The Distribution Of Wealth In America, 1983-2013 – Analysis

By John C. Weicher*

Wealth is one of the most important measures of economic well-being, but also one of the most difficult to measure. Transactions for some types of wealth, such as stocks and bonds, occur very frequently at prices which are readily available, and provide a current valuation; transactions for other types, such as owner-occupied homes, occur much less frequently and the value of the home is not easily measured in between transactions. In addition, shares of stock in a specific corporation are identical; the sale of any 100 shares establishes the value of all shares. By contrast, homes can differ widely; the sale of one three-bedroom, two-bath home does not establish the market value of all such homes even in an area as small as a city block. Research on wealth has been limited by these and other differences, despite extensive and serious efforts by numerous economists and other analysts.

In 1983 the Federal Reserve board began to sponsor a survey of household wealth, the Survey of Consumer Finances. The SCF has been conducted every three years since then. The 2013 survey is the most recently completed; the 2016 survey is underway at present and will become available late in 2017. The SCF contains the most detailed information available about the wealth of American households. It consists of detailed interviews with several thousand households. Some are chosen randomly from the population, while others are selected because they are expected to be households with high wealth. Each household is asked several hundred questions about its assets and its debts, and also about its demographic and other economic attributes. The typical interview last about 90 minutes, but some are substantially more than three hours.

Much of the research on wealth has focused on its distribution – the extent to which wealth ownership is concentrated among a small number of households, and whether it is becoming more or less concentrated over time. This has been true since the first SCF in 1983, and indeed before then using other data. The distribution of wealth in the United States is more concentrated than the distribution of income, as reported in the Current Population Survey conducted yearly by the U.S. Bureau of the Census. Also, the distribution of income has become increasingly more unequal since about 1969. It is natural to expect a similar change for wealth, but that need not necessarily occur.

This study uses the surveys since 1983 to analyze the changes in the distribution of wealth. There are some differences between the 1983 survey and the surveys from 1989 to 2013, so some of the analysis is based on the shorter period.

Wealth and Income

The term “wealthy” is often used indiscriminately to refer to people with high incomes as well as people with high wealth. For that reason, it is essential to make clear the distinction between wealth and income. Wealth is a stock and income is a flow. For any particular household at any particular time, wealth is the value of the total assets it owns, minus the total amount of its debts. Wealth is synonymous with net worth. Income is the money that a household receives over a given period of time, reported most commonly for a calendar year.

Some assets yield income – stocks have a value and pay dividends. But some important assets do not have an income counterpart. Owner-occupied homes are the most valuable asset for many households, and for all U.S. households combined, but they do not produce income. Conversely, wages and salaries – income from working – is the most important category of income, but it does not have a wealth counterpart. It is therefore quite possible for high-wealth households to have low incomes, such as elderly homeowners who are “house poor,” and similarly for doctors or lawyers or other professionals to start their careers at a good salary but have little in the way of assets – just a checking account and a car (and perhaps a loan on the car). It is also possible for the income and the wealth of a household to change in opposite directions, at least for some time.

American Wealth Over Three Decades

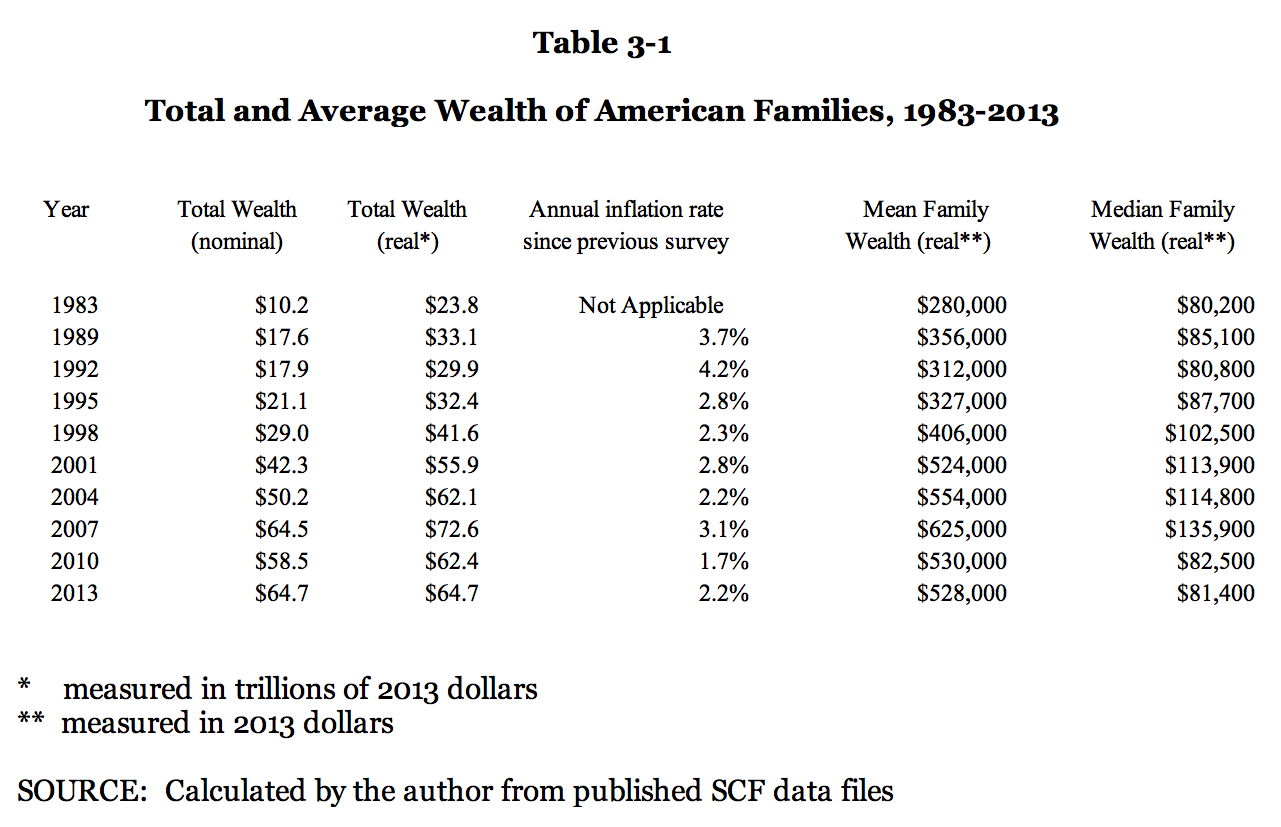

Household wealth in the U.S. increased rapidly between 1983 and 2007. In real terms (throughout this study values are expressed in 2013 dollars, unless otherwise specified), total wealth tripled (from $24 trillion to $73 trillion); average wealth per household more than doubled (from $280,000 to $625,000); and median household wealth increased by 70 percent (from $80,000 to $136,000). Then the Great Recession and the subsequent weak recovery brought about abrupt reversals: total wealth dropped from $73 trillion to $62 trillion by 2010 with a slight increase to $65 trillion by 2013; average wealth per household dropped to $528,000 by 2013, and median household wealth dropped to $81,000 – almost the same as in 1983. This experience is unlike the aftermath of other recent recessions, during which a decline in wealth was temporary, and quickly reversed.

The Changing Composition of Household Wealth

The SCF disaggregates assets into financial and nonfinancial categories. Throughout the three decades, nonfinancial assets comprised the larger share of net worth, but financial assets were an increasing share. In 1983, nonfinancial assets amounted to 72 percent of net worth; by 2013 they amounted to 54 percent. Throughout the period, the most widely held assets were transaction accounts, vehicles, owner-occupied homes, and retirement accounts, in that order. Over 85 percent of households had transaction accounts (90 percent from 1998 through 2013); about 85 percent owned vehicles (rising from 84 percent in 1989 to 87 percent by 2007 and declining to 86 percent by 2013) about 65 percent owned homes (rising from 64 percent to 69 percent in 2004, then dropping to 65 percent by 2013); over 35 percent had at least one retirement account in 1989, rising to about 50 percent by 1998 and remaining at about that level through 2013. The most common liabilities were credit card balances, home mortgages, and car loans; the first two were held by between 38 and 48 percent of all households, the last by 30 to 35 percent. Through 2010, home equity constituted the largest share of total household wealth, privately-owned businesses the second largest (proprietorships, partnerships and closely held corporations whose stock was not widely traded), and retirement accounts a steadily growing third. In 2013 the value of unincorporated businesses slightly exceeded home equity. Home mortgage debt was by far the largest liability, between two-thirds and three-quarters of all household debt.

The growth in retirement accounts was paralleled by increasing ownership of stocks, both directly and indirectly held. In 1989 there were two major household assets, owner-occupied homes and closely-held businesses, which together accounted for about half of total household wealth, even subtracting mortgage debt. By 2001, the total value of stockholdings was larger than either, and amounted to almost a quarter of household net worth; together these three asset categories constituted over 60 percent of household wealth, and continued to do so through 2013.

Changes in the Distribution of Wealth, 1983-2013

The distribution of wealth, and also of income, can be measured by describing the entire distribution (the Gini coefficient) or by measuring the concentration at the high end of the distribution, such as the richest one percent or 10 percent (the concentration ratio). The Gini coefficient is calculated by ranking households from the poorest to the richest, and measuring the cumulative share of total wealth owned by the corresponding cumulative share of all households. If the distribution of wealth is perfectly equal, the Gini coefficient is zero; if all wealth is owned by one single household, the Gini coefficient is unity.

From 1992 to 2007, the distribution of wealth became slightly more unequal by either measure. The changes from one survey to the next were not statistically significant, but the cumulative change was large enough that there was a statistically significant increase in inequality over several surveys, for example 1998 to 2007. There was an increase in wealth across the full distribution; both rich and poor became wealthier.

In the Great Recession, this pattern changed. Rich households and poor households and those in between became poorer. The rich were less affected: the richest 10 percent lost about seven percent of their wealth, while the remaining 90 percent lost about 22 percent of theirs. During the weak recovery after 2009, the distribution of wealth continued to become more unequal. In 2007, the richest 10 percent of U.S. households owned over 71 percent of total household wealth; in 2013 they owned almost 75 percent.

This experience contrasted with the period between 1983-1992. The distribution of wealth became insignificantly more unequal during the expansion that began in 1983, but it became more equal again during and immediately after the 1990-1991 recession. In 1992 the concentration of wealth was about the same as in 1983. The 1983 survey was different from the later surveys in various ways, so comparisons with later surveys are not precise, but it is clear that the experience during and after the 1990-1991 recession was quite different than the experience during and after the Great Recession.

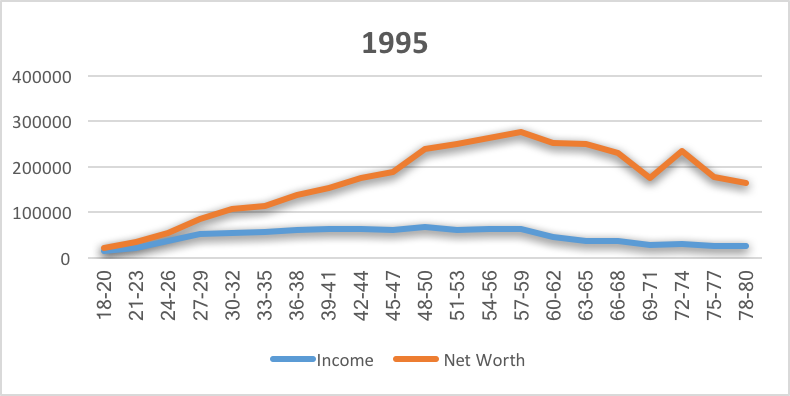

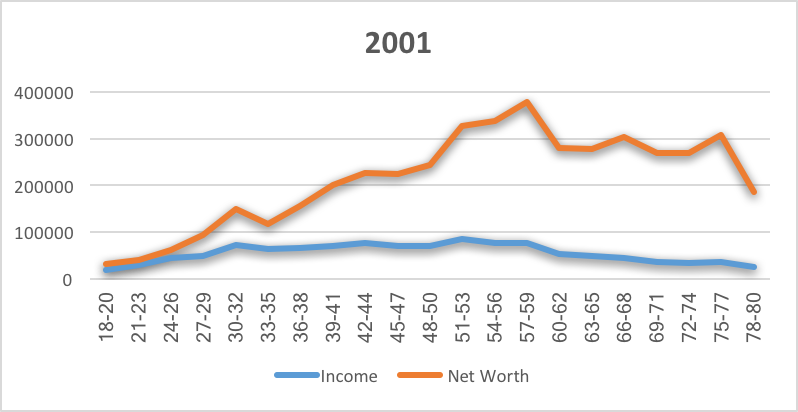

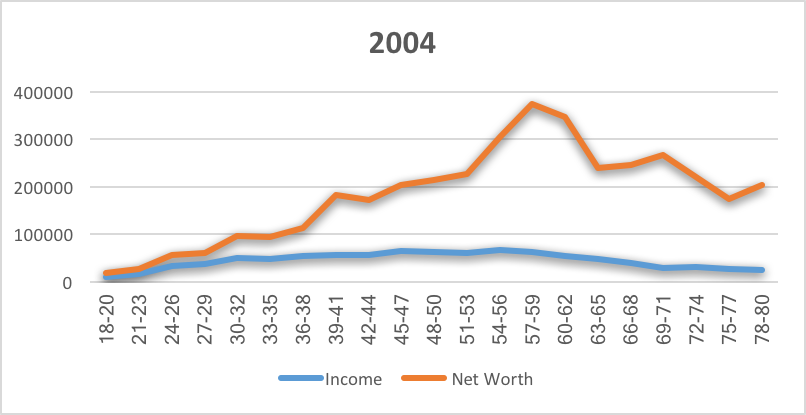

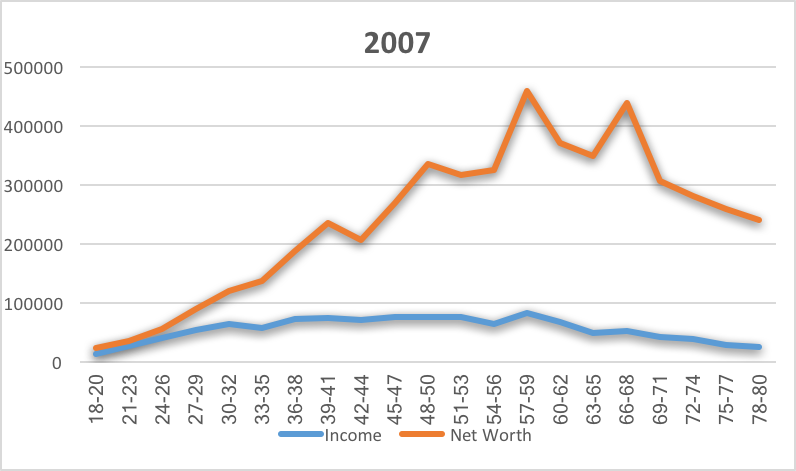

Wealth is much more unequally distributed than income, partly because it is more closely connected to age. Young adults typically start with a salary, a checking account and a car. Over time, their income rises, and they also add to their assets, commonly starting a retirement account and buying a home. Their wealth is likely to increase more rapidly than their income, and continues to do so as they get older. Income has generally been highest for households in their late 40s to late 50s, in the range of $75,000 to $85,000; wealth has generally been highest for households that are about 10 years older, and is in the range of $225,000 to $300,000. This difference usually continues into retirement, until households start to draw on their wealth for living expenses. Age is the most important factor for analyzing the distribution of wealth, although certainly many other factors matter as well.

