The Euro As A Social Bond: Why Do Eurozone Citizens Still Back Single Currency? – Analysis

Why despite the pain in the South of the Eurozone and the anger in the North do the majority of the people still support the euro?

By Miguel Otero-Iglesias*

Most analysts believe the Europeans support the single currency because they are scared of the potential consequences of its break-up. As Barry Eichengreen has put it, a unilateral exit of any of the member states of the eurozone would trigger the mother of all financial crises. No wonder nobody dares to leave. However, this interpretation is overly pessimistic. It fuels the view that the eurozone is an inhospitable island from which it is impossible to escape. This is misleading. The euro is popular due to positive factors: because it facilitates economic exchanges and because it is one of the most potent symbols of European integration. The social literature on money argues that currencies are like languages. They help create a sense of community. This paper aims to show that despite (or because of) the recent crisis, the euro might have started this very same process among eurozone citizens.

Analysis

The euro, the common European currency that arrived on the streets of Berlin, Paris, Rome and Madrid, among other European capitals, on 1 January 2002, has just celebrated its 15th anniversary. This is surprising for some. Since its inception many have predicted its demise. However, there is a cognitive gap between how people see the euro from outside and from within the eurozone. Outside, the feeling is that the single currency was a big mistake, is not working and is doomed. Yet, inside, a large majority of citizens, both in the creditor countries to the north and the more indebted countries to the south, are in favour of the euro. What explains this? The usual answer is that people do not want to leave the single currency because of the redenomination costs and a fear of the unknown. Leaving the euro is like jumping into the abyss. Who wants to do that? The perception might be overly pessimistic, though. The euro brings a number of material benefits that are generally overlooked. Furthermore, in its short history it appears that the common currency has generated social bonds and a common identity, underappreciated outside the eurozone.

Indeed, outsiders have an extremely negative view of the single European currency. The list of prominent scholars, especially from the Anglo-American world, who have predicted, or suggested, the break-up of the euro is long, and growing longer by the year. Five years ago, Martin Feldstein –who had already predicted in 1997 that the euro would lead to conflict in the Old Continent– sentenced that ‘the euro should now be recognized as an experiment that failed’.1 Some months later in 2012, when the first Grexit scenario was imminent (there was a second one in 2015), Paul Krugman wrote: ‘Suddenly, it has become easy to see how the euro –that grand, flawed experiment in monetary union without political union– could come apart at the seams. We’re not talking about a distant prospect, either. Things could fall apart with stunning speed, in a matter of months, not years’.2

Last year Mervyn King, the former Governor of the Bank of England, added his voice to the chorus by warning that ‘if the alternative is crushing austerity, continuing mass unemployment, and no end in sight to the burden of debt, then leaving the euro area may be the only way to plot a route back to economic growth and full employment’.3 For the same reasons Joseph Stiglitz believes that ‘it is important that there can be a smooth transition out of the euro, with an amicable divorce… Europe may have to abandon the euro to save Europe and the European project’.4

This negative view of the euro is not only dominant among economists. The political scientist Andrew Moravcsik, one of the world’s leading experts in European Studies, has recently written that ‘fifteen years ago, when the EU established its single currency, European leaders promised higher growth due to greater efficiency and sounder macroeconomic policies, greater equality between rich and poor countries within a freer capital market, enhanced domestic political legitimacy due to better policies, and a triumphant capstone for EU federalism. Yet, for nearly a decade, Europe has experienced just the opposite’.5

This negative view of the euro is not only dominant among economists. The political scientist Andrew Moravcsik, one of the world’s leading experts in European Studies, has recently written that ‘fifteen years ago, when the EU established its single currency, European leaders promised higher growth due to greater efficiency and sounder macroeconomic policies, greater equality between rich and poor countries within a freer capital market, enhanced domestic political legitimacy due to better policies, and a triumphant capstone for EU federalism. Yet, for nearly a decade, Europe has experienced just the opposite’.5

