Libya Energy Profile: Holder Of Africa’s Largest Proved Crude Oil Reserves – Analysis

By EIA

Libya joined the Organization of the Petroleum Exporting Countries (OPEC) in 1962, a year after Libya began exporting oil.1 Libya holds the largest amount of proved crude oil reserves in Africa, the fifth-largest amount of proved natural gas reserves on the continent, and in past years was an important contributor to the global supply of light, sweet (low sulfur) crude oil, which Libya mostly exports to European markets.

Libya’s hydrocarbon production and exports have been substantially affected by civil unrest over the past few years. In 2011, Libya’s hydrocarbon exports suffered a near-total disruption during the civil war, and the minimal and sporadic production that occurred was mostly consumed domestically. In response to the loss of Libya’s oil supplies in the summer of 2011, the International Energy Agency (IEA) coordinated a release of 60 million barrels of oil from the emergency stocks of its member countries through the Libya Collective Action—the first such release since Hurricane Katrina in 2005.

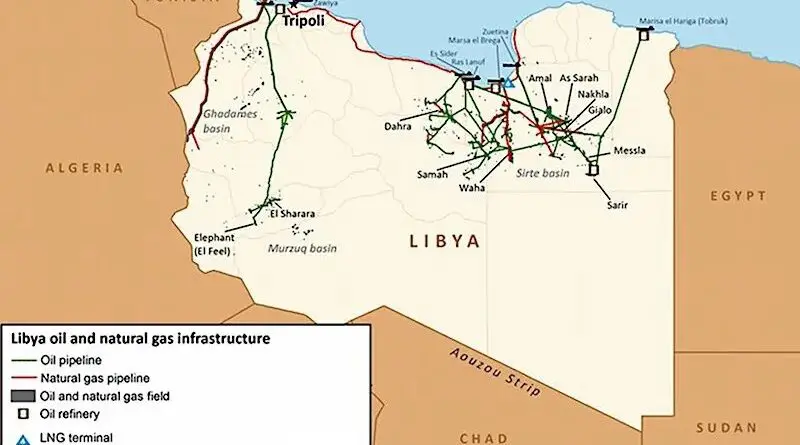

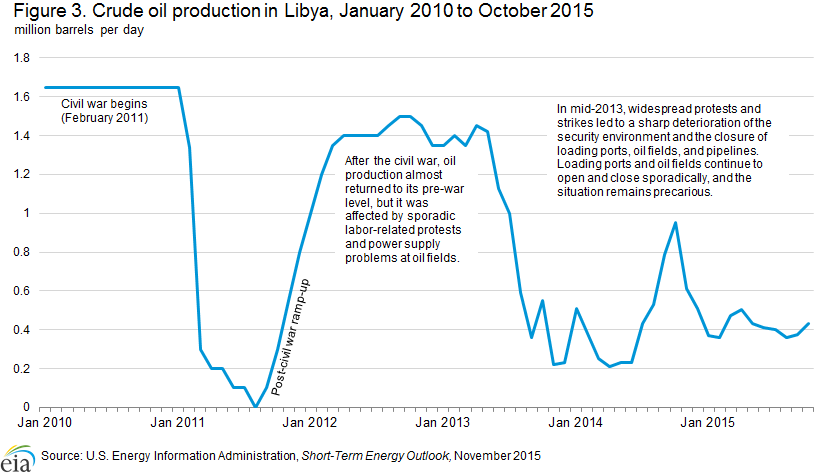

Libya’s oil production recovered in 2012, but it still remained lower than levels before the civil war. In mid-2013, a blockade at several major central-eastern ports (Figure 1) led by Ibrahim Jidran, a branch leader of the Petroleum Facilities Guard (PFG), coupled with protests and closures at oil fields and pipelines in the west, again caused the shut-in of most of Libya’s oil production. Oil production recovered somewhat during the second half of 2014 after deals were made to reopen some ports, but by late 2014 major disruptions reoccurred, and output has not recovered. From January to October 2015, Libya’s crude oil production averaged slightly more than 400,000 barrels per day (b/d), significantly below the 1.65 million b/d that Libya produced in 2010.

