The Aftermath Of Sovereign Debt Crises – Analysis

By VoxEU.org

There is little consensus on the macroeconomic impacts of sovereign debt crises, despite the regularity of such events. This column quantifies the aggregate costs of defaults using a narrative approach on a large panel of 50 sovereigns between 1870 and 2010. It estimates significant and persistent negative effects of debt crises starting at 1.6% of GDP and peaking at 3.3%, before reverting to trend five years later. In addition, underlying causes matter. Defaults driven by aggregate demand shocks result in short-term contractions, whereas aggregate supply shocks lead to larger, more persistent losses.

By Rui Esteves, Seán Kenny and Jason Lennard*

What is the macroeconomic impact of sovereign debt crises? In every year since the mid-1970s, more than 30% of sovereigns have been in default (Beers and Mavalwalla 2017). Despite the scale of the global sovereign debt problem, its consequences are not well understood. Answering this question is important not only retrospectively – to understand the waves of default in history – but also for the present, as the pandemic stretches the fiscal sustainability of developing and emerging economies (Bolton et al. 2020a, 2020b).

Despite the importance of the question, there is little consensus in the literature. The results range from authors who identify sharp and/or persistent recessions after defaults (Reinhart and Rogoff 2009, Furceri and Zdzienicka 2012, Kuvshinov and Zimmermann 2019) to those who find little to no impact (Borensztein and Panizza 2010, Levy-Yeyati and Panizza 2011). Getting the answer right has considerable implications for debtors, creditors, and even for theoretical models of default.

One reason for this uncertainty is that default is not random. Defaults may be both a cause and consequence of economic downturns. If recessions trigger endogenous debt crises, simple estimates of the economic costs of default will be biased upwards, even if defaults had no impact on GDP on their own. Another reason is heterogeneity. Defaults are not created alike, and their economic impact may depend on the underlying causes of debt crises. As a result, the average cost of default may not be a well-defined quantity.

In new research (Esteves et al. 2021), we revisit the aftermath of sovereign debt crises by pooling a large sample of 50 defaulting economies between 1870 and 2010. To address the endogeneity of default, we turn to the narrative approach. The method has been used in other areas of macroeconomics that encounter endogeneity, such as fiscal policy (Romer and Romer 2010, Ramey and Zubairy 2015, Cloyne et al. 2018), monetary policy (Romer and Romer 2004, Cloyne and Hürtgen 2014, Lennard 2018), and banking crises (Jalil 2015, Kenny et al. 2021), but we are the first to employ it in the context of default.

To do so, we read and classify contemporary reports about more than 170 debt episodes. Our sources are creditor organisations and financial newspapers, such as the Economist and Financial Times, whose reputation depended on accurate and unbiased reporting. We use the contemporary opinion to distinguish between endogenous and exogenous debt episodes. In the first category, we include events where the default was the consequence rather than the cause of the economic downturn. We split endogenous factors between domestic aggregate demand and supply shocks. The exogenous category collects cases where the default was precipitated by shocks unrelated to the domestic business cycle of the nation. Exogenous factors include terms of trade shocks, political events, contagion, moratoria granted by creditor nations, and legal events. A recent example of the latter type of default is the 2014 decision by the late US judge Thomas Griesa that forced Argentina into a technical default (Hébert and Schreger 2017).

