Retirement Wealth Trajectories: US Vs England – Analysis

By VoxEU.org

Housing forms a large share of household wealth in many nations. Using comparable data for the US and England, this column argues that the nature of housing as an asset – its utility value, illiquidity, and mix of risk and returns – is an important factor in explaining the trajectory of wealth in retirement.

By Richard Blundell, Rowena Crawford, Eric French and Gemma Tetlow*

Many households hold substantial assets throughout retirement and until death. This fact has been documented in many countries, and is in contrast to the simplest version of the lifecycle model. Many explanations and permutations to the lifecycle model have been proposed to explain this, including bequest motives (De Nardi 2004, Love et al. 2009), precautionary saving for health expenses (Love et al. 2009, De Nardi et al. 2010, Kopecky and Koreshkova 2014), and people’s inability or lack of desire to run down their housing wealth during retirement (Yang 2009, Nakajima and Telyukova 2012). However, the existing literature has not yet reached a consensus on the relative importance of different explanations (see De Nardi et al. 2015 for a recent survey).

This remains an important public policy issue in many countries. The retention of wealth observed among older households stands in apparent contrast to popular concerns over the inadequate retirement wealth accumulation of younger households. Furthermore, the elderly typically hold a large share of national wealth: more than one-third of total wealth in the US is held by households whose heads are over age 65 (Wolf 2004). Understanding the motivations behind household saving behaviour is therefore crucial for deciding whether policy action to influence household behaviour is warranted and, if it is, what form it would best take. For example, if older households hold large amounts of wealth due to bequest motives then changes in inheritance taxation may significantly affect savings behaviour. Alternatively, if households hold large amounts of wealth because their wealth is illiquid (in housing wealth, for example), then the inheritance tax likely has only a small effect on savings behaviour. Furthermore, policy action to improve liquidity or influence households’ asset choices may improve welfare.

The US versus England

In a recent paper, we use comparable data for the US and England, drawn from the Health and Retirement Study and the English Longitudinal Study of Ageing, to examine the similarities and differences in the level and trajectory of assets among households in retirement (Blundell et al. 2016). Both countries share a common language and heritage, but have different institutions and different asset returns, which therefore provide different incentives for households to accumulate and decumulate wealth. Comparing patterns across the two countries therefore helps us to identify what is potentially driving wealth dynamics.

Key findings

We show that life expectancies, median income, and asset levels at age 70-74 were similar in the US and England in 2002, suggesting that resources of those recently retired are similar across the two countries. However, real incomes tend to rise throughout later life in England but fall in the US, meaning that for those near the median, retirement income in England is larger than in the US. Since retirement income is greater in England, the simple lifecycle model would suggest English households have less need to save and should thus decumulate wealth faster than their US counterparts. This conclusion would likely be strengthened further if we built in other explanations that have been put forward for why US households decumulate wealth so slowly at older ages. For example, English households have lower out-of-pocket medical spending late in life and thus need to save less for this than their American counterparts, again allowing them to have lower assets late in life.

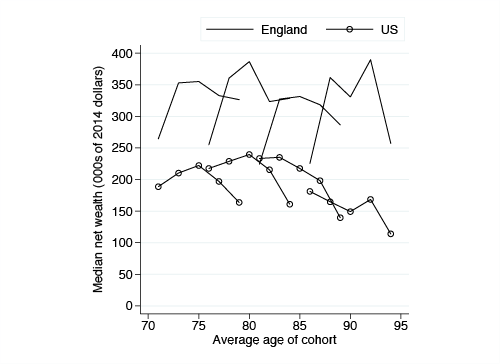

Notes: The sample includes only households where at least one member was still alive and responding to ELSA/HRS at the end of our panel in 2010/11.

However, Figure 1 shows that over the period 2002–2011 assets were drawn down more slowly in England than the US. In fact, median net wealth of older English households actually increased over the period. Figure 1 describes for each country the age profiles of median net assets among our balanced sample of households, divided into four five-year birth cohorts (those born in 1929-33, 1924-28, 1919-23 and 1914-18). For the US, a pattern of broadly declining household wealth with age is found within cohorts. However, the same is not true of England, where we observe significant increases in wealth for each of the cohorts.

Notes: The sample includes only households where at least one member was still alive and responding to ELSA/HRS at the end of our panel in 2010/11.

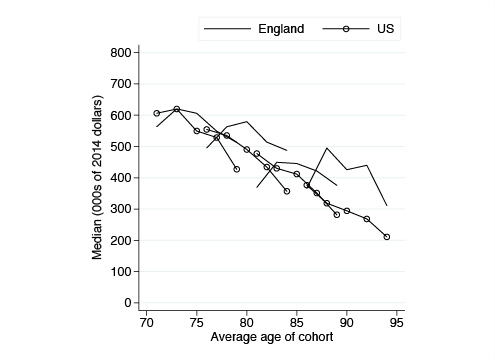

Income grows more rapidly with age in England than in the US. To better assess how differences in income trajectories across the two countries affect household resources in the two countries, we calculate, for each household, the present discounted value of future income, then add this to the wealth measure shown in Figure 1. To calculate the present discounted value of income, we estimate age-specific and household-structure-specific (e.g. married, single man, single woman) income growth rates for both the US and England. Thus we can capture the more rapid income growth for English households. Using information on observed income, and estimated income growth rates to predict income in the future, we create predicted income at each age for each household in each country. Figure 2 shows the sum of wealth plus the present discounted income for the sample of households where at least one member survived to the end. It shows that this measure of resources does decline with age in both countries, since the present discounted value of future income declines with age. However, whereas this measure of wealth declines rapidly in the US, it declines slowly in England. Wealth falls much more rapidly with age in the US, even when considering a broader measure of wealth which includes future income.