How Come?

Several asset and liability categories stand out as contributors to the difference between the experience during the 1980s and the experience during the Great Recession. The category with the most notable difference, and also with the greatest change during the recession and its aftermath, was owner-occupied housing. During the unprecedented peacetime inflation between 1965 and 1982, the real value of financial assets dropped dramatically and the demand for real assets rose sharply as households sought protection against inflation. The most widely held real asset was owner-occupied homes. The homeownership rate rose from 62.9 percent in 1965 to a then-record 65.6 percent in 1982, a very large increase by historical standards. Then as the inflation rate dropped during the 1980s, homeownership decreased and real home prices fell. During and after the 1990-1991 recession, homeownership was stable and real house prices declined slightly. In contrast, homeownership and house prices rose strongly during the 20014-2007 expansion, while since 2007 both have fallen.

Home equity is by far the most important asset for middle-wealth households, and they have been the hardest hurt. Their homeownership rate dropped by more than 10 percentage points in six years. For those who kept their homes, their equity fell by nearly 50 percent, and their total wealth by about 40 percent. The homeownership rate was stable for the richest 30 percent, and while their equity dropped, the decline was less than for those in the middle. The decline in homeownership and home equity was the biggest factor in the increase in inequality.

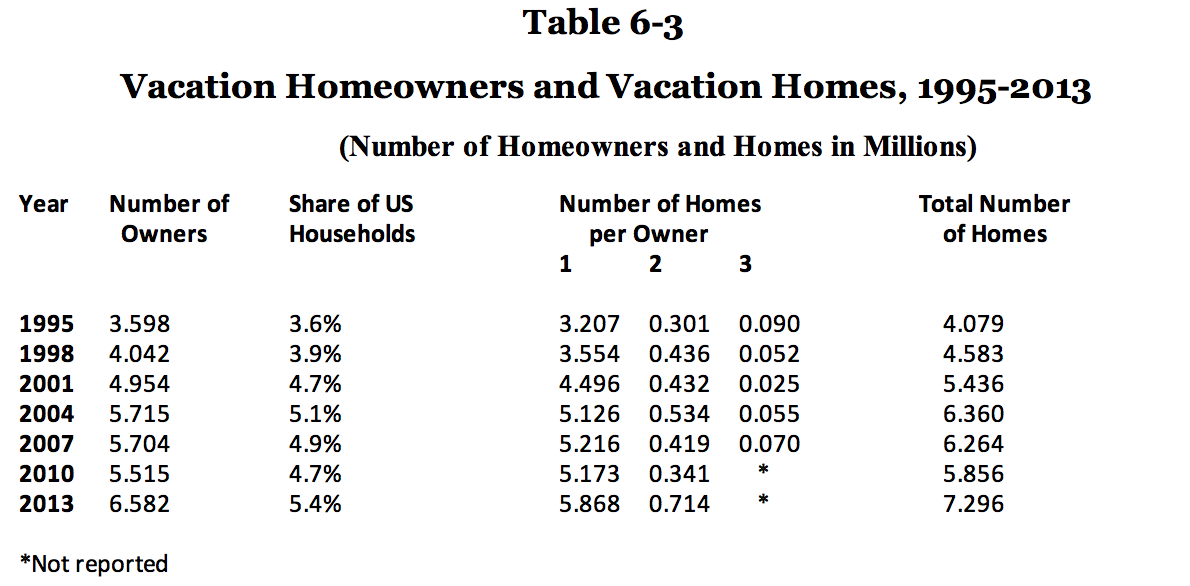

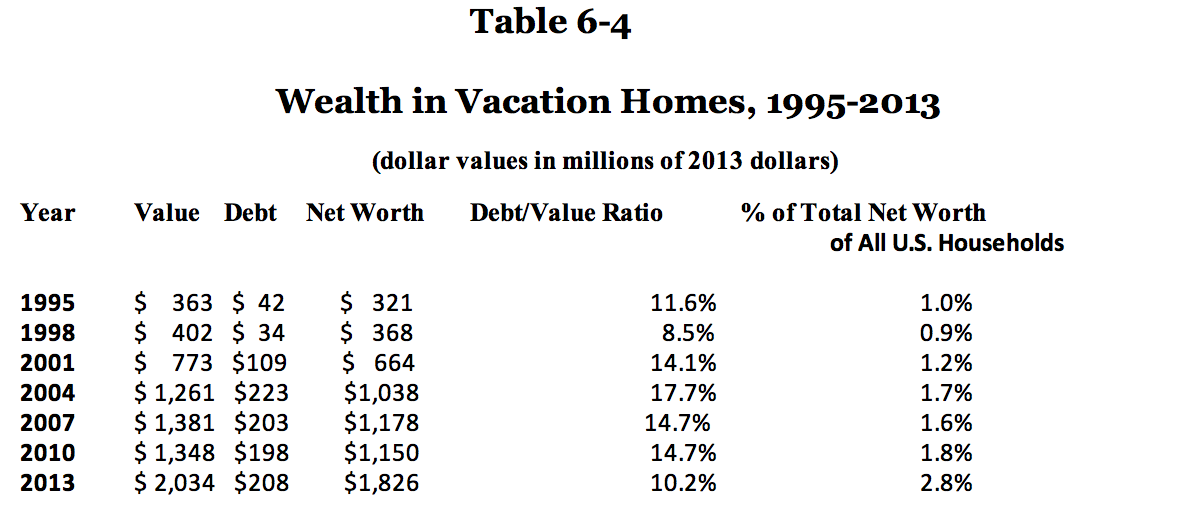

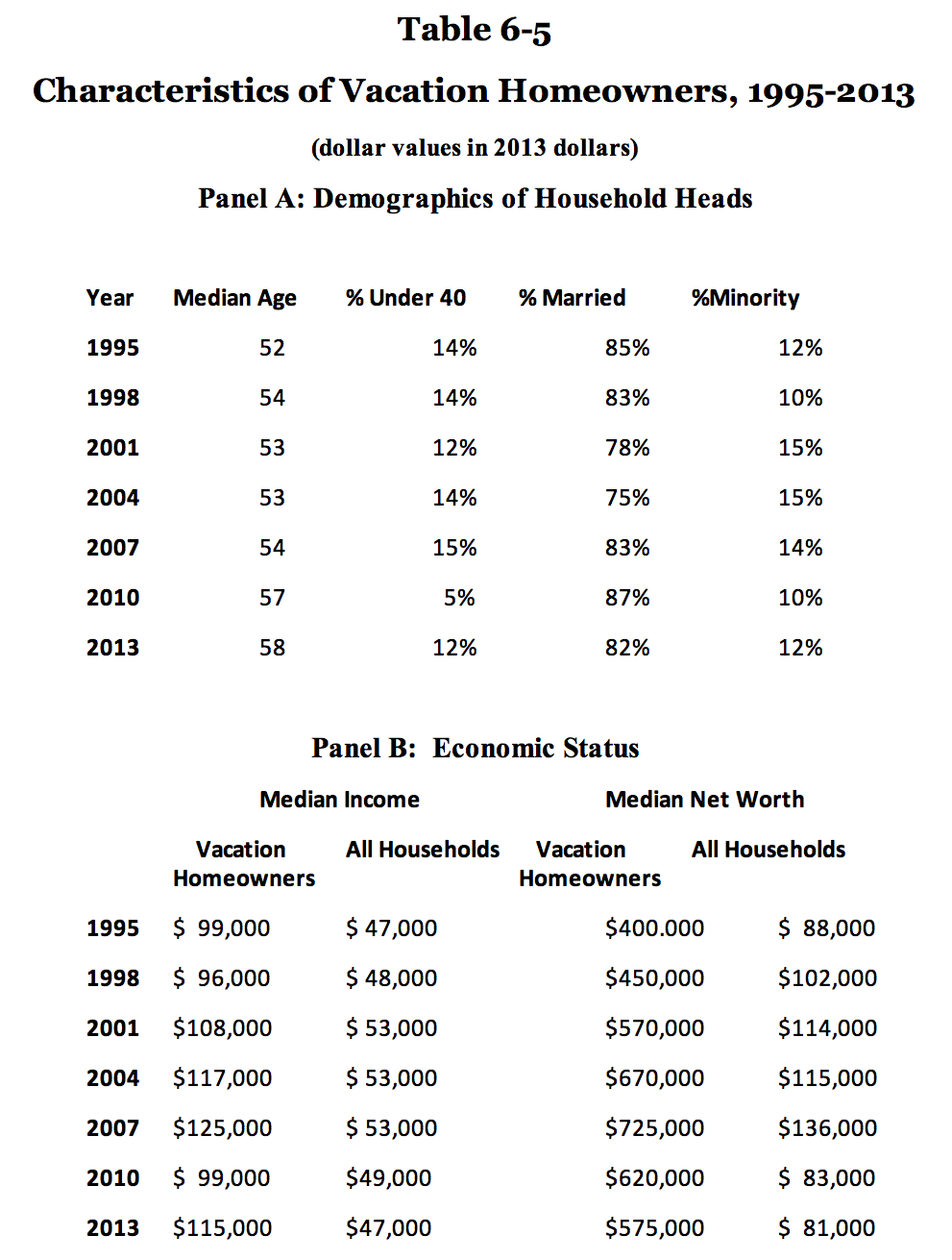

At the same time, the market for second homes – vacation homes – was strong, particularly after 2010. There were one million more vacation homeowners in 2013 than three years earlier, and they owned 1.4 million more homes. Their vacation home equity increased by over 50 percent. Vacation homeowners were wealthier than most households to begin with, and became somewhat more so.

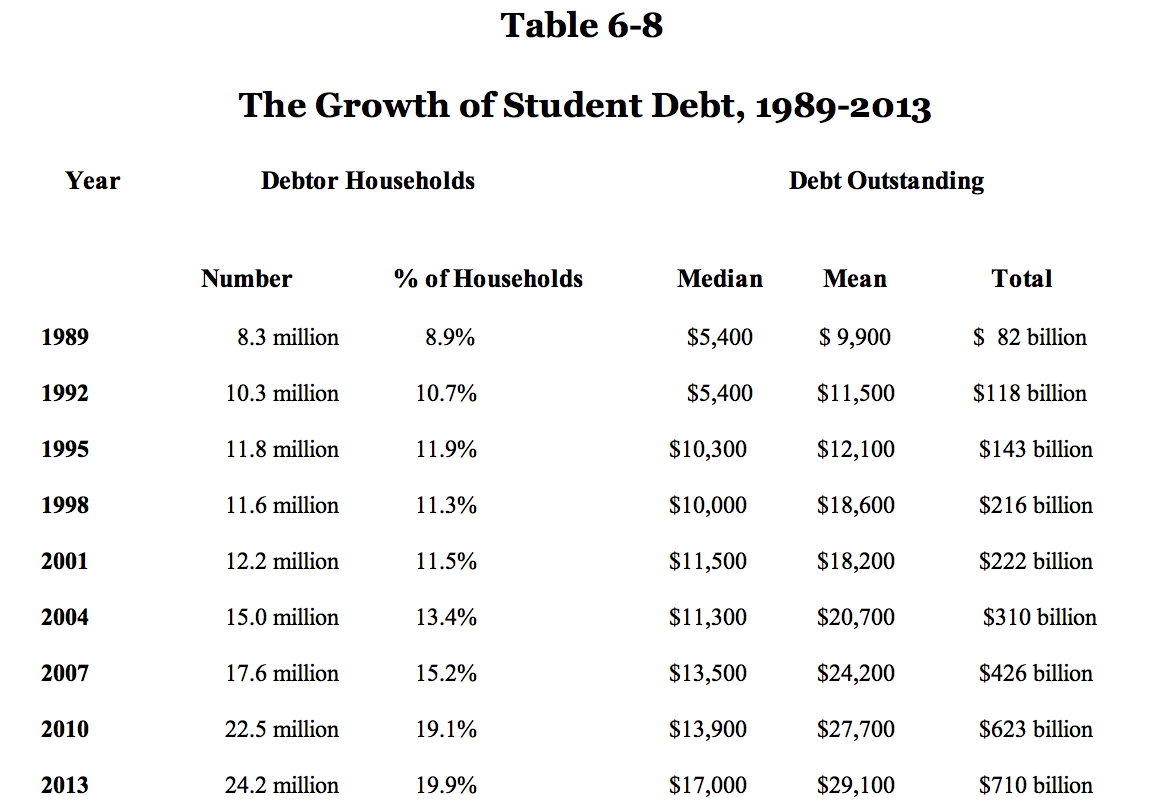

Student debt increased through recessions and recoveries, also contributing to a more unequal distribution of wealth. In 1989 there were eight million households (nine percent of all households) where someone had a student loan, and their total education debt was about $82 billion. By 2007, there were 18 million households (15 percent) with a total debt of $426 billion; by 2013, there were 24 million (20 percent) with a total debt of $710 billion. In 2010, total outstanding student debt exceeded the total value of car loans, and also exceeded total credit card debt. Most student debt is owed by households in the lower half of the wealth distribution, and most are relatively young; the median age for the head of household with student debt has consistently been about 35. Most have a low net worth, partly because they are young and partly because they have student debt. The Great Recession had a substantial impact on these debtors; the median wealth of households with student debt dropped from $43,000 in 2007 to $15,000 in 2013. About 20 percent had a negative net worth in 2007 because their student debt exceeded the aggregate total of all their assets and all their other debts. By 2013, the proportion was about 30 percent.