Why nations default

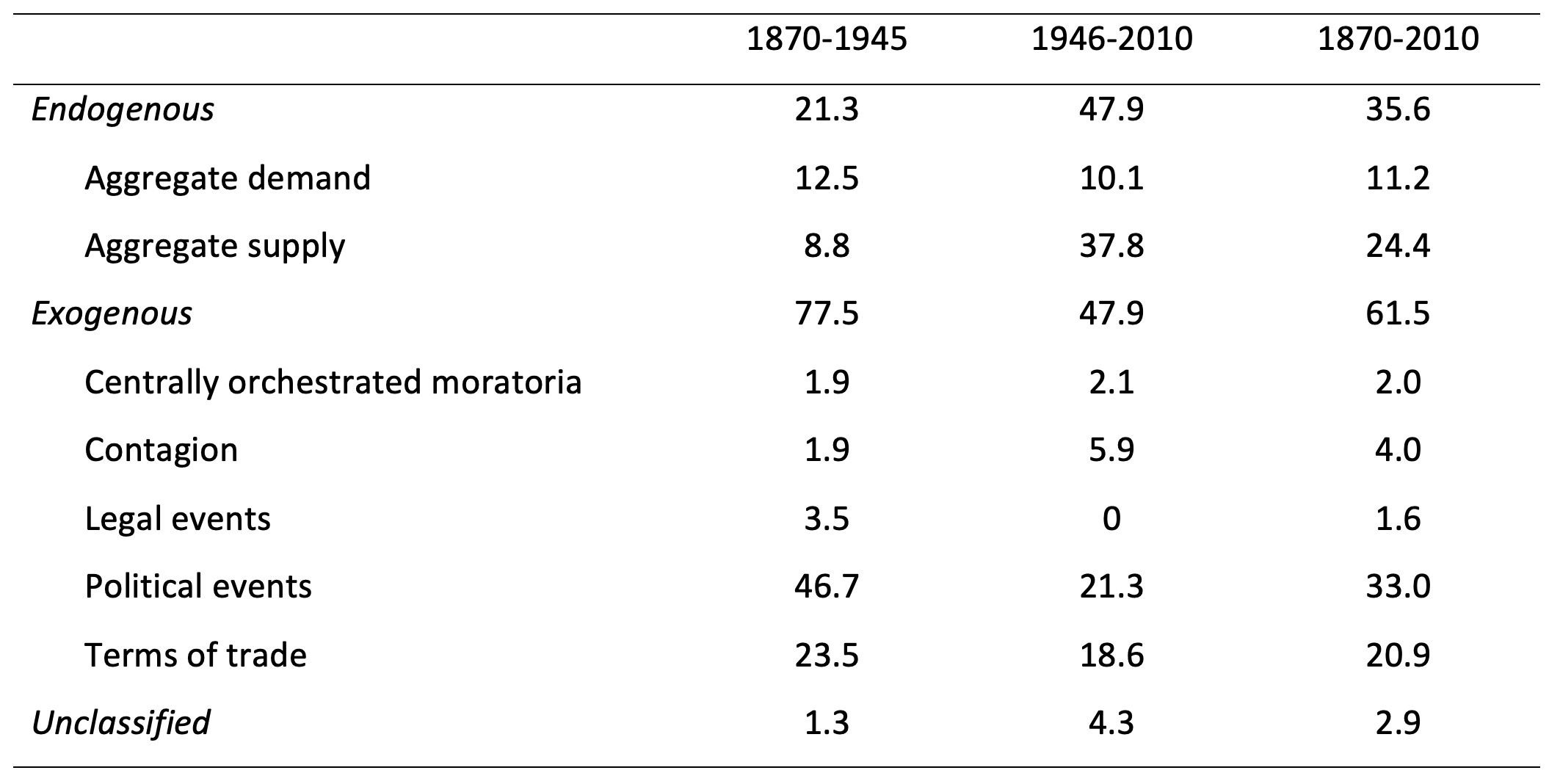

Table 1 breaks down default episodes by the causes identified in our reading of the narrative evidence. Roughly one-third of defaults over the whole period had endogenous causes (especially supply shocks), though that share is much larger in the post-war period. Among the two-thirds of episodes that were exogenous, terms of trade shocks and politics dominate. The prevalence of politics as a cause of default supports models that emphasise political risk (Cuadra and Sapriza 2008).

Table 1 The causes of sovereign debt crises, 1870-2010 (in percentage)

The macroeconomic effects of sovereign debt crises

We estimate the effect of sovereign defaults by panel local projections (Jordà 2005), where we instrument defaults with our classification of exogenous debt episodes (Stock and Watson 2018). As the exogenous defaults are a subset of all defaults, we find that the instrument is highly relevant. Consistent with our identification strategy, the instrument cannot be predicted by lagged macroeconomic observables, such as economic growth or inflation, which is a necessary, if not sufficient, condition of exogeneity.

