Growing Concentration Of Wealth In Italy: Evidence From New Source Of Data – Analysis

By VoxEU.org

Growing wealth disparities can have corrosive effects on equality of opportunity when they crystallise over time and turn into persistent disparities across generations. This column uses newly assembled data from Italian inheritance tax records to show that the wealth share of the top 1% (half a million individuals) increased from 16% in 1995 to 22% in 2016, and the share accruing to the top 0.01% (the richest 5,000 adults) almost tripled from 1.8% to 5%. In contrast, the poorest 50% saw an 80% drop in their average net wealth over the same period. The data also reveal the growing role of inheritance and gifts inter vivos as a share of national income, as well as their increasing concentration at the top.

By Paolo Acciari, Facundo Alvaredo and Salvatore Morelli*

Over the past months, due to mounting financing needs raised by the Covid-19 pandemic crisis, many have been debating and calling for policies to curb growing extreme inequalities, including new taxes on personal wealth ( Scheuer 2020, Landais et al. 2020, Bastani and Waldenström 2020, and Bonnet et al. 2021). Yet, despite the growing policy interest, knowledge about the size distribution of wealth is currently limited.

New data for Italy

In a new paper (Acciari et al. 2021), we make use of newly assembled microdata on the inheritance tax records in Italy, a country with one of the highest wealth-to-income ratios in the developed world. The use of inheritance tax data increases the probability of better covering high-end wealth groups, despite the existence of tax avoidance and evasion behaviours. The data, between 1995 and 2016, cover up to 63% of the deceased. This is the result of the combination of the very high homeownership rate with a key administrative feature of the tax, which is strictly connected to the upkeep of the cadastral (real estate) register: all inheritances involving the transfer of real estate property are obliged to file a return, also when no tax is due (and even when the inheritance tax was abolished between 2001 and 2006).

Adjustments

Several adjustments are applied to the data. First, real estate cadastral values have to be brought in line with market prices. Second, the distribution of decedents needs to be reshaped into the distribution of identified living wealth holders through the application of the mortality multiplier method (i.e. multiplying the number of decedents and their wealth by the inverse of the mortality rate). Third, allowance must be made for the wealth of the unidentified population in the tax data. Fourth, imputations are needed to account for tax exempted assets, and for differences in valuation, and tax evasion.

The benchmark approach adopted in our study is to distribute the full balance sheet of the household sector from the National Accounts (along the lines of the Distributional National Accounts framework developed in Alvaredo et al. 2016, 2020). This is based not on the assumption that the balance sheet gives the correct numbers, but that they provide a reasonable indicator (enshrined in official statistics) of the development of aggregates over time, as well as offer the possibility of better cross-country comparison.

