How Will The Pandemic And War Shape Future Monetary Policy? – Analysis

I. Introduction

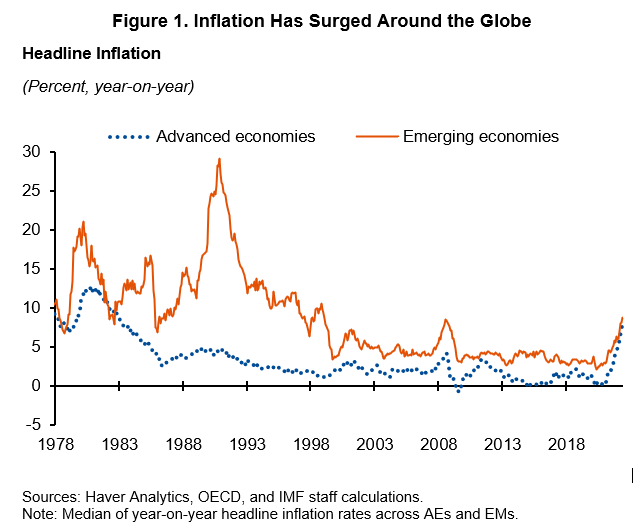

After more than three decades of Great Moderation which saw inflation trending down in both advanced economies (AEs) and emerging markets (EMs), inflation has surged over the last year almost everywhere (Figure 1). The recent period is also unique because of the two tail-risk events that have played out: a global pandemic and Russia’s invasion of Ukraine. It is therefore natural to ask what lessons, if any, this period offers for the conduct of monetary policy in the future. I will cap the horizon at 5 years as that seems a reasonable horizon over which to speculate about the future.

I’d like to view the lessons learned through two lenses. First, while the panel theme suggests a focus on structural change, it is helpful to begin by considering lessons from the pandemic and war that are relevant for monetary policy even if these developments don’t result in regime-shift or structural change. That is, assuming the global economy largely moves back to the low real interest rate environment that prevailed before the pandemic, that inflation returns to target, and the key structural relations underpinning aggregate supply and demand don’t change.

The second lens focuses on the possibility that the pandemic and war may induce persistent structural change in the economy, and, if so, on the implications for policy. For central banks, two questions seem critical. First, will the pandemic change aggregate supply in a way that is likely to materially affect monetary policy tradeoffs? And second, will there be long-lived effects on the equilibrium or neutral real interest rate, r*, or on the transmission of monetary policy to aggregate demand? These questions are relevant for central banks worldwide.

In this paper, I will argue that even in the absence of structural changes, the post-pandemic experience has provided important new perspectives on the Phillips curve and sources of inflation risk that should influence future monetary policy. While existing models embedding a very flat Phillips curve (so that slack has a limited influence on inflation) seem to have performed well in forecasting inflation since the Great Moderation began in the early 1980s, I’ll highlight how they have performed poorly in forecasting the recent inflation surge. These modeling shortcomings help account for why IMF forecasts—like many others— significantly underpredicted the recent rise in global inflation. While we are still working to understand what caused inflation to surge, several factors appear at play. These include the massive size of the global fiscal and monetary stimulus; the speed with which it was deployed; that it was heavily channeled into goods (given the pandemic limited the demand for services), causing key sectors to bump against capacity constraints; and that potential employment likely declined on top of other supply-related bottlenecks.

While the pandemic and war are unique events in many respects, they have stress tested our monetary policy frameworks and strategies. Based on this experience, the robustness of policy strategies based on a flat Phillips curve, including “running the economy hot” and “looking through” temporary supply shocks, should be revisited. While running the economy hot can indeed have important benefits, and is sometimes appropriate, we need to rethink the benefits and costs in light of the more evident inflation risks. This is particularly the case given difficulties in measuring the level of potential employment or output, and because it is more likely that sharp rises in relative prices in key sectors give rise to broad-based inflation when the economy is running near full capacity. Better models of aggregate supply —including those that take more account of capacity constraints at the sectoral level – are also needed, and will help in refining policy strategies.

On the possibility that the pandemic and war could cause structural shifts, I’ll argue that the current period of very high inflation does pose a significant risk that inflation expectations become de-anchored. Moreover, the pandemic and war may induce changes in aggregate supply that increase supply shock volatility and make potential output and employment more difficult to forecast. Such developments, if they materialize, would pose more difficult tradeoffs for central banks. These risks may be intensified if the climate transition is delayed, or if countries try to increase supply chain resilience by adopting inward-looking policies that restrict global trade. Accordingly, I’ll argue that central banks must move decisively today to avoid the risk of de-anchoring, and that global policies should push forward on the Paris climate agenda and support the expansion of diversified global trade. On the aggregate demand side, some considerations, such as ageing demographics and inequality, suggest that the pandemic and war are unlikely to shift us out of a low equilibrium interest rate environment, although this remains subject to considerable uncertainty. The high level of global debt and increasing reliance on fiscal policy to support economies could well raise equilibrium interest rates.

II. What Accounts for the Inflation Surge?

II.A. Existing Models with a Flat Phillips Curve Cannot Explain the Inflation Surge

The inflation surge has clearly been a surprise from the perspective of pre-crisis policy frameworks, especially for AEs. The building blocks of pre-crisis policy frameworks in AEs included the widely held view that the Phillips curve was extremely flat, and that the equilibrium real interest rate had fallen significantly due to factors including demographics, slowing productivity growth, and strong demand for safe assets. The flatness of the Phillips curve was widely corroborated by empirical evidence and reinforced by the experience after the global financial crisis (GFC) of 2008 in which, even as many countries pushed unemployment to multi-decade lows, inflation and medium-run inflation expectations remained below target.

Consistent with this paradigm, existing models—including both empirical and structural models—embedded a low Phillips curve slope. As a result, they can’t explain the recent inflation surge, and predict a much smaller rise in core inflation than has in fact materialized.

