Governments Need Agile Fiscal Policies As Food And Fuel Prices Spike – Analysis

By Jean-Marc Fournier, Vitor Gaspar, Paulo Medas and Roberto Perrelli

Just as increasing vaccinations offered hope, Russia’s invasion of Ukraine disrupted the global economic recovery. One of the most visible global effects has been the acceleration of energy and food prices, triggering concerns about episodes of food shortages and increasing the risks of malnutrition and social unrest. World food prices surged by 33.6 percent in March from a year earlier, according to the Food and Agriculture Organization of the United Nations.

Our latest Fiscal Monitor discusses how governments, faced with record debt and rising borrowing costs, can best respond to the urgent needs. It stresses the call for greater global cooperation.

Highly uncertain fiscal outlook

Economies around the world have accumulated layer upon layer of legacies from past shocks since the global financial crisis. Extraordinary fiscal actions in response to the pandemic led to a surge in fiscal deficits and public debt in 2020.

Moreover, the outlook remained uncertain as the world navigated an unprecedented environment, with rising inflation and increasing divergence in recoveries—and then Russia invaded Ukraine, pushing geopolitical risks sharply up.

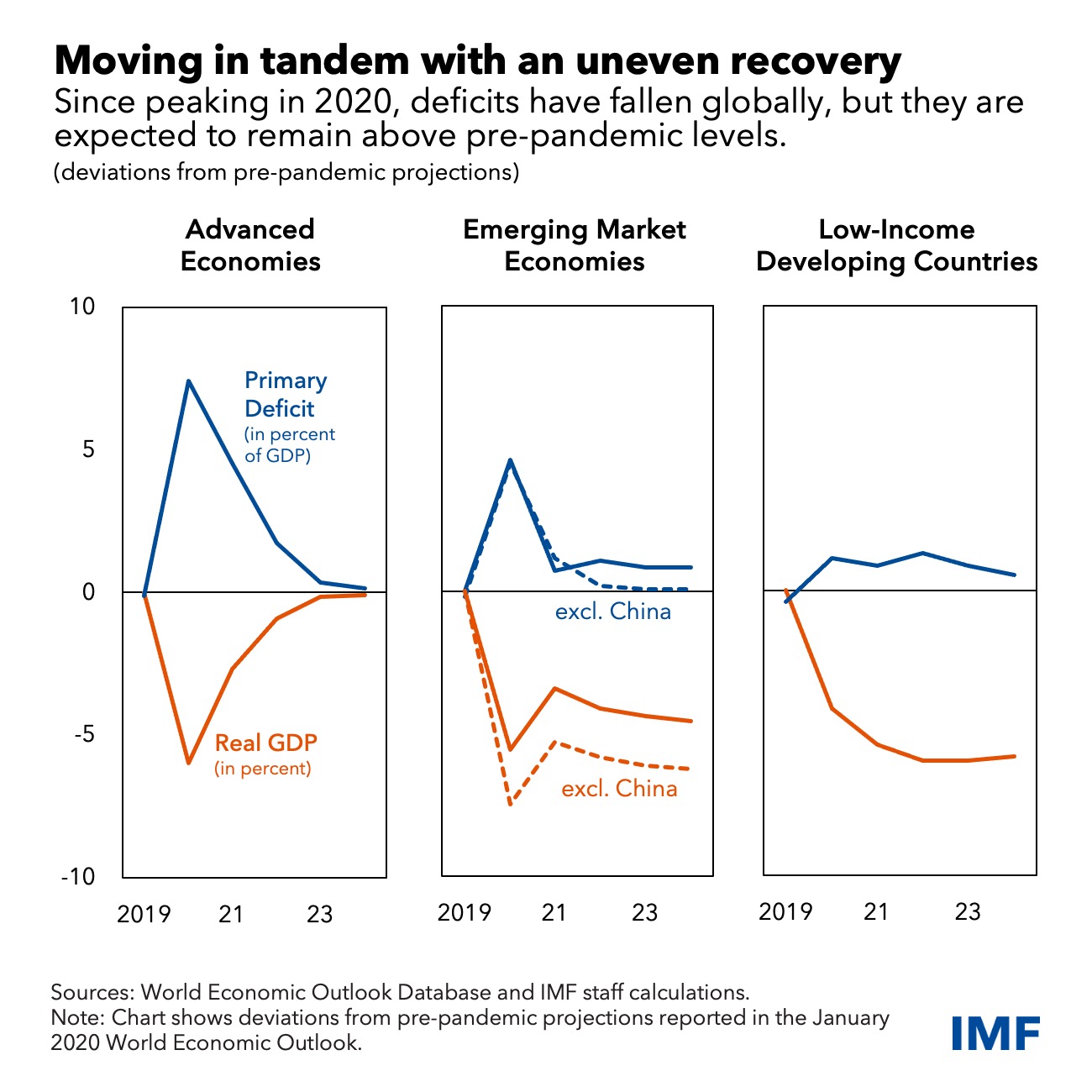

Global deficits and debt are falling from record levels, but the risks around the outlook are exceptionally high and vulnerabilities are rising. Global public debt is expected to fall in 2022 and then stabilize at about 95 percent of gross domestic product over the medium term, 11 percentage points higher than before the pandemic. Large inflation surprises in 2020-21 helped reduce debt ratios, but as monetary policy tightens to curb inflation, sovereign borrowing costs will rise, narrowing the scope for government spending and increasing debt vulnerabilities.

In advanced economies, deficits are projected to decline and policies are shifting from pandemic support to structural transformation. Fiscal outlooks in Europe face exceptional uncertainty given the war in Ukraine and its spillovers. In most emerging markets, deficits will narrow, but with large variations across countries. Low-income countries, already suffering with scarring from the pandemic, have very limited fiscal space as they are hard hit by spillovers from the war.