Main results

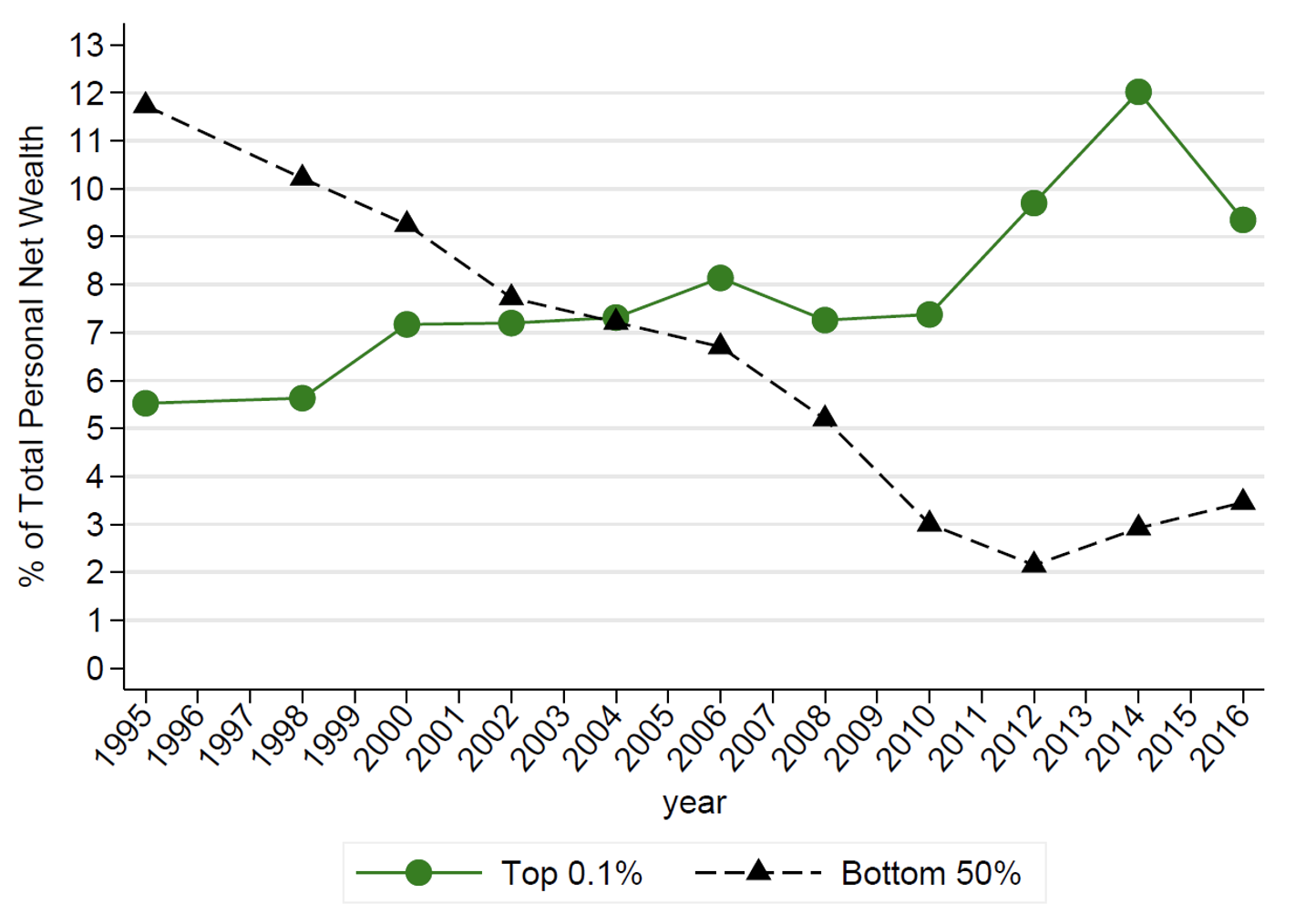

Our estimates suggest that the wealth share of the top 1% (half a million individuals) increased from 16% in 1995 to 22% in 2016; the share accruing to the top 0.01% (the richest 5,000 adults) almost tripled, increasing from 1.8% to 5%. Figure 1 shows a stark inversion of fortunes since 1995. The richest 0.1% saw a two-fold increase in their real average net wealth (from €7.6 million to €15.8 million at 2016 prices), making its share double from 5.5% to 9.3%. In contrast, the poorest 50% controlled 11.7% of total wealth in 1995, and 3.5% recently; this corresponds to an 80% drop in their average net wealth (from €27,000 to €7,000 at 2016 prices). In 1995, the share of the middle 40% was very similar to that of the top 10%, but it declined over time by almost 5 percentage points instead.