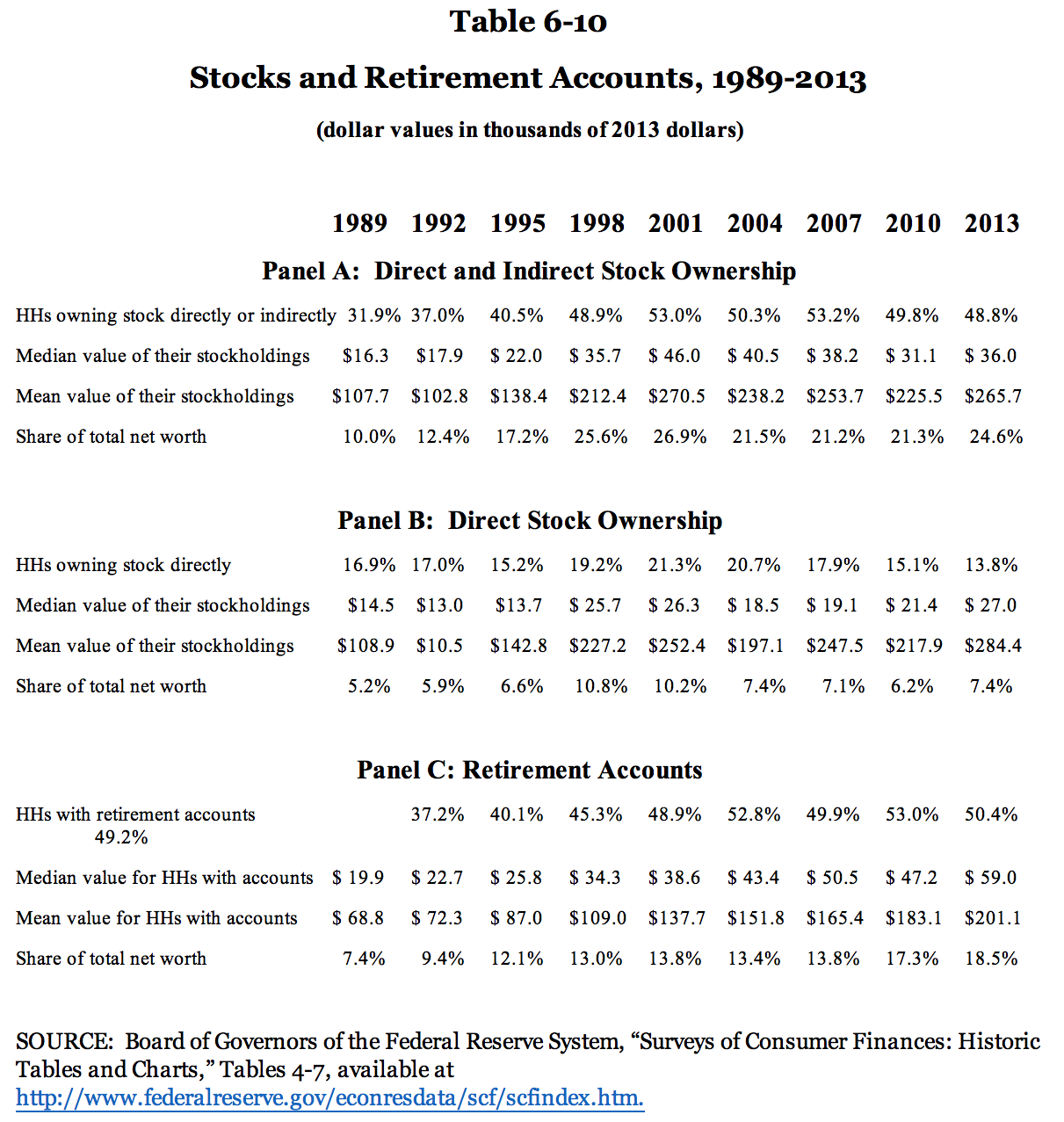

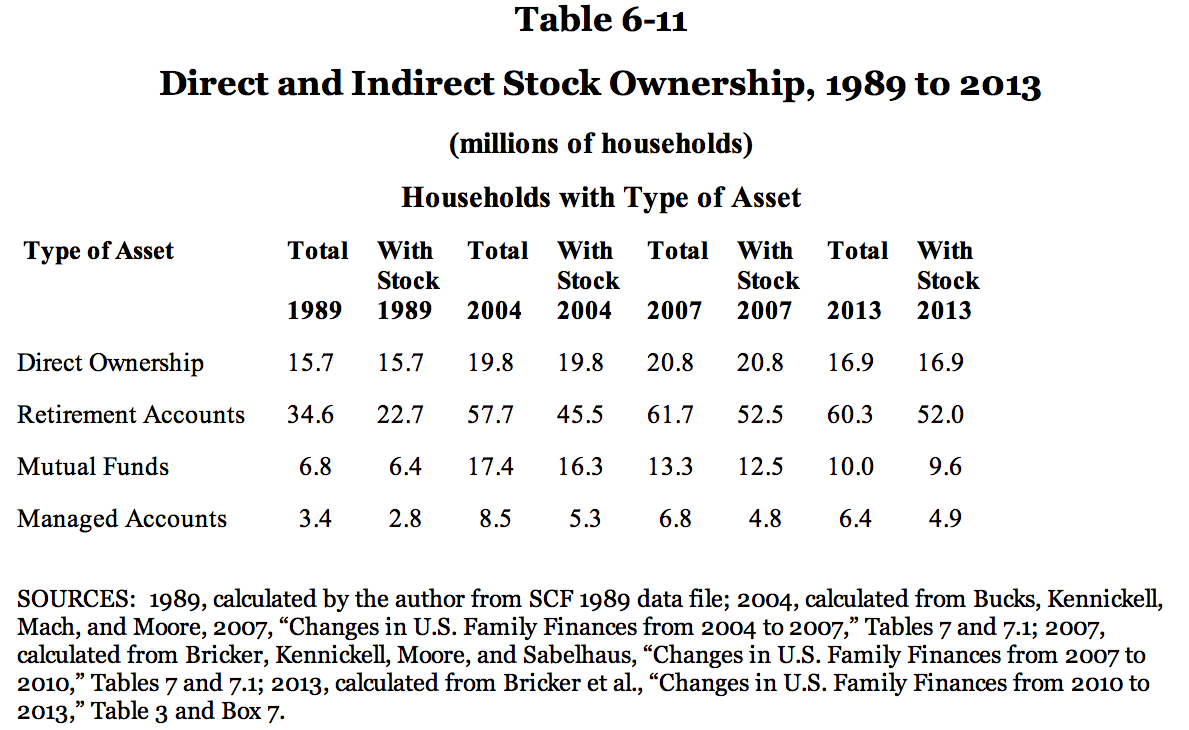

The steadily growing proportion of households with retirement accounts might be expected to promote a more equal distribution of wealth. About half of all households had retirement accounts by 1998, and that has been true ever since. The same is true for stocks; since 1998 about half of all households have owned stocks, either directly or indirectly – through mutual funds, trusts and annuities, but most importantly through retirement accounts. As of 2013, 87 percent of households that owned stocks did so through their retirement accounts; only 28 percent owned stocks directly, and the percentages were smaller for other forms of ownership.

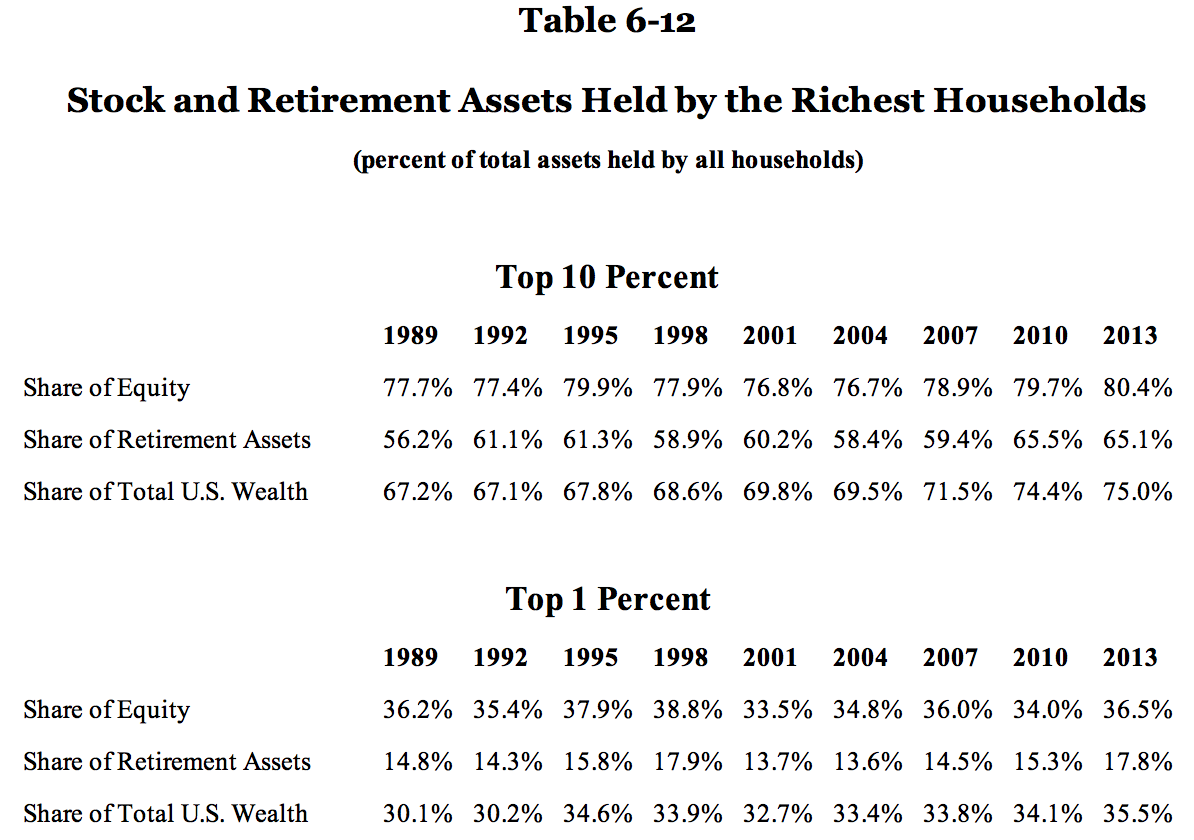

Although half of all households have retirement accounts, the accounts owned by the richest households have consistently had a large share of the assets, and their share increased during and after the Great Recession. Between 1992 and 2007, the retirement accounts of the richest 10 percent of households consistently held about 60 percent of the total value in all accounts. As of 2007, their share was 59 percent. By 2010, their share had risen to 65 percent, and it remained at that proportion in 2013. This was less than their share of total net worth. Retirement assets have not been as concentrated among the richest households as has total wealth and thus it is correct to say that retirement accounts have contributed to a more equal distribution of wealth; but since the Great Recession retirement assets have become more concentrated among the rich.

