Low Real Interest Rates Support Asset Prices, But Risks Are Rising – Analysis

By Nassira Abbas and Tobias Adrian

Supply disruptions coupled with strong demand for goods, rising wages and higher commodities prices continue to challenge economies worldwide, pushing inflation above central bank targets.

To contain price pressures, many economies have started tightening monetary policy, leading to a sharp increase in nominal interest rates, with long-term bond yields, often an indicator of investor sentiment, recovering to pre-pandemic levels in some regions such as the United States.

Investors often look beyond nominal rates and base their decisions on real rates—that is, inflation-adjusted rates—which help them determine the yield on assets. Low real interest rates induce investors to take more risks.

Despite somewhat tighter monetary conditions and the recent upward move, longer-term real rates remain deeply negative in many regions, supporting elevated prices for riskier assets. Further tightening may still be required to tame inflation, but this puts asset prices at risk. More and more investors could decide to sell risky assets as those would become less attractive.

Differing outlooks

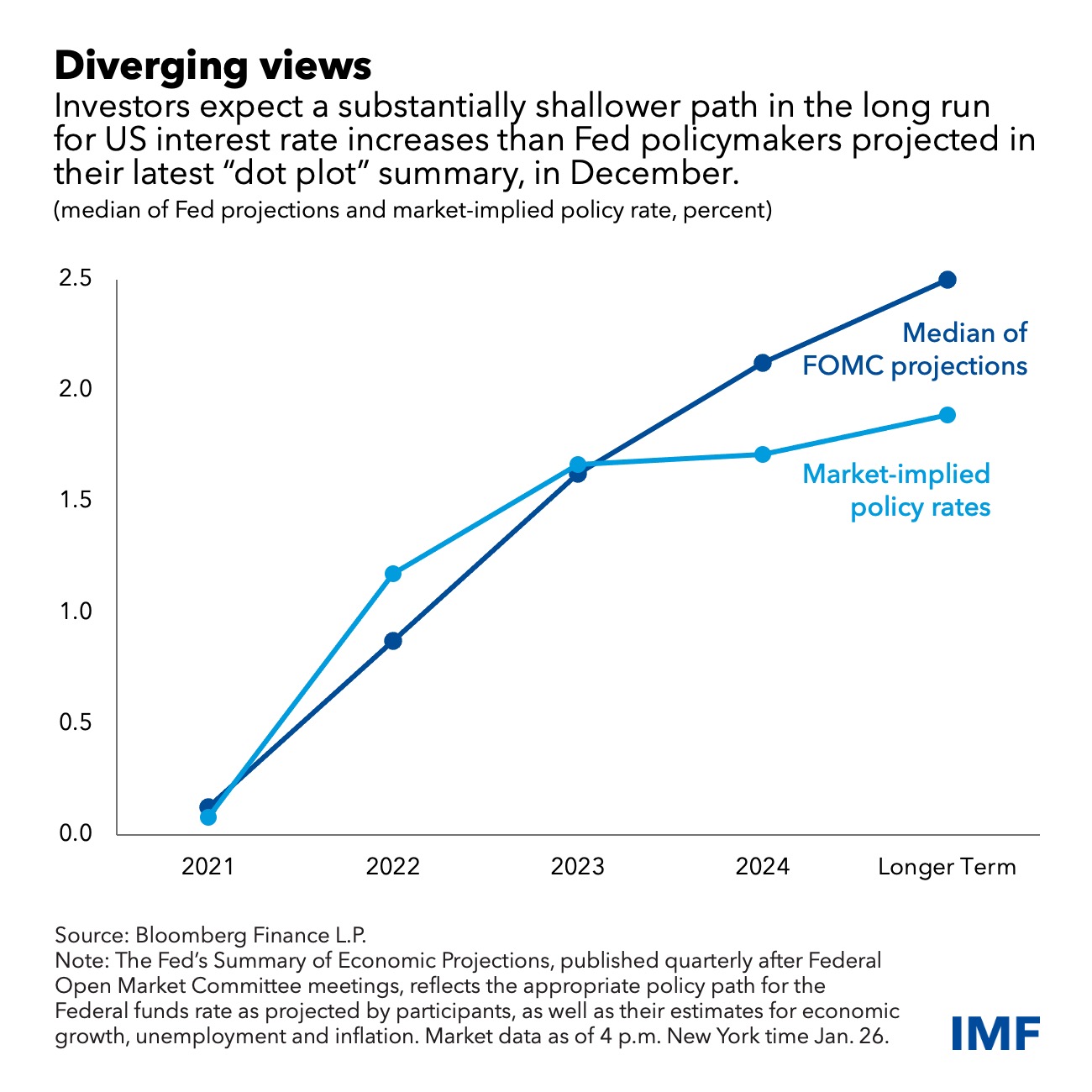

While shorter-term market rates have climbed since central banks’ hawkish turn in advanced economies and some emerging markets, there is still a sharp difference between policymakers’ expectations of how high their benchmark rates will rise and where investors expect the tightening will end.

This is most obvious in the United States, where Federal Reserve officials project that their main interest rate will reach 2.5 percent. That’s more than half a point higher than what 10-year Treasury yields indicate.

This divergence between markets and policymakers’ views on the most likely path for borrowing costs is significant because it means investors may adjust their expectations of Fed tightening upward both further and faster.

In addition, central banks might tighten more than they currently anticipate because of persistent inflation. For the Fed, this means the main interest rate at the end of the tightening cycle might exceed 2.5 percent.

