Increased Gasoline Production And High Inventories Combine To Reduce Global Refinery Gasoline Margins – Analysis

By EIA

EIA recently released the What Drives Petroleum Product Prices website that identifies and tracks several fundamental and financial market factors that influence petroleum product spot and futures prices. This tool offers charts that highlight changes in consumption, production, inventories, and trade, mostly related to the U.S. domestic market along with some charts that include global indicators. The charts, a complement to the existing What Drives Crude Oil Prices website, will be updated monthly in conjunction with the release of EIA’s Short-Term Energy Outlook (STEO).

One aspect of the market that the tool tracks is the U.S. gasoline front-month futures crack spread, which declined recently because of increased U.S. gasoline production and inventories. In June, the reformulated blendstock for oxygenate blending (RBOB)-Brent crack spread was 37 cents per gallon (gal), 18 cents/gal below June 2015 and slightly lower than the five-year average.

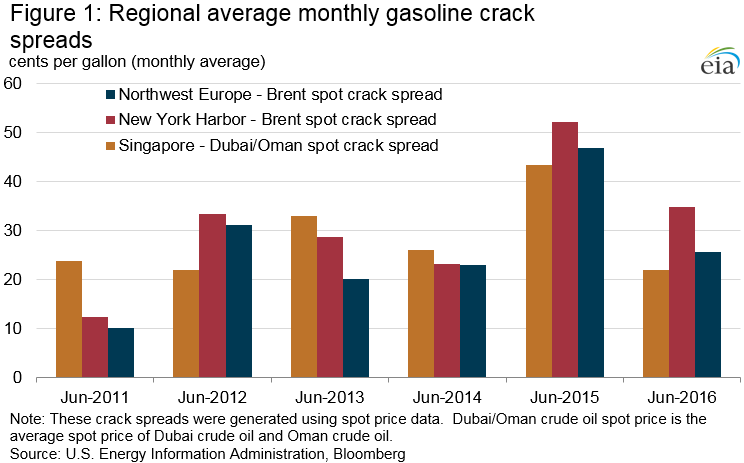

The recent trend of declining gasoline crack spreads extends beyond the United States. Unlike last year when gasoline crack spreads in some regions worldwide rose to match or set new recent record highs, this year, spreads are now significantly below last year’s levels and are generally closer to their respective five-year averages. In order to compare U.S. and international gasoline crack spreads, different spot prices for gasoline and crude oil are used, depending on the regional market. In the European gasoline market, the Northwest Europe gasoline-Brent spot crack spread averaged 26 cents/gal in June, the lowest June spread since 2014. In Asia, the Singapore gasoline-Dubai/Oman spot crack spread averaged 22 cents/gal in June, the lowest June spread since 2012 (Figure 1).

Although gasoline consumption has been robust in countries such as the United States, China, and India, gasoline crack spreads also reflect supply conditions. Growth in gasoline supply has exceeded the increase in gasoline consumption since last summer. Refineries in the United States, Europe, and Asia all increased production of gasoline compared with distillate to take advantage of the high gasoline crack spreads in 2015 and early 2016. Refineries have some ability to gradually adjust petroleum product yields in response to changes in product prices by adding additional equipment or modifying processes and feedstocks.