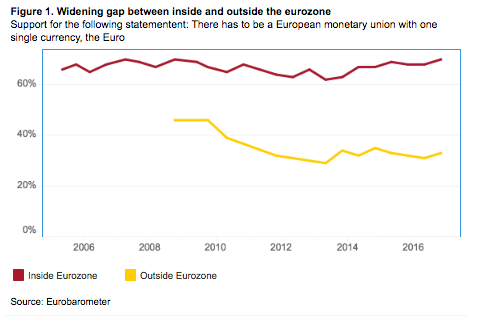

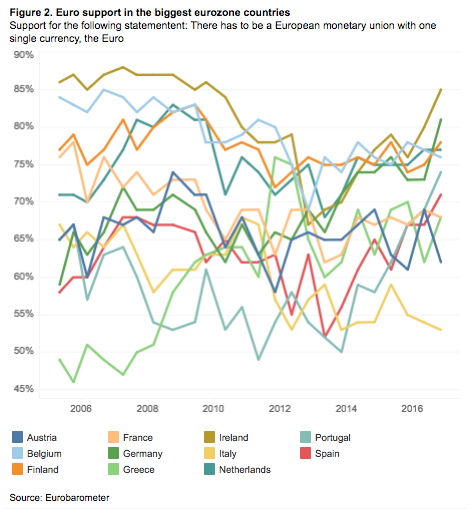

Reading these analyses, and observing the rise of Euroscepticism across the Old Continent, one might be led to believe that the majority of the citizens of the eurozone want to go back to their national currencies. However, the Eurobarometer surveys –the most comprehensive measurement of public opinion in the EU– present a different picture. Support for the single currency among eurozone citizens has been constant over the past 10 years, despite the deep recession (see Figures 1 and 2). It stood at 70% in 2007 before the crisis, it reached a bottom of 62% in 2013 just after the first Grexit scenario, and it has climbed up again to its historic peak of 70% at the end of 2016, the last measurement.6

Reading these analyses, and observing the rise of Euroscepticism across the Old Continent, one might be led to believe that the majority of the citizens of the eurozone want to go back to their national currencies. However, the Eurobarometer surveys –the most comprehensive measurement of public opinion in the EU– present a different picture. Support for the single currency among eurozone citizens has been constant over the past 10 years, despite the deep recession (see Figures 1 and 2). It stood at 70% in 2007 before the crisis, it reached a bottom of 62% in 2013 just after the first Grexit scenario, and it has climbed up again to its historic peak of 70% at the end of 2016, the last measurement.6

Thus, more than two thirds of eurozoners support the single currency and this figure has not changed much over the years. To the contrary, in Greece, the country most affected by the crisis, euro support stood at only 47% in 2005, while 10 years later, in 2015, following the second near-Grexit event, it reached 70%. It seems that the closer the Greeks were to the abyss the more they wanted to avoid it. This stands in clear contrast with the evolution of euro support outside the Eurozone, which in the same timespan fell almost 20 points from 56% to 37%, with massive drops in the Czech Republic (-39 points), Denmark (-25) and Bulgaria (-22). Incidentally, the UK has always been the least supportive country of the euro, at 29% in 2007 and 17% in 2016, the year of the Brexit vote.

These figures confirm the general trend. Outsiders are convinced the euro is a bad idea, while insiders have a more positive view. The disparity leads to the following questions: what explains the euro’s social resilience? What makes people cling to the single currency? Or, looked at from the angle that is usually adopted, why is the euro’s break-up so difficult?

The fear of exiting

The first to have delved into this question was Barry Eichengreen.7 In his much-cited 2007 National Bureau of Economic Research (NBER) working paper he lists the economic, political, technical and legal barriers that any country would have to overcome in order to exit the euro. Starting with the economic ones, Eichengreen explains that a country like Italy –which has accumulated a public debt of 130% of GDP, the world’s third largest in volume terms after the US and Japan– would immediately get credit downgrades and the interest it would have to pay for the next issuance of debt would be prohibitive. Default would be almost impossible to avoid.