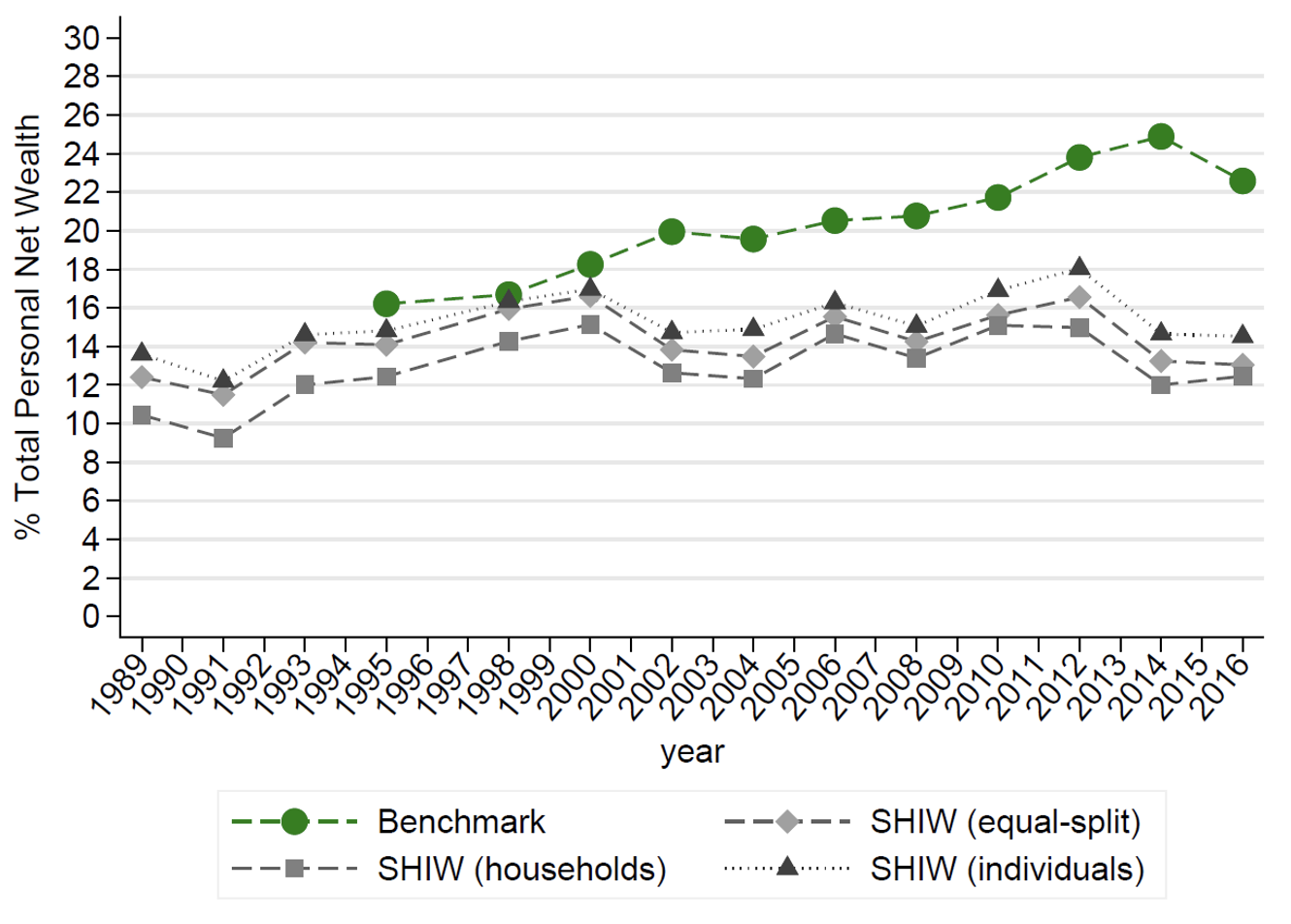

The picture would be rather different had one look at similar estimates from household survey data. According to the SHIW, the share accruing to the top 1% of has remained roughly unchanged between 1995 and 2016, at around 14% (in line with existing works such as Brandolini et al. 2004 and Cannari and D’Alessio 2018a). This is also true once the survey-based calculations reflect the same unit of observation and similar wealth definition employed in tax-based data.

