With Inflation At A 40-Year High, The Fed Is Too Afraid To Act – OpEd

By MISES

By Ryan McMaken*

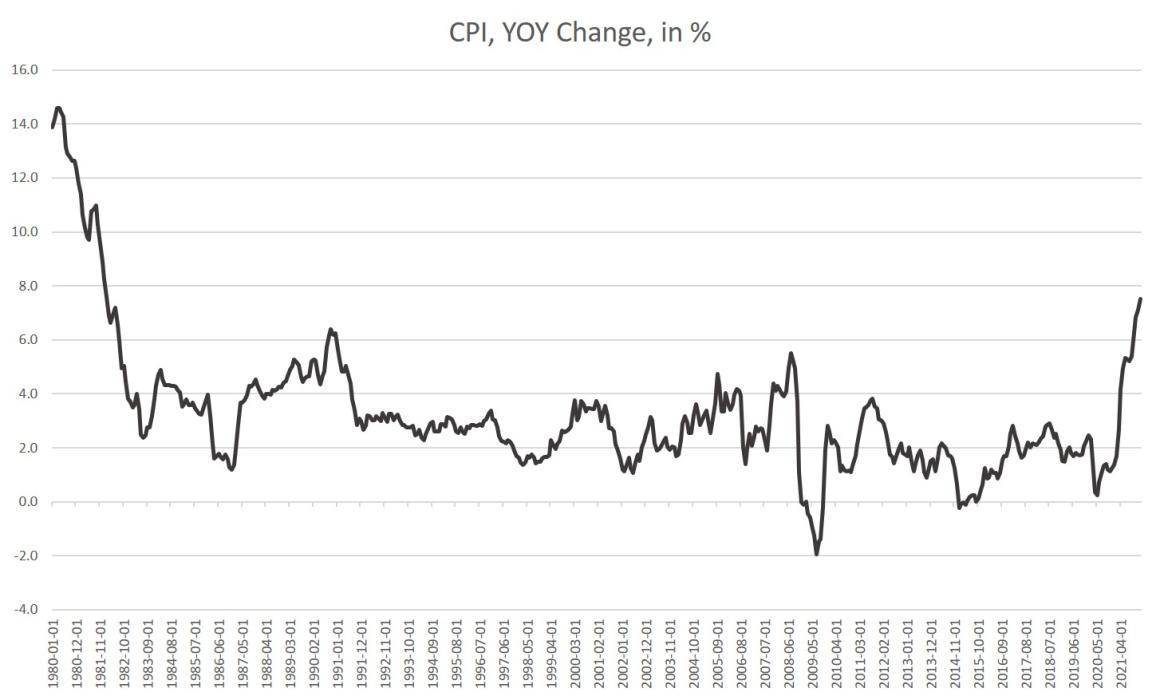

According to the Bureau of Labor Statistics (BLS), Consumer Price Index (CPI) inflation rose 7.5 percent in January, year over year. This was, the BLS notes, the “largest 12-month increase since the period ending February 1982.”

Moreover, “The all items less food and energy index rose 6.0 percent, the largest 12-month change since the period ending August 1982. The energy index rose 27.0 percent over the last year, and the food index increased 7.0 percent.”

When it comes to food, the largest increases were found in “meats, poultry, fish, and eggs, which rose 12.2 percent over the year.”

Housing rose 5.6 percent. Used cars were up a whopping 40.5 percent.

The last time CPI inflation was this high was during February 1982, when the rate was 7.6 percent. That represented an improvement over the very high inflation rates experienced during 1980 and 1981, when inflation topped 18 percent in some months.

With price inflation at a forty-year high, the question remains if the Fed plans to do anything to actually scale back the monetary inflation—a sizable factor in today’s price inflation. The price inflation rate has been above 4 percent since April of last year and has accelerated past 6 percent since October. Yet the Fed’s only action has been to mildly scale back asset purchases funded by the central bank’s monetary expansion. In other words, the Fed has only continued to directly inject new money into the economy even as prices have accelerated upward.

Oh yes, there has been plenty of talk about tapering and taking action to reverse the Fed’s twelve-year-long easy money binge, but the Fed has done essentially nothing. The target federal funds rate remains at 0.25 percent, where it has been since early 2020. Since the Fed started to pretend at being hawkish back in October, its portfolio has increased from $8.5 trillion to $8.8 trillion. It’s true there’s a slight slowing in new purchases, but the fact that some people even claim this is some sort of hawkish turn shows just how far away from “normalization” we remain. The Fed will likely end active asset purchases soon—at least until it decides quantitative easing (QE) is needed again. There’s no talk of actually shrinking the portfolio.