Libya’s economy is heavily dependent on hydrocarbon production. According to the International Monetary Fund (IMF), oil and natural gas accounted for nearly 96% of total government revenue and 98% of export revenue in 2012. Roughly 79% of Libya’s export revenue came from crude oil exports, which brought in about $4 billion per month (or about $48 billion total for the year) of net revenues in 2012.2 The U.S. Energy Information Administration’s (EIA) OPEC Revenues Fact Sheet shows that Libya’s net oil export revenues totaled $9 billion in 2014 as a result of the drop in oil export volumes. During the 2011 civil war, the drop in oil and natural gas production led to an economic collapse, and real gross domestic product (GDP) declined by 62% for the year. Libya’s GDP growth rebounded in 2012, reflecting the relative stability of oil production, but it contracted by almost 14% in 2013 and by 24% in 2014, reflecting the ongoing production disruptions.3

Petroleum and other liquids

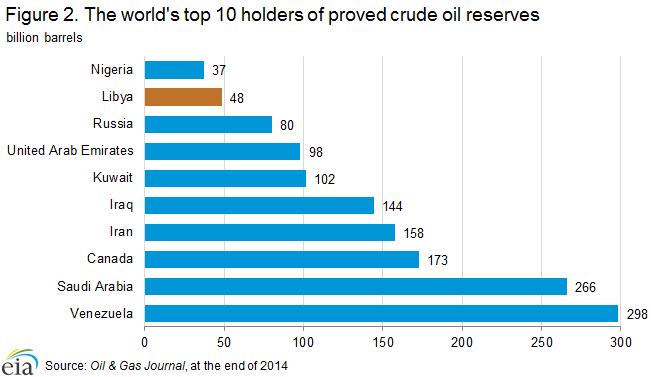

According to the Oil & Gas Journal (OGJ), Libya had proved crude oil reserves of 48 billion barrels as of the end of 2014—the largest endowment in Africa, accounting for 38% for the continent’s total, and the ninth-largest amount globally (Figure 2).4 Libya has six large sedimentary basins—Sirte, Murzuk, Ghadames, Cyrenaica, Kufra, and the offshore—that the government believes have substantial undiscovered potential. About 80% of Libya’s recoverable reserves are located in the Sirte basin, which also accounts for most of the country’s oil production capacity.5 Most of Libya remains unexplored, and ongoing civil unrest has prevented a large-scale exploration program.

Exploration and development

The country’s National Oil Corporation (NOC) has emphasized the need to apply enhanced oil recovery techniques to increase crude oil production at maturing oil fields. Before the 2011 civil war, the NOC claimed that capacity additions of about 775,000 b/d were possible from existing oil fields.

Before the 2013 oil sector crisis, the Libyan government had made several announcements of plans to increase crude oil production capacity to 1.7 million b/d by the end of 2013 and to 2 million b/d in the following years.6 In the past, Libya’s NOC emphasized investing in enhanced oil recovery (EOR) methods to counter depletion of reserves and to expand production capacity at existing fields. In 2009, the NOC announced a development program that entailed the development and rehabilitation of 24 oil and natural gas fields. The NOC’s development program identified several oil-producing fields where capacity could be expanded. The largest capacity additions were planned for the Waha (Oasis) fields, the Nafoura/Augila complex, and the El Feel (Elephant) field. The program aimed to boost total crude oil production capacity by 775,000 b/d from existing fields.7 Currently, plans to pursue any capital-intensive EOR projects in Libya have been postponed because of the political instability, volatile security environment, and lack of funds.

Management of the hydrocarbon industry

Prior to former Libyan leader Muammar Qadhafi’s ouster, Libya’s oil industry was run by the state-owned NOC. The NOC was responsible for implementing Exploration and Production Sharing Agreements (EPSA) with international oil companies (IOCs), as well as its own field development and downstream activities. The NOC subsidiaries include the Sirte Oil Company and the Arabian Gulf Oil Company (Agoco). The NOC continues to be the main body overseeing Libya’s oil and natural gas industry. However, the situation recently became complicated as Libya currently has two competing parliaments vying for power—the elected and internationally recognized House of Representatives and the recently reinstated General National Congress (GNC). The GNC appointed a Ministry of Oil, although the ministry’s role in the oil industry and the degree to which it is working with the NOC remain unclear.

