What The World Can Learn From Argentina’s Holdout Saga – Analysis

By VoxEU.org

As Argentina’s protracted and litigious restructuring saga comes to an end, it is natural to ask what lessons the world can draw from this contentious process. This column takes a close look at Argentina’s ordeal, revealing just how idiosyncratic it has been. While it is therefore less influential than most people think, the long script yields important and unexpected lessons.

By Juan José Cruces and Eduardo Levy Yeyati*

As Argentina’s protracted and litigious restructuring saga comes to an end, it is natural to ask what lessons the world can draw from this contentious process. While a close look reveals that Argentina’s ordeal has been fairly idiosyncratic, and hence less influential than most people think, the 15-year-long script yields important, albeit unexpected, lessons. Here’s a list.

Super-CACs are great and you should use them (but risks remain)

The first lesson has already been learnt and implemented, but it will be at least a decade before we can rely on it. The key problem affecting a sovereign debt restructuring is the lack of a formal bankruptcy procedure whereby a judge can ‘cram down’ recalcitrant creditors when a debtor makes a reasonable offer. Two types of cures have been proposed. The first one, a statutory mechanism that allows an international bankruptcy court to handle the restructuring, never got a lot of traction. The second one, a contractual solution that enables a super-majority of creditors (e.g. 75%) to approve a restructuring that becomes binding for the rest, is known as collective action clauses (or CACs) and was endorsed by developed countries and by the IMF two years after Argentina’s default. Most sovereign debt issued thereafter contains this anti-vulture shield.

The problem with these original collective action clauses is that they ran on individual bonds. Thus, it is easy for a hedge fund to buy 25.1% of a small issue and block the restructuring. If, around the time of default, the bond traded at one-third of its par value (as bonds often do in such circumstances), the blocking ‘investment’ on a 100 million series would only require $8.4 million, a modest ticket in the hedge-fund world.

To cure this problem, in 2014 collective action clauses evolved into super-collective action clauses (or Super-CACs) that allow restructuring on the basis of a single vote across all affected bond series so that, if a country restructures debt for $100 billion, a blocking party need to invest a hefty $8.4 billion to block it. In the process, the language in the bond covenants was modified to preclude that the standard equal treatment clause (known as pari passu) could be interpreted to mean ratable payment – as Judge Griesa did in NML v. Argentina.

So, if you are a sovereign debtor and your bonds have simple collective action clauses, or no collective action clauses at all, you would do well by swapping your debt to super-CACs while global interest rates are low and the markets remain liquid.

Have we solved the sovereign debt restructuring problem? Not so fast! According to a document prepared by the IMF for the International Financial Architecture group of the G20 meeting this week in Washington, there is $935 billion of emerging country government debt outstanding, and only a tiny 11% have super-CACs and refined pari passu clauses. At the very least, there will be a long waiting period before the 2014 vaccines immunise the system. Moreover, contractual perfection is hardly an achievable status and the possibility exists that vultures will try to game the new contracts in ways that we cannot anticipate at this stage. Hence the need to pay attention to the other lessons from Argentina’s sore experience.

Weigh the costs of a hardball approach to restructuring

Argentina took a very tough stance in its restructuring, offering a 73% haircut in present value terms. This compares to a mean haircut of 42% for all restructurings of middle income countries after the Brady plan (Cruces and Trebesch 2014), and a similar mean cut for countries that had debt/GDP ratios at the time of the exchange comparable to that of Argentina. While one could understand why local political considerations could justify the reasonableness of this offer, in hindsight it is less clear that it was such a good strategy. According to Edwards (2015), it was excessive. For one thing, the acceptance rate of the 2005 offer was a mere 76%, the second lowest among all 17 sovereign debt restructurings since 1998 for which we have participation rate data. After adding the creditors who accepted the 2010 reopening of the exchange, Argentina’s 92.7% acceptance rate is the fourth lowest of all restructurings.

