Median Household Wealth In America Is Going Nowhere – OpEd

By MISES

By Ryan McMaken*

Today’s headline at The Wall Street Journal looks wonderful: “U.S. Household Net Worth Neared $107 Trillion in Second Quarter.” The journal is reporting on a new report from the Federal Reserve.

Unfortunately, the fact that the aggregate national net worth is up doesn’t tell us much about how Americans are faring right now. The “$107 trillion” number is just one big number of all assets added up minus debts. Marketwatch sums it up:

“It’s important to stress that the Fed report doesn’t represent the experience for the typical household — this is a report about the aggregate. A separate Fed survey from 2016 showed a little more than half of all families owned stocks, while about two-thirds of households owned homes.”

For the sizable portion of Americans who don’t own homes or a substantial amount of stocks, the report only illustrates, yet again, that asset price inflation mostly benefits people who already own a sizable amount of assets. If you’re a young person looking to build a portfolio — or a prospective first-time home buyer, you’re facing some very high prices right now.

Moreover, not even every homeowner benefits, since the data suggests that homeowners in stylish housing markets are the primary beneficiaries of home price inflation. Americans who own property in less fashionable cities in flyover country aren’t seeing nearly as much growth in their net worth.

This is familiar territory for those who have been monitoring the inflationary practices of central banks over the past decade. Asset price inflation is great for those who already own plenty of assets. Everyone else isn’t quite so lucky. In other words, the rich are getting richer faster. The non-rich are probably just holding steady.

How About All Households?

It looks like those with plenty of stocks and real estate are doing well. On the other hand, median household net worth in the United States doesn’t look so good.

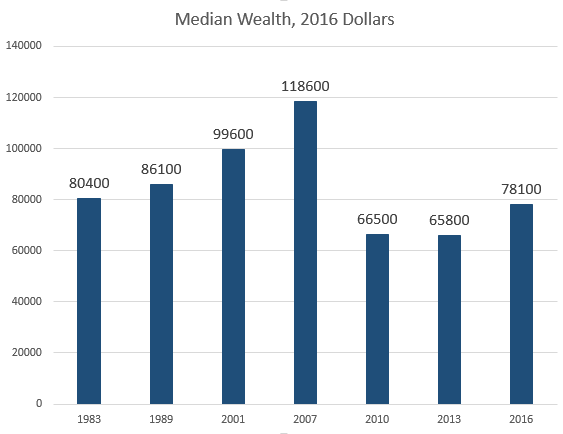

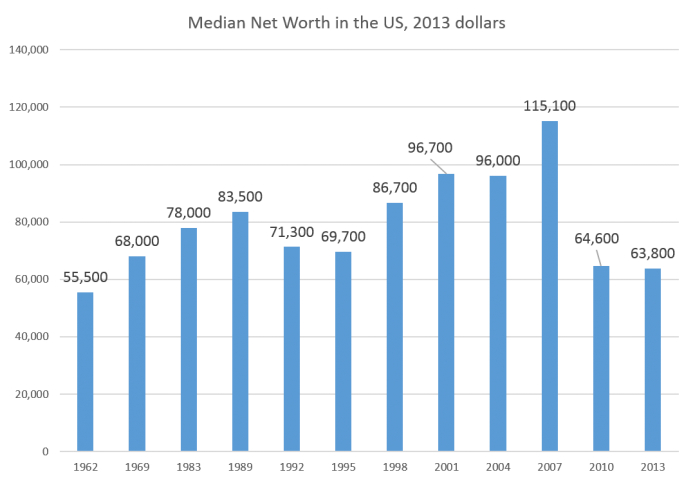

According to a 2017 report by Edward Wolff, median net worth in the United States, at least as late as 2016, was nowhere near returning to where it had been before the last financial crisis. In fact, in 2016, median net worth was about where it had been in 1983, more than three decades ago1:

According to a 2017 report by Edward Wolff, median net worth in the United States, at least as late as 2016, was nowhere near returning to where it had been before the last financial crisis. In fact, in 2016, median net worth was about where it had been in 1983, more than three decades ago1:

In this report, Wolff was updating previous research from 2014 which showed that median wealth in 2013 was still at 1969 levels2.