Figure 1 The inversion of fortunes between 1995 and 2016

Figure 2 Top 1% share: Comparing results with household survey data

A multi-series approach

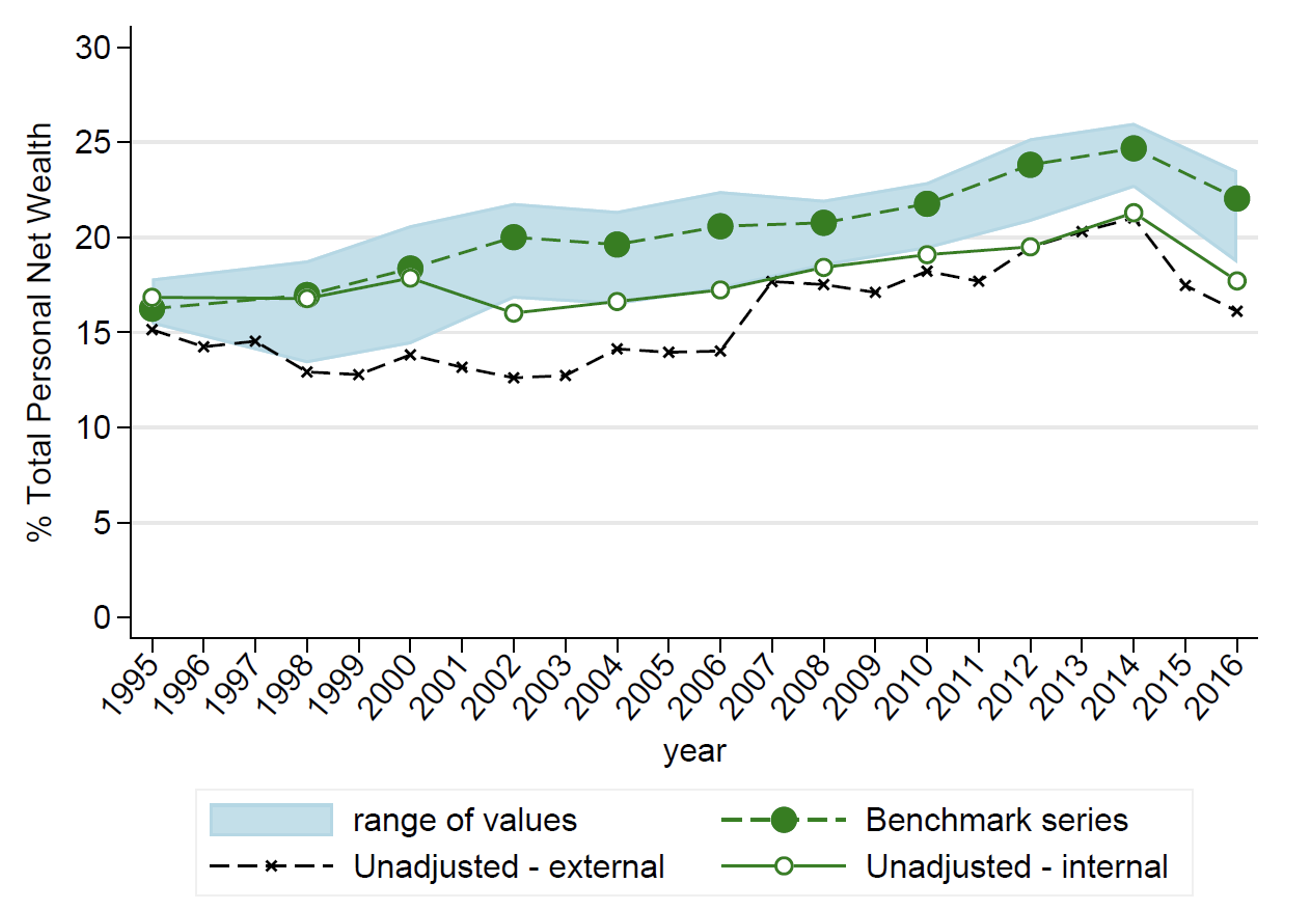

The production of our benchmark series involves a number of controversial imputation decisions, and this led us to produce series based on alternative choices. Given the current imperfect state of data on the distribution of assets and liabilities, presenting the benchmark series in the context of a wider range is preferable to the alternative option of looking at one series resulting from a single source, or from a particular combination of sources. Such a multi-source approach is also crucial to compare our estimates to existing historical series that are not up-scaled to the NA (Kopczuk and Saez 2004, Gabbuti and Morelli 2020, Piketty et al. 2006, Alvaredo and Saez 2009, Alvaredo et al. 2018, Roine and Waldenström 2015).

First, we produce series based on inheritance tax data alone before any imputations, as is done in the ’classic’ estate multiplier method.

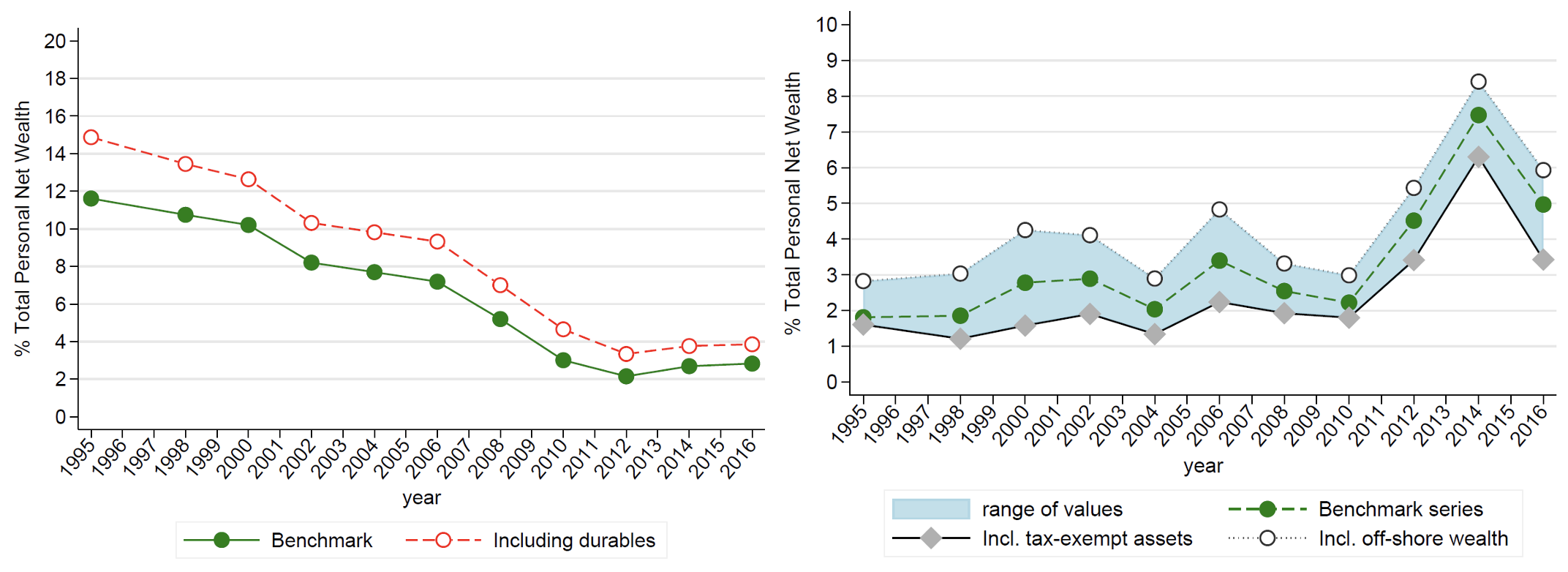

Second, some assets are missing from the official National Accounts records despite their relevance for households, such as vehicles and other durable goods (accounting for approximately 8% of total wealth identified in the 2016 SHIW data) as well as financial assets stashed in off-shore accounts (which, following literature, we estimate to be worth around 2% of personal wealth throughout the period). The imputation of such assets introduces further uncertainty, but it does not appear to affect the trend of the wealth concentration. Nevertheless, whereas the inclusion of durables has stronger effects on the bottom parts of the distribution, the inclusion of unreported offshore wealth mostly changes the distribution above the top 1%.

