US GDP Growth Slows To 2.1 Percent In Second Quarter Due To Investment Slump – Analysis

By Dean Baker

The Gross Domestic Product (GDP) grew at a 2.1 percent annual rate in the second quarter. A drop in both residential and nonresidential investment was the biggest factor in slowing growth. The 0.6 percent drop in nonresidential investment was the first decline in this category since the first quarter of 2016.

Consumption was the most important factor in growth in the quarter, growing at a 4.3 percent annual rate, which added 2.85 percentage points to the quarter’s growth. Durable goods, driven by strong car sales, grew at a 12.9 percent rate and added 0.86 percentage points to the quarter’s growth.

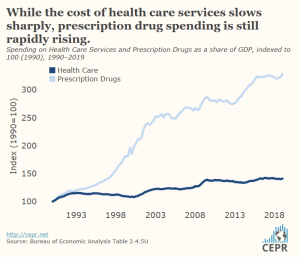

It is worth noting in this area that spending on health care services, which accounts for the overwhelming majority of national health care spending, has been relatively restrained over the last decade, increasing largely at the same pace as overall GDP. There appears to have been a modest acceleration in the last year, with nominal spending up 4.9 percent over the last year, with nominal GDP rising by just 4.0 percent. The story of prescription drugs is much less encouraging. Spending in this area continues to far outpace GDP. It has risen by 7.5 percent over the last year.

The drop in nonresidential investment was driven by a 10.6 percent decline in investment in structures, ironically the category of investment that should have received the largest boost from the tax cut; it is now down by 4.6 percent from its year ago level. Equipment investment rose by just 0.7 percent after a 0.1 percent fall in the first quarter. The pace of investment in intellectual products also slowed sharply, rising 4.7 percent in the second quarter, after double-digit increases the prior two quarters.

Residential investment fell 1.5 percent, its sixth consecutive quarterly decline. Lower mortgage rates should put an end to this drop in the next two quarters.

Inventory growth slowed in the quarter, which subtracted 0.86 percentage points from the quarter’s growth. This is after a big jump in the first quarter, which added 0.53 percentage points to growth. Trade was also a large drag on growth in the quarter, as exports fell at a 5.2 percent annual rate. A high dollar and tariffs also slowed the growth in imports to a 0.1 percent rate, after a 1.5 percent drop in the first quarter. On net, trade subtracted 0.65 percentage points from second-quarter growth.

The government sector added 0.85 percentage points to the quarter’s growth, driven largely by a 15.9 percent jump in nondefense federal spending. This is primarily an artifact of timing as the shutdown led to reported declines of 4.5 and 5.4 percent in the last two quarters.

There continues to be no evidence of inflationary pressure in this report. The core consumer expenditure deflator rose at just a 1.8 percent annual rate in the quarter and is up by just 1.5 percent over the last year.

This report includes revisions to the prior three years’ data. The revised data show GDP growth was substantially slower for 2018 than previously reported, with the growth from the fourth quarter of 2017 to the fourth quarter of 2018 at just 2.5 percent, well below the administration’s projection at the time of the tax cut.

Profits for 2018 were also revised downward. The new data show that the before-tax profit share of net corporate income fell by 0.4 percentage points in 2018. It is now down by 3.2 percentage points from the peak hit in 2014. This suggests that the tighter labor market is enabling workers to regain income shares lost in the Great Recession.

Another item worth noting is that the savings rate has been revised upward. It is now reported at 7.7 percent for 2018 and an average of 8.3 percent in the first half of 2019. This is far above the levels reported for 2010 and 2011 when the large number of underwater homeowners was supposedly depressing consumption.

This report provides evidence that the economy is slowing with no realistic concerns about accelerating inflation. On the downside, the tax cut has clearly not led to the predicted investment boom. On the plus side, the Fed has little reason to worry a rate cut will be inflationary.