Even before the 2011 civil war, policy makers in Libya had been debating the content for a new hydrocarbon law. The last hydrocarbon law passed in 1955 is outdated and does not include much information on natural gas development and EOR projects. The proposed new law aims to establish a unified national law that encompasses all aspects of the hydrocarbon sector. After the 2011 civil war, there were a series of regulatory reviews pertaining to the structure and management of the hydrocarbon industry. The focus was on expanding the downstream sector, reforming the subsidy program, restructuring the NOC, and potential changes to upstream contracts and terms. However, it appears that formal discussions have been stalled because of the continued unrest.

IOCs, mainly from the United States and Europe, participate in Libya’s hydrocarbon sector. IOC involvement in Libya experienced a resurgence in the mid-2000s as various rounds of sanctions were lifted by the United States and by the United Nations (UN). Companies were lured by the country’s bountiful resources, which outweighed regulatory uncertainties and the fact that contractual terms of the EPSA-IV (2005) licensing round were unfavorable to foreign investors. Since the fall of the Qadhafi regime, IOCs have been confronted with new types and unexpected degrees of political and security risks in Libya.

In the short term, IOC involvement in Libya will depend on resolution of political issues, operational security, and new regulatory legislation that is enacted in the future. After Qadhafi’s removal, Libyan officials have often attempted to reassure IOCs that they would honor the sanctity of existing contracts, while also reserving the right to review and revise those contracts that were secured through corrupt practices.

Production

Libya’s oil production was disrupted for most of 2011 because of the civil war, but it recovered relatively quickly following the cessation of most hostilities. The country’s oil sector was crippled again in mid-2013 as widespread protests led to a sharp deterioration of the security environment and the closure of loading ports, oil fields, and pipelines. Most of the country’s oil production continues to be disrupted.

Prior to the onset of hostilities in 2011, Libya had been producing an estimated 1.65 million b/d of mostly high-quality light, sweet crude oil. Libya’s production had increased for most of the previous decade, from 1.4 million b/d in 2000 to 1.74 million b/d in 2008, but production remained well below peak levels of more than 3 million b/d achieved in the late 1960s. Oil production in Libya from the 1970s to the 2000s had been affected by the partial nationalization of the industry and later by sanctions imposed by the United States and the UN that impeded the investment and equipment purchases needed to sustain oil production at higher levels.

Libya is currently going through another crisis that has crippled its oil sector. In mid-2013, a blockade at several major eastern ports led by Ibrahim Jidran, a branch leader of the Petroleum Facilities Guard (PFG), coupled with protests and closures at oil fields and pipelines in the west, caused the shut-in of most of Libya’s oil production. Oil production recovered somewhat during the second half of 2014 after deals were made to reopen some major ports, but by late 2014 major disruptions restarted and output has not recovered. From January to October 2015, Libya’s crude oil production averaged slightly more than 400,000 barrels per day (b/d), significantly below the 1.65 million b/d that Libya produced in 2010 (Figure 3; see EIA’s Short-Term Energy Outlook, Table 3c, for updated monthly crude oil production in Libya).

