Brief Assessment Of COVID-19 Pandemic Impact On China’s Provincial Economies In First Quarter – Analysis

By Anbound

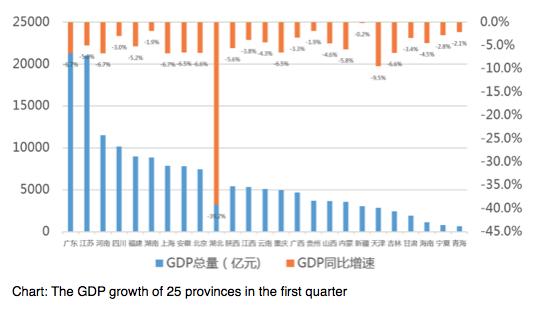

In the first quarter this year, China’s real GDP fell by 6.8% year on year due to Covid-19, the first quarterly GDP decline in 40 years. Judging from the current situation in each region, except for Zhejiang, Hebei, Shandong, Heilongjiang, Liaoning, and Tibet, 25 provinces across the country have released GDP-related data for the first quarter of this year. The negative GDP growth in these 25 provinces indicates that COVID-19 has exerted different influence on the whole country.

From the perspective of growth rate, the most affected by the pandemic is the worst-hit area of Covid-19, Hubei province, where the economic downturn is the most severe. In the first quarter, the GDP of Hubei province fell by 39.2% year-on-year to RMB 637.935 billion, of which fixed asset investment fell by 82.8%; the total retail sales of consumer goods was RMB 293.943 billion, down 44.9% year-on-year; industrial enterprises above designated size, foreign trade, and the other main industries have suffered significant contraction, thus making the province the most economically shrinking province in the country.

Tianjin’s economic growth is also at the bottom of the ranking, where GDP fell 9.5% in the first quarter from a year earlier. Judging from last year’s situation, Tianjin’s GDP growth in 2019 was only 4.8%, and the impact of the pandemic has accelerated the slowdown of economic growth in Tianjin. Among them, the added value of the primary industry was RMB 2.344 billion, down 11.5% year on year. The added value of the secondary industry was RMB 85.292 billion, down 17.7% year on year. The added value of the tertiary industry was RMB 19.799 billion, down 4.9% year on year. It shows that the industrial sector in Tianjin is greatly affected by the pandemic, and the production shutdown and supply chain disruption during the pandemic has a great impact. On the other hand, industries in Shanghai and Guangdong were the most affected. In the first quarter, the added value of the secondary industry in Shanghai and Guangdong was RMB 174.523 billion and RMB 797.807 billion respectively, down 18.1% and 14.1% year-on-year respectively.

The economic growth rate in the economically developed areas such as Beijing, Shanghai, Guangzhou, Anhui, Henan, Chongqing, and other provinces surrounding Hubei, generally fell below -6.5%. The economies of these areas have been hit hard by the pandemic as population movements have severely affected economic activity. However, Hunan province, which is also adjacent to Hubei, was less affected, with GDP only fall by 1.9%, mainly because its economy was less affected by Hubei and was relatively independent. The GDP of Sichuan, the most populous province, also falls by only 3%. On the one hand, Sichuan itself has a relatively independent economy, relatively complete industrial chain, and consumer market, and it is less influenced by the outside world. On the other hand, as a populous province, Sichuan’s employment is mainly local and not restricted by labor mobility, hence it is relatively less affected by the pandemic.

Judging from the current situation of the 25 provinces and cities, except Hubei and Tianjin, the growth rate of the remaining 23 provinces higher than the national GDP growth rate of -6.8% in the first quarter. Among them, Xinjiang’s GDP growth rate in the first quarter ranked first in the country, down 0.2% year-on-year, and the growth rate was 6.6 percentage points higher than that of the country. In addition, Hunan, Guizhou, Qinghai, Ningxia, and other provinces saw their GDP growth rate higher than -3% in the first quarter. In Guangxi and Gansu, the economic growth rates were -3.3% and -3.4% respectively, which were significantly greater than the national level.

In terms of GDP size, Guangdong and Jiangsu are still among the top two provinces in China, with aggregate GDP exceeding RMB 2 trillion in the first quarter of this year. The nominal GDP growth of the two provinces has significantly shrunk, and the corresponding major economic indicators have also been adjusted downwards. Meanwhile, the added value of each industry has decreased, indicating that the pandemic has a prominent short-term impact on economic growth. Currently, there are four provinces whose GDP exceeds RMB 1 trillion, namely Guangdong, Jiangsu, Henan, and Sichuan. Xinjiang, Shanxi, and Yunnan were slightly affected by the COVID-19, and their GDP rankings were improved.

In the first quarter, Xinjiang’s GDP was RMB 305.551 billion, down 0.2% year on year, and its nominal GDP increased by RMB 6.315 billion. The overall economic performance of Xinjiang is stable and tends to positive growth. Therefore, the economic performance of Xinjiang is better than in most provinces, and it is expected to grow steadily again in April. Hunan and Guizhou are among the few provinces with positive nominal GDP growth. In the first quarter, the GDP of these two provinces was RMB 662.482 billion and RMB 370.404 billion respectively, with corresponding nominal GDP growth being RMB 7.644 billion and RMB 1.356 billion.

Judging from the first quarter’s performance, western provinces as a whole were more resilient to the pressures. Some analysts believe that this is not because the western provinces have a better economic background, but because the industries of the western provinces, including Hunan, Jiangxi and other inland provinces, are themselves labor exporting provinces and the local industries were mainly rely on local labor and less dependent on foreign labor than that of coastal areas. In addition, these western provinces have smaller, less outward-looking economies, and therefore less vulnerable to the pandemic. Due to the impact of the pandemic, the coastal areas with massive population outflows in the Spring Festival travel season have been seriously disrupted the production, making it more difficult to resume production in coastal areas than in inland provinces. At the same time, due to the high degree of economic internationalization in the eastern region, it is greatly affected by the obstruction of exports and imports.

Overall, the impact of Covid-19 on China’s economy in the first quarter of this year was widespread. All provinces were basically suffered negative growth and increased economic downward pressure. But at the same time, as ANBOUND noted, the resilience of the Chinese economy has been generally strong under the outbreak, with no major collapses except in Hubei. Even Hubei, which has been under lockdown, has not experienced any major economic downturn. Its main reason comes from two aspects of support, one is the basic living consumption activities based on the large population base, and the other is to ensure the basic operation of the city’s water, electricity, heat, and other infrastructure. In comparison with other provinces, the situation was actually the same. Some basic consumption and the operation of cities have limited the downward trend of the local economy. Some provinces in the western region that had a relatively fast economic growth rate were relatively less impacted and recovered faster, but due to their smaller scale, their contribution to the overall economy is still limited. Some areas in the eastern coastal areas have been greatly affected by the impact of the pandemic, and due to the large size of the economy, they have to assume the main role of “steady growth” in the economic recovery. However, the recovery process is also affected by the external import of the coronavirus, the decline in international trade demand, and supply. Due to various influences, the pressure in the economic recovery process is greater. In particular, the recovery and improvement of the resilience of China’s economy still require more resources input and in-depth economic restructuring.

Final analysis conclusion:

According to the regional economic data released so far, the Covid-19 pandemic has a nationwide impact on the economy, and the negative growth in most of the provinces indicates that the economy is under great downward pressure. However, due to the different economic characteristics, the regional economies show different resilience. But while the pandemic continues to change, the recovery of the overall economy will not be easy and will require an overall adjustment of the macro policies.