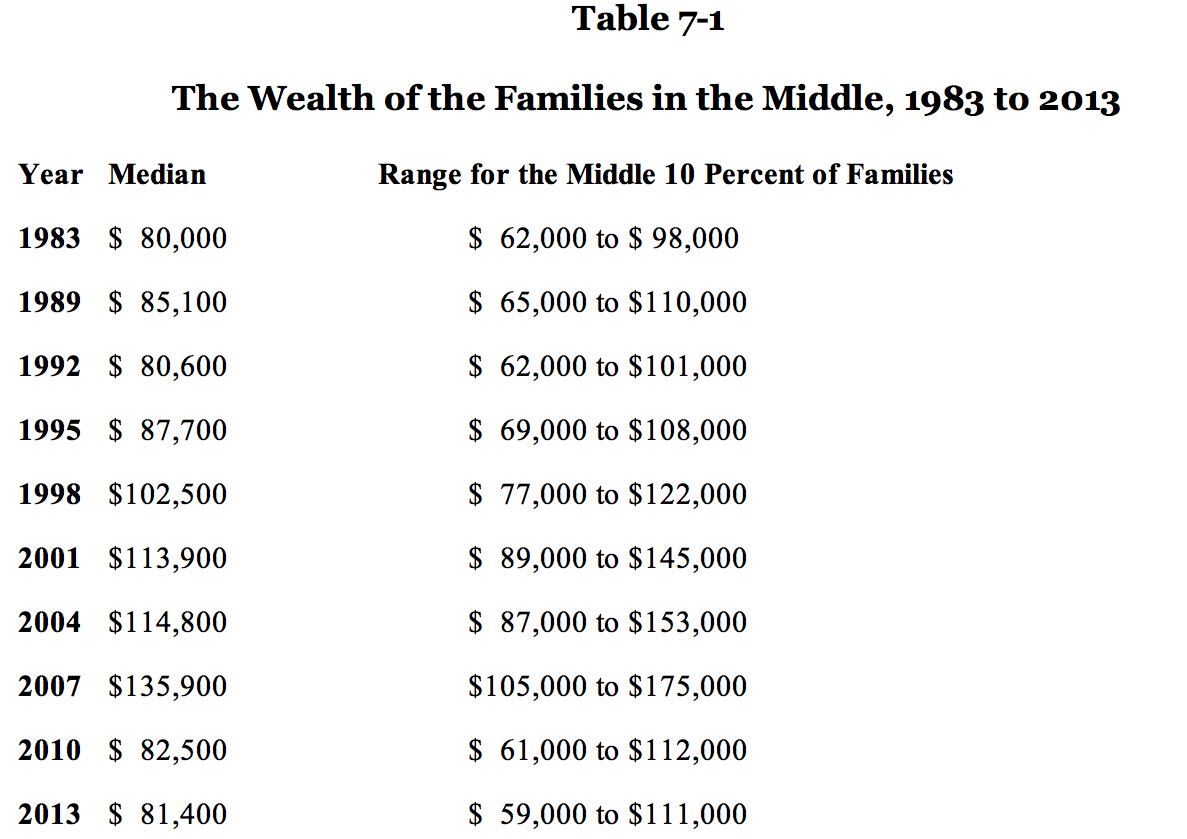

The Families in the Middle

The changes within these various asset and liability categories affected the families in the middle of the wealth distribution – typical American families. There has been relatively little research attention given to the families in the middle. They deserve more attention. As mentioned above, real median household wealth was about $80,000 in 1983, rising to about $136,000 by 2007, and then dropping to $81,000 in 2013. There was hardly any difference between 1983 and 2013; but there was a horrendous loss of 40 percent during the Great Recession and the weak recovery.

This was essentially the experience of families around the median – the middle 10 percent, those whose net worth was between the 45th and the 55th percentile of the wealth distribution. In 2007, the wealth of these families ranged from about $105,000 to $175,000. In 2013, in 2013 the range was between $59,000 and $111,000. Thirty years earlier, the range had been very similar, about $62,000 to $98,000.

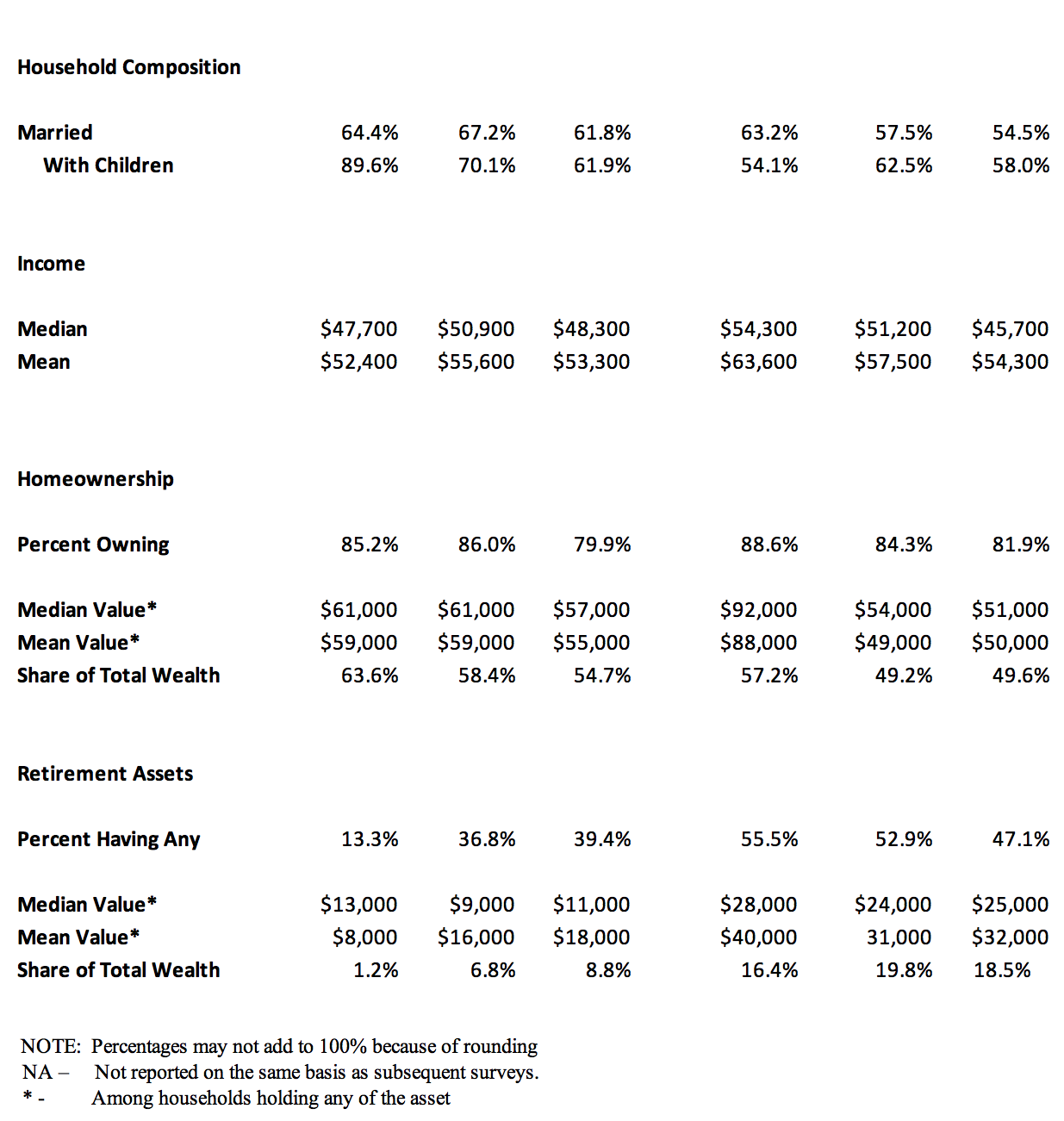

The families in the middle were certainly not the same families in 2013 as they were in 1983, but they were largely the same sorts of families. They were mostly middle-aged, mostly married couples, and if married mostly with children living at home. The real median income of these families was about $48,000 in the earliest survey, peaked at about $54,000 in 2007 and declined to about $46,000 in the latest one – much the same pattern as their wealth. In both years, their income was higher than the median for all households reported by the Census Bureau. One possible contributor to the drop in income between 2007 and 2013 may be that unemployment was higher among the families in the middle. There was no working adult in about five percent of the families where the head of the household was under 65 in 2007; in 2013, about 10 percent did not have a working adult.

It was not particularly noticeable to the public that typical families in 2013 were essentially no wealthier than typical families had been in 1983. Even if the families in the middle in 2013 were the children of families in the middle in 1983, it would not have been obvious to them. Actual prices more than doubled over those three decades: $35,000 in 1983 dollars had the same purchasing power as $82,000 in 2013. Also, most middle-wealth homeowners probably would have had to estimate the value of both the home their parents lived in back in 1983 and the home they owned in 2013.

But the 40 percent decline in wealth between 2007 and 2013 was certainly noticeable, and noticed. About 90 percent of the families in the middle owned a home in 2007, and their equity in their home was about $92,000. This was two-thirds of their wealth. By 2013, only about 82 percent owned a home, and their equity had been cut almost in half, from $92,000 to $51,000. The drop in the value of their home accounted for about 85 percent of the decline in their net worth. Something similar happened to their retirement accounts. In 2007 about 55 percent had accounts, with an average value of $40,000. In 2013 only 47 percent did, and the assets in their accounts were about $32,000, accounting for about 13 percent of the decline in their wealth.

These families were typical of a much broader group, amounting to half of all families: those between the 30th percentile and the 80th percentile of the wealth distribution. For most of these families, their most important assets were their homes and their retirement accounts, which together represented over half of their net worth. On average, they lost 37 percent of their wealth.

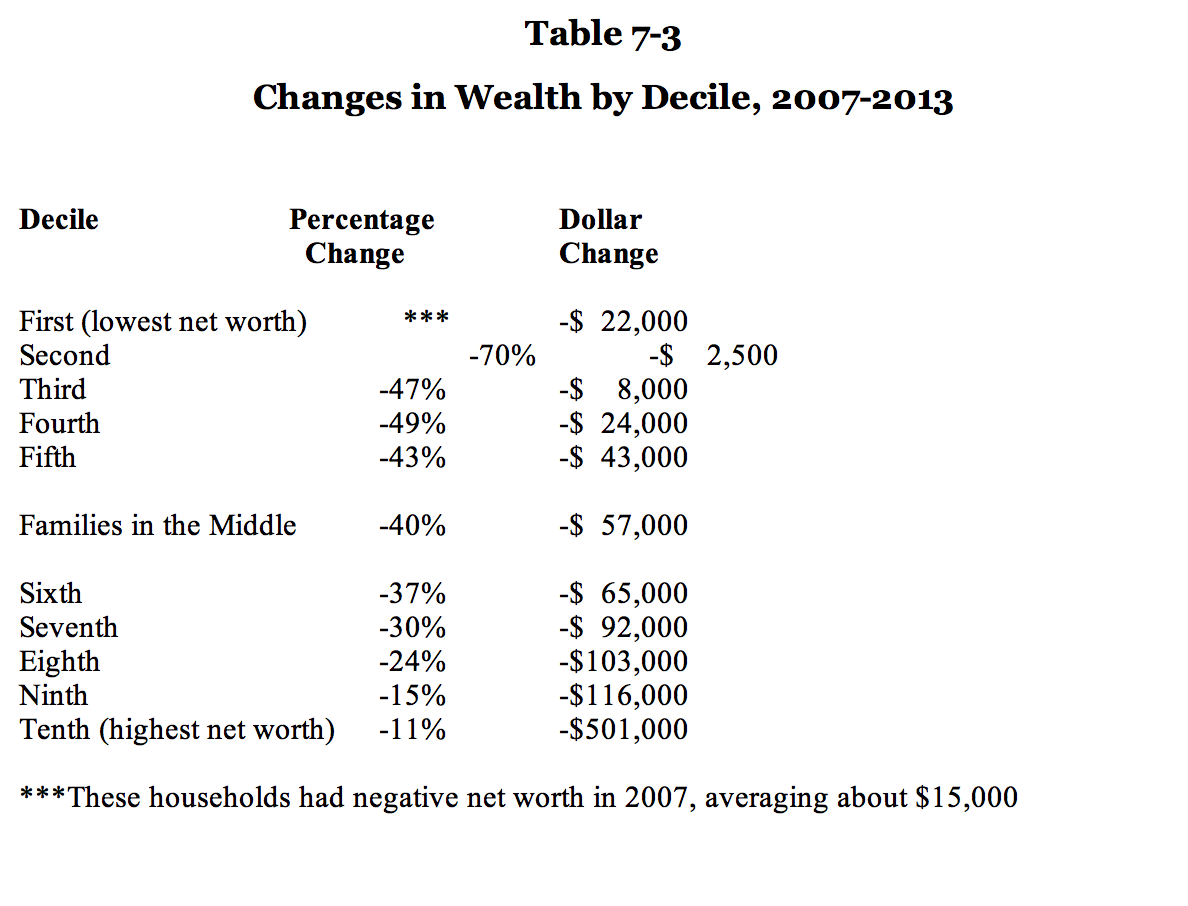

In every wealth bracket, Americans were hurt by the Great Recession, but not all Americans were hurt to the same extent. The richest 10 percent saw their average wealth drop from $4.5 million to $4 million, a loss of about 11 percent. As a result, their share of total household wealth increased from 71 percent in 2007 to 75 percent in 2013 – their largest share reported in any Survey of Consumer Finances over the full three decades. The share of the 10 percent in the middle dropped from 2.1 percent to 1.6 percent. Between 2007 and 2013, the distribution of wealth became noticeably more unequal, for the first time since the first SCF in 1983.

The depth of the recession, the weakness of the recovery, and the more unequal distribution of wealth may all have contributed to the dissatisfaction of Americans with the current state of America. Since the beginning of 2009, a majority have consistently said they believe America is “on the wrong track,” as opposed to “going in the right direction.” Typically, about 60 percent have the negative view, compared to about 30 percent with the positive. Current opinions are modestly less negative than they were in 2013, but more negative than they were in 2010, just after the Great Recession.

1. The Distribution of Wealth: The Political and Analytical Context

Economic inequality in the United States has attracted a great deal of attention in recent years, beginning with President Obama’s major speech in December 2013.1 Among economists and other social scientists, Thomas Piketty’s 700-page book on inequality, Capital in the Twenty-First Century, has been much praised and much criticized.2 But inequality has been front-page news for more than three decades. Liberals express great concern about increasing inequality; conservatives decry it as an obsession.3 It is an important issue in tax policy debates, and in discussions of programs intended to help the poor in the short run, such as welfare, and in the long run, such as education.