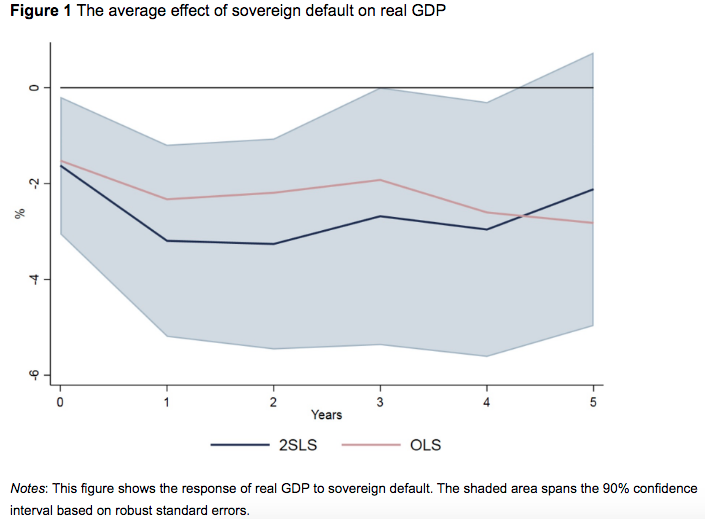

Figure 1 represents the impulse response up to five years after the start of a default. Our results suggest that there is a moderate but statistically significant contraction in economic activity in the aftermath of defaults. Output falls by 1.6% on impact, peaking at -3.3% after two years and reverting to trend by year five. The figure also plots the OLS estimates ignoring the endogeneity of default decisions. Comparing the two sets of estimates, we confirm that there is a bias, but it is quantitatively small, averaging 0.4% of GDP over the five-year horizon.

We also investigate the potential mechanisms for this output contraction. In line with others, we find evidence that defaults harm the traded sector via a current account reversal (Asonuma et al. 2016) and are more disruptive when associated with domestic credit crunches (Kuvshinov and Zimmermann 2019).

All defaults are different

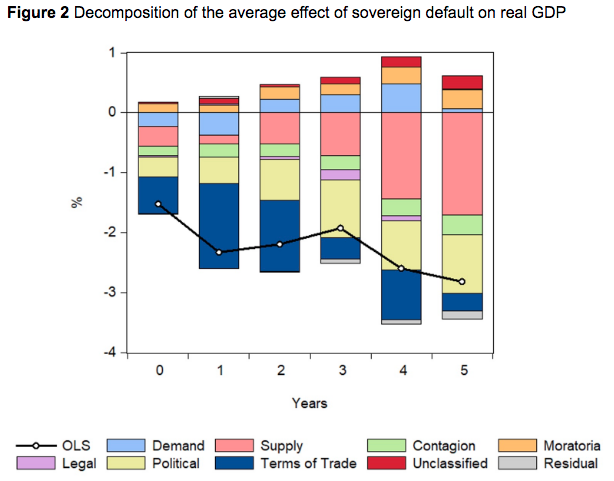

We next explore the potential heterogenous effects of default by the underlying cause. Figure 2 shows a decomposition of the average effect represented in Figure 1, by the seven causes identified in the narrative evidence. In terms of the endogenous crises, defaults sparked by aggregate demand shocks result in short-run contractions, whereas aggregate supply shocks lead to larger, more persistent losses. In terms of exogenous crises, defaults initiated by external trade shocks and politics are especially punishing, though the impact of the former is more frontloaded than the latter. Unsurprisingly, the decomposition supports the expectation that external debt relief (moratoria) organised through creditor countries is expansionary, increasing output by 4.2% on impact and by 9.1% after five years (Reinhart and Trebesch 2016).

But what is a default?

Our results stand in the middle ground of the literature. On the one hand, we reject the puzzling result that defaults are a free lunch, and on the other that defaults are persistent disasters. On average, debt crises leave temporary, not permanent, economic scars. In this sense, default is not destiny. However, within this result hides a large heterogeneity. This has an obvious bearing on policy. Recognising that not all defaults are created alike can potentially improve the targeting of policy intervention ex-post to smooth the impact of, or prevent, spillovers from debt crises. Our results also underscore that heterogeneity is likely to be a greater obstacle to benchmarking the costs of defaults than endogeneity. This could be particularly relevant for theoretical contributions that calibrate the typical costs of defaults from particular episodes.

One final challenge to benchmarking the costs of default has to do with how we date the events. A number of historical chronologies are available in the literature and we find that our estimates are sensitive to which chronology we use. Part of this variation is probably due to different definitions of what constitutes a default (Tomz and Wright 2013). For instance, more restrictive concepts that ignore partial defaults are likely to censor episodes with moderate macro outcomes, biasing the resulting estimates up. But another fraction of the difference is due to timing issues. In our work with narrative sources, we came across a number of instances where the news of default was reported prior to the date recorded in the standard chronologies. As the costs of default are estimated relative to the GDP trend outside of default episodes, getting the start of the episodes wrong is bound to influence the estimation of the whole time profile of GDP after a debt episode. Further research on how to define and date sovereign debt episodes is therefore needed.