Krugman, Stiglitz and others, taking Argentina as an example, believe that a return to national currencies and the consequent devaluations would help the Southern countries of the euro to stimulate internal demand, export more and then quickly regain market access. But Eichengreen is sceptical. As he puts it: ‘would reintroducing the national currency and following with a sharp depreciation against the euro in fact help solve these countries’ competitiveness and debt problems? The presumption in much of the literature is negative’. The competitiveness gains generated by a devaluation of around 25% of the new Portuguese escudo or the Spanish peseta would immediately be offset by creeping inflation, especially if the price of petrol were to rise again above US$100. In order to avoid this, the Government would have to either convince foreign creditors that it is serious about fiscal rectitude (so as to eliminate the spectre of further devaluations) or build an institutional framework that would foster sufficient dialogue between employers and workers to avoid wage increases. A herculean task in these countries.

On top of the economic difficulties, a country leaving the euro would also face negative political consequences. Unless the exit is negotiated in good terms with the rest of the euro partners, the diplomatic backlash would be damaging. The exiting country would be portrayed as a traitor to the European integration project and treated as a pariah, with expulsion from the EU as a real possibility. In fact, legally the only way to exit the euro is by leaving the EU since in the treaties there is no provision to that effect. Other legal obstacles would be to redenominate all the domestic contracts in the new currency and pay international contracts and debts and loans signed or issued overseas denominated in euros in a currency that would be much weaker.

Finally, there would also be the technical difficulties of introducing a new currency (a process that can take years) and the prior introduction of capital controls to avoid capital flight and the collapse of the banking system. In the recent euro crisis, capital controls were introduced in Cyprus and Greece in a relatively smooth manner, but this only occurred because the two countries decided to stay in the euro. The current capital controls would create much greater disruption should the exit from the euro be imminent, especially if the decision to exit is not previously backed by a legitimate democratic mandate, either by being part of the electoral programme of the Government or via a binding referendum. As Eichengreen suggests, all these obstacles mean that an exit would trigger the mother of all financial crises. No wonder, therefore, that people in the eurozone do not want to leave the single currency.

The social glue of the euro

Eichengreen’s analysis gives support to those that think that the main reason why the euro membership is still intact is because of fear. The governments and the people are so scared about the possible consequences of breaking up the single currency that they are willing to suffer the euro’s straitjacket. But perhaps this perception is too negative. People might want to stay in the euro because they see positive aspects in it too. Despite the recession, many citizens in the south of the eurozone are convinced that the EU and the euro offer stability. Their discontent with EU institutions has increased in the aftermath of the crisis, but trust in their national institutions is even lower. They find that the problems in their economies are not due to the euro, but rather of a domestic nature. One should not forget that countries like Portugal, Spain and Greece are relatively new democracies (they were dictatorship until the 1970s) with an institutional framework less robust than that of the eurozone’s core countries.

For many citizens of the south, membership in the rich club of the eurozone secures high living standards and democratic rule. On the other hand, higher levels of inequality and corruption and an underdeveloped civil society make many of them believe that if they were to abandon the euro, and possibly the EU, the extractive elites of their countries would have even more unfettered power. In this regard, the euro functions as a straightjacket for society as a whole, crucially also for the elites who are now constantly monitored by Brussels. As the Spanish sociologist Pérez-Díaz has pointed out, with the euro, Spain has imitated Ulysses’ strategy of tying himself to the mast. He also makes another important point. The weaker a country becomes in the international arena, the more it clings to the euro.8 This happened to Greece and Spain, and it is likely to occur to Italy and France. As the old saying goes: the euro was created for two types of countries: those that are small and those that do not yet know that they are small.

The stability of the euro is a feature that cannot be emphasised enough. Before the single currency, most people with a certain amount of wealth in the southern countries of the Eurozone would stash away around 30% of their money in a hard currency (dollars or Deutsche Marks, for example), if possible overseas. The same trend returned in 2011 and 2012 at the peak of the euro crisis when redenomination risks were high, and it receded after July 2012 once Mario Draghi, backed by Angela Merkel, said that the ECB would do ‘whatever it takes’ to support the single currency. The euro’s value has remained relatively stable despite undergoing an existential crisis. Spanish and Portuguese pensioners know how to value that, and the same goes for businessmen and women who do not need to fear devaluations, and the middle class tourists of these countries who have now a hard currency that they can use all over the world like their German and French peers.