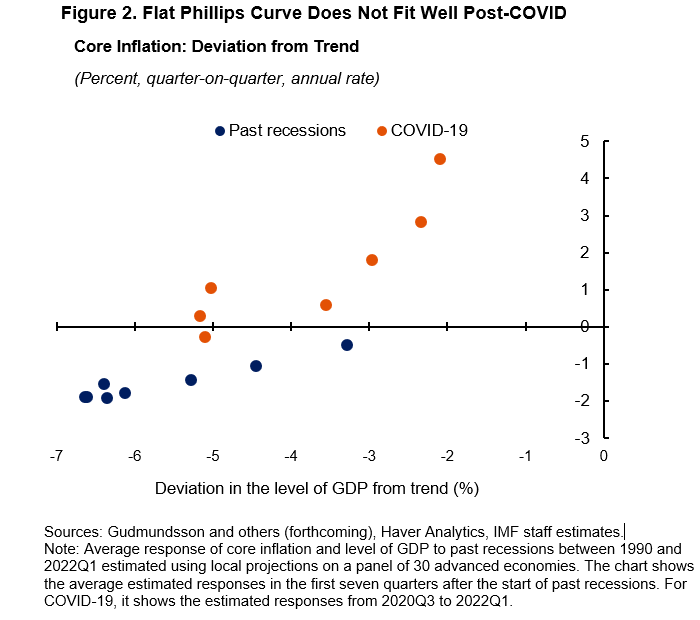

Figure 2 highlights the unusual behavior of inflation in the pandemic recovery based on quarterly data for advanced economies. The blue dots plot average inflation against the deviation of output from trend during past downturns dating to 1990—derived from local projections—and are consistent with a very flat Phillips curve. By contrast, the pandemic recovery (starting in 2020Q3) shows inflation rising sharply even while output remained below the pre-pandemic estimated trend. This is suggestive of both a steeper Phillips curve and fall in potential output.

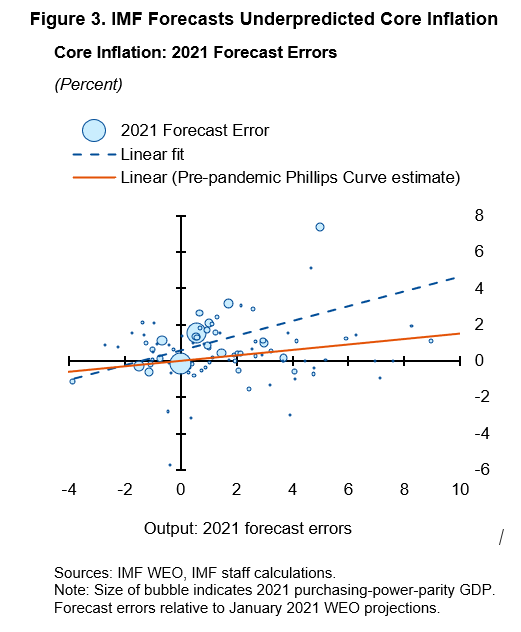

Given the flat estimated Phillips curve, most inflation forecasts tended to underpredict inflation—including those of the IMF. Figure 3 illustrates this by showing how IMF forecasts of core inflation made in early 2021—here for a broad group of advanced and emerging market economies—tended to systemically underpredict core inflation, so that forecast errors are systematically large and positive. The forecast errors are large relative to historic norms for both AEs and EMs. It is true that the price inflation forecasts missed in part because forecasts of unemployment—on which they were conditioned—were also too pessimistic. But given the very flat Phillips curves, it would have made little difference to core inflation forecasts even if forecasts for unemployment had been exactly correct.

Interestingly, the forecast errors turn out to be highly correlated with GDP outturns in these economies. This suggests that demand-side pressures may have played a much more fundamental role in generating inflation than captured by the small weight on the unemployment gap in the Phillips curve. As I will later discuss, this may reflect that the usual measures of slack have understated resource pressures, that the weight on slack may be larger, or other factors.

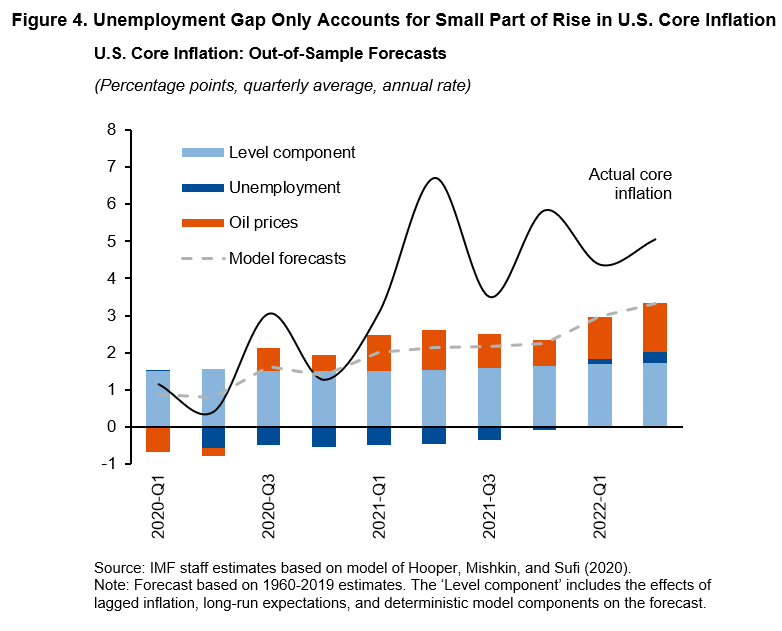

It is helpful to complement this graphical analysis with more formal econometric analysis—presented in Figure 4 for the United States—to help gauge the role of labor market tightness in accounting for inflation. Our model is based on re-estimating the model of Hooper, Mishkin, and Sufi (2020), and specifies that U.S. core inflation depends on the unemployment gap; long-term inflation expectations (10-year horizon); and oil prices. The specification and estimates—including of the Phillips curve slope—are very much in line with other research, including estimates by Federal Reserve staff.[1]

While the model turns out to fit U.S. core inflation very well over the pre-COVID period, consistent with the view that inflation behavior is well-explained by a very flat Phillips curve, it significantly understates the rise in core inflation out of sample since the spring of last year. While it does predict some rise in core inflation—to about 3 percent in 2022: Q2 from 2 percent earlier—less than ¼ percentage point of the inflation runup is attributable to the fall in unemployment below the estimated natural rate. Thus, existing models suggested little reason for concern about inflation pressures.

II.B. What Factors Have Driven the Inflation Surge?

The sharp runup in inflation in many countries—notwithstanding that unemployment rates have only returned to pre-pandemic levels—surely reflects some of the highly unusual developments we’ve seen in the wake of the pandemic, including the recent war in Ukraine. Nonetheless, exploring further why our models missed the inflation surge is helpful not only in gauging what policies are needed to bring down inflation today, but also for devising more robust policy strategies in the medium run.