Implications of the rate-path divide

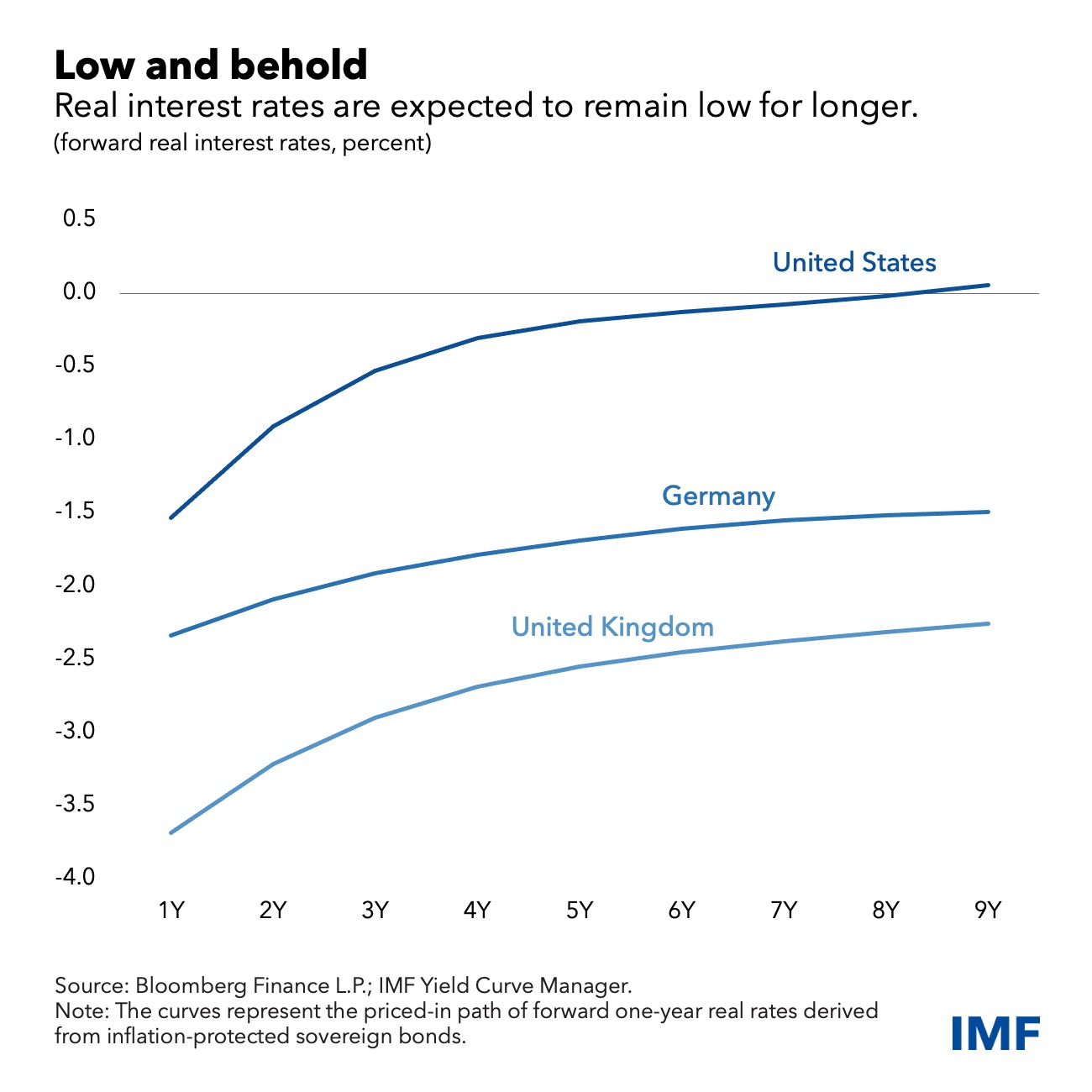

The path of policy rates has important implications for financial markets and the economy. As a result of high inflation, real rates are historically low, despite the recent rebound in nominal interest rates, and are expected to remain so. In the United States, long-term rates are hovering around zero while short-term yields are deeply negative. In Germany and the United Kingdom, real rates remain extremely negative at all maturities.

Such very low real interest rates reflect pessimism about economic growth in coming years, the global savings glut due to aging societies, and demand for safe assets amid higher uncertainty exacerbated by the pandemic and recent geopolitical concerns.

The unprecedented low real interest rates continue to boost riskier assets, notwithstanding the recent upward move. Low long-term real rates are associated with historically elevated price-to-earnings ratios in equity markets, as they are used to discount expected future earnings growth and cash flows. All things being equal, monetary policy tightening should trigger a real interest rate adjustment and lead to higher discount rate, resulting in lower stock prices.

Despite the recent tightening in financial conditions and concerns about the virus and inflation, global asset valuations remain stretched. In credit markets, spreads are also still below pre-pandemic levels despite some modest widening recently.

After an exceptional year supported by solid earnings, the US equity market started 2022 with a steep retreat amid high inflation, uncertainty about growth and weaker earnings prospects. As a result, we expect that a sudden and substantial rise in real rates could cause a significant drop for US stocks, particularly in highly valued sectors such as technology.

Already this year, the 10-year real yield has increased by nearly half a percentage point. Stock volatility soared on greater investor nervousness, with the S&P 500 down more than 9 percent for the year and the Nasdaq Composite measure tumbling 14 percent.