Figure 3 Top 1% without imputations

Figure 4 Wealth shares imputing durables and unreported off-shore financial wealth

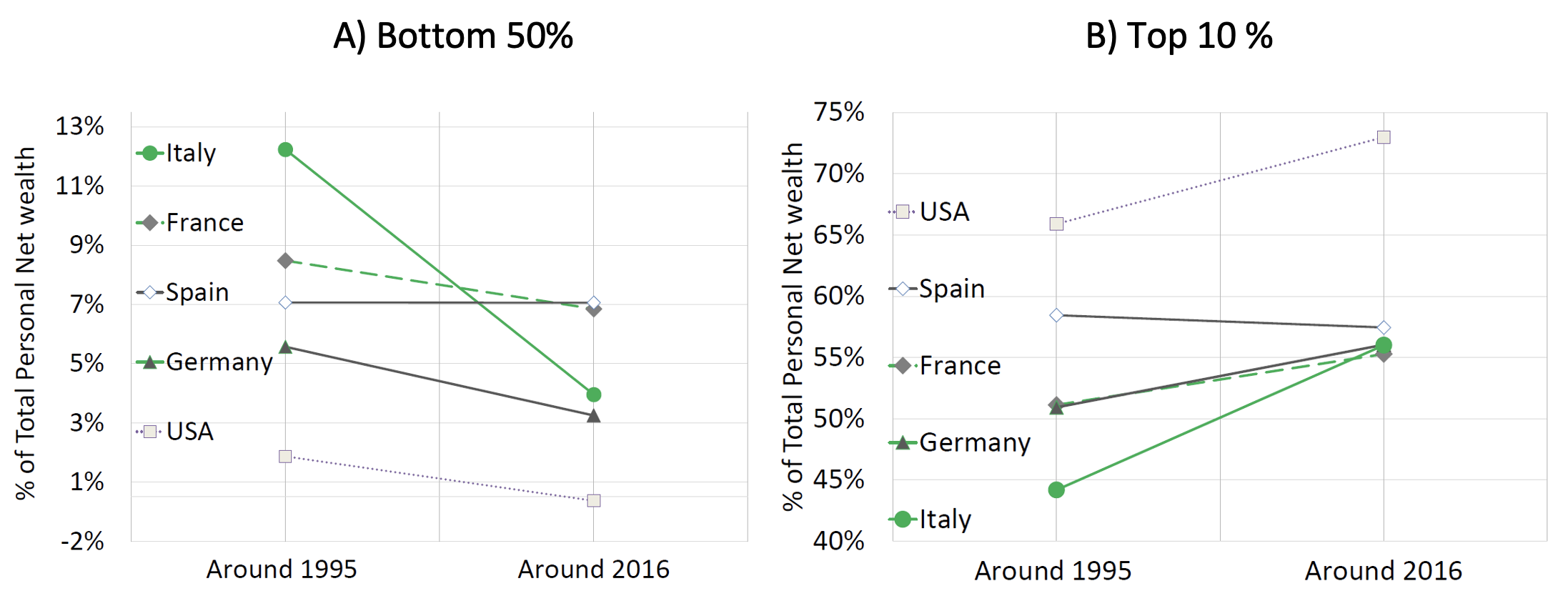

The level of wealth concentration observed in Italy appears to be in line with other European countries such as France, Spain, and Germany (Albers et al. 2020, Garbinti et al. 2016, Martínez-Toledano 2017). However, its time evolution is closer to that found in the US (Saez and Zucman 2016, Batty et al. 2019). By contrast, whereas the Italian middle 40% share remains relatively high, the share of the bottom 50% (composed of approximately 25 million individuals) experienced the strongest decline since the mid-1990s when compared to other countries. Our series are triangulated with external evidence from the global Forbes rich list. Using Forbes, we can track the evolution of the share of the five richest individuals since 1988 and the picture is broadly consistent with the benchmark evidence.

Figure 5 Wealth concentration: A cross-country comparison

Figure 6 Top 0.01% share of wealth vs richest five individuals in Forbes rich list

The potential determinants of wealth concentration

Identifying the channels affecting the evolution of wealth inequality is a fundamental question that has important implications for policy and has been attracting a considerable amount of attention (Khun et al. 2018, Poschke and Kaymak 2016)

In attempting to discern the potential determinants of wealth inequality trends, our paper makes additional contributions to the literature. Our estimates suggest that although average wealth grows with age, the dispersion of wealth within each age (and gender) group is not too dissimilar from that in the overall population. Moreover, we also provide new evidence that asset portfolios are highly heterogeneous across the distribution. Wealthy Italians hold the greatest portion of their portfolios in financial and business assets, adults between the median and 90th percentiles, in the form of real estate (mostly housing), whereas poorer adults hold the biggest share of gross wealth in current and saving accounts, valuables, and they also hold an important share of debt. In line with these findings, we show that the wealth shares of all groups above the 90th percentile are mostly driven by the dynamics of non-housing assets.

