US GDP Records Historic 32.9 Percent Drop – Analysis

By Dean Baker

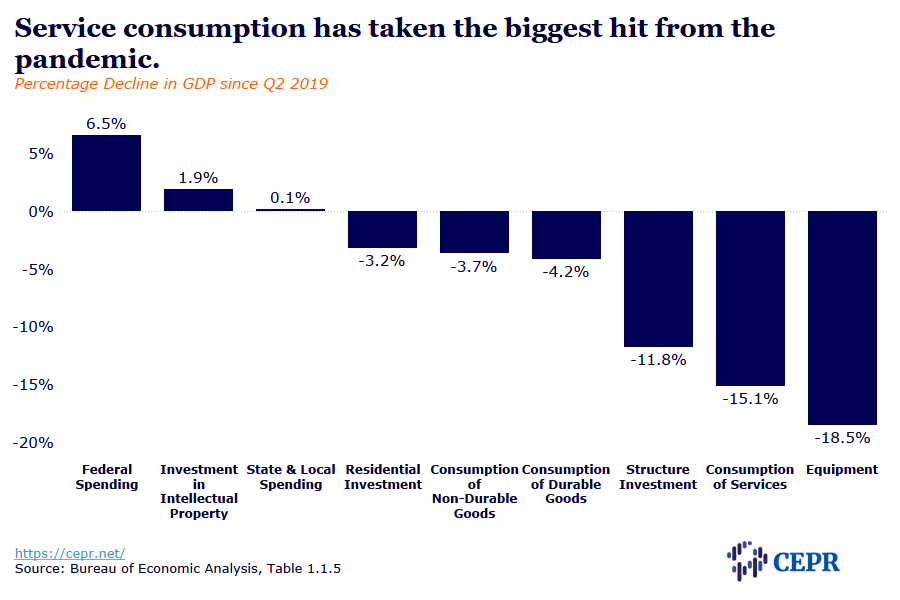

The Gross Domestic Product (GDP) shrank at a record 32.9 percent annual rate in the second quarter. While almost all the major categories of GDP fell sharply, a 43.5 percent drop in consumption of services was the largest factor, accounting for 22.9 percentage points of the drop in the quarter. Nonresidential fixed investment also fell sharply, dropping at a 27.0 percent annual rate. Residential investment fell at a 38.7 percent annual rate.

The plunge in service consumption was expected, since this was the segment of the economy hardest hit by the shutdowns. Within services, health care, food services and hotels, and recreation were the biggest factors reducing growth by 9.5 percentage points, 5.6 percentage points, and 4.7 percentage points, respectively.

Spending on health care services fell at a 62.7 percent annual rate in the quarter. This was due to people putting off a wide range of medical and dental checkups and procedures, which far more than offset the care needed by coronavirus patients. The annual rate of decline for food and hotel services was 81.2 percent and for recreation services 93.5 percent.

Consumption of nondurable goods fell at a 15.9 percent annual rate. Declines in clothing and gasoline purchases were the biggest factors, taking 1.0 percentage point and 0.9 percentage points off the quarter’s growth, respectively. Demand for durable goods fell at just a 1.4 percent rate, but this followed a decline of 12.5 percent in the first quarter. Interestingly, spending on cars actually rose slightly in the quarter, adding 0.15 percentage points to growth.

Consumption expenditures by nonprofits serving households rose at 182.5 percent annual rate, adding 3.0 percentage points to the quarter’s growth. This reflects the effort by private foundations and charities to ameliorate the hardships being experienced by many households.

Both structure and equipment investment fell sharply in the quarter, declining at 34.9 percent and 37.7 percent annual rates, respectively. The drop in equipment investment is especially striking since it fell at a 15.2 percent rate in the first quarter. Investment in intellectual products fell at a more modest 7.2 percent annual rate. Residential investment fell at a 38.7 percent annual rate, although this followed a jump of 19.0 percent in the first quarter.

Exports and imports both fell sharply, with exports dropping at a 64.1 percent rate and imports falling at a 53.4 percent rate. Because US imports are so much larger than exports, trade actually added 0.7 percentage points to growth in the quarter.

Federal government spending rose at a 17.4 percent annual rate, driven by a 39.7 percent increase in nondefense spending, presumably most of which is pandemic related. State and local spending fell at a 5.6 percent rate, likely reflecting school closings in the quarter.

Prices fell sharply in the quarter, with the Personal Consumption Expenditure (PCE) deflator falling at a 1.9 percent annual rate and the core PCE falling at a 1.1 percent annual rate. These declines reflected sharp drops in the price of items such as gasoline, hotels, and clothes. Many of these declines were already being reversed by the end of the quarter. They will almost certainly not continue into the third quarter.

The savings rate soared to a record 25.7 percent. This reflects the jump in disposable income attributable to the pandemic checks, coupled with the sharp drop in spending. Nominal disposable income rose at a 42.1 percent annual rate. This rise was, of course, uneven, with people who were still getting their regular paychecks or retirees seeing large jumps in income from the pandemic checks, but with many of the unemployed seeing sharp drops.

With the economy mostly reopened, despite serious outbreaks of the pandemic in large parts of the country, we are virtually certain to see strong growth in the third quarter. But even if the economy grows at a 15 or 20 percent annual rate, it would be nowhere close to recovering the losses from the last two quarters.

The shape of the rescue package currently being debated will also be hugely important. In addition to the unemployment insurance supplements that will be necessary for laid-off workers to sustain their consumption, state and local governments will need large amounts of money both to avoid layoffs and to implement programs for the safe reopening of schools, workplaces and businesses. In this context, it is very difficult to see any economic rationale for the $1,200 pandemic checks.