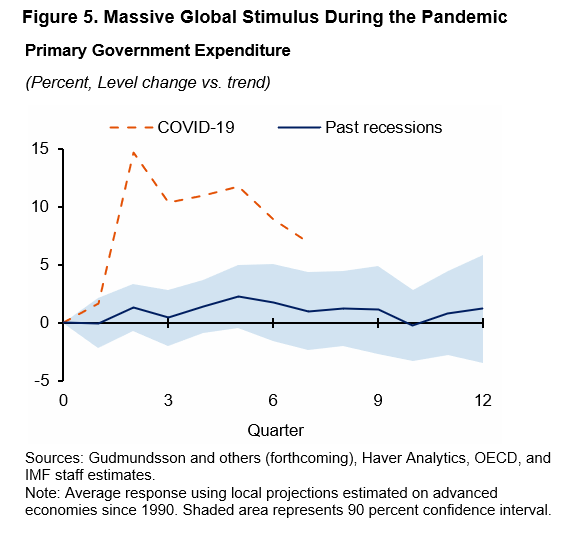

Although our understanding of the causes of the global inflation surge is still evolving, several factors appear to be playing a major role. First, global demand was buoyed by an aggressive policy response, as many countries deployed fiscal and monetary stimulus at the same time. Figure 5 provides some idea of the massive size of the fiscal stimulus relative to past recoveries in AEs. These stimulative policies played a vital role in cushioning the magnitude of the COVID-19 recession and in promoting faster recovery. But they have helped fuel the recent inflation, especially against the backdrop of contractions in global supply driven by COVID-19 shutdowns and pervasive supply chain bottlenecks.

Second, because the pandemic limited the ability of households to consume services, the large demand stimulus was in effect heavily channeled towards non-contact goods, especially consumer durables such as autos. With this massive rotation towards goods, goods demand rebounded far more quickly than services, and this helped drive a much faster runup in goods price inflation. The runup in goods price inflation was the key driver of the inflation surge around the world, followed by surging energy prices, especially since Russia’s invasion of Ukraine. It seems very likely that binding capacity constraints at the sectoral level—including specialized labor—worked in a nonlinear way to fuel these sharp price increases, with supply disruptions also playing a material role. These rapid price increases contributed to significant shifts in household and firm expectations about inflation that may have also contributed to more broad-based inflationary pressures, including by affecting wage formation.

Third, the pandemic reduced potential labor supply and output. This partly reflects the exit of older workers from the labor force, but also shifts away from certain contact-intensive sectors such as health care. This decline helps account for why the labor market in the United States and other countries appears much tighter than pre-pandemic, even though employment is at or below pre-crisis levels. The strong pickup in demand for services in the past year has made the decline in effective labor supply all the more evident, and together these developments help account for the broadening of inflationary pressures to services as well as wages.

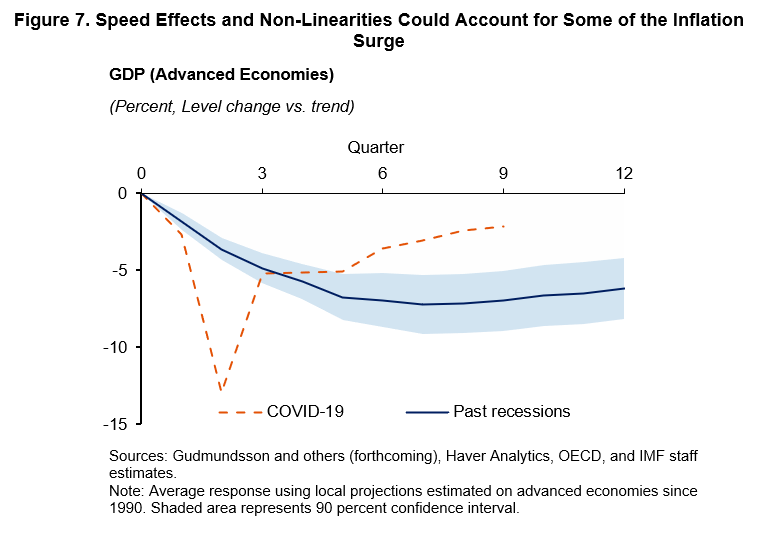

Fourth, it is plausible that speed effects—that is, effects related to the speed of the recovery—accounted for some of the inflation surge. As seen in Figure 7, the rebound in demand since early last year—and pace of employment gains—has been extraordinarily rapid relative to the pace of earlier recoveries, including from the GFC. This fast recovery put unusual strain on key sectors of the economy.

All told, the massive demand stimulus and contractions in supply would not be enough to account for much inflation if the Phillips curve was flat and linear. But the strong channeling toward goods early in the recovery made capacity constraints kick in at the sectoral level, so that the Phillips curve—at least in a reduced form sense—looks much more upward-sloping and nonlinear. Of course, our understanding of the factors driving inflation and the channels through which they operate remains work-in-progress.[1]

III. What Are the Lessons for Future Monetary Policy?

These observations lead naturally to considering whether the pandemic and the war in Ukraine have changed our understanding of how the economy works in a way that should influence future policy strategy. While the pandemic was surely a unique shock with many idiosyncratic features, my sense is that it in effect provided a stress-test of the existing policy framework. We can learn from it—especially about the Phillips curve and aggregate supply—and should reconsider the appropriateness of policy prescriptions in that light.

One key prescription that emerged in several AEs from the period between the GFC and the pandemic was that it was OK, and potentially desirable, to run the economy hot, by which I mean allowing unemployment to run well below its natural rate and output to move above potential. This strategy seemed to work well both for the United States and other advanced economies in the long post-GFC recovery: unemployment fell gradually while inflation remained below central bank targets. Given effective lower bound risks, allowing unemployment to fall below its long-term natural rate was in fact helpful in ensuring that inflation expectations didn’t drift down and further constrict policy space. Moreover, it helped generate a very broad-based labor market recovery that pushed down unemployment rates of disadvantaged segments of the population to historic lows.