Figure 7 The composition of wealth across the wealth distribution

Figure 8 The contribution of housing and non-housing wealth the the growing concentration

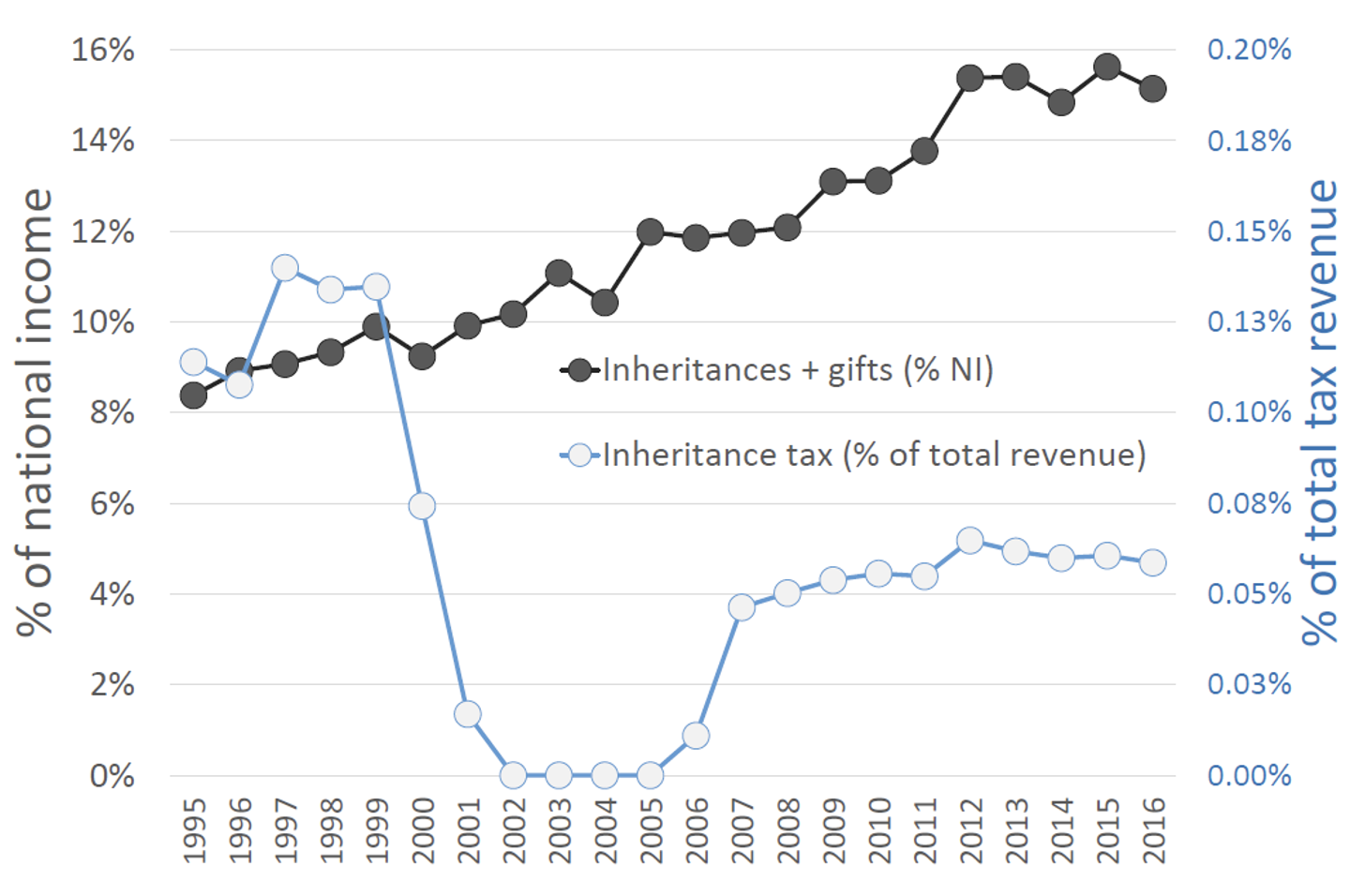

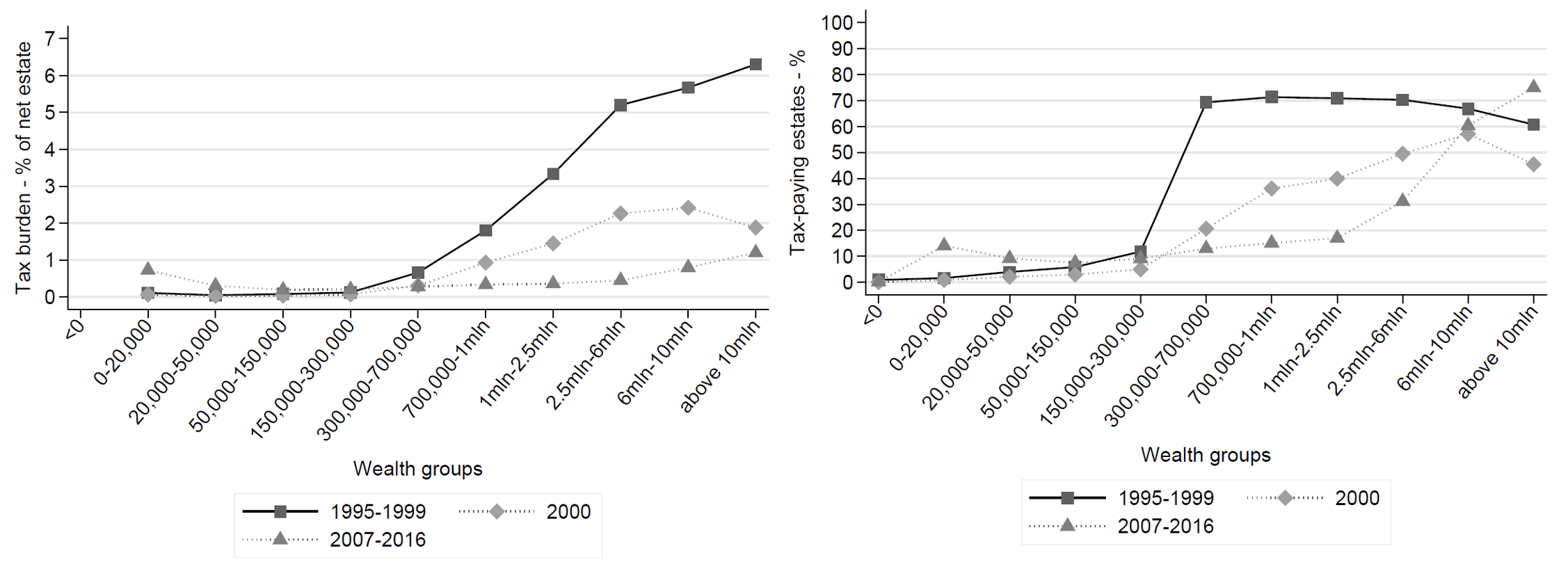

Lastly, we provide new evidence on the growing role of inheritance and gifts inter vivos as a share of national income, as well as their increasing concentration at the top (the value of the estates is adjusted to allow for underreporting of assets as well as for the missing wealth of non-filers). Associated to these trends, we estimate that wealthy inheritors were subject to an overall decreasing tax burden over the past 20 years. On the one hand, a lower proportion of inheritances generated by large bequests are subject to taxation today with respect to mid 1990s. On the other hand, the average tax burden of large bequests has also shrunk substantially over the same period of time, undermining the progressivity of the inheritance and gift tax (see also Boserup et al. 2016 and Nolan et al. 2020).

Figure 9 Inheritance and gifts as a percentage of national income vs inheritance tax collection as a percentage of total tax revenue

Figure 10 The decline of the tax burden on the wealthy

Concluding remarks and policy implications

Improving our knowledge of the size distribution of wealth and its determinants is a realistic goal with important implications for policy intervention. Growing wealth disparities can have corrosive effects on equality of opportunity when they crystallise over time and turn into persistent disparities across generations. Available, comparable cross-country measures suggest that Italy is one of the countries where an offspring’s socioeconomic status is most dependent on that of their parents, implying low intergenerational mobility across generations (Acciari et al. 2019, Bloise 2018, Cannari and D’Alessio 2018b, Corak 2013).

