China’s Growing Real Estate Bubble – Analysis

By MISES

By Trieu Nguyen*

China’s economy has been growing dramatically for many years to become one of the world’s leading economies. According to the World Bank, in 2018, China’s GDP (nominal) was 13,608 trillion USD, the second-highest in the world.1 However, there is some underlying unsustainability in their development strategy that impressive aggregative economic indexes are unable to expose. This is because these indicators do not take into account the structure of the economy.

In order to counter the 2008 financial recession, the government of China has been following expansionary monetary policy with different instruments, in which two major ones are: increasing the money supply on behalf of fiscal stimulus, and credit expansion under low interest rates. However, the abuse of these instruments will cause additional risks and misfortune for the growth of China in the long run. Even as expansionary monetary policy boosted the GDP of China post-recession, this expansion is barely seen in the production of basic consumer goods. It represents a speculative bubble in fixed asset investments (FAI), especially on real estate. From an Austrian-school perspective, this bubble is a consequence of a change in the structure of production of the economy of China stimulated by their expansionary monetary policy.

The bubble, however, did not expand evenly and equally in the whole country. The most important thing about the real estate bubble is location, for capital-intensive areas are likely to have more building construction than others. Predictably, the bubble can be seen in major economic zones of China: Beijing, Shanghai, and Shenzhen. In Beijing, massive public spending of the local governments has been continued for many years after the recession. These spending flowed mostly to FAI, and along with other supporting legislation, stimulates the real estate market, whose expansion accounted for approximately 50% in total FAI of Bejing from 2008 to 2016.

Among different fixed assets, real estate market is one of the most important markets of China as well as in Beijing, with a contribution about 15.7% to the total GDP of the city in 2016. Furthermore, the growth of real estate dominates as one of the most important objectives on the development strategy of the local government. Nevertheless, due to the insecure monetary policy from the national government, numerous signs of malinvestment, and many periodic fluctuations, have been emerging in the real estate market. A dramatic expansion in recent years of FAI, especially the real estate in Beijing, is considered to be the consequence of:

- The increase in money supply: Including the 4,000-billion-RMB-stimulus package released in 2008 along with high level of increasing money supply from the program.

- Low — artificially low — interest rates leading to credit expansion during the period 2008-2016.

- Government policies which led to real estate revenues in order to supplement government coffers. Real estate markets contribute heavily the total revenue of the local government.

Austrian-school economists argued that a change in the structure of production follows a change in the interest rate. In their model, the interest rate is determined on the market for loanable funds. According to Austrian business cycle theory (ABCT), money injection and lowering interest rates are two sides of the same coin as they force the interest rate to be below the real rate. Given the fact that the interest rate is now lower, long-term projects are made possible relative to other short-term projects. Frame it in a different way, now the net present value of return is higher due to the artificially low rate. Consequently, it encourages enterprises to take loans to invest, thus investment increases.

On the other hand, resources are also pulled toward early stages of production, including the construction of real estate and other kinds of fixed assets such as land. As explained above, available credit that can be used to purchase land and for construction will be cheaper. The demand for housing construction and land will increase and then push up their price. Like other types of investment, the net present return of owning house and land will potentially increase. This spiral effect will spread out the whole economy and inevitably stimulate a real estate bubble.

As a result, long-term, malinvested projects that seemed to be feasible will eventually become impossible to carry out. Resources pulled toward early stages of production will need to be liquidated, and the economy will inevitably suffer a predictable recession.

I. Money Injection

On 9 November 2008, the government of China released the 4 trillion RMB (US$586 billion) stimulus package, which was considered to be the stimulus for the economy when the recession became worse. The purpose of this stimulus package aims at investing in infrastructure, low cost housing, and other related markets. In the distribution of the package, infrastructure, Sichuan earthquake reconstruction, low cost housing, and rural livelihood made up 84% in total.

The goal of the government of China was to utilize the package to expand the credit availability for the business, especially for small and medium ones. It induced the local governments, especially Beijing, to increase their spending, as well as putting more pressure on local commercial banks to make cheap credit more easily available. As a result, their state-owned enterprises (SOEs) were supplied a large amount of financial capital to deploy the stimulus program. On the other hand, since revenue from the real estate market dominates the revenue of the local government of Beijing, in order to boost the local economy, governments continued to promote activities on the real estate market to increase their revenue for other public investment. Unfortunately, it led to a massive increase in fixed-asset investments, and more inefficient investment.