The situation in Libya has become even more complicated as vital oil infrastructure has been attacked or caught in cross fire, leading to severe damage that would take months, or maybe years, to repair. During the 2011 civil war, oil infrastructure, for the most part, was not damaged or targeted. However, in December 2014, the eastern Es Sidra export terminal, Libya’s largest export terminal, caught on fire after it was hit by a rocket. Many of its storage tanks were severely damaged, significantly lowering its export capacity. In addition, groups claiming to be affiliated with the Islamic State of Iraq and the Levant (ISIL) have severely damaged pipelines and vital equipment at oil fields in the eastern Sirte region that were operated by the Waha Oil Company, which includes companies from the United States, and an oil field operated by Total (Table 1).8

Libya also produces an estimated 50,000 b/d to 100,000 b/d of non-crude oil liquids, which include condensate and natural gas plants liquids. These non-crude oil liquids typically come from the Mellitah natural gas processing plant, a natural gas processing plant at the Intisar complex, and a natural gas liquids plant in Marsa al-Brega.

| Load ports | Region | Main fields | Refinery | Field operator | Lead foreign partners |

|---|---|---|---|---|---|

| Es Sider (Sidra) | central-east | Waha, Samah, Dahra, and Gialo | Waha Oil Company | ConocoPhillips, Marathon, Hess | |

| Mabruk (Mabrouk) | Mabruk | Total | |||

| Ras Lanuf | central-east | Nafoura | Agoco | none | |

| As Sarah/Jakhira b(C96), Nakhla (C97)1 | Wintershall | Wintershall, Gazprom | |||

| Amal, Naga, Farigh | Harouje | Suncor (PetroCanada) | |||

| Marsa al-Hariga (Tobruk)2 | east | Sarir, Messla, Beda, Magrid, Hamada3 | Ras Lanuf; Tobruk; Sarir | Agoco | none |

| Zueitina | central-east | Abu Attifel, NC-125 | Mellitah | Eni | |

| Nakhla (C97)1 | Wintershall | Wintershall, Gazprom | |||

| Intisar Complex and NC744 | Zueitina Oil Company5 | Occidental, OMV | |||

| Marsa al-Brega | central-east | Brega (Nafoura/Augila complex) | Marsa al-Brega | Agoco | none |

| Nasser (Zelten), Raguba, Lehib (Dor Marada)6 | Sirte Oil | none | |||

| Mellitah | west | El Feel (Elephant), mixed with condensate from Wafa and Bahr Essalam gas fields | Mellitah | Eni | |

| Zawiya or Zawia (Tripoli) | west | El Sharara (NC-115 and NC-186 fields) | Zawiya | Akakus | Repsol, Total, OMV |

| Bouri7 | west | Bouri (offshore) | Mellitah | Eni | |

| Farwah (Al-Jurf)7 | west | Al-Jurf (offshore) | Mabruk | Total | |

| 1Oil from Nakhla (C97) is mixed with oil from Eni’s Abu Attifel field. 2Most of the production from Agoco fields can be sent to Ras Lanuf and Marsa al Hariga (Tobruk). 3Oil from the Hamada field, which is located in the West, is sent to Zawiya. The oil is typically used domestically. 4Oil produced at NC74 is sent to Ras Lanuf. 5The Zueitina grade can also be sent to the Ras Lanuf terminal. 6Output from Lehib is mixed with output from one of Harouje’s fields and sent to Ras Lanuf. 7Bouri and Farwah (Al-Jurf) are offshore loading platforms of Mellitah. Sources: U.S. Energy Information Administration based on data from Energy Intelligence, Middle East Economic Survey (MEES), company websites, Oil & Gas Journal, and Lloyd’s List Intelligence (APEX tanker data) |

|||||

Crude oil exports

Libya typically exports most of its crude oil to European countries, with Italy being the leading recipient. The United States resumed importing crude oil from Libya in 2004 after sanctions were removed, although the amount imported typically is small.

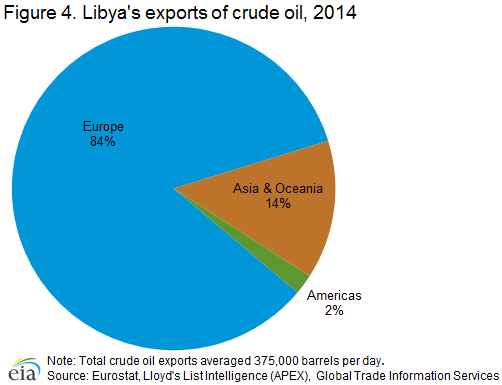

In 2014, Libya exported an average of 375,000 b/d of crude oil, which is lower than the 2012 level of almost 1.3 million b/d and similar to the 2011 level of 400,000 b/d during the civil war (Figure 4).9 Libya’s exports have been curtailed because of disruptions to oil production that escalated in mid-2013 and continued through 2015. Preliminary data shows that for the first seven months of 2015, Libya’s crude oil exports averaged 300,000 b/d.

