In Eurasia New Financial Centers Are In Offing: Is Shanghai Ready For Prime-Time? – OpEd

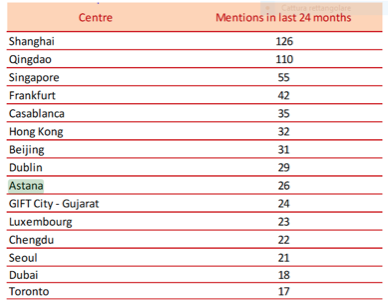

The Global Financial Centers Index (March 2018) shows the steady performance of the top five financial centers over time, including London, New York, Hong Kong, Singapore, and Tokyo, remain at the top the pyramid. In an interesting question solicited to respondents over which centers they estimated to become more significant in the next few years, five of the top seven centers are Asian, and ten of the 15 centers have their place in Eurasia (Table 1).

Even more remarkable than the number is the extent to which the new centers appear flourishing from East Asia to the center of Europe in a rather singular synchrony.

At the bottom there are two developments contributing to the new wave of financial centers. For one, the shift of the center of gravity of global financial markets from North America and Europe to Asia plays as a major factors at propelling old a new financial hubs. Sited in large, continent size-economies, old and new centers, from Shanghai, Beijing, Mumbai to Astana are fed by their own financial markets (Figure 2), and play as attractor factor of capital inflows.

In the current turbulent environment, instigated by the US Administration, China has shown resilience to swings in global risk sentiment has been an important factor supporting broader flows to emerging markets. According to the Institute of International Finance (June 2018), “China saw more than $21 billion of net inflows in April, bringing total inflows to over$53 billion this year. This reflects both stricter enforcement of capital controls and improved investor appetite against the backdrop of declining corporate sector indebtedness in China”.

The departure of the United Kingdom from the European Union is the second most relevant factor. The relocation of finance activities in Mainland Europe, and the re-emergence of old and new centers from Frankfurt, to Paris, Amsterdam, and Milan are likely to strengthening the single currency, and completing the European Banking Union, and capital markets integration.

The re-emergence financial centers, Frankfurt, Paris, Amsterdam, to Shanghai, Mumbai, Astana, and the creation of new, bold competitors reveal a renewed interest in the role of finance. The devastation of the crisis has increased governments’ attention to the damage that an unfettered finance inflict to domestic economy, and the downsides involved in being subject to highly concentrated, self- financial centers. Not only, as Elliott wrote, can “liquidity occasionally move rapidly if a significant factor changes suddenly”. Arnaud ET Alii (2012) warn that the size of a country’s financial sector compared to the size of domestic economy should not near the threshold at around 80-100, and if it continues to rise above, finance starts having a negative effect on economic growth.

By propelling national financial centers to attract financial flows, governments in Asia and Europe aim at counterbalancing anemic economic growth in the manufacturing sector with large scale infrastructure investments.

A large and vigorous economic hinterland, and continent-size prudential regulatory jurisdictions are the indispensable background of the new financial centers in Asia, and Europe. The great strength of New York vis-à-vis London is, according to Elliott, “its vast hinterland (…) that even if its global competitiveness temporarily slips, it will be able to maintain a very large volume of business, and the people and institutions it supports, based purely on the American business. This would make it easier to overcome temporary bumps in the road” (2011).

For covering several features of the New-York ‘s model Shanghai casts the Asian prototype of a financial center well rooted in a large and sovereign economy. China’s announcement of easing the access to domestic market through raising ownership limits is arousing great interest among investors eager to gain a greater share of the world’s second largest economy. In the program, for sure, there are provisions for joint venture requirements and ownership caps in a broad range of industries to protect domestic groups from competition and induce sharing of foreign technology and management of expertise with local partners.

These measures could appear merely symbolic , until Chinese policymakers engage more deeply in the financial sector, and first of all, address once and for all the exhausting story of the RMB foreign exchange policy. Letting the RMB, the People’s currency, freely available to market participants is the unavoidable premise to genuine opening to foreign financial services.

As a matter of fact, China’s unique achievements in the manufacturing sector, the dependence on credit banking, being more sensitive to business cycle than services and finance, have fueled serious unbalances in the economy. So, giving center stage to financial deepening, and picking Shanghai to qualify among the global financial centers by 2020 make sense in China’s supply-side reforms aimed at rebalancing the economy to services, and, furthering the internationalization of the RMB. An additional, and strategic objective for Shanghai is to become an investment and financing center of the Belt and Road Initiative, providing the Belt and Road Initiative financially, and developing into a global financial service center with a focus on renminbi-denominated financial products.

Indeed, Shanghai, and other centers in Eurasia, including Paris or Frankfurt share several features with New York rather than London. Contrasting the two models may help to grasp the evolving features of the new financial centers in Eurasia. UK withdrawal from the EU offers evidence of the inbuilt vulnerabilities of a “global model” that typically defines the City of London. Giving up the large European economic hinterland, the relatively smaller size of UK’s economy vis-a-vis its financial sector fatally affects the financial sector too.

Wrapping Up

The recent financial crisis has urged a critical lesson on the Western finance, especially in financial services. Crisis management within and across jurisdictions is taking a more “Bayesian approach” that primes policymakers in home/continental jurisdictions to be more interventionist, and reduce room to global regulatory entities.

Balancing the global reach and scope finance, and anchoring it to hinterland’s real economy, policymakers are better prepared to supervision financial stability. Indeed, these developments signal a de-concentration of the global finance, and open to finance’s decentralization, where large continent-size jurisdictions take place at the expense of global, nation-state based entities.

- Being more global doesn’t guarantee a financial hub to retain lasting supremacy.

- Even for finance, a naturally foot-loose industry, a strong and large hinterland is critical to the survival of Financial Hubs.

- The risk of a global financial center, like London, is to become an offshore center, relatively more vulnerable to policy made elsewhere, particularly by the Eurozone (Wolf 2016).

- Continent-size jurisdiction and the new financial centers tell that in finance, size does matter too.

*Miriam L. Campanella, University of Turin, Senior Fellow ECIPE, Brussels

Notes:

1. References in this article can be found in The Changing Geography of Finance.Shifting Financial Flows, and the … https://papers.ssrn.com/abstract=3202644 –

2. The Global Financial Centres Index 23 – Long Finance www.longfinance.net/Publications/GFCI23.pdf

3. IIF Capital Flows Tracker Looking Through the … – Breakingviews

4. Alicia Garcia-Herrero (2018) The World and Asia in 2018. Natixis.

5. A case in point is the current controversy between EU and UK. Rejecting the provisions included in the Brexit whitepaper Barnier emphasized the “system of generalized equivalence”, proposed by May’s government would in reality be jointly run by the EU and UK. A situation incompatible to the EU jurisdictional independence.