But the pandemic recovery suggests that the inflation risks of running the economy hot may be considerably higher than previously thought. First, there are major difficulties in measuring economic slack—the employment or output gap. This risk was highlighted in research by Orphanides (2002) as a major cause of the Great Inflation of 1965-82: in essence, policymakers were “running the economy hot” without realizing that potential output and employment were lower than what they were targeting. The difficulty in measuring slack has also become more apparent during the pandemic. Measures of slack based on pre-crisis trends—whether unemployment, or more broad-based measures such as the employment rate of prime-aged workers, have suggested little cause for concern even in recent months; whereas measures such as the vacancy-to-unemployment and quit rates suggest a red-hot labor market in the United States and some other countries.

While mismeasurement would not be a problem if the Phillips curve was flat, there is a reasonable body of evidence suggesting that nonlinearities become significant at very low unemployment rates. For example, the Hooper, Mishkin, and Sufi (2020) paper estimates that the rise in inflation from a marginal decrease in unemployment is several times larger when the unemployment rate falls below 4 percent than at higher levels of unemployment of, say, more than 5 percent. Because it’s hard to measure slack, it’s difficult for policymakers to tell exactly when those heightened pressures will kick in, but the risks to inflation get significantly higher in a hot economy.

Second, the pandemic experience suggests that in a hot economy, it is more likely for shocks to cause overheating at the sectoral level as various sectors hit capacity constraints. The high interconnection between sectors means that binding constraints in one sector—such as energy production—can easily translate into cost pressures for many other sectors.

Third, and relatedly, inflation may rise quickly in a hot economy due to speed effects. Supply curves are less elastic in the short term. Thus, rapid increases in demand—including potentially from fiscal stimulus—tip the economy more easily into a situation of more intense price pressures.

From a policy perspective, running the economy hot may still be desirable under certain circumstances. In particular, for an economy in recession and facing chronically low inflation—conditions that could well resurface in coming years—the commitment to allow the economy to eventually run hot may spur faster recovery today and keep inflation expectations from drifting below target (Eggertsson and Woodford, 2003). But the pandemic experience suggests that the modalities of how the policy is deployed and communicated should take more account of upside inflation risks that may emerge down the road. Thus, policymakers might well seek to push unemployment below the natural rate, but should be more cautious about calibrating policy to generate a deep and persistent undershoot. Forward guidance should also be accompanied by more explicit “escape clauses” to deal with the risk that inflation rises more than expected. And in more normal circumstances with inflation close to target, policymakers should be considerably more wary about the inflation risks posed by a hot economy.

A second prominent view pre-pandemic was that major central banks could rely on their credibility to largely “look through” temporary supply shocks on the premise that they would have only a transient influence on inflation. While it was recognized that policy rates would have to adjust in response to second round effects, i.e., the more persistent effects on inflation, the latter were typically estimated to be very small (at least for advanced economies). Hence, policymakers didn’t expect to have to move policy rates much even in response to fairly large shocks—they could “look through” the shock rather than face a difficult tradeoff between inflation and employment objectives.

But the pandemic experience suggests that central banks need to be more attentive to the risk that supply shocks may have broad-based and persistent effects on inflation under certain conditions, and that these second-round effects may emerge with surprising speed. The bigger second-round effects may arise because strong upward price pressures in certain sectors become more diffuse through supply-chain linkages, from unexpectedly strong transmission to wages, or because the shocks affect inflation expectations in a way that heavily influences price or wage-setting.

Hence, some refinement to how central banks implement a “looking through” strategy—to ascertain whether the conditions for very small second-round effects are likely to be satisfied—would seem warranted. Drawing on the pandemic experience, several factors could influence the likelihood that supply shocks may give rise to substantial second-round effects, and thus call for a more forceful policy response. First, the size and breadth of the shock likely matters: While little policy response may be required if the shock is confined to a particular market, and is clearly supply-driven, such an approach can result in undue inflationary pressure if the shock encompasses many more sectors. Initial conditions also matter. Thus, the prescription of “looking through” may lead to problems if inflation has already been running high, so that inflation expectations are more likely to be dislodged by additional shocks. Central banks may also need to react more aggressively in a strong economy in which producers can pass on cost hikes more easily and workers may be less willing to accept real wage declines.

To help refine these strategies and their implementation, we will clearly need better models of aggregate supply that take account of the pandemic experience. Models that use alternative measures of slack—such as the ratio of vacancies to unemployment—may better capture labor market tightness than models that key off the unemployment gap, and better account for inflation dynamics. It will also be useful to further develop sectoral models that differentiate between goods and services, and which incorporate capacity constraints at the sectoral level as well as different speeds of price adjustment.[1] Such models can be helpful in gauging how shocks that begin in goods markets—as in the pandemic—may give rise to broader pressures on wages and the prices of services (i.e., second-round effects). Relatedly, we will need to deepen our understanding of how wage and price-setting decisions are influenced by expectations about future inflation, and about which expectations measures are most relevant (e.g., household or market-based, and at what horizon?) Such modeling will help better assess the robustness of central bank policies.

IV. Risks of Structural Change

I’ll next turn to the possibility that the pandemic induces persistent structural shifts or regime change that could have significant implications for monetary policy in the medium -term. Such shifts may be compounded by developments following the war in Ukraine. I’ll begin by focusing on aggregate supply and the Phillips curve, and then turn to possible shifts on the aggregate demand side.

IV.A. Risk of De-Anchoring of Inflation Expectations

One key risk is that the current high level of inflation leads to a de-anchoring of inflation expectations. My sense is that central banks are very attentive to this risk and are acting to contain it. Recent model estimates of inflation expectations provide some assurance of stability. Still, with inflation running near double-digit levels in the United States and many advanced economies, and some emerging markets experiencing even higher inflation, such risks are more material for the global economy than at any time in the last few decades.

