Oil Market Showdown: Can Russia Outlast The Saudis? – Analysis

By OilPrice.com

By Dalan McEndree

“Two men enter, one man leaves, two men enter, one man leaves, two men enter…” — Mad Max: Beyond Thunderdome

November 27, oil consuming countries will celebrate the first anniversary of the Saudi decision to let market forces determine prices. This decision set crude prices on a downward path. Subsequently, to defend market share, the Saudis increased production, which exacerbated market oversupply and further pressured prices.

While the sharp decline in crude prices has saved crude consuming nations hundreds of billions of dollars, the loss in revenues has caused crude exporting countries intense economic and financial pain. Their suffering has led some to call for a change in strategy to “balance” the market and boost prices. Venezuela, an OPEC member, has even proposed an emergency summit meeting.

In practice, the call for a change is a call for Saudi Arabia and Russia, the two dominant global crude exporters, which each daily export over seven-plus mmbbls (including condensates and NGLs) and which each see the other as the key to any “balancing” moves, to bear the brunt of any production cuts.

Both, it would seem, have incentive to do so, as each has lost over $100 billion in crude revenues in 2015—and Russia bears the extra burden of U.S. and EU Ukraine-related economic and financial sanctions. Yet, while both publicly profess willingness to discuss market conditions, neither has shown any real inclination to reduce output—in fact, both countries seem committed to keeping their feet pressed to their crude output pedals. In the course of 2015, both have raised output and exports over 2014 levels—Saudi Arabia by ~500 and 550~ mbbls/day respectively and Russia by ~100 and ~150. The Saudis have repeatedly cut pricing to undercut competitors to maintain market share in the critical U.S. and China markets, while the Russian Finance Ministry recently backed away from a tax proposal which Russian crude producers said would reduce their output.

This apparent bravado notwithstanding, the two countries’ entry into the low-price Crudedome is ravaging their economies. Should crude prices decline from current levels, or even just stagnate, it is possible neither country will exit the CrudeDomeunder its own power.

IMF WEO Data: Recessions as far as the Eyes can See

Both Saudi Arabia and Russia paint positive portraits on current and future economic performance. At a conference in Moscow on October 14, President Putin said that Russia had reached if not passed the peak of its economic crisis and predicted economic growth in coming years. Arab News announced in the first paragraph of its report on Q2 Saudi economic performance that Q2 GDP grew 3.79 percent year-over-year, up from 2.3 percent growth in Q1.

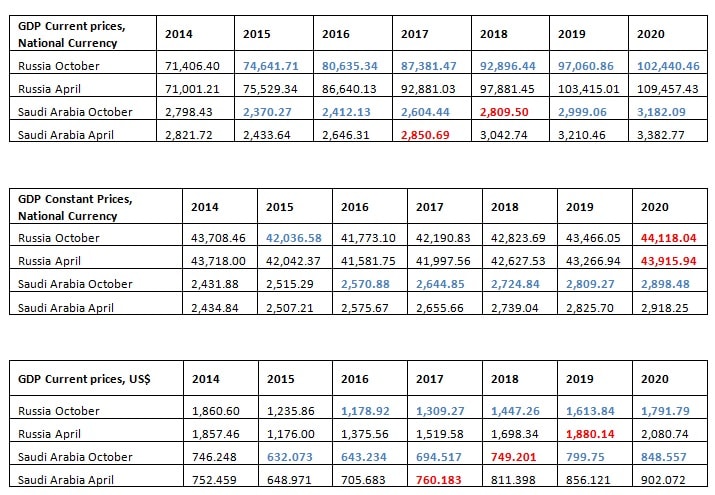

Yet IMF October 2015 and April 2015 World Economic Outlook projections for the Russian and Saudi economies a paint pessimistic portrait, as the following three tables, forecasting GDP through 2020 in current prices/national currency, constant prices/national currency, and current prices/US$ show (all data in billions).

– In each of the data series, except the April and October ones, Russian current prices/national currency and the Saudi constant prices/national currency series, GDP declines from 2014 to 2015. (When adjusted for estimated inflation, however, the forecasts for Russian GDP current prices/national currency show GDP declining from 2014 levels—to 64,039 billion Rubles given inflation of 17.943 percent in the April series; in the October series, to 64,463 billion rubles, given inflation of 15.789 percent. The growth shown in the Saudi constant prices/national currency series results from the reduction in the deflator, which the Saudi National Statistical Office, Central Department of Statistics and Information uses to convert current national currency GDP into constant national currency. For example, decreasing the deflator from 115.073 to 94.234 in the October series and to 97.066 from 115.889 in the April series turns a decrease in GDP in current prices into an increase in GDP in constant prices).