Median wealth has increased significantly from 2013 to 2016, but as of 2016 it remained down 33 percent from where it was in 2007.

It’s possible that in 2018, a full decade after the financial crisis, net wealth has recovered to its previous peak. We don’t know. But, even if median wealth finally recovers around 2018, what will happen to median wealth in the next recession if stock prices and home prices decline?

As Wolff shows in his report, the majority of wealth held by Americans (56 percent) is in the form of a principal residence, financial securities, and pension funds — which are themselves largely composed of financial securities.

As Wolff shows in his report, the majority of wealth held by Americans (56 percent) is in the form of a principal residence, financial securities, and pension funds — which are themselves largely composed of financial securities.

Will it also take a decade to recover from the next recession? Let’s hope not. But if the past decade is any indicator, we could be looking at 20 years of sideways movement in median wealth if something doesn’t change. Sure, overall aggregate wealth will continue to increase as the wealthy continue to see ongoing increases in the prices of their assets. Central-bank-fueled asset-price inflation will contribute to this.

Moreover, inflationary monetary policy directly benefits the politically well-connected at the expense of others, as recently explained by Thorsten Polleit:

There is an additional severe problem with central banks’ fiat money: It affects income and wealth distribution, and it does so in a non-merit-based, anti-free market way. To understand this, we have to consider that if and when the quantity of money increases in an economy, the prices of different goods will be affected at different points in time and to a different degree. In other words: A rise in the quantity of money changes — and necessarily so — peoples’ relative income and wealth position.

The early receivers of the new money will be the beneficiaries, for they can purchase goods at still unchanged prices with their fresh money. As the new money is passed from hand to hand, prices are rising. The late receivers are put at a disadvantage: They can purchase only goods at elevated prices with their new money. In other words: The early receivers of the new money get rich(er), the late receivers get poor(er). Needless to say, those who do not receive any of the new money will be worst off.

If we want to see better growth in wealth for ordinary people, it’s clear that the “stimulus” strategies of the past decade aren’t cutting it.

In fact, according to banking-industry researcher Karen Petrou, “Post-crisis [i.e., post-2008] monetary and regulatory policy had an unintended but nonetheless dramatic impact on the income and wealth divides.” In a recent interview with Petrou at Bloomberg, Petrou explains how new banking regulations have driven banks toward catering to the wealthy:

[C]apital requirements imposed after the banking crisis make it a lot more expensive for banks to do a startup small-business loan than go into wealth management. Startup loans are riskier than wealth management, of course, but the capital costs have become prohibitive, and banks don’t lose money on purpose. … it’s basically impossible for banks to make mortgage loans to anyone but wealthy customers.

This wouldn’t be the first time that government regulations benefit a small number of wealthy at the expense of everyone else. But combine this with inflationary monetary policy and we get at least a few insights into why median wealth in the United States is so sluggish.

About the author:

*Ryan McMaken (@ryanmcmaken) is the editor of Mises Wire and The Austrian. Send him your article submissions, but read article guidelines first. Ryan has degrees in economics and political science from the University of Colorado, and was the economist for the Colorado Division of Housing from 2009 to 2014. He is the author of Commie Cowboys: The Bourgeoisie and the Nation-State in the Western Genre.

Source:

This article was published by the MISES Institute

Notes:

1. “Household Wealth Trends in the United States, 1962 to 2016: Has Middle Class Wealth Recovered?” by Edward N. Wolff. NBER Working Paper No. 24085, Issued in November 2017 (http://www.nber.org/papers/w24085)

2. “Household Wealth Trends in the United States, 1962-2013: What Happened over the Great Recession?” by Edward N. Wolff. NBER Working Paper No. 20733, Issued in December 2014. (http://www.nber.org/papers/w20733)