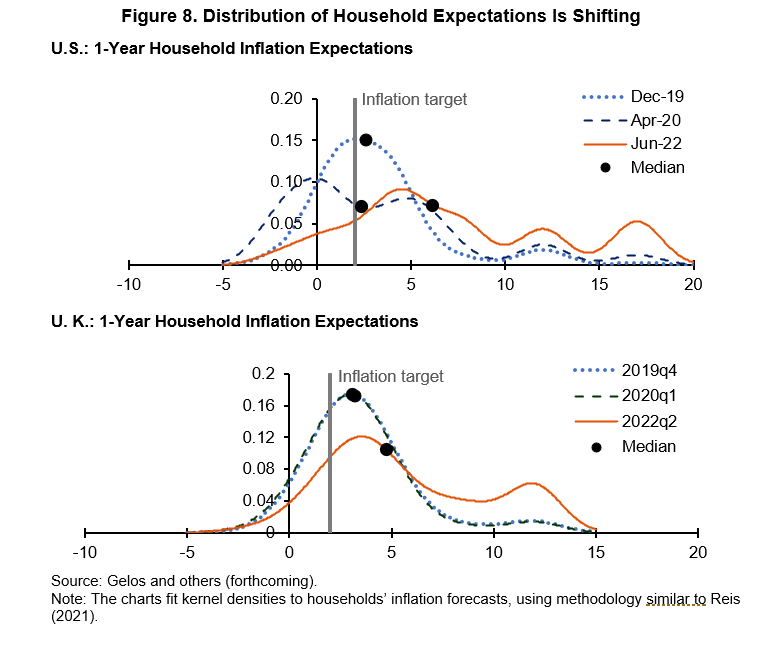

Both market-based and survey evidence suggest considerable upside inflation risk for both the United States and other advanced economies. For example, in the United States, current estimates based on options suggest roughly a 20 percent chance that inflation averages over 4 percent over the next 5 years. This is consistent with Ricardo Reis’ research that indicates that the risk of an “inflation disaster” is quite high (Hilscher, Raviv, and Reis, 2022). Evidence on household inflation expectations derived from surveys, including those shown in the charts for the United States and United Kingdom, respectively, indicate that the distributions of households’ expectations have shifted substantially. High inflation outcomes are viewed as more likely, especially at horizons of one to three years. In the absence of a forceful policy response, such shifts of expectations at shorter horizons may well feed into wage and price-setting decisions and heighten the risk of de-anchoring. Notably, disagreement about inflation prospects has risen relative to the pre-pandemic period and there has been an increase in the proportion of households expecting very high inflation outcomes. Some preliminary evidence suggests that higher disagreement among households on near-term expectations can be indicative of future shifts in longer-term expectations (Gelos and others, forthcoming).

De-anchoring would make addressing monetary policy tradeoffs much more challenging, as both exchange rate depreciations and supply shocks would have much more persistent effects on inflation. Thus, more forceful tightening would be needed in response to adverse supply shocks to move inflation back to target, resulting in a larger contraction in real activity.

IV.B. Other Key Risks to Aggregate Supply in the Medium-Term

Advanced economy central banks have—since the GFC—largely focused on the challenge of providing additional stimulus to boost both output and inflation in the face of a binding lower bound on policy rates, without facing a tension between these objectives. But there is a significant risk that the supply-side disruptions we’ve seen during the pandemic will give rise to an environment where aggregate supply is much more volatile even in the medium-term. In this case, central banks would face new challenges in dealing with supply shocks that force them to make difficult tradeoffs between fighting inflation and supporting employment or growth.

On the labor market side, post-pandemic labor supply is likely to be more uncertain and hence harder to predict for some time (Duval and others, 2022; Faberman, Mueller, and Sahin, 2022; Crump and others, 2022). There is a great deal of uncertainty about whether people will return to contact sectors such as health care, and on what the increased demand for flexibility means for aggregate labor supply. And COVID-19 itself may pose ongoing challenges as new strains emerge and cause recurrent shutdowns, or if the virus has highly damaging effects on the health and hence labor supply decisions of households. In this vein, a recent study indicated that about 20 percent of people experiencing long-COVID (about three percent of those in the study) found that their daily activities had been markedly impaired, suggesting that COVID-19 may significantly affect labor supply (Waters and Wernham, 2022).

The pandemic and war have also delayed global progress on achieving climate targets consistent with the Paris agreement, increasing the risk of a disorderly climate transition. While some shift in priorities is understandable given the severity of the pandemic and escalation in energy prices during the past year, decisively pushing ahead with the climate agenda is critical if we are to hope for a reasonably smooth transition.

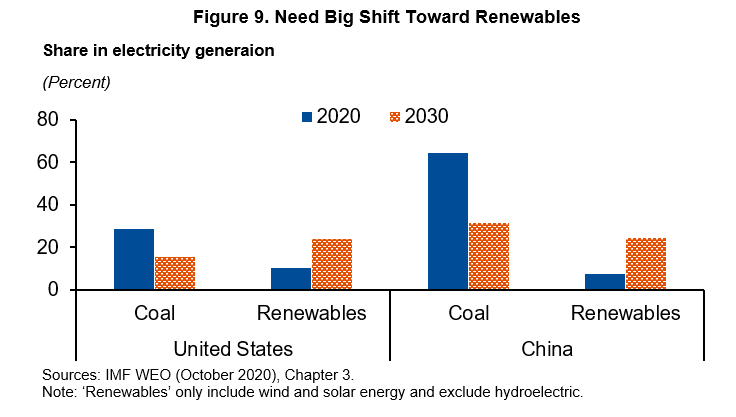

IMF staff analysis indicates that major shifts in the structure of energy production—from coal and fossil fuels to cleaner energy sources, as seen in Figure 9—will be needed in the current decade if the Paris goals are to be achieved. The policy packages required—including some combination of carbon taxes, subsidies for renewables, and regulatory changes—will, by design, cause a sharp decline in the production and consumption of coal, oil, and natural gas. Potential output is likely to fall in the near term, though the hit may be small if some revenue from carbon taxes is used to boost the economy’s capacity (including through incentivizing green investment). But moving now allows for a more gradual and predictable implementation of these policy changes which will greatly reduce the costs.

Conversely, staff analysis suggests that delaying the transition even a couple of years will substantially increase the economic costs and heighten the risk of a disorderly transition in which carbon taxes would have to be ratcheted up quickly to limit the devastating effects of climate change. Central banks would have to grapple with much larger energy price shocks, and the high uncertainty that would prevail in such an environment would weigh heavily on investor and consumer confidence and overall economic growth.

On the product markets side, Russia’s invasion of Ukraine and policy actions taken in response have led to a large spike in uncertainty about trade policy. While some restructuring is desirable to deal with security risks and build resilience, global policymakers will have to be attentive to the risks of taking policy actions that can fuel fragmentation and a disorderly restructuring of global trade.