Although our paper expands the available windows of observation on the Italian wealth pyramid, many data limitations remain. It is imperative to invest more on the production of statistics on the wealth holdings of both the low end and the high end of the wealth distribution.

A detailed census on real and financial assets would be an excellent source for estimating the distribution of wealth holdings – a real estate registry already exists in the form of the cadastre (although the actual cadastral values of real estate need updating to be brought in line with market valuations). An accessible and comprehensive registry of financial assets will likely become a concrete reality, given that since 2011 financial institutions are obliged to share data concerning financial wealth holdings of their individual customers with the tax agency. A renovated survey on household wealth holdings would also prove to be a valuable source (e.g. by pre-filling some of the questions using information from asset registries and by using a new sampling design that over-samples wealthy households). Such investments in official statistics are necessary to obtain better information on both the individuals with large fortunes and the poorer segments of the wealth distribution in order to gain a more complete view on financial vulnerability and insecurity of households. The recent COVID-19 pandemic has highlighted the importance of available personal liquid assets to accommodate large and widespread income shocks for a sustained period of time.

*About the authors:

- Paolo Acciari, Head of Unit, Italian Ministry of Economy and Finance

- Facundo Alvaredo, PSE; INET@Oxford; IIEP-UBA-Conicet; Research Fellow, CEPR

- Salvatore Morelli, Assistant Professor of Public Economics, University of Roma Tre

References

Acciari, P, A Polo, and G L Violante (2019), “‘And Yet it Moves’: Intergenerational Mobility in Italy”, NBER Working Paper 25732..

Acciari, P, F Alvaredo, and S Morelli (2021), “The Concentration of Personal Wealth in Italy: 1995-2016”, CEPR Discussion Paper 16053.