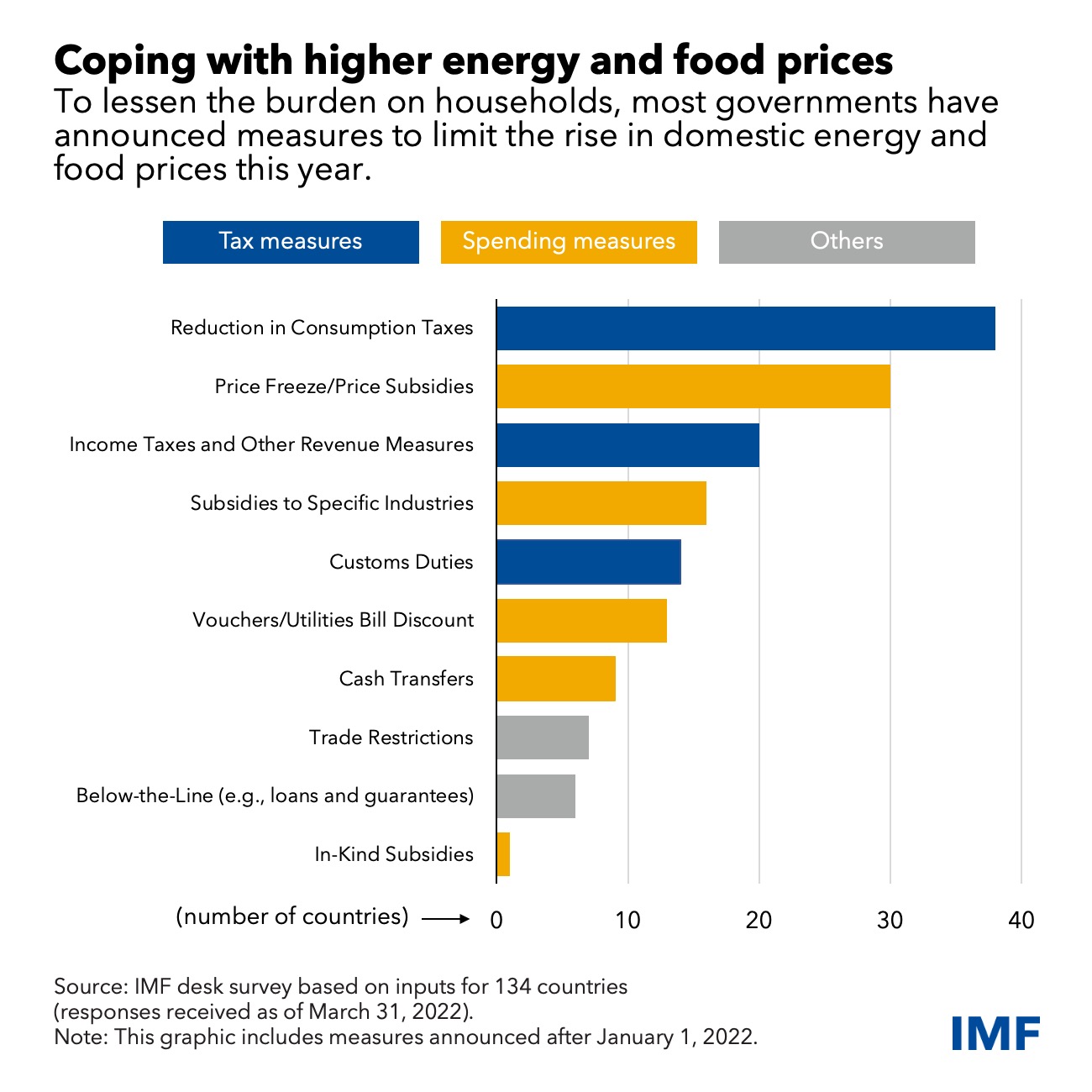

The different shocks have also brought new risks to public finances. Governments are under pressure to deal with the rising energy and food prices. To alleviate the burden on households, ensure food security, and preempt social unrest, most governments have announced measures to limit the rise in domestic prices. However, such actions could have large fiscal costs and exacerbate global demand and supply mismatches, putting further pressure on international prices and possibly leading to energy or food shortages. This would further hurt low-income countries that rely on imported energy and food.

Moreover, the fight against poverty has suffered a setback, especially in emerging markets and low-income countries. Relative to pre-pandemic trends, the COVID-19 crisis pushed 70 million more people worldwide into extreme poverty in 2021. In many advanced economies, households were protected by direct government support or job-retention schemes. Households spent less and saved more because of social distancing, mobility restrictions, and uncertainty about the future. These excess savings are an important buffer but, if spent quickly, they could further add to the inflation momentum. The situation is much more dire in other countries with large numbers of poor people—where rising inflation could push more into poverty and exacerbate the food crisis.

Managing crisis upon crisis

Governments face difficult choices in this highly uncertain environment. They should focus on the most urgent spending needs and raise revenue to pay for them.

We recommend agile fiscal strategies tailored to individual country circumstances:

- In the economies hardest hit by the war in Ukraine and sanctions on Russia, fiscal policy needs to respond to the humanitarian crisis and economic disruptions. Given rising inflation and interest rates, fiscal support should be targeted to those most affected and priority areas.

- In nations where growth is stronger and inflation pressures remain elevated, fiscal policy should continue its shift from support to normalization.

- In many emerging markets and low-income economies facing tight financing conditions or the risk of debt distress, governments will need to prioritize spending and raise revenues to reduce vulnerabilities.