Typically, most of Libya’s crude oil is sold to European countries. In 2014, about 84% of Libya’s crude exports were sent to Europe. The leading recipients were Italy, Germany, and France. The United States restarted oil imports from Libya in 2004, after sanctions were lifted. The United States imported 5,000 b/d of crude oil from Libya in 2014, less than the 43,000 b/d of crude oil imported in 2013.

Consumption and refining

Libya consumed an estimated 220,000 b/d of petroleum and other liquids in 2014, according to the International Energy Agency.10 Most of Libya’s oil consumption comes from its domestic refineries. According to OGJ, Libya has five refineries with a combined crude oil distillation capacity of 378,000 b/d (Table 2).11 Libya’s average total refinery utilization rate was only about 20% in 2013 and 2014 because of oil disruptions, according to data from IHS Energy.12

| Refinery name | Capacity (thousand b/d) |

|---|---|

| Ras Lanuf | 220 |

| Zawiya | 120 |

| Tobruk | 20 |

| Sarir | 10 |

| Marsa al-Brega | 8 |

| Total | 378 |

| Source: Oil & Gas Journal, at the end of 2014 | |

Natural gas

As with its oil sector, Libya’s natural gas industry recovered in 2012, but production still remained below the pre-war level. Libya’s rank as a producer and reserve holder is less significant for natural gas than it is for oil. About half of its natural gas production is exported to Italy via the Greenstream pipeline.

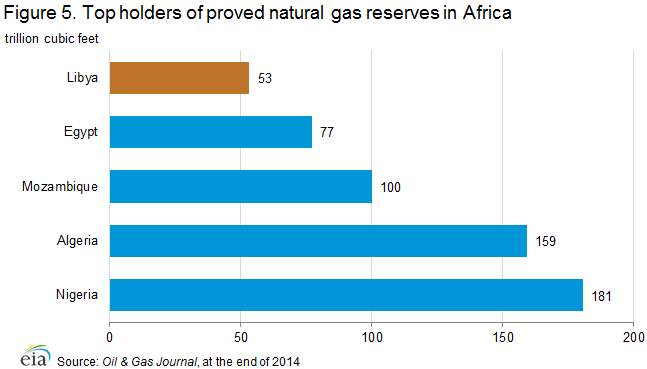

OGJ estimated that Libya’s proved natural gas reserves were 53 trillion cubic feet, making it the fifth-largest natural gas reserve holder in Africa (Figure 5).13 Before the transformative events of 2011, new discoveries and investments in natural gas exploration had been expected to raise Libya’s proved reserves in the near term.

Sector organization

Many of the same entities involved in oversight and operations of the oil industry exercise similar functions for natural gas. Likewise, some of the same questions and uncertainties about the future are equally applicable to both sectors. Libya’s natural gas sector is mostly state-run by the NOC and its Sirte Oil Company subsidiary. IOCs in Libya are less involved in natural gas production than they are in oil production, although Eni is a notable exception because of its stake in the large Western Libya Gas Project.

Exploration and production

Libya’s natural gas production and exports increased considerably after 2003 with the development of the Western Libya Gas Project and with the opening of the Greenstream pipeline to Italy. Italy is currently the sole recipient of Libya’s natural gas exports.