Albers, T N H, C Bartels, and M Schularick (2020), “The Distribution of Wealth in Germany, 1895-2018”, ECONtribute Policy Brief No. 001.

Alvaredo, F and E Saez (2009), “Income and Wealth Concentration in Spain From a Historical and Fiscal Perspective”, Journal of the European Economic Association 7(5): 1140-1167.

Alvaredo, F, A B Atkinson, L Chancel, T Piketty, E Saez, and G Zucman (2016), “Distributional National Accounts ( DINA ) Guidelines: Concepts and Methods used in WID.world”, WID.world Working Paper Series N 2016/1.

Alvaredo, F, A B Atkinson, and S Morelli (2018), “Top Wealth Shares in the UK Over More than a Century”, Journal of Public Economics 162(March): 26-47.

Alvaredo, F, A B Atkinson, T Blanchet et al. (2020) “Distributional National Accounts ( DINA ) Guidelines: Concepts and Methods Used in World Inequality Database”, WID.world working document.

Bastani, S and D Waldenström (2020), “Capital taxation: A survey of the evidence”, VoxEU.org, 9 November.

Batty, M, J Bricker, J Briggs et al. (2019), “Introducing the Distributional Financial Accounts of the United States”, Finance and Economics Discussion Series – Board of Governors of the Federal Reserve System 2019-017.

Bloise, F (2018), “The Poor Stay Poor, the Rich Get Rich: Wealth Mobility Across Two Generations in Italy”, CIRET Working Paper 4.

Bonnet, O, G Chapelle, A Trannoy and E Wasmer (2021), “Land is back – it should be taxed, it can be taxed”, VoxEU.org, 16 March.

Boserup, S, W Kopczuk, and C T Kreiner (2016), “Bequests and wealth inequality: Evidence from Denmark”, VoxEU.org, 11 March.

Brandolini, A, L Cannari, G D’Alessio, and I Faiella (2004), “Household Wealth Distribution in Italy in the 1990s”, Temi di discussione del Servizio Studi – Banca D’Italia 530.

Brandolini, A, L Cannari, G D’Alessio, and I Faiella (2018), “Inequality Amid Income Stagnation: Italy Over the Last Quarter of a Century”, Questioni di Economia e Finanza – Occasional papers – Banca d’Italia 442.

Cannari, L and G D’Alessio (2018a), “Wealth Inequality in Italy: A Reconstruction of 1968-75 Data and a Comparison with Recent Estimates”, Questioni di Economia e Finanza – Occasional papers – Banca d’Italia 428, Banca d’Italia.

Cannari, L and G D’Alessio (2018b), “Education, Income and Wealth: Persistence Across Generations in Italy”, Questioni di Economia e Finanza – Occasional papers – Banca d’Italia 476.

Corak, M (2013), “Income Inequality, Equality of Opportunity, and Intergenerational Mobility”, Journal of Economic Perspectives 27(3): 79-102.

Gabbuti, G and S Morelli (2020), “Inheritances, Wealth Concentration and Regional Divides in Italy during the First Globalisation”, unpublished manuscript.

Garbinti, B, J Goupille-lebret, and T Piketty (2016), “Accounting for Wealth Inequality Dynamics : Methods , Estimates and Simulations for France ( 1800-2014 )”, WID.world Working Paper Series N 2016/5.

Kopczuk, W and E Saez (2004), “Top Wealth Shares in the United States, 1916-2000: Evidence from Estate Tax Returns”, National Tax Journal LVII(2): 445-486.

Kuhn, M, M Schularick and U Steins (2018), “Asset prices and wealth inequality”, VoxEU.org, 9 August.

Landais, C, E Saez, and G Zucman (2020), “A progressive European wealth tax to fund the European COVID response”, VoxEU.org, 3 April.

Martínez-Toledano, C (2017), “Housing Bubbles , Offshore Assets and Wealth Inequality in Spain”, WID.world Working Paper Series N 2017/19.

Nolan, B, J C Palomino, P Van Kerm, and S Morelli (2020), “The intergenerational transmission of wealth in rich countries”, VoxEU.org, 19 September.

Piketty, T, G Postel-Vinay, and J-L Rosenthal (2006), “Wealth concentration in a developing economy: Paris and france, 1807-1994”, The American Economic Review 96(1): 236-256,.

Poschke, M and B Kaymak (2016), “US wealth inequality: Quantifying the driving factors”, VoxEU.org, 17 April.

Roine, J and D Waldenstrom (2015), “Long-Run Trends in the Distribution of Income and Wealth”, in Handbook of Income Distribution, Volume 2, Elsevier.

Saez, E and G Zucman (2016), “Wealth Inequality in the United States Since 1913: Evidence From Capitalized Income Tax Data”, Quarterly Journal of Economics.

Scheuer, F (2020), “Taxing the Superrich”, UBS Center.

Mattew Smith, M, O Zidar, and E Zwick (2019), “Top Wealth in the United States: New Estimates and Implications for Taxing the Rich”, unpublished manuscript.