This study analyzes the distribution of wealth, one of the most important measures of economic well-being. It uses the Federal Reserve Board’s triennial Survey of Consumer Finances, first conducted in 1983 and most recently in 2013. The SCF contains the most detailed information available about the wealth of American households.

Inequality: What We Know, and What We Don’t

It is widely believed that the richer are getting richer and the poor are getting poorer, and have been for a long time – at least since “Ain’t We Got Fun?” became a popular song in the 1920s.4

There are several reasons for thinking so. Total wealth has increased dramatically in America since consistent data first became available in 1983. At that time, we Americans were worth $33 trillion, in the aggregate; by 2013, the latest date for which detailed information is now available, we were worth almost double that amount, $65 trillion (both measured in 2013 dollars). It is easy to see that some people are very rich. Forbes magazine annually publishes a list of the 400 richest families in the country. Their combined net worth is estimated at $2.34 trillion, which is a new record.5 It is also regularly reported that there are more millionaires or billionaires now than there were a few years ago. From this it is easy, but not necessarily accurate, to infer that inequality is increasing; some of the rich are getting richer.

In addition, the distribution of income has become more unequal in the United States, and has been doing so since about 1969. There is much more information available about household income than about household wealth, and many people do not clearly distinguish between income and wealth. This is true of journalists, business people, ordinary citizens, and even economists, in my experience.

A third reason is that “wealth” commonly seems to be thought of only as “financial wealth.” When I mention my research on the distribution of wealth to journalists, people in business, ordinary citizens or economists, they almost invariably respond with a comment about the stock market. Stock indices have risen dramatically over the last three decades; the Standard and Poor’s 500 rose elevenfold between 1983 and 2013, there were impressive stock market booms in the 1980s, 1990s, and 2000s. (There were also large and sharp declines during 2000-2002 and 2008-2009.) The conventional wisdom is that rich people own stocks and middle-class and poor people don’t, or don’t own much; with the rise in stock prices, it seems to follow quite logically that the distribution of wealth is becoming more unequal.

Finally, wealth is in fact unequally distributed, much more so than income, for perfectly understandable reasons. The most important is that people accumulate wealth over their lifetimes, so that older people are on average much wealthier than younger people. The fact that wealth is unequally distributed now, however, does not mean that it is more unequally distributed than it used to be. But it is easy to confuse “high inequality” with “rising inequality.”

Some academic studies have also contributed to the conventional wisdom, particularly some of the early research using the first Surveys of Consumer Finances. When the tabulations of the 1983 SCF were published, the data appeared to show a very large increase in the concentration of wealth among the very richest Americans, compared to somewhat similar previous surveys.6 Subsequent investigation of the data showed that the increase in concentration was entirely the result of an error in the information for one household, which reported an extremely large holding in one asset category, and which also had the biggest weight of any household in the survey. (The SCF, like virtually all economic surveys, is based on a sample of households, and those households are then weighted to reflect the total population. Similar techniques are employed for political polls.) A follow-up interview with the household determined that the original data was erroneous.7 In the meantime, however, the original calculation had attracted substantial media and political attention.8 The SCF results were published during the heated political debates about the economic policies of President Reagan; critics of the President cited the SCF as showing that the President’s program was helping the rich and hurting the poor. A report published by the Joint Economic Committee, relying on the original results of the SCF, sharply attacked the President and attracted further attention.9

The correction was reported by the Federal Reserve Board and the Survey Research Center of the University of Michigan (which conducted the SCF for the Fed). It was noted in the press, and the JEC published a second report using the corrected data to argue that the distribution of wealth had not changed.10 But this was not enough to countermand the original impression.11 Inequality remained a component of the standard critique of Reaganomics. Indeed, and ironically, the error seems to have generated the current research and policy interest in the distribution of wealth. Had the data originally been reported correctly, there would have been much less for scholars to explain to begin with, and probably much less interest by the media.

In fact, even the original, erroneous tabulation did not imply anything about President Reagan’s policies. The 1983 SCF was being compared to a 1977 Survey of Consumer Credit, which contained much less information about wealth, omitting several categories of assets including one very important category, ownership of unincorporated or closely-held businesses. In 1983, these businesses accounted for over 20 percent of total household net worth, and over 50 percent of their value belonged to the richest one percent of households. Including businesses, the richest one percent of all households owned 31.5% of all net worth; excluding businesses, the richest one percent owned 25.9 percent.12 The 1977 SCC also reported the dollar values in brackets rather than to the dollar, which further limits comparability.13 Moreover, of course, the years between 1977 and 1983 include two political Administrations – indeed, more years of the Carter Presidency than the Reagan Presidency – and two very different economic experiences: three years of accelerating inflation and economic expansion between 1977 and the beginning of 1980, followed abruptly by back-to-back recessions and unanticipated disinflation during the early 1980s.

Some early academic studies using the SCF also appeared to show increasing inequality. In a series of papers published in the Review of Income and Wealth, economist Edward Wolff reported a substantial increase in inequality between 1983 and 1989, the dates of the first two Surveys of Consumer Finances.14 Wolff’s results also attracted attention because the dates happened to bracket the economic expansion that occurred under President Reagan. He subsequently argued that the increase in wealth inequality during the 1980s was greater than at any time since the 1920s, and implied that the Great Depression was due to the earlier increase.15 Research by other scholars demonstrated that Wolff’s results for the 1980s depended on technical adjustments to the data: the choice of weights for the individual households in the sample, and whether (and how) the reported wealth holdings in the SCF were adjusted so that the totals were aligned with totals reported in other sources of financial data for the US economy. Alternative and equally plausible technical procedures yielded the conclusion that wealth inequality had not increased much (conceivably not at all) between 1983 and 1989, and further research showed that the increase during 1983-1989 was reversed during 1989-1992, a period that included a moderate recession.16 Wolff’s conclusions and policy recommendations, however – higher marginal income tax rates and a new federal tax on wealth, in order to reduce inequality – were popular among liberal policymakers and journalists, and his ominous comparison of the 1920s and 1980s complemented the view of some historians that inequality was a major cause of the Great Depression and contributed to concerns that a new Depression was imminent.17

These analyses are not definitive, but they continue to set the tone for media reaction to each new SCF when the results are released every three years. A finding that inequality has not increased tends to be greeted with surprise, and even skepticism; a finding that inequality has increased appears to be much more consistent with prior expectations.18

The Nature and Structure of the Study

This analysis reports in detail on the changes in the distribution of wealth between 1989 and 2013, using data for the last nine Surveys of Consumer Finances. These nine surveys are quite consistent in coverage and methodology. The analysis also looks back to the 1983-1989 period, despite the fact that there are various differences between the 1983 SCF and the later ones, because the 1980s remain controversial and matter for policy discussions.

The next chapter defines wealth and lists its major categories. It also explains the differences between wealth and income, and explains how the distributions of these two related economic measures can move in different directions. Income and wealth are certainly correlated; high income households usually are wealthy households. But the correlation is far from perfect; in the triennial SCF it falls between 0.4 and 0.6 in various years, certainly significantly different from zero but also significantly different from unity.

Chapter 3 reports on the total wealth of all American families over the last three decades, as background to the analysis of the distribution of that total, and Chapter 4 describes the changes in the composition of our wealth. The three major categories of our wealth have been and are: financial assets such as stocks and bonds; ownership of unincorporated and closely-held business, including proprietorships, professional practices, and most commercial real estate; and homeownership, the equity that Americans have in their homes. These three categories comprise about 60 to 75 percent of our wealth. Their relative importance has varied over the last three decades.

Chapter 5 presents the basis analysis of the changes in the distribution of wealth over time. I divide the 30 years into three periods: 1983-1992, the strong economic recovery after the back-to-back recessions of 1980 and 1981-1982, ending with the recession of 1990-1991; 1992-2007, two long economic booms separated by a moderate recession in 2001 (which owing to the timing of the SCF is not very prominent in the data); and finally 2007-2013, the Great Recession and the unusually weak recovery that followed, and indeed has persisted since 2013 and is now in its seventh year. (The period from the mid-1980s to the end of 2007 is frequently referred to as the “Great Moderation,” during which the volatility of economic activity was significantly reduced, especially compared to the erratically increasing inflation that the U.S. experienced between about 1965 and 1982.19) Over these 30 years, the total wealth of Americans increased substantially, even adjusting for inflation and population growth.

The distribution of that wealth became slightly more unequal between 1983 and 1989, but that was reversed during the recessionary period from 1989 to 1992; total real wealth increased by about 25 percent. Over the next 15 years, the distribution became more unequal, but the change from one survey to the next was not statistically significant and total real wealth more than doubled.

During the Great Recession, however, the distribution of wealth became significantly more unequal and total real wealth fell by more than 10 percent. Accordingly, Chapter 6 discusses some of the reasons for those changes, with particular attention to important categories of assets and liabilities.

Chapter 7 focuses on the changes in wealth that occurred for families in the middle of the wealth distribution over the three decades. These families have attracted substantially less attention than “the rich,” and less also than poor families have received.

The concluding chapter summarizes the changes between 1983 and 2013, and assesses their implications for the economic well-being of American families, and also for Americans’ attitudes about our economy and our society. Our belief about the distribution of economic well-being is at the core of our self-image, and one reason for our exceptionalism; we have traditionally believed that “the sky’s the limit,” and we have usually been more concerned with economic opportunity than economic inequality. Changes in the distribution of wealth matter for our self-understanding, and can affect all sorts of economic and social policies.

The Survey of Consumer Finances

The data source for the analysis is the Federal Reserve Board’s Survey of Consumer Finances (SCF). This is one of the few sources of information on household wealth that reports asset and liability holdings of individual households for a sample of the entire population on a consistent basis over time. As mentioned above, the survey was first conducted in 1983. Subsequent surveys have been conducted triennially, with the most recent in 2013. The data therefore cover a 30-year period, but the 1986 survey was not considered satisfactory and has seldom been included in analyses by either Federal Reserve Board staff or independent economists. There are also differences between the 1983 survey and the later ones in the techniques used to weight the sample observations to represent the universe of American households. Consistent weighting techniques were developed in 1997 for the surveys of 1989, l992, and 1995. They have been used for the later surveys, and are used in this analysis.20 I also describe separately the distribution of wealth between 1983 and 1992, using weights that were constructed at the time those surveys were taken, because the distribution of wealth became a matter of particular public interest in the mid-1980s with the publication of the 1983 survey.

An important feature of the SCF is that it includes a special sample of high-income households that can be expected to have unusually large wealth holdings, as well as a cross-section chosen randomly to represent the entire population of households. Because wealth is concentrated among a relatively few households, a national sample of households will give little information about a large fraction of household wealth. The high-income sample has grown in importance from one survey to the next, reflecting an effort to give more equal sampling probabilities to all dollars of wealth, rather than all households.21

The only earlier survey with a similar methodology, including a sample of high-wealth households, is the Survey of Financial Characteristics of Consumers in 1962, also conducted by the Federal Reserve Board.22 The long interval between the SFCC and the first SCF suggests caution in comparing the results in detail. The Federal Reserve also conducted a Survey of Consumer Credit in 1977, which has sometimes been used to compare the distribution of wealth with the 1983 SCF, but the SCC has much less information on wealth holdings than any of the later surveys, or the SFCC, and primarily reports on the credit experience of households. It omits some important wealth categories, such as the value of unincorporated or closely-held businesses, and reports holdings in brackets rather than to the dollar, with a top bracket of $200,000 or more. Analysis of the 1983 SCF using these conventions shows that the results are quite sensitive to the way in which the data are reported.

Unless Otherwise Specified…

I have adopted two conventions throughout this paper, which the reader should keep in mind, especially when referring to any of the numerous tables that appear throughout the analysis.

The SCF financial data is publicly available in two forms: nominal dollars, and real dollars as of the year of the most recent survey (at this point, 2013). For convenience and consistency, I have reported nearly all dollar amounts in 2013 dollars. If a dollar amount is not in 2013 dollars. either in the text or the tables, the year to which it refers is specified.

Most of the data comes from the SCF, and most of the calculations have been performed by myself, working with one or more of the research assistants who have been very helpful on worked with me. I have not thought it useful to repeat “SOURCE: Calculated by the author from SCF data files,” in table after table. If another source is used, it is cited.

2. Basic Concepts: Wealth and Income

The most useful starting point for this analysis is to make clear the distinction between wealth and income. Indeed, it is essential. The terms are often used interchangeably, and often used inaccurately even by people who write about them and make a living teaching about them. Since I first began writing on the distribution of wealth some 30 years ago, a number of economists have asked me from time to time for copies of my work on “the distribution of income,” even though all of my research papers have wealth in the title, and none have income. If economists do not manage to keep the terminology straight, it is no wonder that the press and the public get them mixed up.

The basic distinction is that wealth is a stock and income is a flow. Wealth is the value of a stock of assets at a given point of time. For a particular household, wealth is the value of the total assets it owns, minus the total liabilities, the amount of its debts. Wealth is synonymous with net worth. Income is the money that households receive over a given period of time, reported most commonly for a calendar year.23

Wealth includes:

- the value of a home, minus the amount owed on the mortgage.

- the value of the cars owned by the household, minus the amount owed on any car loans.

- the value of any rental housing or commercial property owned by the household, minus the mortgages on those properties.

- the value of business owned directly by the household —proprietorships, partnerships, independent professional practices in law or medicine, farms, and stock in closely-held corporations which are not publicly traded — minus any debts owed by the business.