II. Artificially Low Interest Rates

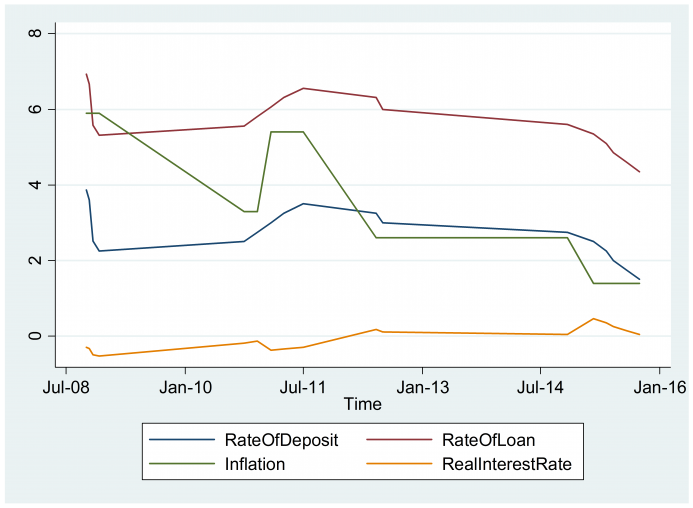

The government of China actively decreased interest rates for both commercial bank loans and for deposits at banks. The interest rate for loans decreased twice at the end of 2008 and 2012, with the lowest one was 5.31% on 12/2018, and approximately 4.5% was maintained from 2015 until now.

On the other hand, because the rate of deposit is always in between 2.5 – 3.5%, which is also the range of the inflation rate, the real interest rate approached zero or became negative.

When the real interest rate is not positive, money lenders, instead of maintain their level of savings, will change to other types of investment that can yield a higher return. Two major markets that are usually attractive for idle cash are the stock market and real estate. However, as a consequence of the 2008 financial crisis, the stock market of China suffered a great loss until the first quarter of 2014. With the decline of the stock market, in which the value of SSE Composite Index fluctuated only in between 2000 and 3000 yuan per share, real estate became the only market that attracted NSEs with idle cash.

Fixed assets have tendency to rise in price under a low interest rate regime. With large amounts of liquidity available for these assets, speculation sped up. Because of the resulting mass speculation, the price of real estate in Beijing increased rapidly by 20.2%, which is the fifth highest one in China, after Chongquing (27.0%), Shanghai (23.7%), Hangzhou (21.8%), Nanjing (20.5%).

Speculation is caused by low interest rates, but also by other national and local government policies designed to increase credit. From 2010, credit requirements for housing for households and small businesses were abolished. From 2011 to 2014, big cities including Beijing, Shanghai, Shenzhen simplified the requirements for housing credit, as well as other endowment on housing tax. Moreover, People’s Bank of China forced financial institutions to lower their reserve requirement 3 times during this period. As a result of these policy changes, investment on real estate, even risky investment, increased rapidly by the commercial banking system. Consequently, the real estate market continued to be stimulated and expanded.

III. The Expansion of the Real Estate Market

Noting the distribution of fixed assets investment, it can be seen that the increase mostly came from the real estate market, not from other production sectors.

The most significant periods of growth in FAI in Beijing can be seen in 2009 and 2012, in which the growth rates of infrastructure are 26% and 27.8% respectively. In 2008, the total investment for real estate in Beijing was only 19 billion RMB. In mostly doubled in 2016, with 40 billion RMB flowed to the real estate market. Among different fixed assets investments, the investment for real estate made up the most, with the peak is 52.8% in 2010 and 2015.

However, the investment in real estate of Beijing declined slightly in the period from 2015 to 2016. In 2014, after the national government realized that the growth of the real estate market was out of their control, they decided to suspend some supporting policies on housing to stabilize the market, such as increasing the minimum reserve requirement 6 times and abolishing low tax policy for real estate. The decrease of real estate investment during this period can be explained as a consequence of these regulation.