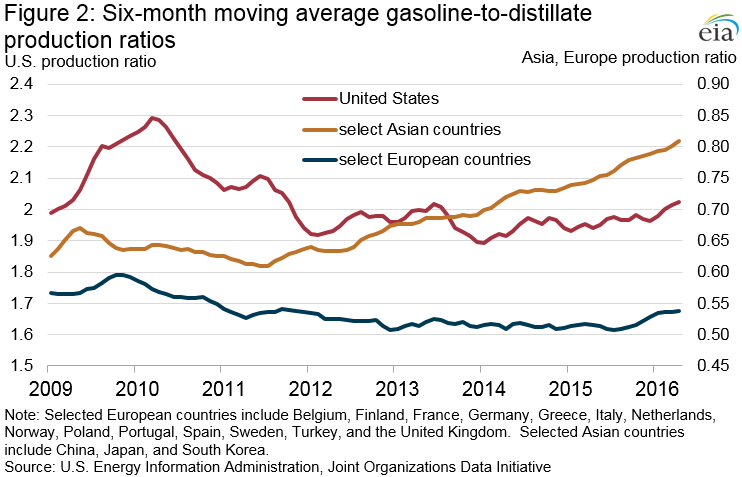

The gasoline-to-distillate production ratio differs widely across global regions, reflecting differences in their input slates and refinery configurations, which are often selected with an eye toward the mix of petroleum products used within each region (Figure 2). In the United States, the six-month moving average gasoline-to-distillate production ratio in April is at its highest level since 2011. Using data from the Joint Organizations Data Initiative (JODI), the aggregate, six-month average gasoline-to-distillate production ratio for 14 European countries, which was relatively stable from the start of 2013 through mid-2015, has risen nearly 6% since June 2015. In the Asian market, the aggregate, six-month average gasoline-to-distillate production ratio of China, Japan, and South Korea reached its highest level ever recorded by JODI in April, primarily driven by the Chinese refining sector, which produces the most petroleum products in Asia.

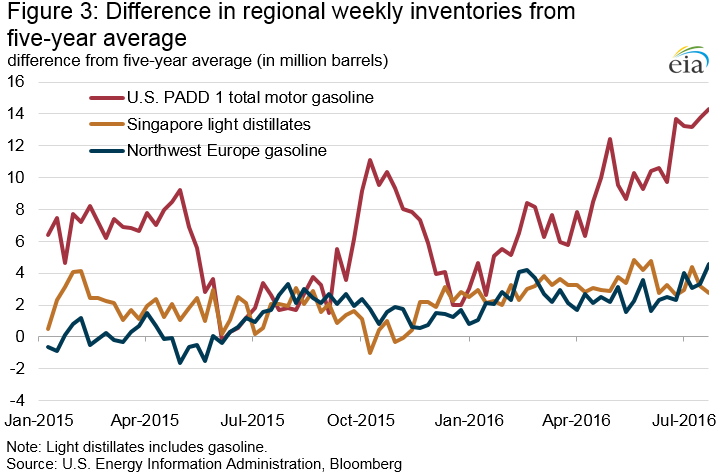

The shift toward increased gasoline production has resulted in high gasoline inventory levels globally that have remained consistently above five-year averages. In the United States, gasoline inventories in Petroleum Administration for Defense District (PADD) 1, the location of the New York Harbor trading hub, were 14.3 million barrels higher than the five-year average level as of July 22. The difference in PADD 1 inventory levels from the five-year average has been generally growing since January. In the Northwest Europe trading hub, gasoline inventories were 4.6 million barrels above the five-year average as of July 21, the largest difference in at least two years. In the Singapore trading hub, light distillate inventories, which include gasoline, were 2.8 million barrels above the five-year average as of July 20 (Figure 3). The increase in gasoline inventories in three major storage hubs has been a major driver of declining spreads between gasoline and crude oil prices throughout the world.

Based on projections for U.S. gasoline and distillate production in the July STEO, the U.S. gasoline-to-distillate production ratio is expected to remain elevated through the summer, which could keep inventory levels high and put further downward pressure on domestic gasoline crack spreads for next few months. Trade press reports suggest that some Asian refineries will not increase refinery runs through the summer, running counter to that region’s seasonal trend, because of high inventories and low cracks spreads. How gasoline crack spreads evolve through the second half of 2016 will depend on if and how refineries respond to lower gasoline crack spreads, whether by changing their output mix or reducing refinery runs.

U.S. average regular gasoline retail and diesel fuel prices decline

The U.S. average regular gasoline retail price dropped five cents from the previous week to $2.18 per gallon on July 25, down 56 cents from the same time last year. The Midwest price fell seven cents to $2.08 per gallon, the West Coast price dropped five cents to $2.67 per gallon, the East Coast price fell four cents to $2.12 per gallon, the Gulf Coast price fell three cents to $1.98 per gallon, and the Rocky Mountain price dropped one cent to $2.26 per gallon.

The U.S. average diesel fuel price fell by two cents from a week ago to $2.38 per gallon, down 34 cents from the same time last year. The Midwest price fell three cents to $2.34 per gallon, while the West Coast, East Coast, and Gulf Coast prices each fell two cents to $2.66 per gallon, $2.39 per gallon, and $2.24 per gallon, respectively. The Rocky Mountain price remained virtually unchanged at $2.43 per gallon.

Propane inventories gain

U.S. propane stocks increased by 2.2 million barrels last week to 89.6 million barrels as of July 22, 2016, 0.2 million barrels (0.2%) higher than a year ago. East Coast and Midwest inventories each increased by 0.8 million barrels, while Gulf Coast and Rocky Mountain/West Coast inventories increased by 0.4 million barrels and 0.2 million barrels, respectively. Propylene non-fuel-use inventories represented 3.2% of total propane inventories.