More importantly, in order to get creditors to swallow this bitter pill, Argentina offered two legal assurances to those who tendered in the exchange – both of which eventually boomeranged against the debtor.

First, there was the Rights Upon Future Offers (RUFO) clause contained in the exchange bond contracts. It guaranteed tendering bondholders that, if Argentina were to make a better offer at any point during the ten years after the exchange, it would also make it available to them. In effect, this rather unusual clause prohibited Argentina from settling with holdouts on better terms before 2015. For example, when the US Supreme Court confirmed the ruling of lower courts against Argentina in June 2014, there was ample discussion about whether settling at that time would violate the RUFO clause. Indeed, there was a risk that if Argentina were to settle with the 7% of remaining holdouts, it might impair what had already been arranged with the other 93% of original creditors who had accepted Argentina’s previous offers.

In part because the acceptance rate to the offer made in November 2004 was very low at the beginning, and in part at the request of organised creditor groups, in early February 2005 Argentina enhanced the RUFO clause with a Lock Law that stipulated that no further official offers were to be made after the debt exchange, and that no other dealings with creditors whatsoever were ever to be made – including of course repurchasing held-out bonds in the secondary market at dirt-cheap prices, something that would have proved very convenient ex post.

By burning the government’s bridges, the Lock Law was intended as a dissuasive now-or-never element in the context of a game of chicken with tired creditors. As it turned out, this de jure subordination of the old debt to the new debt was the main point in NML’s pari passu case, as the law stated in black and white that holdouts were not to have the same treatment as exchange bondholders. Thus, after engineering an attachment-proof payment system abroad and successfully resisting attempts to seize reserves, real estate and even an old frigate, Argentina failed by its own Trojan horse – the ‘innovative’, redundant and ultimately self-defeating Lock Law.

The rise in creditor litigation: Argentina and the rest of the world

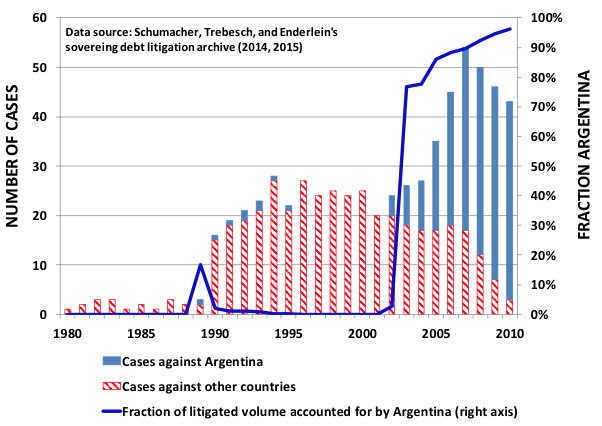

Tying one’s hands had an important toll, as reflected by litigation activity. The above figure is a refinement of Figure 1 in Schumacher et al. (2015) shown in Cruces (2016). It illustrates the outstanding institutional investor creditor lawsuits against sovereigns in courts in the US, the UK, and the World Bank’s ICSID, at the end of each year between 1980 and 2010 (left axis). The solid line depicts the participation of claims against Argentina in the total amount under litigation (measured on the right axis). Of the 43 suits pending at the end of 2010, 40 were against Argentina and they accounted for 96% of the amount involved.

State-contingent debt may look better on paper

Argentina issued a bond in 1998 that, with the benefit of hindsight, proved to be a particularly bad and costly idea. Known as a Floating Rate Accrual Note (or FRAN), the bond carried a variable coupon that was proportional to the country’s financing cost, as measured by the yield on some other — more liquid — sample bond that was set to mature in 2006. Floating Rate Accrual Notes were expected to save on interest should Argentina become Latin America’s next investment grade credit, which the government aspired to at that time. Unfortunately, events moved in the exact opposite direction and the contract ended up protecting the buyer against the deterioration of Argentina’s credit rating. As Matt Levine recently noted, the bond resembled a credit default insurance contract written by the issuer against itself.