A key risk is that policymakers respond to concerns about supply chain vulnerabilities by adopting more inward-looking policies. Staff analysis, including in the IMF’s spring World Economic Outlook (WEO), has instead highlighted the substantial benefits of building more diversified supply chains that are spread out over a broader set of countries and hence are less susceptible to adverse developments in any specific country. As illustrated in the Figure 10, model-based simulation analysis in the April 2022 WEO (IMF, 2022) considered the hit to GDP from a country-specific supply chain disruption abroad, and showed that a more diversified production structure can reduce the GDP losses by roughly 50 percent. By contrast, a shift toward more inward-looking policies would not only raise production costs substantially, but also make countries more vulnerable to supply-side shocks.

IV.C. Risks More Acute for EMs

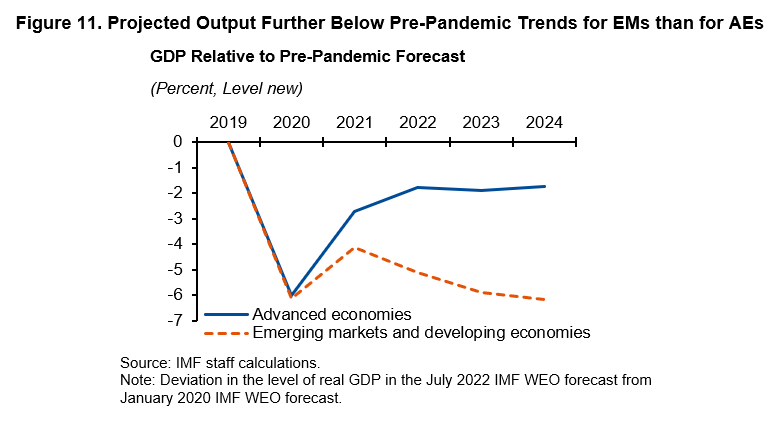

The decline in average EM inflation over the last two decades went along with a shift to greater central bank independence and—for many EMs—a shift to an inflation targeting framework. The recent surge in inflation has less to do with “running the economy hot” or “looking through supply disruptions” but is mostly a consequence of large external shocks, a larger share of goods in consumption baskets, and lower potential output alongside demand recoveries. Our projections for output from the WEO (5 years out) are much further below pre-pandemic trends for EMs than for AEs, so that the pandemic has been a major structural break for these economies. Despite having larger output/employment shortfalls relative to AEs, EMs have responded much faster to rising inflation pressures. Should the risks of greater supply shock volatility and heightened fragmentation materialize, they will pose considerably more difficult policy tradeoffs for central banks globally, but especially for EMs where inflation expectations are already less well-anchored.

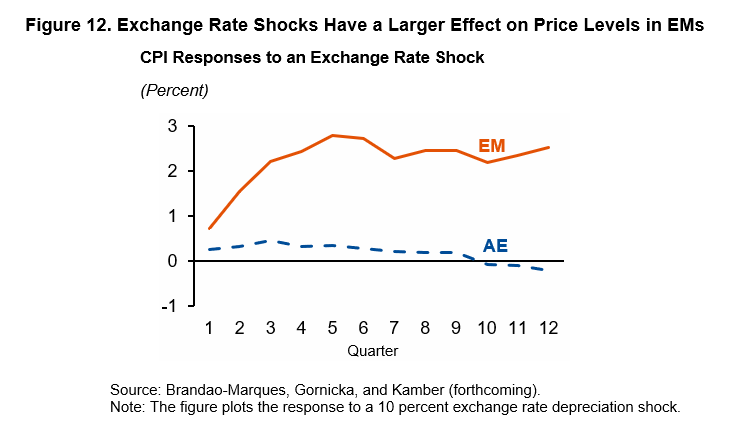

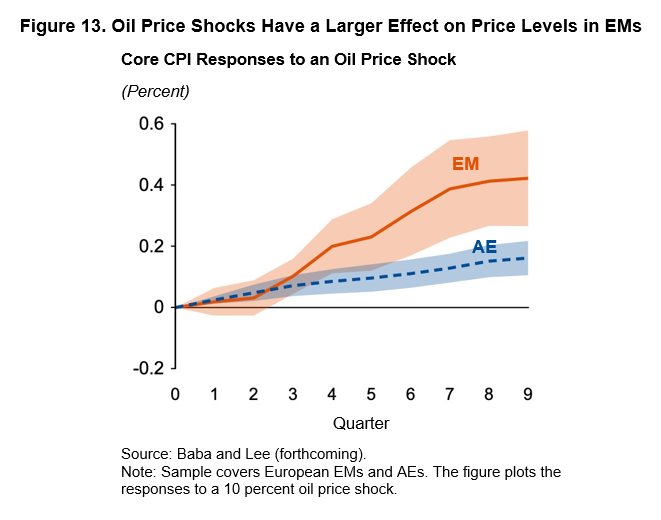

While EM central banks have made major strides in gaining monetary policy credibility in the past two decades—and have achieved a much higher degree of control over inflation—external shocks still pose greater challenges than to AEs. The pass-through from commodity price shocks and exchange rate changes to inflation tends to be much higher and more persistent than for AEs. To illustrate, Figure 12 shows some recent staff estimates which indicate that a 10 percent depreciation of EM currencies against the dollar causes the price level to rise about 2 percent, several times larger than in advanced economies. The bigger rise in inflation means that EM central banks must raise interest rates more aggressively to curtail inflationary pressures, so that a depreciation may well be contractionary as the stimulus from net exports (working mostly through reductions in imports in the short run, consistent with dominant currency pricing) is more than offset by a fall in domestic demand.[1] Similarly, Figure 13 draws on other IMF staff estimates which show that the effects of an oil price shock on inflation—also scaled to be 10 percent initially—are also much larger for EMs than for advanced economies (note: here the focus is just on European economies).

Accordingly, a persistent shift to a more fragmented global environment—which would expose EMs to greater commodity price shocks and exchange rate pressures—would confront EM central banks with worse policy tradeoffs, often forcing them to tighten to rein in inflation at the cost of substantially weakening growth. For many EMs, these tradeoffs may be compounded by concerns about access to international funding (owing to monetary tightening in AEs) and financial stability risks given domestic buildup of private debt.[1]

Of course, policy tradeoffs for EMs would worsen further if a legacy of the pandemic and war turns out to be a weakening of policy credibility and poorer anchoring of inflation expectations. As noted, many EM central banks—to their credit—began aggressively hiking policy rates to control inflationary pressures and keep inflation expectations well-anchored. But with credibility in EMs still more fragile than in AEs, inflation expectations are more susceptible to de-anchoring, including if inflation runs persistently high rather than coming down in the next year or two in line with most forecasts.

