the Research Department of the IMF. Previously, he was in the European Department where he worked on the euro area and, briefly, on Iceland. His research in labor economics and household finance focuses on earnings dynamics, income and wealth inequality, and entrepreneurship.

- Adil Mohommad is currently an Economist in the Research Department of the IMF. He has previously served as an economist on numerous IMF country teams including India, Australia, New Zealand, Nepal, Bhutan, and Tuvalu.

- Andrea F. Presbitero is Senior Economist in the Research Department of the International Monetary Fund, CEPR Research Fellow in the International Macroeconomics and Finance programme, and Associate Fellow at SAIS Europe. He has been Assistant Professor at the Universita’ Politecnica delle Marche and Associate Professor of Economics at the Johns Hopkins University School of Advanced International Studies (SAIS)

Source: This article was published by IMF Blog