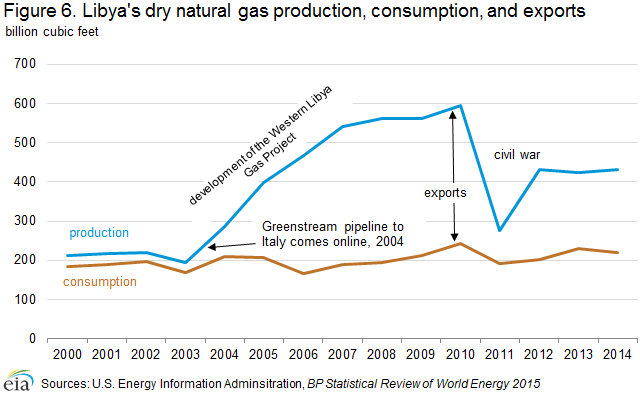

Libya’s dry natural gas production grew substantially from 194 billion cubic feet (Bcf) in 2003 to 594 Bcf in 2010. The Western Libya Gas Project (WLGP), which is operated by Eni and the NOC through the Mellitah Oil & Gas joint venture, accounted for most of Libya’s natural gas production growth after 2003. The WLGP includes the onshore Wafa field and offshore Bahr Essalam field. Typically, most of the natural gas produced from WLGP is exported via the Greenstream pipeline, and the remainder is consumed domestically. Most other natural gas output in Libya is produced by the NOC and its Sirte Oil Company subsidiary in the onshore Sirte Basin and is associated with oil production.

As with oil, Libya’s natural gas production was almost entirely shut in for sustained periods in 2011. Dry natural gas production averaged 277 Bcf in 2011, more than a 50% drop from the previous year. Natural gas production soon recovered to an average of 431 Bcf in 2012 and stayed relatively unchanged in 2013 and 2014 (Figure 6).14

The NOC has announced plans to increase the country’s natural gas production from offshore and onshore fields. New or expanded projects to support this goal include associated oil and natural gas fields in various stages of development, most notably Faregh, operated by Waha in the Sirte Basin, and Mellitah’s offshore Bouri field. Previously, the NOC planned to monetize the natural gas that is flared. Increased production of marketed natural gas would most likely result in a greater use of natural gas in the electricity sector and free up more oil for export. However, like all prospective oil and natural gas plans in Libya, greater development of the natural gas sector is contingent on support and certainty of political institutions and the security environment.

Consumption and exports

In 1971, Libya became the third country in the world, after Algeria and the United States (Alaska), to begin exporting liquefied natural gas (LNG). In the past, the country exported a small amount of LNG to Spain. However, Libya’s LNG plant was damaged during the 2011 civil war, and Libya has not exported LNG since early 2011.

In 2014, Libya consumed about 221 Bcf of dry natural gas, or slightly more than half of what the country produced. Libya exported the surplus of its production (211 Bcf in 2014) to Italy via the Greenstream pipeline (Figure 5).15 Natural gas production and exports have partially recovered since the 2011 civil war but still remain lower than pre-war levels. In 2011, natural gas exports dropped to 85 Bcf, about 75% lower than the previous year. Prior to the 2011 civil war, Libya exported natural gas via pipeline to Italy and in the form of LNG to Spain. However, Libya’s LNG plant was severely damaged during the 2011 civil war, and Libya has not exported LNG since early 2011.

GreenstreamLibya’s capacity to export natural gas increased dramatically after October 2004, when the 370-mile Greenstream pipeline came online. The pipeline starts in Mellitah, where natural gas piped from the onshore Wafa field and offshore Bahr Es Salam field is treated for export. The pipeline runs underwater to Gela in Italy (on the island of Sicily) and the natural gas flows onward to the Italian mainland. The Greenstream pipeline is operated by Eni in partnership with NOC. It has an annual capacity of 8 billion cubic meters (282 Bcf).16

Liquefied natural gas (LNG)In 1971, Libya became the third country in the world (after Algeria in 1964 and the United States in 1969) to export LNG. Libya’s only LNG plant, built in the late 1960s at Marsa al-Brega, is owned by the NOC and operated by Sirte Oil Company. However, the plant went offline in February 2011 as a result of damage sustained during the civil war and has not exported LNG since early 2011. Prior to its closure, the plant had been operating at partial capacity because of lack of maintenance and technology upgrades. Libya’s LNG was being exported to Spain and sold on a spot basis.17