Inflation expectations in EMs also seem to be more sensitive to the fiscal position than in AEs, which is a concern given the runup in public debt in the wake of the pandemic. As seen in Figure 14, a surprise increase in government debt boosts medium-term expected inflation in EMs significantly, while having little effect in advanced economies.

The heightened sensitivity of inflation expectations to the fiscal stance likely captures a broader concern that EM central bank independence is less secure than advanced economies. Central banks everywhere, including in AEs, may face more incursions on their independence if inflation remains persistently high and they need to maintain tight monetary policies even as unemployment rises. However, these risks are higher for EMs given weaker institutional frameworks and protections. As independent monetary policy is a linchpin for the anchoring of inflation expectations, de-anchoring is an even greater risk for these economies.

IV.D. Potential Shifts in r* and Transmission to Aggregate Demand

In principle, the pandemic and war could also have enduring effects on the demand side of the economy by affecting the equilibrium or neutral real interest rate (r*), or the transmission of policy rates to output through the Investment-Savings (IS) curve.

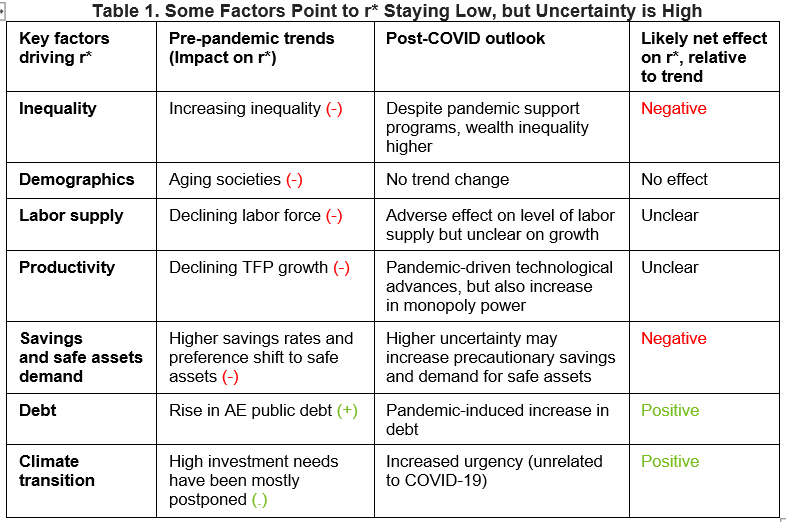

It’s helpful to consider the channels through which the pandemic and war could potentially affect r* in a way that would be consequential for policymakers in the medium term. These include the “usual suspects” listed in the table, which include effects on inequality, demographics, productivity and labor supply growth, the demand for safe assets, and public debt and investment.

It is possible that the pandemic and war will put further downward pressure on r* through increased demand for savings and safe assets, and through their effects on inequality. While the aggressive policy response kept the pandemic from having much effect on income and consumption inequality (at least in advanced economies), wealth inequality increased further. However, these effects could well be offset by other pandemic-related developments that could boost r* in the medium run. Notably, the pandemic may have heralded a shift in readiness to use fiscal policy to counteract recessions, which may increase r* by increasing global demand as well as the supply of safe assets. Further, if the postponement of climate investment during the pandemic spurs much-needed large-scale catch-up public investment, r* could also rise.

It seems either unlikely that the pandemic will have much of a quantitative effect on other key determinants of r*, such as demographics, or the effects are simply uncertain at this point, such as in the case of productivity growth. In the latter case, the pandemic has clearly spawned rapid technological progress in areas such as online retail, but may have also increased firm concentration in a way that may restrain future technological advances.[1]

All in all, while there are factors such as ageing demographics and rising inequality that are likely to keep r* low, there remains high uncertainty around its trajectory.[2]

I don’t expect that the pandemic will have large effects on the open economy IS curve for most advanced economies. There is some risk, however, that the transmission of policy rate changes to aggregate demand in EMs could be adversely affected by the large buildup of debt that occurred during the crisis. A tightening of policy may be more likely to cause a large rise in risk spreads to heavily indebted borrowers, making monetary transmission less predictable.

V. Implications for Policy: Lessons, Future Risks, and What Central Banks Must Do Today

To wrap up, I do think that the pandemic and war raise new challenges for central banks. Since the GFC and until very recently, advanced economy central banks have focused on the problems of providing enough stimulus to support demand and boost too-low inflation. The issues were all about providing enough firepower to deal with the effective lower-bound on policy rates and addressing downside risks to inflation and activity. There was little sense that inflation could rise persistently and substantially above target, or that central banks would face major tradeoffs in addressing supply shocks. Risk management—at least for advanced economy central banks—shifted heavily toward a focus on downside rather than upside inflation risks.

The pandemic and war have underscored the need for the risk management framework to take full account of both upside and downside risks to inflation, as well as to the possibility that serious tensions may arise between the objectives of price stability and employment or growth. The pandemic has reminded us again that the Phillips curve may not be flat when the economy is operating at high capacity and expanding strongly, and that shocks—such as big jumps in energy prices—may play out very differently in such an environment relative to one in which growth is more subdued. Accordingly, it will be important to revisit the robustness of policy strategies—including of “running the economy hot” and “looking through” temporary supply shocks—in the light of more palpable upside inflation risks. These approaches can produce considerable benefits, but we must think about how to refine the strategies to better contain the risks they may pose to price stability.

Beyond these lessons, there is good reason for concern that the pandemic and war may lead to an era in which supply shocks are larger, and in which inflation expectations may be less well-anchored. These risks are most acute for emerging markets, especially those with high debt levels where fiscal dominance can easily take hold. But with inflation running near double digits for the first time in several decades, AE central banks also face significant risks.

Accordingly, central banks must act decisively today to ensure that inflation expectations are anchored. We can’t have sustained economic growth going forward without re-establishing price stability and making sure that our policy framework is well-suited to securing this goal. Forward guidance can play an essential role in communicating how central banks will bring this about. Central banks should indicate that they will “stay the course” and maintain tight policy as long as inflation remains high. And if inflation proves unexpectedly persistent, they should underscore their resolve to tighten more aggressively, even if it means a sharp cooling of the economy and rise in unemployment.