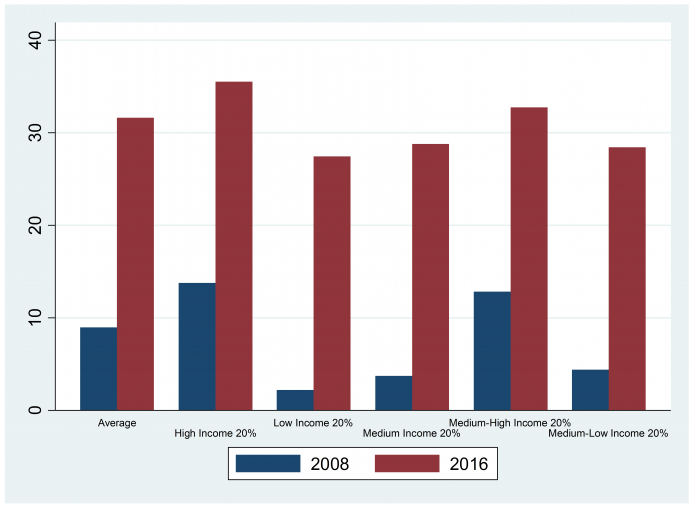

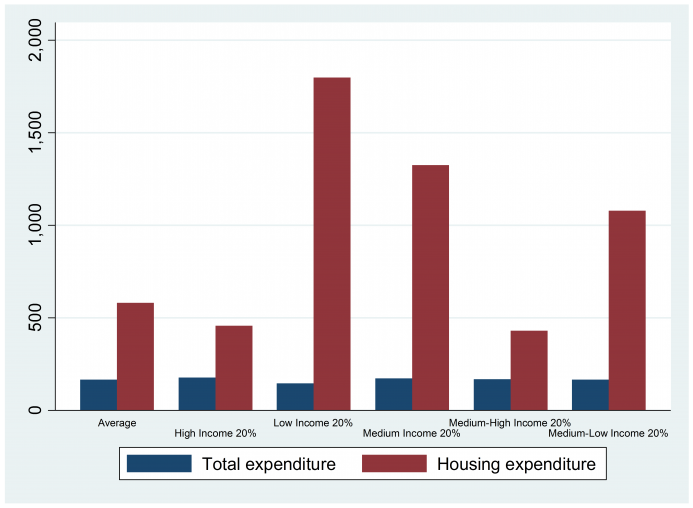

Classifying FAI by type, mostly all of the FAI is domestic, while foreign FAI made up only 3-4% of total FAI. While other types of FAI have been growing slightly, from 2008 to 2016, state-owned FAI increased by 183%, which equals 119.94 billion RMB. By the fact that domestic FAI, especially state-owned FAI always made up a large proportion in total FAI, it is likely prices in fixed assets like real estate are affected more by government policy than real market factors.Another characteristic of a speculative bubble is that the speculative purchases make up a large proportion in total expenditure. In this case, it is the relative rate of housing expenditure comparing with total expenditure, which measures the capacity to bear the housing price of households. Beijing is the city that has the highest real estate prices in the country, with 27.497 RMB per meter square.5 In comparison to the disposable income, it was one of three highest increasing rate, with Shanghai and Guangzhou. While the disposable income increased only 828% from 1993 to 2011, the increase in housing prices was 2242%. The difference between the total expenditure and the expenditure on housing also reflected the fact that the increase of price was out of range for most households. In 2008, housing expenditure was only 8.95% of the total expenditure, however, in 2016, it already increased to 31.59%. Moreover, after 8 years, while the growth of total expenditure is only 164%, the following growth of housing expenditure is 580%. Especially, it happened mostly on the low income group to the medium income group. For the low income, the growth of housing expenditure was approximately 1800%.

For now, it can be concluded that there are two major factors have caused the bubble on FAI and real estate in Beijing: money injection on behalf of fiscal stimulus and credit expansion under artificially low interest rate. These two factors led to speculation and rapid investment, since it created a multiplier effect with a massive amount of extra cash flowed into the real estate market. In light of ABCT, it can be predicted that this bubble, with its hidden risks, will eventually lead to economic recessions. For the case of Beijing specifically, real estate is one of the most important markets that dominate the development strategy of both local government as well as China. Thus, in the long run, these risks can become severe for the whole macroeconomy.

*About the author: Trieu Nguyen is currently a student at Hillsdale College majoring in Economics and Mathematics, and a graduate of Mises University and Vietnam Institute for Economic and Policy Research.

Source: This article was published by the MISES Institute

- 1.World Bank. (2019), “GDP Ranking,” available at: http://datacatalog.worldbank.org/dataset/gdp-ranking (accessed 18 May 2019).

- 2.INFRA Update. (2010), ” Supporting China’s Infrastructure Stimulus Under the INFRA Platfrom”, available at: https://siteresources.worldbank.org/INTSDNET/Resources/5944695-1247775731647/INFRA_China_Newsletter.pdf (accessed 20 June 2018).

- 3.Ibid.

- 4.Tradingeconomics. (2018b), “China Shanghai Composite Stock Market Index”, available at: https://tradingeconomics.com/china/stock-market (accessed 11 July 2018).

- 5.Statista. (2017), “China: Sale Price of Real Estate by Region 2016”, available at:

https://statista.com/statistics/242877/sale-price-of-real-estate-in-china-by-province. (accessed 27 June 2018) - 6.Ibid.

- 7.Ibid.