Strong Consumption And Inventories Lead To Faster Growth In Second Quarter – Analysis

By Dean Baker

The economy grew at a 2.6 percent annual rate in the second quarter, up from a 1.2 percent rate in the first quarter. The growth was driven primarily by a 2.8 percent rate of growth in consumption expenditures. Due to downward revisions to growth for the last three quarters, growth over the last year is just 2.1 percent.

While consumption was boosting growth in the quarter, inventories were at least not subtracting from it. The rate of inventory growth was virtually the same as in the first quarter. By contrast, there was a sharp slowing in inventory growth between the fourth quarter of 2016 and the first quarter of 2017, which subtracted 1.46 percentage points from growth in the quarter. The rate of growth of final sales of domestic product, which excludes inventories, was 2.6 percent in the second quarter, almost identical to the 2.7 percent rate in the first quarter.

The current pace of inventory accumulation is near zero, which means that inventories are likely to provide a substantial boost to growth in the next two quarters as accumulation returns to a more normal pace. This could easily add half a percentage point to growth over the next two quarters.

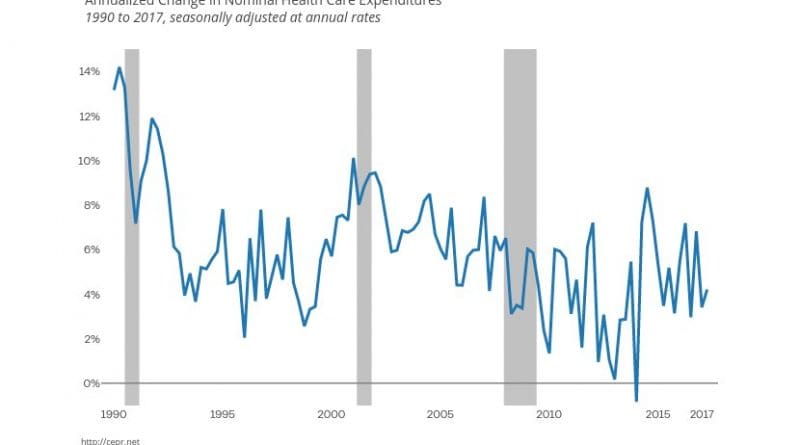

The strongest component of consumption was durable goods, which grew at a 6.3 percent annual rate. Recreational goods and vehicles were the biggest part of this growth, increasing at a 13.4 percent annual rate. Spending on services grew at a modest 1.9 percent annual rate. Health care spending continues to be restrained. Over the last year, nominal spending on personal health care services (the vast majority of health care spending) increased by just 4.3 percent. Spending on health care has grown much less rapidly in the last decade than in the 1990s and prior decades.

Non-residential investment grew at a 5.2 percent annual rate, down from 7.2 percent in the first quarter. Residential construction contracted at a 6.8 percent annual rate, subtracting 0.27 percentage points from growth. This is a fall from a first-quarter level that was likely inflated by unusually good winter weather in the Midwest and Northeast. It will not be repeated.

Net exports were a modest positive in the quarter, adding 0.18 percentage points to growth. Exports grew at a 4.1 percent annual rate, while imports rose at a 2.1 percent rate. With the recent decline in the dollar, we are likely to see continued reduction in the trade deficit in future quarters.

The government sector also gave a small boost to growth in the quarter, as a 2.3 percent growth in federal spending (all in military) more than offset a 0.2 percent rate of decline in state and local spending. This sector is also likely to provide modest contributions to growth in future quarters.

This report provides further evidence that inflation is slowing. The overall personal consumption expenditure deflator rose at just a 0.3 percent annual rate in the quarter and the deflator for the core index rose at a 0.9 percent annual rate. Both are far below the Fed’s 2.0 percent target.

The comprehensive revisions that came out with this report do little to change the overall picture of a slow-growing economy with little inflation. There was a modest downward revision to profits for 2016 of $12.4 billion (0.6 percent), but this was more than fully explained by a downward revision of $18.0 billion to the profits reported by the Fed. Due to its large asset holdings (the result of quantitative easing), the Fed’s profits are now under 4.5 percent of all corporate profits. Profits did decline by $46.2 billion in the first quarter (second quarter data aren’t available until August) as a tighter labor market is allowing workers to get back some of the income share lost in the downturn.

One item that may portend slower growth in future quarters is the unusually low savings rate. The savings rate has been under 4.0 percent for the last three quarters. This is the sort of savings rate we would expect to see in a bubble, which could indicate that the recent run up in stock prices and/or house prices is driving consumption. With some major stocks almost certainly over-valued and some housing markets getting “frothy,” there is potential for a correction that will be a substantial hit to consumption, although nothing like the crashes in 2001 and 2008.