While central banks must be in the driver’s seat in the battle against inflation—and have the requisite tools—other policies can help. First, fiscal policy should play a supportive role. While there is a strong case for fiscal policy to help low-income households under current the circumstances, such support should be targeted and avoid providing macro stimulus.[3] And some countries should likely tighten fiscal policy further. Second, global policymakers need to push ahead on the climate agenda—failing to do so will not only complicate the task of central banks, but will pose grave risks to economic stability and global well-being. Finally, global policies that encourage the expansion of global trade and reduce fragmentation risks will both reduce the risk of volatile supply shocks and help boost potential output around the globe.

*About the author: Gita Gopinath is the First Deputy Managing Director of the International Monetary Fund (IMF) as of January 21, 2022. In that role she oversees the work of staff, represents the Fund at multilateral forums, maintains high-level contacts with member governments and Board members, the media, and other institutions, leads the Fund’s work on surveillance and related policies, and oversees research and flagship publications.

Source: This article is based on remarks by Gita Gopinath – Prepared for the Jackson Hole Symposium, and published by the IMF

References

Baba, Chikako, and Jaewoo Lee. Forthcoming. “Second-Round Effects of Oil Price Shocks.” IMF Working Paper, International Monetary Fund, Washington, DC.

Board of Governors of the Federal Reserve System. 2022. “Summary of Economic Projections.” Meeting of the Federal Open Market Committee, Washington, DC, June 14–15.

Brandao-Marques, Luis, Marco Casiraghi, Gaston Gelos, Olamide Harrison, and Gunes Kamber. Forthcoming. “Public Debt and Inflation Expectations.” IMF Working Paper, International Monetary Fund, Washington, DC.

Brandao-Marques, Luis, Lucyna Gornicka, and Gunes Kamber. Forthcoming. “Exchange Rate Pass-Through in Emerging Market Economies.” IMF Working Paper, International Monetary Fund, Washington, DC.

Crump, Richard K., Stefano Eusepi, Marc Giannoni, and Ayşegül Şahin. 2022. “The Unemployment-Inflation Trade-off Revisited: The Phillips Curve in COVID Times.” NBER Working Paper 29785, National Bureau of Economic Research, Cambridge, MA.

Duval, Romain, Yi Ji, Longji Li, Myrto Oikonomou, Carlo Pizzinelli, Ippei Shibata, Alessandra Sozzi, and Marina M. Tavares. 2022. “Labor Market Tightness in Advanced Economies.” IMF Staff Discussion Note 2022/001, International Monetary Fund, Washington, DC.

Eggertsson, Gauti B., and Michael Woodford. 2003. “The Zero Bound on Interest Rates and Optimal Monetary Policy.” Brookings Papers on Economic Activity 1: 139–233.

Faberman, R. Jason, Andreas I. Mueller, and Ayşegül Şahin. 2022. “Has the Willingness to Work Fallen During the Covid Pandemic?” NBER Working Paper 29784, National Bureau of Economic Research, Cambridge, MA.

Fernald, John, Huiyu Li, and Mitchell Ochse. 2021. “Labor Productivity in a Pandemic.” FRBSF Economic Letter 2021-22 (August 16).

Gelos, Gaston, David Hofman, Julia Otten, Gurnain Pasricha, and Zoe Strauss. Forthcoming. “Are Household Inflation Expectations De-Anchoring?” IMF Working Paper, International Monetary Fund, Washington, DC.

Gudmundsson, Tryggvi, Chris Jackson, Rafael Portillo, and Daniel Rivera Greenwood. Forthcoming. “The Global Inflation Surge of 2021: Stylized Facts and Cross-Country Variation.” IMF Working Paper, International Monetary Fund, Washington, DC.

Hilscher, Jens, Alon Raviv, and Ricardo Reis. 2022. “How Likely Is an Inflation Disaster?” Unpublished.

Hooper, Peter, Frederic S. Mishkin, and Amir Sufi. 2020. “Prospects for Inflation in a High Pressure Economy: Is the Phillips Curve Dead or Is It Just Hibernating?” Research in Economics 74 (1): 26–62.

International Monetary Fund (IMF). World Economic Outlook Databases. Washington, DC.

International Monetary Fund (IMF). 2020a. World Economic Outlook: A Long and Difficult Ascent. Washington, DC, October.

International Monetary Fund (IMF). 2020b. “Toward an Integrated Policy Framework.” IMF Policy Paper 2020/046, Washington, DC.

International Monetary Fund (IMF). 2022. World Economic Outlook: War Sets Back the Global Recovery. Washington, DC, April.

McGregor, Thomas, and Frederik Toscani. Forthcoming. “A Bottom-Up Reduced Form Phillips Curve for the Euro Area.” IMF Working Paper, International Monetary Fund, Washington, DC.

Orphanides, Athanasios. 2002. “Monetary-Policy Rules and the Great Inflation.” American Economic Review 92 (2): 115–120.

Reis, Ricardo. 2021. “Losing the Inflation Anchor.” Brookings Papers on Economic Activity BPEA Conference Draft, September 9.

Waters, Tom, and Thomas Wernham. 2022. “Long COVID and the Labour Market.” IFS Briefing Note BN246, Institute for Fiscal Studies, London, U.K.

[1] Fernald and others (2021) suggest that longer-term effects of the pandemic on productivity will be modest, but note considerable uncertainty.

[2] The most recent Federal Open Market Committee (FOMC) projections about the long-run real policy rate, based on the June 2022 Summary of Economic projections, suggests a real neutral rate that is essentially unchanged from its December 2019 level of about 0.5 percent.

[3] Separately, through composition shifts, fiscal policy can support labor and product market reforms to ease bottlenecks and boost aggregate supply.

[1] The complexity of such policy trade-offs in a context of significant frictions may in some cases warrant the use of additional policy tools, including FX intervention, capital flow measures, and macroprudential policies, as explored in the IMF’s Integrated Policy Framework (IMF, 2020b).

[1] Moreover, currency depreciation in EMs is often associated with investor flight that causes domestic financial conditions to tighten and hence exacerbates the output decline, especially for economies with high FX liabilities.

[1] See McGregor and Toscani (forthcoming) for an empirical model of inflation in the euro area that differentiates across sectors.

[1] Other factors may account for some of the rise in inflation during the pandemic in addition to those discussed here, including, for instance, higher price markups or persistent declines in labor productivity (the latter would tend to boost unit labor costs).

[1] The Hooper, Mishkin, and Sufi (2020) analysis is attractive insofar as it considers a wide range of specifications and also allows for nonlinearities.