The price stability that the euro offers is obviously also valued in the north of the Eurozone. There the euro might not be seen as an anchor of democracy as in the south, but the elimination of exchange-rate risks and transaction costs are on their own a great advantage. Before the single currency, German and Dutch exporters would always fear that the forthcoming devaluation of the lira or the franc could ‘unfairly’ help their Italian or French competitors. Equally, if they travelled south as tourists they would always be afraid of overpaying given that they had to pay, and mentally count, in another currency. These concerns are now eliminated. The euro just makes life simpler. Furthermore, apart from these transactional and functional advantages, many in the North, and the South, are proud to use a common currency. Consciously or subconsciously they know that it represents the coming together of different countries with different languages and cultures, and with a bloody past that should not be repeated.

In this regard, it is important to analyse money not just as an economic phenomenon but also as a cultural and sociological one. As Eric Helleiner has pointed out, currencies can foster a common identity in many different ways, even if they are not loved.9 Thus far, research on the social and identity impact of the euro is underdeveloped, but those that have investigated the phenomenon, such as Giovanni Moro and his co-authors in the ‘The Other Side of (the Euro) Coin’ project, have no doubts that ‘people living in the Eurozone (whether it be a lucky or unlucky condition) are citizens of the EU in a way that is different from that of their fellow citizens of non euro EU countries’.10 This is one of the reasons why outsiders have such difficulty in understanding the insiders. The daily use of euro notes, for instance, is transformed in a repeated and standardised pattern that is common to all eurozone inhabitants. The euro has created a common code. By being the unit of measurement for a number of social facts and relations it has become ‘a medium of meaning’. As Moro points out, ‘in a Union characterized by the “poligamy of languages”, the euro is the only existent common language’.

This common language and symbolism not only operates internally but also externally. It is interesting to see, as Kathleen McNamara highlights, that ‘the € symbol has come to signal the EU’s de facto logo, recognizable from afar and universally readable in any language. Note that very few currencies have their own widely recognized graphic symbol or currency sign: The British pound (£), Japanese yen (¥), and US dollar ($), and now the euro (€)’. Thus, ‘the value of the euro against other currencies has become another standardized, numerical focal point representing Europe, offering an external face of a consolidated Europe to the world’.11 Many Eurozone citizens might feel some pride in this.

Thus, from a social point of view, money functions like a language. It brings people closer and creates a sense of community because the citizens that share a common currency experience monetary phenomena such as interest rates, depreciation and appreciations together. Over time, this creates a bond. The work of Helleiner is relevant again here. In his view, the feeling of being in the same boat ‘appears to be particularly noticeable in situations in which the collective monetary experiences are of a quite dramatic nature’. In some of these cases, the ‘speculative attacks on the national currency are often portrayed in militaristic terms as an attack on the national community as a whole’. The debt crisis in the eurozone was certainly such a dramatic, even existential moment, which affected everyone within it. Throughout the crisis many eurozoners, leaders and citizens alike, felt they were under fire from financial market speculators based in London and New York. Coincidentally in 2010, when the Greek crisis broke out, the late Tommaso Padoa-Schioppa summarised the general feeling by using the military metaphors suggested:

‘A mighty army has advanced on the citadel of the European currency with the cry: “It will never work!”… The besiegers were thousands… Their reasoning was as follows: the euro area is not a political union and can never become one… The citadel, therefore, is doomed to capitulate. Equally strong and simple was the credo of the defenders, who countered: “It can work!”.’12

Helleiner also highlights that although certain people might strongly disagree about how a particular currency is managed and therefore for them the collective monetary experience of the eurozone crisis might not foster a sense of positive allegiance, these same people would nonetheless have to recognise that the value of their currency is dependent on the trustworthiness of the authority issuing it and on the fellow citizens using it. ‘This dependence, in turn, may have helped to contribute to a greater sense of belonging to, as well as to greater faith in’ the Eurozone community, for instance. This would particularly be the case when the currency in question remains ‘reliable as a medium of exchange and stable in value over time’, as has been the case with the euro. As mentioned above, the social effect of the relative stability in the euro’s value throughout the crisis is a very important aspect. As Helleiner reminds us, ‘Simmel, for example, suggested that stable money can become a powerful symbol of trust and social stability because of its certainty as a measure of value. In a chaotic and changing world, it can seem a constant and stable reference point over time’.13 Arguably, the euro has performed this anchor role throughout the crisis.