– Between the April and the October forecasts in most of the data series, GDP deteriorates (blue font). Crude prices bear much of the responsibility: the April forecasts were based on $58.14 and $65.65 per barrel oil in 2015 and 2016 respectively, while the October projections are based $51.62 and $50.36 respectively.

– The year in which GDP exceeds 2014 GDP is noted in red font. As a result of the deterioration in GDP forecasts between April and October in the Saudi current prices/national currency series, GDP does not exceed 2014 GDP until 2018 instead of 2017; in the Russian current prices, US$ series, GDP exceeds 2014 level after 2020 instead of 2019; in the Saudi current prices/US$, the recovery is pushed to 2018 from 2017. (In inflation adjusted terms, Russian GDP in current prices, national currency would be below 2015 levels in 2020).

In Russia, the impact of low crude revenues on GDP has raised questions about Russia’s long term economic prospects. Some see Russia’s economic growth potential as 1 percent annually or less due to low energy prices, low productivity levels, and a shrinking population, while Alexei Kudrin, finance minister from 2001 to 2011, recently commented that Russia’s growth model for the last fifteen years—using income from energy exports to drive up wages, domestic demand and therefore growth—will no longer work. With the government strapped for funds, and energy income no longer supporting domestic demand, some see investment as the sole possible driver of growth.

IMF WEO Data: Budget Deficits as far as the Eyes can See

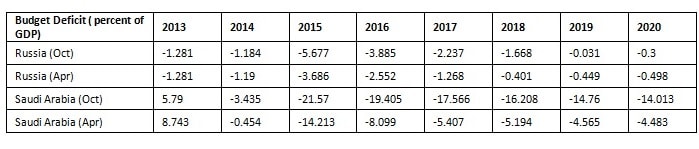

Both the Saudi and Russian governments depend on energy revenues to fund their budgets—oil funds ~90 percent of the Saudi budget and oil and natural gas ~52 percent of the Russian budget. With the decline in prices, the Saudi budget anticipates a deficit of 20 percent of GDP in 2015 and the Russian budget a deficit of 3.3 percent of GDP. The April and October WEO budget projections in national currencies (Rubles and Riyals) show the deficits decreasing, but continuing through 2020 for both countries:

The following table shows that as a percentage of GDP, the deficits decline steadily through 2020. However, as a percentage of GDP, the WEO October projections show the Saudi deficits remain double-digit through 2020—the potential impact of which will be discussed in the section on currencies.

As planning for the 2016 fiscal year proceeds, fiscal reality is forcing both governments to scramble for new sources of revenues and/or opportunities to cut spending to reduce their budget deficits. The Russian government suspended the budget rule using a long term average of crude prices to set spending, since the resulting $80 average price would have dictated unreasonable spending in 2016.

President Putin ordered a 10 percent cut in Interior Ministry personnel, imposed a one million headcount ceiling on this ministry, and planned cuts in Kremlin headcount. The Finance Ministry sought a change in the mineral extraction tax formula to generate an additional 609 billion rubles in 2015 and 1.6 trillion through 2018, but pressure from the Economic and Energy Ministries and Russian producers forced the Finance Ministry to consider alternatives with less negative impact on crude production. In addition, the government reportedly is taking some $13 billion from national pension funds, while the Russian Central Bank is preparing proposals on government pension guarantees that would shift some pension funding burden from the government budget to companies and individuals.

The Saudi government is also scrambling. After an eight year hiatus from issuing sovereign debt, the Saudi government announced a plan during the summer to borrow $28 billion in 2015 and launched the borrowing with a $5 billion offering in August. The Ministry of Finance has banned contracts for new projects, hiring and promotions, and purchase of vehicles or furniture in the fourth quarter, while the newly created Council for Economic and Development Affairs must now approve all government projects worth more than $27 million. The Saudi government also is preparing to privatize airports and contemplating seeking private financing for infrastructure projects.

The budget situation puts the Saudi government in a difficult situation. On the one hand, the size of the deficits requires drastic cuts in spending, but such drastic cuts would impact politically sensitive areas such as energy subsidies, government employment opportunities for Saudi citizens, education, and economic development projects. On the other hand, depleting Saudi government reserves to finance the deficits will put the Saudi sovereign credit rating at risk, which would raise the cost of borrowing as well as pressure the Saudi currency (the consequences of which are discussed below).