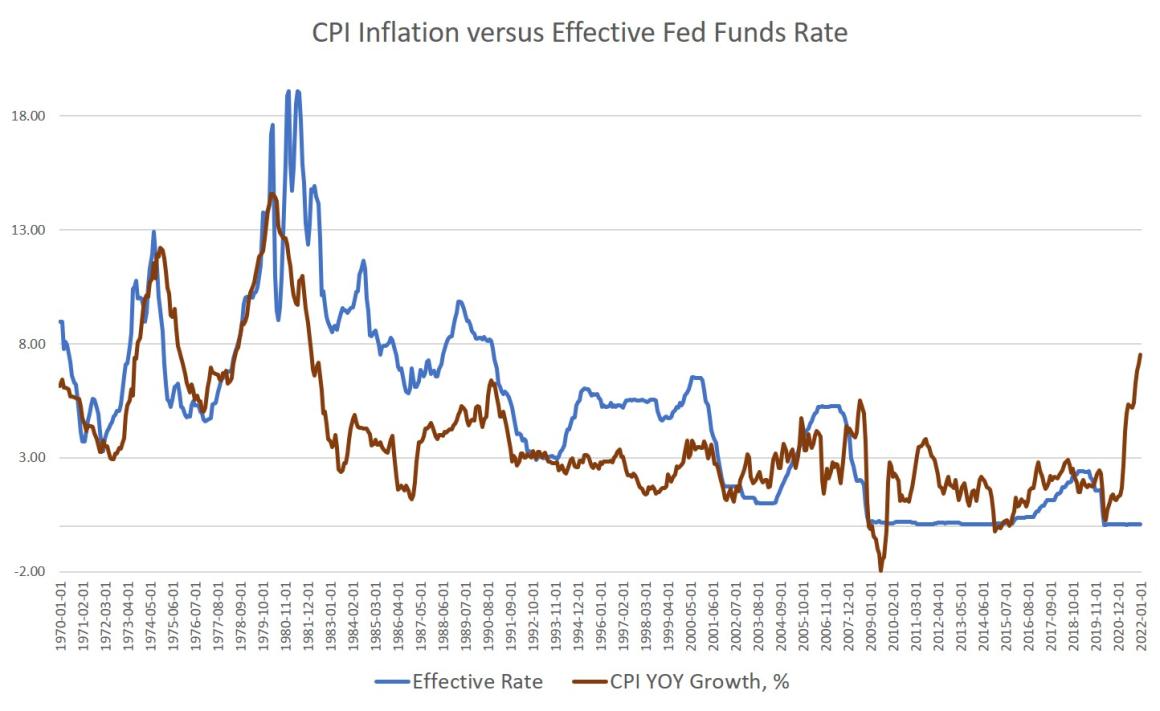

The lack of action on interest rates is quite remarkable as well. The last time the CPI inflation rate was at 7.5 percent, the effective federal funds rate was around 12 percent. Back in 1989, the Fed had also allowed interest rates to rise as inflation rose, with the effective federal funds rate topping out around 9.5 percent. Again, in 2006, interest rates outpaced CPI inflation. Combined with forces of disinflation such as international trade and rising productivity, this took the edge off increases in price inflation in the short term.

It’s true that since Greenspan began to pursue a weak dollar in the late 1980s, the larger policy has always been toward greater monetary inflation. Yet until the Janet Yellen era, there was nonetheless some recognition that keeping interest rates at zero while flooding the market with new money through asset purchases might be a problem.

But thanks to people like Yellen and Jerome Powell, those days are now in the past. Now the “strategy” is to keep interest rates near zero even as price inflation soars to a forty-year high. We can see the disconnect clearly here:

So what will the Fed do in the next few months? It seems the most hawkish predictions are that the Fed might raise the federal funds rate by 1 percent, while doing nothing to actually decrease the size of the portfolio, which would truly tighten the money supply.

Rather, we’ll get a very milquetoast “taper” that will be implemented with extreme caution as the Fed prays it won’t tank the markets.

This all, of course, demonstrates just how incredibly weak out current bubble economy is—and the Fed knows it. Back in 2019, after nearly a decade of expansion, the Fed managed to get the target fed funds rate up to 2 percent. That likely led to the repo panic that year, which led the Fed to restart asset purchases after a brief sell-off. The economy was already headed into 2020 in a weakened state before the covid panic hit.

But now the Fed fears the economy is too weak to withstand even a 1 percent target rate raised slowly over a year. (Mind you, that’s the max anyone is seriously talking about. The likely increase in the target rate is much smaller.) The Fed is scared stiff that even the smallest sudden move could pop these asset bubbles, so the money-creation train has only slowed to the tiniest degree.

Fed mouthpieces, of course, congratulate themselves for this.

For example, St. Louis Fed president James Bullard has been patting the Fed on the back for not crashing the economy so far. The Wall Street Journal quotes Bullard this week:

“We don’t want to be disruptive or surprising markets…. I would like to do this in the smoothest way possible, and we, so far, have achieved that,” [Bullard] said, adding that he would change his view “if the data went against us here.”

In other words, the Fed has been very smooth, according to Bullard. Never mind the fact the Fed hasn’t actually done anything except slightly slow asset purchases. Bullard is right, however, that any real actions would surprise the markets. The market is probably already pricing in widespread skepticism that the Fed will do anything other than implement a handful of twenty-five-basis-point increases over the year.

In other words, it’s hard to imagine the Fed’s dovish faux hawkism will amount to something that can do anything to rein in inflation much—unless, of course, the Fed triggers a recession. And this is what the Fed is afraid of. If it hits the panic button and really does raise rates, say, fifty basis points, how will the markets react? The Fed doesn’t know and is afraid to find out.

Other factors weigh against any sizable Fed action as well. The federal government needs to keep interest rates down so it can continue to borrow trillions of dollars for ongoing covid “relief” and new wars. Any significant increase in interest rates could force sizable budget cuts to programs in order to pay interest on the debt. In an extreme case, high rates could even cause a sovereign debt crisis. We might also find the Fed is more committed to propping up asset prices than it is to lowering price inflation. That means the Fed will be choosing billionaires over regular people. That won’t be a surprise if it happens. The central bank has become the great tool of wealth redistribution from middle-class dollar holders to wealthy Wall Street hedge funders.

*About the author: Ryan McMaken is a senior editor at the Mises Institute. Send him your article submissions for the Mises Wire and Power and Market, but read article guidelines first.

Source: This article was published by the MISES Institute