Impact on economic growth

Our growth-at-risk estimates, which link future economic growth downside risks to macrofinancial conditions, could increase substantially if real rates rise suddenly and broader financial conditions tighten. Easy conditions helped global governments, consumers, and businesses withstand the pandemic, but this could reverse as monetary policy tightens to curb inflation, moderating economic expansions.

In addition, capital flows to emerging markets could be at risk. Stock and bond investments in those economies are generally seen as being less safe, and tightening global financial conditions may cause capital outflows, especially for countries with weaker fundamentals.

Looking ahead, with persistent inflation, central banks face a balancing act. All the while, real interest rates remain very low in many countries. Monetary policy tightening must be accompanied by some tightening of financial conditions. But there could be unintended consequences if global financial conditions tighten substantially. A higher and sudden increase in real interest rates could lead potentially to a disruptive price revaluation and an even larger selloff in stocks. As financial vulnerabilities remain elevated in several sectors, monetary authorities should provide clear guidance about the future stance of policy to avoid unnecessary volatility and safeguard financial stability.

*About the authors:

- Nassira Abbas is a deputy division chief in the Global Markets Monitoring and Analysis Division of the Monetary and Capital Markets Department and an author of the Global Financial Stability Report.

- Tobias Adrian is the Financial Counsellor and Director of the IMF’s Monetary and Capital Markets Department. He leads the IMF’s work on financial sector surveillance and capacity building, monetary and macroprudential policies, financial regulation, debt management, and capital markets.

Source: This article was published by IMF Blog