Electricity

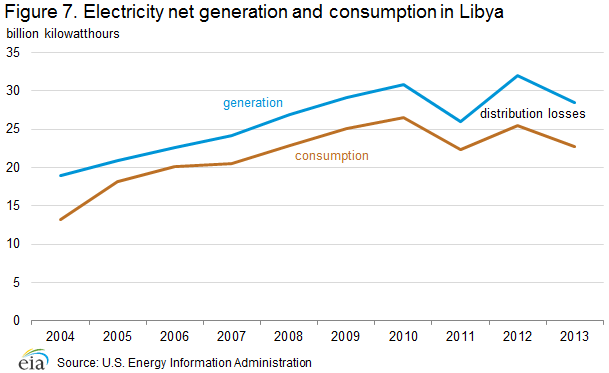

Electricity generation more than doubled from 2000 to 2010. Despite growth in electricity generation in Libya and a high electrification rate, Libya suffers from regular power outages.

According to the latest 2012 estimate from the International Energy Agency, 99% of Libyans living in rural areas and all Libyans living in urban areas had access to electricity, which is one of the highest electrification rates among African countries.18 Despite these high rates, the country suffers from power outages caused by electricity shortfalls to end users, including operators of oil and natural gas fields. Power shortfalls have affected production at some of Libya’s largest oil fields, including fields operated by Agoco and Mellitah.

Installed electricity generation capacity has grown by 50%, from 4.7 gigawatts in 2002 to 7.1 gigawatts in 2012. Electricity generation has grown at a faster rate than capacity, more than doubling from 2000 to 2010 (Figure 7). The growth in electricity generation reflects higher economic growth and greater investment in the oil and natural gas sectors, particularly after sanctions were lifted. In 2013, electricity generation in Libya was 28.5 billion kilowatthours, slightly lower than the 2012 level of 32 billion kilowatthours, which reflects increased oil supply disruptions. Libya’s power plants are fueled entirely by oil and natural gas.

Notes:

- Data presented in the text are the most recent available as of November 19, 2015.

- Data are EIA estimates unless otherwise noted.

Endnotes:

2International Monetary Fund, Libya country report (May 2013), page 22-23.

3International Monetary Fund, “Arab Countries in Transition: Economic Outlook and Key Challenges” (October 9, 2014), page 13; and World Bank Data, GDP Growth, (accessed October 2015).

4Oil & Gas Journal, “Worldwide Look at Reserves and Production,” (January 1, 2015).

5Arab Oil & Gas Directory, www.stratener.com, “Libya,” (2013), page 256.

6Middle East Economic Survey, “Libya: Light at End Of Tunnel As Losses Hit $7.5bn,” (September 20, 2013), Volume 56, Issue 38.

7Arab Oil & Gas Directory, www.stratener.com, “Libya,” (2013), page 257-8.

8U.S. Energy Information Administration based on articles and data from Energy Intelligence, Middle East Economic Survey (MEES), company websites, Oil & Gas Journal, and Lloyd’s List Intelligence (APEX tanker data).

9Eurostat Database (accessed October 2015); Lloyd’s List Intelligence, APEX tanker tracking service, (accessed October 2015, Global Trade Information Services, Customs data from destination countries, (accessed October 2015).

10International Energy Agency, MODS database, Non-OECD oil demand, (accessed October 2015).

11Oil & Gas Journal, “Worldwide Refining,” (January 1, 2015).

12IHS Energy, Annual Long-Term Strategic Workbook, Refining and Product Markets: Africa, (April 2015).

13Oil & Gas Journal, “Worldwide Look at Reserves and Production,” (January 1, 2015).

14EIA data and BP, “Statistical Review of World Energy June 2015.”

15Ibid.

16Energy Intelligence Group, World Gas Intelligence, “Libya Halts Italy Flows,” (October 8, 2014).

17Arab Oil & Gas Directory, www.stratener.com, “Libya,” (2013), page 267-8.

18International Energy Agency, Electricity Access Database, World Energy Outlook, 2014.