- any stocks or bonds, and any mutual funds.

- the balances in checking account and savings accounts.

- the cash value of whole life insurance policies.

- the present value of IRAs and Keogh plans, and other retirement savings accounts.

On the liability side, net worth takes account of any installment debt, such as student loans, credit card balances or other consumer debt, as well as the mortgages on homes and other property, auto loans and business debt mentioned above.

There are a number of common exclusions from wealth measures, some of them quite important for a family’s wellbeing. Wealth seldom includes the value of consumer durables, such as furniture or appliances, even though it includes the debt incurred to purchase them. Wealth also typically excludes the present value of any pension benefits or Social Security payments that the household expects to receive in the future. These present values can certainly be quite large, but they are also difficult to quantify.24

Income information is collected by several federal agencies. The Bureau of Economic Analysis calculates total personal income as part of the National Income and Product Accounts. These are published in six broad categories and in 19 subcategories.25 The broad categories are:

- Employee compensation

- Income of proprietors

- Rental income

- Income from assets

- Transfer payments

- Contributions to government social income programs (an offset to income received)26

Table 2-1 lists the components of net worth, both assets and liabilities, and their relative importance for American households between 1983 and 2013, calculated as averages from the data for the individual Surveys of Consumer Finances. By far the largest component is the value of owner-occupied homes, even taking account of the outstanding principal balances on home mortgages and home equity lines of credit. It has amounted to about 23 percent of net worth, on average, over the surveys between 1983 and 2013. Certainly, not all households are homeowners; the homeownership rate for the 10 survey years averaged about 66 percent. But home equity represents about 35 percent of the net worth of those households that do own homes. The value of unincorporated and closely-held business is the second largest category. The third largest is common stock, including directly owned stocks and stock held within mutual funds, trusts, or retirement accounts; the total value of stock held in any of these forms amounts to 17 percent of household wealth. Investment real estate, including both rental and commercial, consists of property owned directly by an individual or through a partnership, as opposed to stock holdings in corporations that invest in real estate.

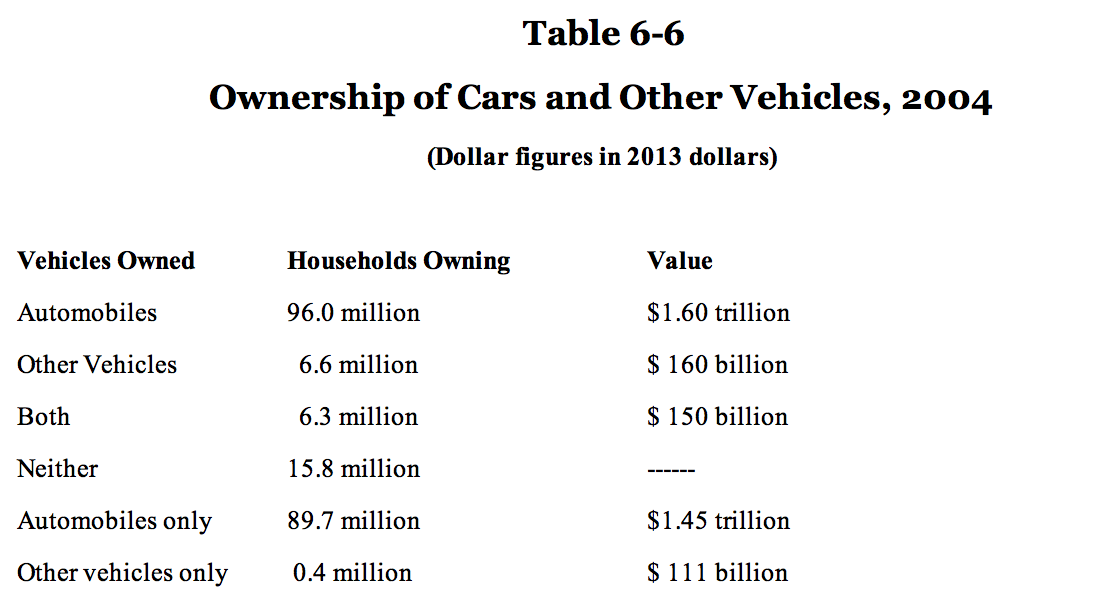

The most widely held assets are automobiles and checking accounts. Consistently, about 85 percent of households owned one or the other, and most owned both. Although the values of individual accounts or automobiles are not large, in the aggregate they accounted for over 10 percent of net worth.

This is not the common perception about the composition of wealth. Journalists, businessmen, and citizens, in my experience, tend to equate “wealth” with “stocks and bonds.” They think in terms of financial assets, and tend to dismiss real assets from consideration or minimize their significance. Some economic analysts also give primacy to financial assets in describing the distribution of wealth.27 But financial assets amount to less than half of all household wealth, ranging from 33 to 47 percent in the individual surveys, with an average of 41 percent.

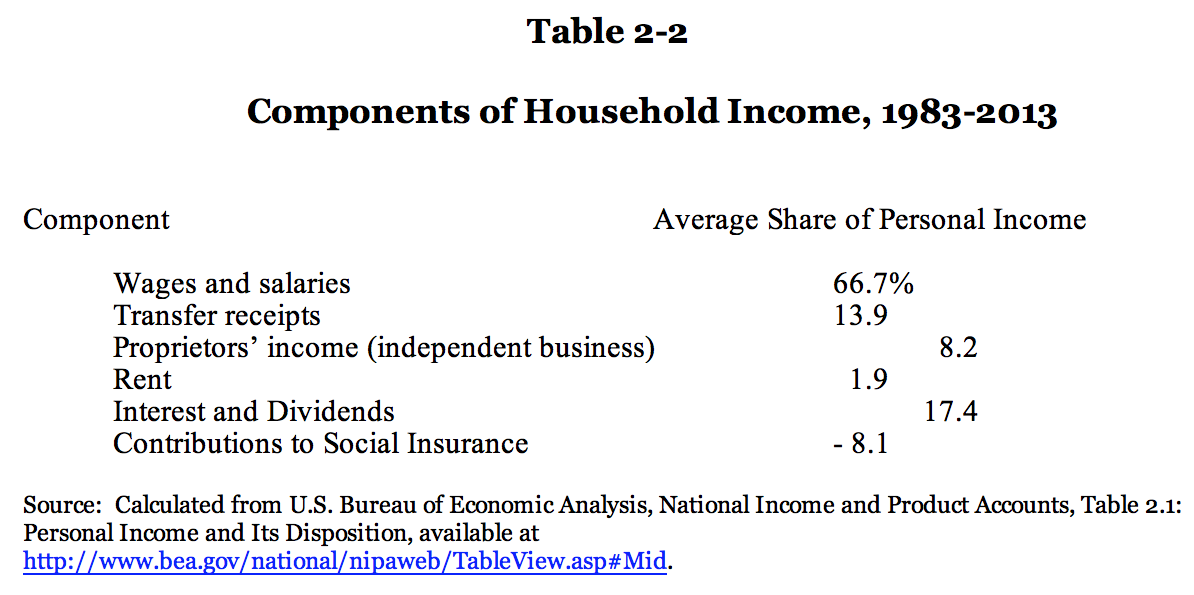

Different categories matter for wealth and for income. The largest component of income is income from employment – wages and salaries, etc. Over the 1983-2013 period, wages and salaries have amounted to 67 percent of all personal income, on average, as reported in the National income and Product Accounts and shown in Table 2-2.28 There is no counterpart to this category in the wealth statistics. The same is true for transfer payments, which averaged 14 percent annually over the period.

The converse is true for home equity, the largest component of household wealth. There is no income generated by households’ equity in their homes, and thus no counterpart to home equity in the income received by households. In addition, one of the mostly widely-held assets – automobiles, trucks, and other vehicles, owned by 86 percent of American households – also yields no income. The value of cars and other vehicles amounts to about 3 percent of household net worth, even after taking account of the principal balances owed on loans to purchase them.

It is possible to create measures of human capital, making use of wage, salary, and self-employment income, and economists have made such estimates for some purposes, such as serving as expert witnesses in wrongful death lawsuits, for example.

Similarly, it is possible to impute the annual rental value of owner-occupied homes, and such imputations are included in the Consumer Price Index (CPI) produced by the Bureau of Labor Statistics (BLS). “Imputed rent” is the rent which a homeowner would receive if he or she chose to move out of their home and rent it to someone else: “To see why imputed rent is a real form of income, consider two homeowners living in identical houses. Suppose they trade houses, each living in the other’s. They now pay rent to each other because …[each] is now the other’s landlord. If they pay identical rent, it would appear that it all cancels out, except that each now has rental income to report on her taxes. In principle, that rental income is there even when one lives in one’s own home.”29 The CPI calculates imputed rent by collecting information on the rents actually paid for rental housing, and using them to estimate the rental value of similar homes, which are in fact occupied by their owner. As stated by BLS, “The most efficient way to measure the price of the shelter service owner occupants receive from their homes is to estimate the rent that the residence would command.”30

Imputed rent is also used in the National Income and Product Accounts produced by the Bureau of Economic Analysis, in discussions of “tax expenditures” in the federal budget each year, and in the major recurring reports on the budget published by the Congressional Budget Office.31 A few countries include imputations in the definition of taxable income in their tax codes, albeit at very low values for the imputed rents or very low tax rates.32

For that matter, it is also possible to impute the annual rental value of cars and other vehicles. But calculations of these imputed values of these economic concepts are not included in the statistics on household income produced by the Bureau of Economic Analysis and the statistics on household wealth in the Survey of Consumer Finances.

To summarize, four-fifths of the income people receive has no corresponding component in their wealth, and one-quarter of the wealth people own does not generate income. Rising house prices will increase the wealth of about two-thirds of American households, and possibly affect the distribution of wealth. They will not affect the distribution of income. Similarly, rising, stagnant, or falling wages are likely to affect wealth only gradually, as they affect household savings. It is therefore not automatic that the distributions of wealth and income will change in the same direction over time. This is especially plausible over short periods of time, such as the three years between consecutive Surveys of Consumer Finances, but it can occur over longer periods as well. Thus the increase in median household income between 2014 to 2015, recently reported by the Census Bureau, does not imply that household wealth increased as well – welcome news though it certainly is.33

The practical consequences of these differences in measurement will be evident in the remainder of this analysis. The basic points to keep in mind are, first, that income and wealth are different concepts and have different components, and second, that trends in the distributions of income and wealth can move in opposite directions.

3. American Wealth over Three Decades

Growth and Recession, 1989-2013

Wealth in the United States increased rapidly, as the SCF reports – until the Great Recession. This is clearly shown in Table 3-1. Total wealth increased sixfold between 1983 and 2007; adjusted for inflation, total wealth tripled. The annual average rate of increase was about eight percent for nominal wealth, and close to five percent for wealth in real terms. The data for 1983 are not precisely comparable to the later years, but there is no question that both nominal and real total wealth, measured consistently, increased during the economic boom of the 1980s, as well as between 1989 and 2007.34

Average real wealth per family more than doubled from 1983 to 2007; median wealth per family increased by 70 percent.

The story is quite different since 2007. During the Great Recession and immediately afterwards, total wealth dropped by almost 15 percent, adjusted for inflation; average wealth per family by 15 percent; and median wealth per family by 40 percent – almost back to its level in 1983. Moreover, neither total, mean, nor median wealth has recovered any of these sharp declines since 2007; in terms of wealth, we remain at the depressed levels of the Great Recession. (Nominal wealth fell by 10 percent between 2007 and 2010, but has since recovered to its 2007 level.)

This experience is unlike the aftermath of other recent recessions. Before the Great Recession, there were more typical postwar recessions during 1990-1991 and during 2001 (March to November), each lasting only eight months. Real wealth declined between 1989 and 1992 by about 10 percent, very nearly the same as occurred between 2007 and 2010, while mean and especially median family wealth dropped by smaller percentages (12 percent and five percent, respectively). But from 1992 to 1995, total net worth rose to almost its 1989 level, median family net worth exceeded it, and mean family net worth regained about one-third of the loss, while between 2010 and 2013, total net worth regained about 20 percent of its previous decline and both mean and median family net worth continued to decline, albeit slightly.

The recovery after 2001 was similar to the recovery after 1992, but it is difficult to measure the changes over the economic cycle because the data collection period for the 2001 SCF almost perfectly coincides with the dates of the recession – May to December for the SCF interviews, March to November for the recession. Thus some households were interviewed just before or at the cyclical peak, while others were interviewed at or just after the cyclical trough.