- Commodity exporters that benefit from higher prices should seize the opportunity to rebuild buffers.

Government responses to the surge in international commodity prices should give priority to protecting the most vulnerable. A critical objective is to avoid a food crisis while keeping social cohesion. Countries with well-developed social safety nets could deploy targeted and temporary cash transfers to vulnerable groups while allowing domestic prices to adjust. This will limit budgetary pressures and create the right incentives to increase supply (such as investing in renewable energy). Other countries could allow a more gradual adjustment of domestic prices and use existing tools to help the most vulnerable during this crisis, while taking steps to strengthen safety nets.

Fossil-fuel price hikes further highlight the urgency in accelerating the transition to clean and renewable energy, which would increase energy security and help meet the urgent climate agenda—we are dramatically off-track to limit global warming to 2 degrees Celsius.

About 60 percent of low-income countries are either at high risk of debt distress or already experiencing it. They face persistent scarring from COVID-19. They are especially vulnerable to food price rises, given the large share of food spending in their households’ budgets. These countries need support from the international community.

But the need for collective action is broader. Global cooperation is necessary to tackle pressing and urgent problems that the world is facing: energy and food crises, current and future pandemics, debt, development, and climate change.

*About the authors:

- Jean-Marc Fournier is an economist in the IMF’s Fiscal Policy and Surveillance Division, Fiscal Affairs Department.

- Vitor Gaspar, a Portuguese national, is Director of the IMF’s Fiscal Affairs Department.

- Paulo Medas is Division Chief in the IMF’s Fiscal Affairs Department and oversees the IMF’s Fiscal Monitor.

- Roberto Perrelli is a Senior Economist in the IMF’s Fiscal Policy and Surveillance Division, Fiscal Affairs Department, where he also works on the IMF Fiscal Monitor.

Source: This article was published by IMF Blog