*About the authors:

- Rui Esteves, Professor, Graduate Institute, Geneva

- Seán Kenny, Post-doctoral Researcher, Department of Economic History, Lund University

- Jason Lennard, Post-doctoral Researcher, Department of Economic History, LSE

References

Asonuma, T, M Chamon and A Sasahara (2016), “Trade costs of sovereign debt restructurings: Does a market-friendsly approach improve the outcome?”, IMF Working Paper WP/16/222.

Beers, D and J Mavalwalla (2017), “Database of Sovereign Defaults”, Bank of Canada Technical Report No. 101.

Borensztein, E and U Panizza (2010), “Do Sovereign Defaults Hurt Exporters?”, Open Economies Review 21: 393-412.

Bolton, P, L Buchheit, P-O Gourinchas, M Gulati, C-T Hsieh, U Panizza and B Weder di Mauro (2020a), “Necessity is the Mother of invention: How to Implement a Comprehensive Debt Standstill for COVID-19 in Low- and Middle-income Countries”, VoxEU.org, 21 April.

Bolton, P, M Gulati and U Panizza (2020b), “Legal Air Cover”, VoxEU.org, 13 October.

Cloyne, J and P Hürtgen (2014), “Why Monetary Policy Matters: New UK Narrative Evidence”, VoxEU.org, 15 May.

Cloyne, J, N Dimsdale and N Postel-Vinay (2018), “Positive Effects of Fiscal Policy on Economic Growth: New Evidence from the Great Depression in Britain”, VoxEU.org, 2 November.

Cuadra, G and H Sapriza (2008), “Sovereign Default, Interest Rates and Political Uncertainty in Emerging Markets”, Journal of International Economics 76(1): 78-88.

Eichengreen, B, A El-Ganainy, R Esteves and K Mitchener (2019), “Public Debt through the Ages”, VoxEU.org, 1 April.

Esteves, R, S Kenny and J Lennard (2021), “The Aftermath of Sovereign Debt Crises: A Narrative Approach”, CEPR Discussion Paper 16166.

Furceri, D and A Zdzienicka (2012), “How Costly Are Debt Crises?”, Journal of International Money and Finance 31(4): 726-42.

Hébert, B and J Schreger (2017), “The Costs of Sovereign Default: Evidence from Argentina”, American Economic Review 107(10): 3119-45.

Jalil, A (2015), “A New History of Banking Panics in the United States, 1825-1929: Construction and Implications”, American Economic Journal: Macroeconomics 7: 295-330.

Jordà, Ò (2005), “Estimation and Inference of Impulse Responses by Local Projections”, American Economic Review 95(1): 161-82.

Kenny, S, J Lennard and J D Turner (2021), “The Macroeconomic Effects of Banking Crises: Evidence from the United Kingdom, 1750-1938”, Explorations in Economic History 79.

Kuvshinov, D and K Zimmermann (2019), “Sovereigns Going Bust: Estimating the Cost of Default”, European Economic Review 119: 1-21.

Lennard, J (2018), “Did Monetary Policy Matter? Narrative Evidence from the Classical Gold Standard”, Explorations in Economic History 68: 16-36.

Levy-Yeyati, E and U Panizza (2011), “The Elusive Costs of Sovereign Defaults”, Journal of Development Economics 94(1): 95-105.

Ramey, V and S Zubairy (2015), “Government Spending Multipliers in Good times and in Bad: Evidence from US Historical Data”, VoxEU.org, 23 January.

Reinhart, C M and K S Rogoff (2009), This Time is Different: Eight Centuries of Financial Folly, Princeton: Princeton University Press.

Reinhart, C M and C Trebesch (2016), “Sovereign Debt Relief and its Aftermath”, Journal of the European Economic Association 14(1): 215-51.

Romer, C D and D H Romer (2004), “A New Measure of Monetary Shocks: Derivation and Implications”, American Economic Review 94: 1055-84.

Romer, C D and D H Romer (2010), “The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks”, American Economic Review 100(3): 763-801.

Stock, J H and M W Watson (2018), “Identification and Estimation of Dynamic Causal Effects in Macroeconomic Using External Instruments”, Economic Journal 128(610): 917-48.

Tomz, M and M L J Wright (2013), “Empirical Research on Sovereign Debt and Default”, Annual Review of Economics 5: 247-72.