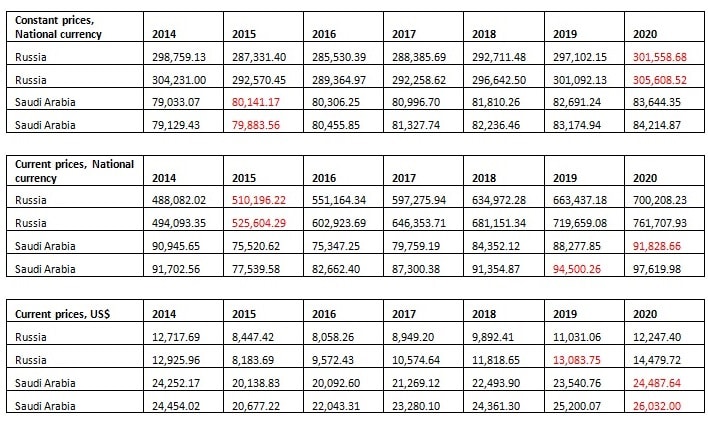

IMF WEO Data: Lagging Per Capita Income as far as the Eyes can See

In both Russia and Saudi Arabia, the governments have attempted to shield their citizens from job cuts. In Russia, the government has discouraged businesses from shedding employees, while the Saudi government has maintained headcount in the government and government-related bodies, where most Saudis nationals are employed.

In terms of income, however, the situation is different. IMF WEO projections show per capita income in 2015 declining from 2014 levels in both Russia and Saudi Arabia, and only slowly recovering (the year exceeding 2014 levels in red font). (The increases in per capita income in the Russia current prices, national currency and in the Saudi constant prices, national currency series results from the same factors discussed in the section on GDP).

Impact on Currencies

The steep decline in crude prices has pressured both currencies. The Ruble has suffered two curses. First, it has declined substantially relative to “hard” currencies, such as the US$, the Euro, British Pound, and the Swiss Franc. Against the U.S. dollar, it depreciated ~29 percent from November 27, 2014 to October 13, 2015 (48.58/US$, to 62.77). Second, it has been and continues to be highly volatile, its fate tied to moves in crude prices. The Ruble reached its post-November 27 low on June 27 (33.73/US$) and twice reached its high of ~70/US$ (January 30 69.47, August 24 70.89). A chart is available on Bloomberg.

The pressure on the Ruble forced the Russian Central Bank to take a series of emergency measures. At the end of last year, it spent ~$100 billion from its foreign currency reserves to defend the Ruble (it finally abandoned the defense when it proved futile and allowed the Ruble to float). In the same period, it extended emergency “hard” currency funding to major Russian banks and businesses with “hard” currency obligations that were coming due at the end of 2014. The Central Bank also sharply raised interest rates—to 17 percent at one point—and has kept the rates high to defend the Ruble (currently ~11 percent). Two examples illustrate the impact of Ruble devaluation:

– Transaero, until recently Russia’s second largest passenger airline, attributed being forced into bankruptcy to high interest rates and a devalued Ruble—the former raised the cost of financing, the latter pushed up prices in Rubles and therefore reduced demand in Russia for international flights and increased the cost, in Rubles, of repaying foreign currency denominated loans and interest.

– The Association of European Businesses in Russia recently announced that sales of new cars and light commercial vehicles contracted 29 percent in August year-over-year and forecast a 37 percent decline for all of 2015. It cited price increases that the car manufactures were forced to take to cover the increased cost of foreign parts and systems used in domestic auto manufacturing.

Volatility is equally pernicious. As another Bloomberg article points out, Russian businesses, unsure of what the value of the Ruble will be long term or even day-to-day, are deferring investment despite generating substantial (Ruble) profits—the very investment which some believe the Russian economy needs to grow and which has been contracting for 20 months.

The Saudis have avoided both Riyal depreciation and volatility. The government has insisted it will keep the Riyal pegged at 3.75/US$ and financial markets thus far have taken comfort from Saudi reserves (estimated to exceed $660 billion). However, as deficits deplete reserves and events occur that threaten the peg and Saudi oil-related export revenues, this comfort quickly could dissipate. After the Chinese Central Bank unexpectedly devalued the Yuan by ~2 percent against the US$, bets that the Saudis would be forced to abandon the peg spiked.

Breaking the peg would devastate the Saudi economy. It would drive up the cost of imports—and Saudi Arabia depends substantially on imports for a wide variety and high percentage of necessary consumer, business, and government goods and services—from food to oil, petrochemical, and other industrial equipment and services to military equipment, supplies, and training. It would also harm the Saudis who recently have been increasing their exposure to “hard” currency denominated loans.

Sovereign Wealth and Foreign Currency Reserves

Both the Saudis and the Russians are drawing down reserves they accumulated during the $100-plus/barrel crude price era to finance their spending. Over the nine months to July 2015, Saudi reserves declined $76 billion, from $737 billion to $661 billion, implying an annual rate of $100 to $130 billion. Should large withdrawals continue, or the amounts increase, confidence in the Riyal will sink.

Besides the $100 billion the Central Bank spent defending the Ruble, the Russian government has used funds from its sovereign wealth funds (the National Welfare Fund and the Reserve Fund) to reduce to fund priority projects, particularly in the energy industry—Rosneft sought one of the largest amounts. In June, Stratfor put the draw on the sovereign wealth funds at $44 billion.