Notes: The sample includes only households where at least one member was still alive and responding to ELSA/HRS at the end of our panel in 2010/11.

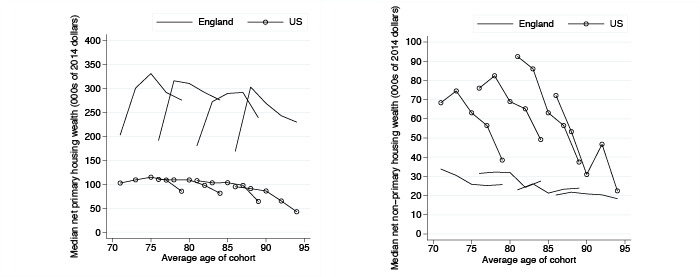

Figure 3 shows the age-profiles of net primary housing wealth (left panel) and net other wealth (right panel) for the balanced panel. The left panel shows that the sharp increase in median wealth in England is driven by increases in net housing wealth. This has a considerable impact on the profile of total net wealth in England because of the importance of primary housing in the household portfolio (in 2002 primary housing accounted for two-thirds of wealth among English households aged 70-74).

We show that this striking difference is largely attributable to the more rapid growth in house prices in England over the period. Between 2002 and 2005 average real house prices increased by around 50% in England, compared to around 20% in the US. However, notwithstanding the question of why households did not draw on this positive wealth shock, there are other differences as well: non-housing wealth was decumulated less rapidly in England, and even stripping out house price changes, housing wealth was drawn on less in England than the US.

Implications

These comparisons suggest that the nature of housing as an asset – its utility value, illiquidity, and mix of risk and returns – is likely to be an important factor in explaining the trajectory of wealth in retirement. This is in line with the findings of Nakajima and Telyukova (2013, 2014), and contrary to the findings of Skinner (1996). In this analysis we do not quantify the relative importance of housing versus other factors driving retirement savings, such as bequest motives or saving to insure against the risk of living long and having high medical spending. Disentangling the relative importance of these factors is an interesting direction for future research.

*About the authors:

Richard Blundell, David Ricardo Chair of Political Economy, University College London

Rowena Crawford, Associate Director, Institute for Fiscal Studies

Eric French, Professor of Economics, University College London; Fellow, Institute for Fiscal Studies and CEPR

Gemma Tetlow, Economics Correspondent, Financial Times

References:

Blundell, R., Crawford, R., French, E. and Tetlow, G. (2016). ‘Comparing retirement wealth trajectories on both sides of the pond’, Fiscal Studies, vol. 31, pp.105-130.

De Nardi, M. (2004), ‘Wealth inequality and intergenerational links’, Review of Economic Studies, vol. 71, pp. 743–68.

De Nardi, M., French, E. and Jones, J. B. (2010), ‘Why do the elderly save? The role of medical expenses’, Journal of Political Economy, vol. 118, pp. 39–75.

De Nardi, M., French, E. and Jones, J. B (2015), ‘Savings after retirement: a survey’, National Bureau of Economic Research (NBER), Working Paper no. 21268.

Kopecky, K. and Koreshkova, T. (2014), ‘The impact of medical and nursing home expenses on savings’, American Economic Journal: Macroeconomics, vol. 6, no. 3, pp. 29–72.

Love, D. A., Palumbo, M. G. and Smith, P. A. (2009), ‘The trajectory of wealth in retirement’, Journal of Public Economics, vol. 93, pp. 191–208.

Nakajima, M. and Telyukova, I. (2012), ‘Home equity in retirement’, Networks Financial Institute, Working Paper no. 2011-WP-08B.

Nakajima, M. and Telyukova, I. (2013), ‘Housing in retirement across countries’, Boston College Center for Retirement Research, Working Paper no. 2013-18.

Nakajima, M. and Telyukova, I. (2014), ‘Reverse mortgage loans: a quantitative analysis’, Federal Reserve Bank of Philadelphia, Working Paper no. 14-27.

Skinner, J. S. (1996), ‘Is housing wealth a sideshow?’, in D. Wise (ed.), Advances in the Economics of Aging, Chicago, IL: University of Chicago Press.

Wolff, E. (2004), ‘Changes in household wealth in the 1980s and 1990s in the U.S.’, Levy Economics Institute, Working Paper no. 407.

Yang, F. (2009), ‘Consumption over the life cycle: how different is housing?’, Review of Economic Dynamics, vol. 12, pp. 423–43.

I was trying to find out the causes of wealth accumulation or de-accumulation of this study but I could not. The study finds some implications about housing but the basic implication was speculative because the study suggested just “likely”. So, whether in the analysis or the implications this study is deficient. There is strong implication of this study a reader can discern easily: looting. This study informs public policy officials that retirees are wealthy and the government should confiscate parts of this wealth by raising taxes, cutting social security, and other tools. This study is not new in its implications, because governments do loot retiree wealth by taking more deductions on health care and high monopoly prices of services such as utility. Financiers are also looting this wealth by the high fees on pension funds. (Pension funds pay high fees for recommendations of investing in bad assets). Retirees’ wealth is also depleting by the high cost of education and the debt of their family members, because retirees do help their family members. Retiree’s wealth was generated by hard work, and public policy and financiers should end their naked looting of this wealth. Soon, financial institutions will loot this wealth by the negative interest rate, the bail-in policies, and the electronic money suggested by some economists.