Measuring Household Wealth, 1983-1995

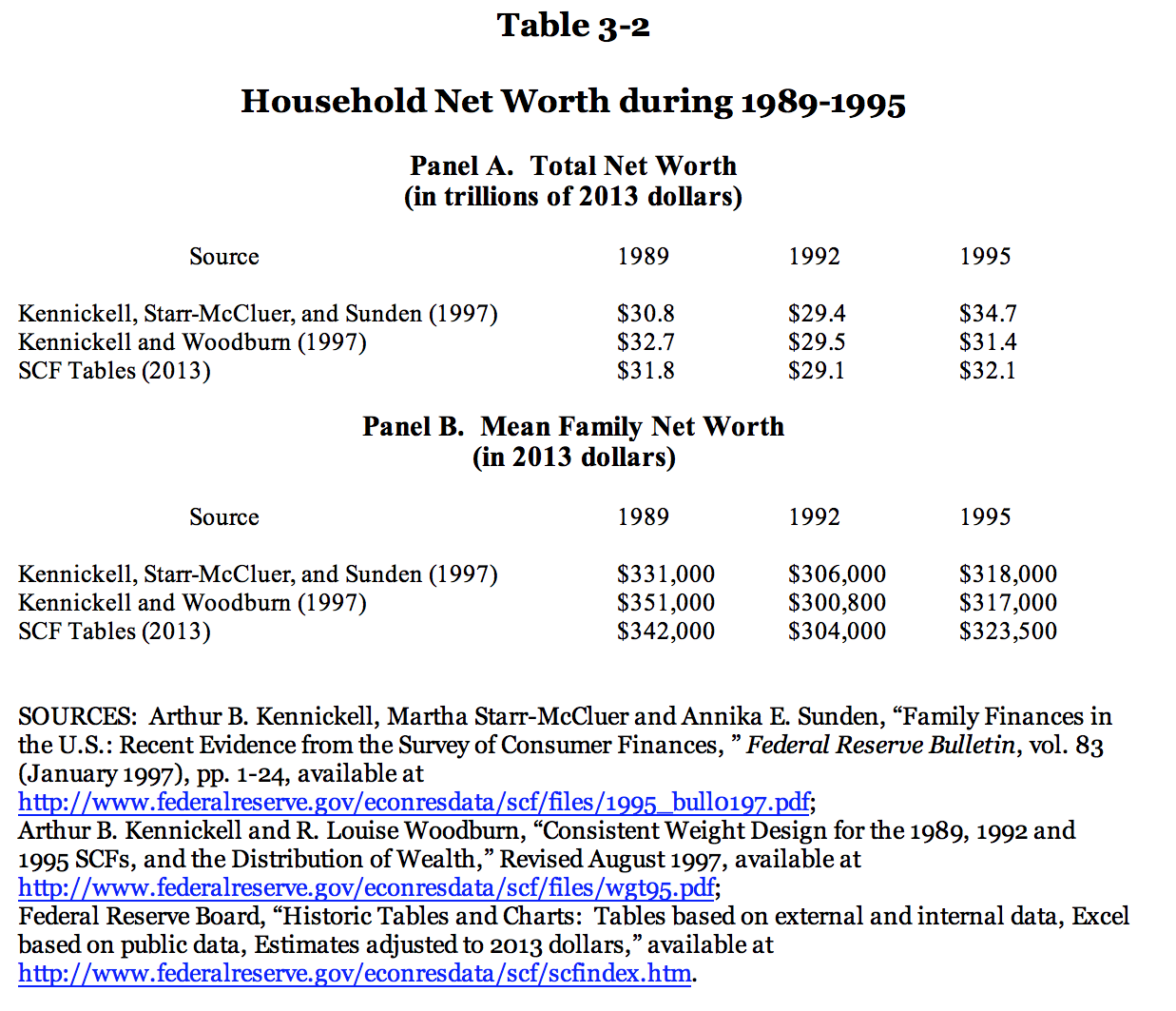

As explained in Chapter 1, the SCF data for 1983 are not precisely comparable to the later years. The same is true for the weights originally constructed for each of the first three surveys. Consistent weighting techniques were developed in 1997 for the surveys of 1989, 1992, and 1995. These weights have been used for the subsequent surveys. The weighting techniques could not be used for 1983, however; the information needed for that purpose was no longer available by 1997.35 Thus it is possible to describe the changes in the distribution of wealth on a consistent basis during 1989-2013, but not during 1983-2013. It is possible, however, to use the original weights for 1983, 1989, and 1992, in combination with the consistent weights for 1989, 1992, and 1995, to look at 1983-1992 separately, and then use the two overlapping periods to describe, at least in general terms, what happened over the full period 1983-2013.

There is, however, a further complication. Before the consistent weights were developed in 1997, there had been a period of active research into weighting issues, during which more than one set of weights had been constructed for each of the first three surveys. The results for 1983 to 1992 in particular depend on which sets of weights are chosen for the analysis. For the 1983 survey, weights were constructed separately by analysts at the Survey Research Center, which conducted the SCF, and by analysts at the Federal Reserve Board. The SRC weights were aligned on the basis of total households and the division between urban and rural location. The first set of FRB weights were aligned on the basis of the household totals for the four U.S. Census regions. Subsequently, the FRB analysts constructed a second set of weights when the individual income tax data for 1982 suggested that the high-income household sample might have been weighted too heavily.

There are differences of about seven percent in both total wealth and mean family wealth, depending on which set of weights is used. Calculating with the FRB weights, total wealth is about $23.8 trillion in 2013 dollars; calculating with the SRC weights, total wealth is about $25.5 trillion. Similarly, mean family net worth is about $280,000 in 2013 dollars with the FRB weights and $300,000 with the SRC weights.36 Subsequent research by the Federal Reserve analysts typically used the FRB weights for comparison with later surveys.37

This difference does not materially affect most of the measures of net worth reported in Table 3-1. Nominal total wealth rose about sixfold between 1983 and 2013, and real total family wealth by about 150 percent, using either set of 1983 weights. Mean real family wealth doubled over the three decades, using either set of weights.38

For the 1989 survey, two sets of weights were created and published as part of the database for the survey: preliminary weights used by the Federal Reserve analysts for comparing 1983 to 1989, and revised weights for comparing 1989 to 1992. The difference between them was not large. The preliminary weights produced net worth estimates about 2.25 percent above the revised weights.39 The original Federal Reserve Bulletin article that reported the 1989 wealth calculations and compared them to 1983 employed the preliminary weights. Total net worth was calculated as $30.5 trillion and mean family net worth as $327,000 both in 2013 dollars).40 This article was published in 1992.

Between 1992 and 1997, Federal Reserve analysts conducted a number of further studies in weighting, typically calculating mean family net worth in the range of $330,000 to $342,000 for 1989. This research culminated in a 1997 working paper and Federal Reserve Bulletin article, both of which created consistent weights for the 1989, 1992 and 1995 surveys to describe changes in net worth over that period. Most recently, the Federal Reserve Board has prepared tables reporting net worth for each of the surveys since 1989.

The results from these weights are shown in Table 3-2. There are some differences between the calculations for 1989, with a range of about six percent between the highest and lowest estimates for both total and mean family net worth, but the overall pattern is clear (see table 3-2).

There was a sharp decline between 1989 and 1992, and a partial recovery between 1992 and 1995. Also, when 1983 is included, it is clear that there was a substantial increase in wealth during the 1983-1989 boom, but much of that gain was lost during and immediately after the 1990-1991 recession. Using the values for 1983 in Table 3-1, about 20 percent to 35 percent of the 1983-1989 increase in total wealth, and about 50 to 67 percent of the corresponding increase in mean family wealth, was lost during the next three years. Despite the recession, however, net worth increased dramatically between 1989 and 2007. Total real wealth more than doubled, and mean real family wealth rose by 75 to 90 percent.41

4. What We Own, and What We Owe: The Changing Composition of Household Wealth

The net worth of American households consists of their assets minus their debts –a broad range of assets, partially offset by debts for numerous purposes. The importance of these assets and debts varies over time; some categories have increased in importance over the last 30 years, while a few have diminished, and some have fluctuated. Chapter 2 enumerated the major asset categories, without much description; this chapter describes them more fully. The enumeration of assets has been quite consistent since 1989, but the questionnaire for the first SCF in 1983 differed in several respects from the later ones. Accordingly, this chapter parallels the discussion in Chapter 3, first describing the changes between 1989 and 2013 and then comparing 1983 and 1989. The differences between the surveys do not affect most of the basic patterns of change over the full 30 years.

Financial and Non-Financial Wealth

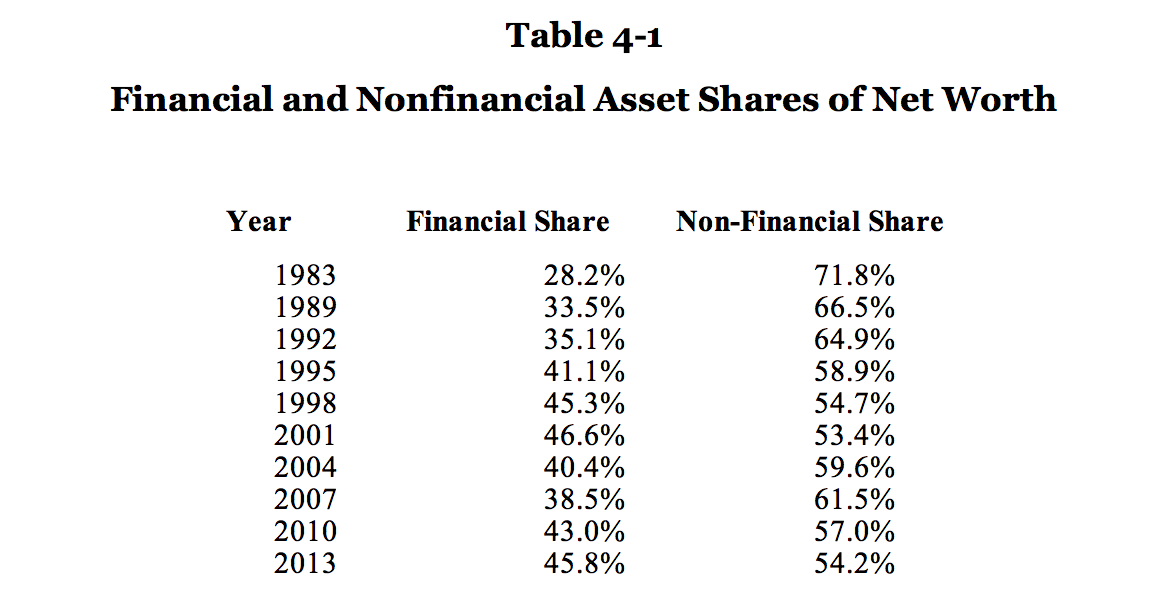

One convenient way to classify assets and debts is in terms of two broad groupings: financial and non-financial. This classification has been reported in the Federal Reserve Bulletin articles discussing each SCF and comparing it to its predecessor, and in most of the working papers subsequently written and available on the SCF website.42 They are also used in the published tables comparing data on a historical basis for all of the SCFs since 1989.43 The relative importance of financial and non-financial wealth is shown in Table 4-1.

Two points stand out: the non-financial share of net worth has been declining over the three decades, except during 2001-2007, the last half of the homeownership boom; and non-financial wealth has been the larger half of household net worth throughout the three decades, belying the popular notion that wealth consists mostly of stocks and bonds.

While the non-financial share of wealth has been declining, the total value of non-financial assets, in real terms, has generally been growing from one survey to the next. There are two exceptions: non-financial wealth declined by 12 percent between 1989 and 1992, and since 2007 non-financial wealth has fallen by 23 percent, with the end of the homeownership boom and the collapse of the housing finance system. Despite these abrupt changes, non-financial wealth has more than doubled since 1983.

Financial wealth has grown more rapidly. It has more than quadrupled in the last three decades, becoming a larger share of a larger stock of wealth. There are also two exceptions to this persistent trend, both small: total financial wealth declined by four percent from 2001 to 2004, and by one percent between 2007 and 2010. The magnitude of this latter, very modest decline partly stems from the timing of the surveys. Between October 2007 and October 2010 (about the midpoint of the SCF interviewing period for those surveys), both the Dow Jones Industrial Average and the S&P 500 declined by close to 25 percent, and the NASDAQ Composite declined by 10 percent; but as of the spring of 2009, halfway through the interval between the 2007 and 2010 SCFs, all three had lost more than half of their value over the previous 18 months.44