There are better forms of contingent debt, to be sure. The oldest and simplest alternative is to use a callable bond. This is like the refinancing option embedded in a typical home-mortgage loan. It allows a family the right to refinance the loan should interest rates drop. The Brady bonds issued after the debt defaults of the 1980s had this feature built in.

In October 2001, right before the default, the floating interest rate for the Floating Rate Accrual Notes was fixed at 25.4%. By April 2002, with the country already in default, the interest was at 72.8%, and by the time of the Floating Rate Accrual Note’s maturity in 2005 it had reached an astonishing 101%. The cherry on the cake came in 2009, when a ruling by Judge Griesa in favour of NML accepted to use the last mark after the sample bond’s expiration, 101%, to carry interests forward until the date of the final money judgement. In sum, after 2006, the interest on the Floating Rate Accrual Note was tied to the ‘yield’ on a dead bond that was also defaulted, and kept constant by a court decision until money judgments were entered.1

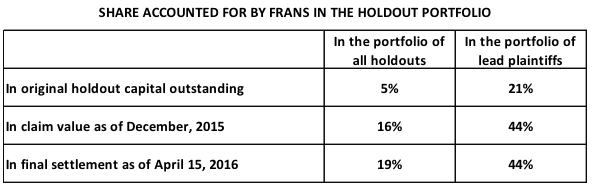

Compared with the majority of the other held out bonds that accrued fixed rates of interest of around 11% per annum, the Floating Rate Accrual Notes resulted in a significant distortion in the distribution of claims as shown in the following table.

The ruinous consequences of this bond aside, its key role in the holdout saga is the fact that it offers a strong incentive, 101% per year to be precise, to hold out. If you want defaulted creditors to stay away from the exchange and engage in protracted litigation, there is simply no better instrument around.

As highlighted in Cruces and Samples (2016), sovereigns issuing debt under New York law should set a reasonable default rate in their bond contracts to avoid excessive pre-judgement interest liabilities.

Are GDP warrants really all that useful?

Another, less ruinous but still costly state contingent instrument was the GDP-indexed warrant. In principle, by introducing higher payments in high-growth years and low payments in low-growth years, the warrants promised to smooth out debt service ratios and stabilise public finances. In practice, however, as the market penalised its exoticism and illiquidity at the time of the primary issuance, the internal rate of return from purchasing warrants when they first began trading in the market, collecting the coupons paid so far and selling them in November 2015 is an astronomical 35% per year in dollar terms. On first sight, that high rate could be attributed to the lack of familiarity that the market initially had with the instrument. However, Argentina issued GDP warrants again in 2010 and the return on this latter issue has been just the same.

According to a forthcoming book, for each $100 of present value of new instruments that participating bondholders obtained in the 2005 exchange, they took $87 worth of bonds and $13 worth of GDP-warrants (Cruces 2016). However, between 2005 and 2014, Argentina paid $10 billion for its bonds and almost $13 billion for its GDP-warrants. The talk among experienced market participants is that, if Argentina had offered just a fraction of what it paid via the GDP warrants packaged in a classical plain-vanilla bond, it would have achieved a much higher participation rate and would have avoided much of the pain that it has had to endure since 2005. The fancy GDP-warrants were a terrible deal for Argentina.

Minimum participation thresholds and exit consents: Leaving the door open

One tool that is friendlier towards creditors is to only go ahead with the exchange if a minimum participation threshold is attained. Uruguay used this in 2003 and the IMF had asked Argentina to use it too, to no avail. ‘Exit consents’ are another handy device as they enable the creditor to deprive the old bonds of key non-payment terms that mitigate the risks of litigation by holdouts. Curiously enough, an Argentine province, Mendoza, used this in a clever manner in its 2004 restructuring and was thus able to block holdout litigation.