China: The Sword of Damocles

In an era of low crude prices, modest economic growth, and modest crude demand growth, both Saudi Arabia and Russia (and other crude exporters) look to China as a source of incremental revenue to make up for the massive absolute declines in revenue and are prepared to compete intensely for market share.

One can imagine, then, the panic in Riyadh and Moscow when they contemplated the implications of the Chinese Central Bank’s decision to devalue the Yuan by ~2 percent against the U.S. dollar and the possibility this was the first salvo in a series of devaluations.

– For the Saudis, devaluation, if continued, will force the government to decide between volume and revenue. Pegged to the US$, Saudi crude, priced in US$ will become more expensive for the Chinese. It will reduce demand for Saudi crude and/or make the crude of other exporters—e.g. the Russians—whose currencies float. Yet reducing the US$ price to support volumes to China will reduce crude export revenues, which, if sufficiently substantial, could undermine confidence in the Saudi economy and therefore the Riyal peg to the US$.

– For the Russians, the Chinese Central Bank announcement possibly produced excitement at the prospect of competitive advantage over the Saudis in pricing. Quickly, however, excitement may have turned into anxiety. Neither side has made public critical details—including the currency or currencies in which sales will be settled and priced—of three bilateral energy megadeals: Rosneft’s $270 billion 2013 agreement to supply 300,000 mbbl/day annually to China for 25 years; the $400 billion, 30 year agreement signed in 2014 to supply natural gas to China from Eastern Siberia; and the negotiations underway to supply natural gas from Western Siberia.

Are prices set in US$, Rubles, Yuan, a basket of currencies (US$, Euro, Swiss Franc)? Are the Chinese expected to pay in Yuan at the Yuan/Ruble exchange rate? In Rubles at the Ruble/Yuan exchange rate? In Yuan at the Yuan/US$ exchange rate? Each alternative has different implications for Rosneft’s and Gazprom’s gross and net revenues from the sale of crude (Rosneft) and natural gas (Gazprom).

And the Winner is…

Despite the intense pain they are suffering in the low price Crudedome, both the Russian and Saudi governments profess for public consumption that they are committed to their volume and market share policies.

This observer believes the two countries cannot long withstand the pain they have brought upon themselves—and this article only scratches the surface of the negative impact of low crude prices on their economies. They have, in effect, turned no pain no gain into intense pain no gain and set in motion the possibility neither will exit the low price Crudedome under its own power.

Article Source: http://oilprice.com/Energy/Oil-Prices/Oil-Market-Showdown-Can-Russia-Outlast-The-Saudis.html

The article is another lie by the media which defends the imperialist agenda of the dictatorship of the financiers. The article clearly makes the point that the Kingdom of Saudi Arabia is to blame for the economic slowdown in the emerging countries and the global economy. The article contends that that the driving force causing the slowdown or even the global recession is the increased oil production coming from the KSA, and if the Kingdom cuts oil production, then the price of oil will rise; hence, the global economy will be recovered. This analysis is totally misleading and incorrect, because the global economic slowdown has been generated by Bush’s wars and low real investment rates in the world due to central banks’ money printing (or quantitative easing). The story is as follows. It is true that the KSA was producing ten million barrels of oil a day and oil was expensive hitting $140 in 2008. The high price of oil was a bubble created by the Bushes’ wars which took Iraq out of the oil market since 1991. Later, Libya was taken out of the oil market, and the world lost about 6 million barrels of oil a day. Then Iran’s oil was taken out of the oil market due to US sanction, and other sanctions were imposed on Russia. These bad decisions created oil shortage, pushing oil prices to its highest level. This process allowed the world fracking oil industry to enter the oil market and to prosper at the expense of other oil countries; hence, oil production increases and the price declines. It is unfair to single out one producer to blame for the decline in oil price and the global economic slowdown. One can blame the Bushes’ and the Obama administration for the creation of artificial disturbance in the oil market and the bad economic policies used in US and Europe: low taxes on the wealthy, quantitative easing, and austerity, policies that created low profit rate in industries, poverty, unemployment, and debt.

Currently, the global recession is caused by the dislocation of economic activity generated by central banks’ money printing (Japan, USA, ECB, and China) or what is called quantitative easing. This policy started by Japan and the US Fed, a policy that has shifted real investment towards financials for higher returns, weakening real investments in the western countries. Money printing has created huge cash held by the wealthy individuals and corporations which engage in stock buyback rather than finding new opportunities to invest in industrial projects. Low investment rates have created a shortage of aggregated demand, which has affected negatively economic growth and employment. This money dislocation coupled with low taxes on the wealthy and austerity along with looting pension funds and wealth of depositors by the zero and negative interest rates have created massive inequality and poverty and huge amount of debt in the world (as there is about $200 trillion in debts) .