US GDP Shows Healthy Growth In Third Quarter, Driven By A Shrinking Trade Deficit – Analysis

By Dean Baker

Most of the drop in the saving rate is due to capital gains taxes, not people spending their savings

The economy grew 2.6 percent in the third quarter, a sharp turnaround from two quarters of negative growth in the first half of the year. A shrinking trade deficit was the biggest factor, adding 2.77 percentage points to the quarter’s growth. This was more than enough to offset a sharp decline in residential construction and slowing inventory accumulation, which subtracted 1.37 percentage points and 0.7 percentage points from growth, respectively.

Normal Growth Means Respectable Productivity Growth

The 2.6 percent GDP growth reported for the quarter, coupled with near flat growth in work hours (the number of self-employed declined sharply in the quarter), likely means that productivity grew at close to a 2.0 percent annual rate in the third quarter.

This comes after an unprecedented pace of decline in the first half of the year, with productivity dropping at a 7.1 percent annual rate in the first quarter and a 4.1 percent annual rate in the second quarter. These declines were likely attributable to a variety of factors including the winter omicron wave, rapid turnover in the labor market, and supply chain disruptions. But whatever the causes, we seem to be back on a path of normal productivity growth, which will alleviate inflationary pressure in the economy.

Inflation Edged Downward

The core Personal Consumption Expenditures (PCE) rose at an annual rate of 4.5 percent in the third quarter, down from 5.6 percent in the first quarter and 4.7 percent in the second quarter. While the 4.5 percent pace is well above the Fed’s 2.0 percent target, the direction of change is noteworthy. If inflation were being driven largely by an excessively tight labor market, then inflation should be accelerating, not slowing.

Saving Rate Fell, but Main Factor is Higher Capital Gains Taxes

The saving rate edged lower in the quarter to 3.3 percent of disposable income from 3.4 percent in the second quarter. That compares to a saving rate of 8.8 percent of disposable income in 2019 before the pandemic.

This has been generally portrayed as people spending down the savings they accumulated during the pandemic. While this is true to some extent, the biggest factor is that people are paying more taxes, presumably capital gains taxes on stocks they sold in the last year. (Capital gains are not counted as income.)

The tax share of personal income rose from 11.8 percent in 2019 to 14.7 percent in the third quarter. If the tax share of personal income had remained constant, the saving rate would have been more than 3.0 percentage points higher in the third quarter.

Consumption of Goods Fell, While Services Continue to Increase

We are continuing to see a reversal of the pandemic shift from service consumption to goods consumption. Consumption of goods fell at a 1.2 percent annual rate, with the biggest factor being a sharp drop in car purchases, but real spending on gas and food also declined.

Consumption of services grew at a 2.8 percent annual rate, down from a 4.6 percent pace in the second quarter. This increase led to a 1.4 percent growth pace for consumption overall. The growth rate for services is only moderately higher than we had been seeing before the pandemic, so we are not seeing a story of massive catch up following the pandemic.

Health Care Spending Continues to Fall as a Share of GDP

Medical spending continued to edge lower as a share of GDP. It is now 0.9 percentage points lower than the 2019 share. Since the Centers for Medicare and Medicaid Services had projected 0.2 percentage points increase per year, we are now 1.5 percentage points below trend. This is equivalent to $375 billion in annual savings on health care spending.

Residential Construction Falls at a 26.4 Percent Annual Rate

The falloff in residential construction accelerated in the third quarter, declining at a 26.4 percent rate after dropping at a 17.8 percent rate in the second quarter. This is consistent with monthly data showing a sharp decline in housing starts, although construction has not fallen to the same extent, as builders still have a large backlog of homes to finish.

Another factor in the decline is the end of the mortgage refinancing boom. The fees associated with refinancing are counted in this category. The larger category that includes these fees fell at a 40.7 percent annual rate in the quarter.

Investment Growth Remains Strong

Equipment investment returned to double digit growth, increasing at a 10.8 percent annual rate after a small decline in the second quarter. Investment in intellectual products also remains healthy, growing at a 6.9 percent rate. This was more than enough to offset the continuing decline in investment in nonresidential structures, which fell at a 15.3 percent rate. Nonresidential investment as a whole grew at a 3.7 percent rate.

Inventory Accumulation Returns to Normal

Inventories subtracted 0.7 percentage points from growth in the quarter, but still grew at a $61.9 billion annual rate. Since inventories had been growing at an extraordinary pace in the prior three quarters, this means that the third quarter pace was a drag on GDP growth. With many retailers reporting excessive inventories, we may see further slowing, and possibly even declines, in the next two quarters.

The buildup of inventories is good news from the standpoint of inflation, as many retailers will have to markdown prices to move merchandise. On the negative side, farm inventories fell at a $22.9 billion annual rate, continuing a long pattern of declines. This could mean that inflation in food prices will persist.

Exports Surged, But Growth Is Not Likely to Continue

Exports rose at a 14.4 percent annual rate in the third quarter after rising at a 13.8 percent rate in the second quarter. This added 1.63 percentage points to growth in the quarter. Imports fell at a 6.9 percent rate, adding 1.14 percentage points to growth in the quarter.

The export surge is unlikely to continue. With the economies of most of our major trading partners weakening and likely falling into recession, they will be buying less from the United States. The surge in the dollar also acted to make our goods less competitive, further dampening exports and raising imports.

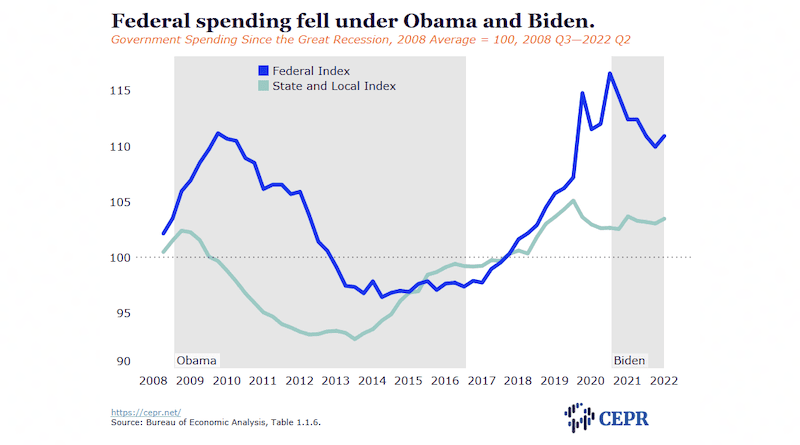

Government Spending Added 0.42 Percentage Points to Growth in the Quarter

Federal spending increased at a 3.7 percent annual rate in the quarter, while state and local spending rose at a 1.7 percent rate. Federal spending has declined as a share of GDP under President Biden, as it did under Obama.

Third Quarter Looks Very Good

The overall picture in the third quarter GDP report is overwhelmingly positive. The economy is on a path of healthy growth again. Furthermore, it looks like inflation is slowing, albeit slowly. The return to positive productivity growth indicates that many of the problems with reopening from the pandemic are behind us and the economy will look much more normal going forward.

However, the Fed’s rate hikes will slow the economy further in future quarters. We are unlikely to see a comparable boost to growth from net exports in the next few quarters. Residential construction will contract further, and we may again see drags on growth from inventories if retailers look to pare back their stockpiles.

In short, this is a very good picture, but one with many clear warning signs