Another smart option is to leave the exchange open after the initial settlement, so that holdouts can accept the exchange retroactively if they repent from their initial decision. To implement this, the debtor can create a trust fund caring for the interest of future tenderers – it would give to this trust fund the same securities given to exchange bondholders and make payments to it as if holdouts had accepted the exchange. Then holdouts could take their share as they decide to join the exchange at a later date.

It is possible to avoid attachments

Vulture funds are very active in trying to obtain attachments of state property, but New York courts have been very respectful of the limitations contained in the Foreign Sovereign Immunities Act of 1976. So, troubled debtors would do well by transferring property of the central government that is used for commercial purposes in the US out of the reach of courts before the going gets tough.

And, above all, stay away from the exotic and be reasonable

There is no need to be radically innovative. Argentina would have likely closed the saga much earlier if it had not overdesigned the offer. Be standard.

And be reasonable, as well. The New York courts, which favoured Argentina in the early parts of the restructuring process, turned bitterly against it when the debtor resisted abiding by their rulings after the 2005 exchange. Later, they overreacted with a pari passu injunction to force Argentina to negotiate, which received widespread criticism from the international community and from affected third parties. However, as Argentina’s new government made a reasonable offer in early 2016, the court again tried to strike a balance between enforcing contracts and facilitating a deal.

Indeed, proving that courts can display this flexibility may be crucial for New York to remain the main issuing site for emerging country sovereign debt, as English courts are known to be more favourable to debtors in dealing with recalcitrant creditors. Of the outstanding stock, about 45% are governed by English law and about 51% by New York law. According to the IMF (2016) Latin American issuers ‘who tend to move together as a group’ account for approximately 74 % of New York law new issuances. God forbid that this business be lost to London!

Ultimately, Argentina’s legal war was highly idiosyncratic, the result of two self-inflicted wounds: an exotic bond issued in April 1998, and the flawed Rights Upon Future Offers and Lock Law approved at the time of the 2005 debt exchange to force creditors to take a deeper cut. The main lesson from the saga? Don’t make the same mistakes.

*About the authors:

Juan José Cruces, Director of the Center for Financial Research (CIF), Universidad Torcuato Di Tella and Professor of Financial Economics

Eduardo Levy Yeyati, Visiting Professor of Public Policy, Harvard Kennedy School; and Professor of Economics and Finance (on leave), Universidad Torcuato Di Tella (UTDT) and Universidad de Buenos Aires

References:

Cruces, J J (2016), “Una república sin buitres: para bajar el costo de invertir en la Argentina productive” (A Republic Without Vultures: To Lower the Cost of Productive Investments in Argentina), Fondo de Cultura Económica, forthcoming.

Cruces, J J, and T R Samples (2016), “Settling Sovereign Debt’s ‘Trial of the Century’”, Emory International Law Review, forthcoming.

Cruces, J J, and C Trebesch (2014), Sovereign Debt Restructuring Haircut dataset.

Edwards, S (2015), “Sovereign Default, Debt Restructuring, and Recovery Rates: Was the Argentinean “Haircut” Excessive?”, NBER working paper.

International Monetary Fund (2016), “Inclusion of Enhanced Contractual Provisions in International Sovereign Bond Contracts”, Briefing for G20 Meeting, 6 April.

Schumacher, J, C Trebesch, and H Enderlein (2014), “Sovereign Defaults in Court”.

Schumacher, J, C Trebesch, and H Enderlein (2015), “What Explains Sovereign Debt Litigation?”, Journal of Law and Economics 58(3).

Endnotes:

1 Absurdly, these astronomical rates result from comparing the secondary market price of the defaulted sample bond with its original contractual cash-flows. It is well-known that defaulted bond prices reflect the expectation of their restructuring value, since the old contractual cash flows have been accelerated, and hence the normal computation of a yield to maturity is senseless. In fact, after the 2005 exchange, Argentine exchange bond yields were closer to 9% per annum.