Hence, if one takes the social literature on money, it becomes clear that over the past years the euro might have helped develop a sense of community in the eurozone. Not only because people share a common language when they calculate value, but also because they have experienced a number of (in some cases traumatic) phenomena together. Incidentally, a comparative study by Thomas Risse and his collaborators of parliamentary discourses and media coverage in the different eurozone countries shows that the public opinion agendas at specific moments of the euro crisis were very similar. This creates bonds, even if there are disagreements. From this point of view, ‘Controversies about European policies and the subsequent politicisation of the EU are good, not bad for the sense of community and for construction of a European polity’.14 Furthermore, the resilience of the euro’s value in the midst of an existential crisis such as that undergone in the eurozone between 2010 and 2012 might have strengthened the trust in the common currency, not only in the South, used to weaker and more unstable currencies, but also in the North, where people have always feared that the euro would become a weak currency. Eurobarometer data show eurozoners have a stronger European identity than those outside. The euro might not be the only reason, of course. But it is true that those that favour the euro also tend to feel more European.

Conclusion

The economic, political, technical and legal constraints identified by Eichengreen and others might partly explain why a majority of eurozoners want to keep the single currency. But they imply that they do so because the costs of leaving are too high. This is a negative, constraining, approach. By focusing more on the social aspects, in particular how the euro functions as a common language, observers both outside and inside the monetary union might find more positive elements that explain why people might actively want to continue using the single currency despite the pain in the South and the anger in the North. Citizens in the eurozone are certainly not in love with the euro, but they find it so convenient and a fact of life, especially the younger generations, that they do not want to go back to the old national currencies.

About the author:

*Miguel Otero-Iglesias, Senior Analyst, Elcano Royal Institute | @miotei

Source:

This article was published by Elcano Royal Institute.

Notes:

1 M. Feldstein (2012), ‘The failure of the euro’, Foreign Affairs, January/February.

2 P. Krugman (2012), ‘Apocalypse fairly soon’, The New York Times, 17/V/2012.

3 M. King (2016), ‘“Forgive their debts” is not the answer’, The Telegraph, 28/II/2016.

4 J. Stiglitz (2016), ‘A Split euro is the solution for Europe’s single currency’, Financial Times, 17/VIII/2016.

5 A. Moravcsik (2016), ‘Europe’s ugly future’, Foreign Affairs, November/December.

6 See Eurobarometer standard series.

7 B. Eichengreen (2007), ‘The Breakup of the Euro Area’, NBER Working Paper, nr 13393, September.

8 V. Pérez-Díaz (2013), ‘Between the natural and moral order of things: the euro and the problem of agency’, in G. Moro (Ed.), The Single Currency and European Citizenship, Bloomsbury, New York.

9 E. Helleiner (1998), ‘National currencies and national identities’, American Behavioral Scientist, vol. 41, nr 10.

10 G. Moro (Ed.), The Single Currency and European Citizenship, Bloomsbury, New York.

11 K. McNamara (2015), The Politics of Everyday Europe, Oxford University Press, Oxford.

12 T. Padoa-Schioppa (2010), ‘Euro remains on the right side of history’, Financial Times, 13/V/2010.

13 Helleiner (1998), op. cit.

14 T. Risse (2014), European Public Spheres: Politics is Back, Cambridge University Press, Cambridge.

Europeans back the euro because they don´t like admit they made a mistake, and see badly any move backwards in european integration out of fear it may led all the way back to european disintegration and back to war in the continent.

The true future is of course the middle ground. Disintegration of the euro into several different euro national currencies (the same way Nordics have different krona, and English speaking countries have different dollars [Australian, new Zealand, Canadian, and so on].

Its important to admit europe is not ready YET for the use of single currency, but divide into several currencies with the same name (Euros) shows the world the commitment of working together, plus the continue existence of a euro council were countries cooperate and work to keep those currencies as close to each other as possible.

It also keep Europeans together into currencies with the same name (which is psychological very valuable).

All this must be done in mind of a future single currency once/if europe gets to be ready for such a thing.