EIA’s Global Crude Supply Outlook Considers Planned And Unplanned Production Outages – Analysis

By EIA

The U.S. Energy Information Administration’s (EIA) May Short-Term Energy Outlook (STEO) forecasts that global liquid fuels supply will grow by 0.5 million barrels per day (b/d) in 2016 and by 0.8 million b/d in 2017. The supply growth comes from production increases by members of the Organization of the Petroleum Exporting Countries (OPEC) that more than offset decreases in non-OPEC supply. This level of supply growth compared with expected demand growth implies that the oil market will remain relatively loose through the first half of 2017, with significant inventory builds continuing through the end of 2016.

The May STEO estimates, however, that global crude oil production outages averaged 2.8 b/d in April, up slightly from March. This number will likely be higher for May in the June STEO, based on the reduction of Alberta’s oil sands production caused by wildfires. EIA estimates that oil sands output fell in recent days by as much as 1.0 million b/d, as wildfires reached Fort McMurray, Alberta, the center of Canadian oil sands industry. Consequently, EIA expects that second-quarter 2016 Canadian oil sands production will be reduced significantly. Depending on the extent of damage, production outages could carry forward into summer.

The current reduction in Canadian crude oil output is due not to direct damage from the fires in Alberta, but rather the evacuation of oil workers from Fort McMurray. Oil sands operations may be seriously reduced by the unavailability of staff in the coming days and weeks. As a result, Suncor, Shell Albian Sands, and Syncrude were among many oil sands production companies confirming production outages or reduced rates at their sites. At this point, press accounts say the wildfires have been slowed, helped by cooler weather, and plans are underway for rebuilding the portion of the town destroyed and reconnecting utilities throughout Fort McMurray. It is likely that companies will be able to provide temporary accommodations and services for critical personnel. EIA expects that Canada’s production in the second quarter of 2016 will fall by an average of 0.5 million b/d from first-quarter levels before rebounding in the third quarter.

EIA’s global supply forecast incorporates planned and unplanned supply disruptions for both OPEC and non-OPEC producers, and accounts for natural declines at both mature fields and new fields. Unplanned production outages occur frequently and for a variety of reasons, including military conflicts, natural disasters, and technical difficulties. In order to include unplanned disruptions in its forecast, EIA makes assumptions about the duration and magnitude of the disruptions. For OPEC producers, estimated outages pertain to crude oil only; outages among non-OPEC producers incorporate all liquid fuels.

In general, EIA’s estimates of unplanned production outages are calculated as the difference between estimated effective production capacity (the level of supply that could be available within one year) and estimated realized production and outages due to normal maintenance. Therefore, these outage estimates can differ from those measured against other capacity types, such as nameplate capacity or the production level before the disruption.

EIA re-evaluates its estimates of effective production capacity for each producer, and the total level of disrupted volumes is adjusted when there is a change in effective capacity. Recent examples include the reduction of Syria’s and Yemen’s estimated shut-in volumes, where an assessment of damage to fields and infrastructure led to the conclusion that the severe decline in effective capacity will prevent volumes previously categorized as unplanned outages from coming back online within one year. In Iran, shut-in volumes were also reduced to zero following the removal of international sanctions targeting its oil sector in January 2016. Without sanctions, Iran could increase its production or carry spare capacity.

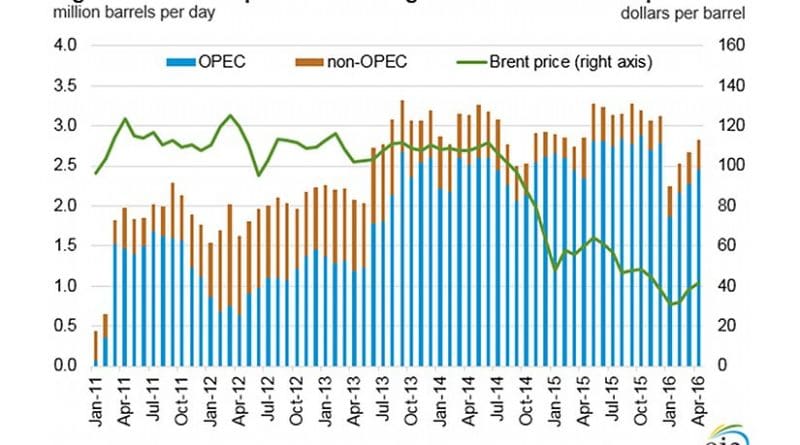

Because most changes in unplanned outages (and their magnitude and timing) are not foreseeable, they can have an especially pronounced effect on oil prices (Figure 1 above). Before 2014, for example, relatively high levels of unplanned disruptions along with relatively low surplus production capacity contributed to a tighter oil market and higher crude oil prices. The effect of disruptions on crude oil prices diminished in recent years as North American production rose to record high levels, causing a prolonged period of global inventory builds that more than offset supply lost to unplanned outages.

Unplanned crude oil supply disruptions among OPEC producers have accounted for most outages since 2012. These outages, which increased annually between 2011 and 2015, averaged about 2.7 million b/d in 2015. Libya (1.0 million b/d), Iran (0.8 million b/d), Nigeria (0.3 million b/d), and Iraq (0.2 million b/d) accounted for most of OPEC’s unplanned supply disruptions in 2015. The stoppage of production at the Wafra and Khafji fields in the Neutral Zone straddling Saudi Arabia and Kuwait caused, on average, an additional 0.4 million b/d in outages during 2015. With the exception of Iran, the issues underpinning the outages in most of these cases remain largely unresolved.

Further uncertainty among OPEC producers stems from the unfolding situation in Venezuela, which is in the midst of societal and economic turmoil. EIA’s STEO forecast includes expected declines in Venezuela’s 2016 and 2017 production stemming from the absence of investment required to boost production and offset declines and the inability of the state oil company Petroleos de Venezuela S.A. (PdVSA) to pay oil service companies for continued work. However, EIA’s forecast does not include projections of unplanned disruptions that could significantly reduce Venezuela’s production.

U.S. average regular retail gasoline price decreases, diesel fuel price increases; regions mixed

The U.S. average regular retail gasoline price decreased two cents from the previous week to $2.22 per gallon on May 9, down 47 cents from the same time last year. The Midwest price fell seven cents to $2.12 per gallon, the Gulf Coast price was down a penny to $1.99 per gallon, and the West Coast price fell less than a penny to $2.63 per gallon. The Rocky Mountain price increased five cents to $2.21 per gallon, while the East Coast price rose less than a penny to $2.22 per gallon.

The U.S. average diesel fuel price increased by less than a penny from the previous week to remain $2.27 per gallon, down 61 cents from the same time last year. The Rocky Mountain price increased two cents to $2.28 per gallon, while the West Coast and Midwest price each rose one cent to $2.49 per gallon and $2.24 per gallon, respectively. The East Coast price increased less than a penny to remain $2.31 per gallon. The Gulf Coast price dipped one cent to $2.13 per gallon.

Propane inventories gain

U.S. propane stocks increased by 1.3 million barrels last week to 73.2 million barrels as of May 6, 2016, 4.7 million barrels (6.9%) higher than a year ago. Midwest inventories increased by 1.3 million barrels, while East Coast and Rocky Mountain/West Coast inventories each increased by 0.1 million barrels. Gulf Coast inventories decreased by 0.1 million barrels. Propylene non-fuel-use inventories represented 5.3% of total propane inventories.