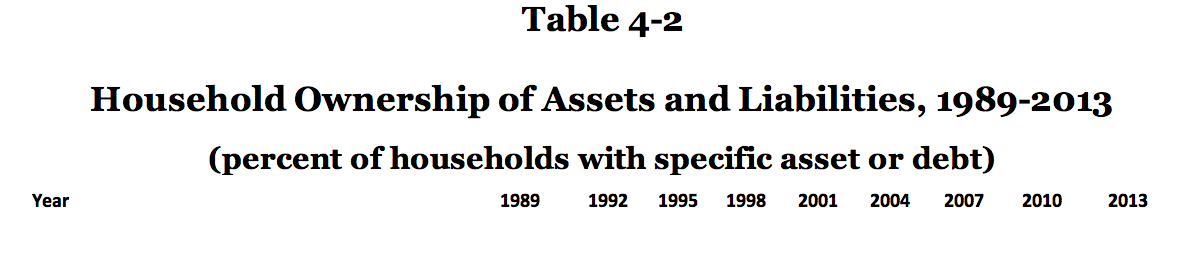

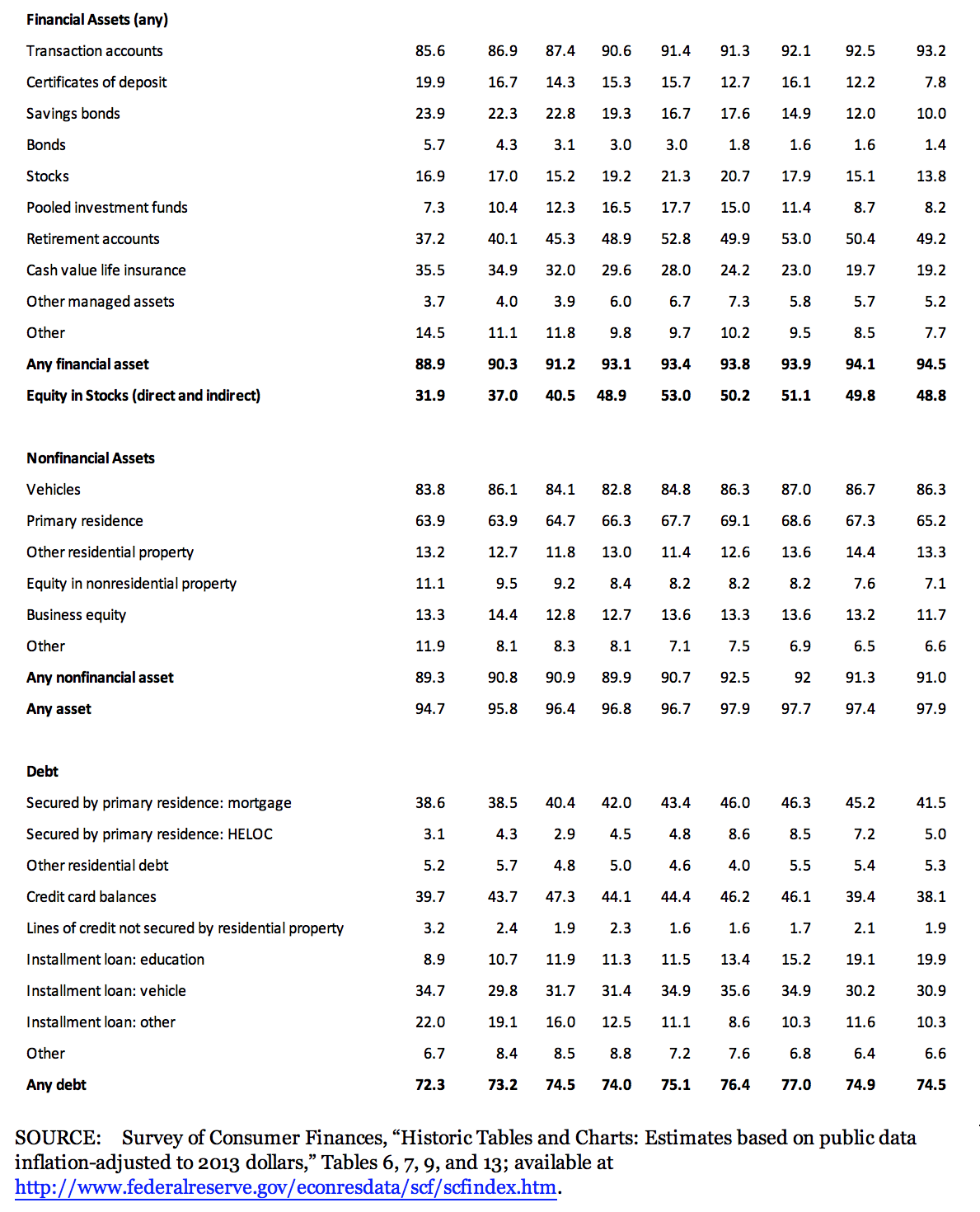

Tables 4-2 and 4-3 disaggregate assets and debts into categories, following the classifications in the Federal Reserve Bulletin articles and working papers. Table 4-2 reports the percentage of households holding various assets or owing various debts; table 4-3 reports the net worth for each category, expressed as the mean value across all U.S. households, including those who did not hold that type of asset.

The most widely held assets in 1989 were: transaction accounts (85.6 percent of all households), vehicles (83.8 percent), owner-occupied homes (63.9 percent), retirement accounts (37.2 percent), and cash value life insurance (35.5 percent). These were still the most widely held assets at the cyclical peak in 2007, in the same order; and for that matter the most widely held in 2013, after the Great Recession, also in the same order. Indeed, these were the five most widely owned assets, in that order, in each of the nine surveys.

The most widely incurred debts as of 1989 were credit card balances (39.7 percent), home mortgages (38.6 percent), and vehicle loans (34.7 percent). These remained the most common liabilities in all of the surveys through 2007 – not quite in the same order, because home mortgages were slightly more widely held than credit card debt by 2007. Both were held by about 46 percent of households.

Student loans became noticeably more common. Nine percent of households had one or more student loans outstanding in 1989; 15 percent did so in 2007.

Changes in Asset Holdings and Debts, 1989-2007

By contrast, the value of many of these assets and debts in household portfolios changed substantially after 1989, as Table 4-3 shows. The value of owner-occupied homes nearly doubled between 1989 and 2007, although homeowners’ equity increased to a lesser extent because mortgage debt more than doubled. The value of retirement assets more than tripled.

Indeed, the most fundamental change between 1989 and 2007 was the growing importance of stocks in household portfolios. This was very much the result of the creation of Individual Retirement Accounts in 1974, and their expansion to all workers in 1981. By 2001 more than half of all households had retirement accounts, although not all of these accounts included stock.45 Investment in mutual funds also increased dramatically, although not all of these funds included stock either. The value of stocks directly owned by households more than doubled, and the value of other managed assets (such as trusts and annuities) also increased, although the proportion of households holding stocks directly began to decline after 2001, and the proportion with other managed assets was small.

The SCF reports the proportion of households owning stock directly or indirectly and the value of these holdings – “stocks” and “stocks (direct and indirect).” As of 1989, over 60 percent of the stock owned by households was owned directly, as shares. By 1995, less than half was directly owned; by 2001, less than 40 percent; by 2013, less than one-third.

Indirect holdings of stock are held in retirement accounts, mutual funds, trusts, annuities, and other managed accounts. The incidence of stock ownership rose from 32 percent in 1989 to 51 percent in 2007, parallel to the spread of retirement accounts, which rose from 37 percent to 53 percent. The value of stockholdings increased from $31,000 to $115,000, while the value of retirement accounts rose from $26,000 to $88,000. The growing importance of retirement accounts is evident in these data.

Some other categories of assets also showed noteworthy increases between 1989 and 2007. Both transaction accounts and vehicle ownership increased, from 86 percent to 92 percent and from 84 percent to 87 percent, respectively. As mentioned previously, these were the two most widely held assets through the period. Despite the fact that the vast majority of households owned a checking account and a car at the start of the period, ownership of both increased during the long economic expansion, and the value of these assets also increased.

Over the same period, there were noticeable declines in the ownership of assets that were fairly widely held in 1989. U.S. savings bonds were owned by about a quarter of all households in 1989; by 2007 only 15 percent held any. Ownership of certificates of deposit dropped from 20 percent of households to 16 percent. More than one-third of households owned cash value life insurance in 1989; 23 percent owned this sort of life insurance by 2007 – although it was still the fifth most widely held type of asset.

The growing importance of stock ownership is even more pronounced in Table 4-3. In 1989 there were two major household assets: owner-occupied homes and unincorporated or closely-held businesses. Together, they accounted for about half of the wealth of all households, even after subtracting mortgage debt. Stock ownership, direct and indirect, represented about eight percent of household wealth. By 2001, the value of stockholdings was larger than either home equity or unincorporated business, and represented almost a quarter of total family net worth. At the peak of the business cycle in late 2007, stock ownership had receded to a little less than 20 percent of total net worth, less than home equity or unincorporated business, but these three categories were about two-thirds of the total net worth of American households.

Homeowners’ equity declined by about 20 percent between 1989 and 1995, then rose sharply and steadily, doubling between 1995 and 2004, with a small further increase between 2004 and 2007.

On the liability side of the balance sheet, student loan debt increased steadily. The nine percent of households with student loans in1989 owed about $10,000, on average; the 15 percent with loans in 2007 owed $24,000. Student debt offset about one-half of one percent of households’ total assets. Home equity lines of credit (HELOCs) became more common; they represented about four percent of mortgage debt for homeowners by 2001, and have remained at about that share or slightly lower.

The Great Recession and Its Aftermath

Between 1992 and 2007 real mean household wealth doubled, enjoying an annual average growth rate of about 4.5 percent. In the Great Recession, mean wealth dropped by 15 percent, with no recovery after 2010. The decline was almost across the board, in terms of asset categories. The only clear exception was transaction accounts – held by 92 percent of households in 2007 and 93 percent in 2013, and with a $5,000 increase in the mean balance. Ownership of “other residential real estate” increased between 2007 and 2010, but then dropped below the 2007 ownership rate by 2013. The values of assets by category also declined, with the exceptions of retirement assets and managed assets. In almost every asset category, fewer households held the asset and their holdings were less valuable. Possibly on a more positive note, debt holdings also fell, overall and by category, with the single exception of student loans. Between 2007 and 2013, the proportion of households carrying student loans rose from 15 percent to 20 percent, and their average loan balance from $24.000 to about $29,000. The total amount of student debt rose by 25 percent, as Table 4-3 shows, large enough to offset over one percent of household assets.

Despite the continued importance of retirement accounts, stockholders suffered between 2007 and 2010. The average value of their portfolios, including both direct and indirect ownership, declined by about 15 percent between 2007 and 2010 – and there were about one million fewer stockholders.46 There were fewer households directly owning stocks, fewer with mutual fund holdings, and fewer with retirement accounts. The average value in retirement accounts, however, rose by about 10 percent, and there were many more households with retirement accounts than direct stock owners or households with mutual fund holdings, which helped to mitigate the decline in value for all stockholders. The stock market had recovered by 2013, and the number of households owning stock and the average value of their portfolios both rose after 2010,

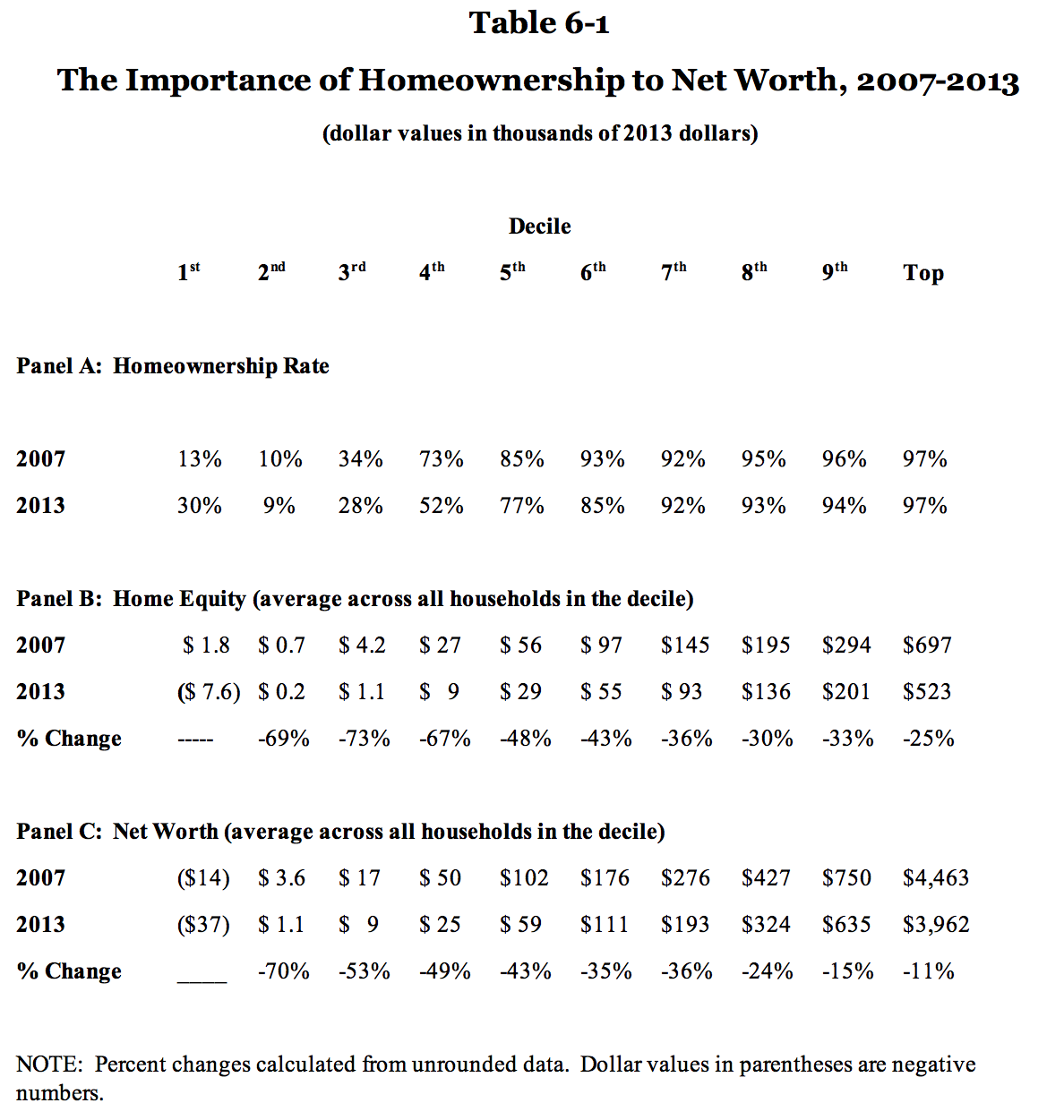

Homeowners were less fortunate. The homeownership rate dropped from 68.6 percent in 2007 to 65.2 percent in 2013,47 and for the first time, the SCF found that home equity was not the largest share of household net worth in 2013. It was a close second to equity in unincorporated business. The dramatic drop by more than one-quarter between 2007 and 2010, and the further decline to 2013, are clear from the “home equity” data in Table 4-3.

For homeowners, their situation was probably worse than the data in Tables 4-2 and 4-3 indicate. Of the 68.6 percent of households who were owners in 2007, 0.5 percent were “underwater,” in their own judgment: the outstanding principal balance on their mortgage or mortgages was greater than their estimated value of their home. By 2010, 64.7 percent were homeowners, and 5.5 percent thought they were underwater. By 2013, 65.2 percent were homeowners and 4.9 percent thought they were underwater. Altogether, 68.1 percent were owners with equity in their home in 2007; 59.2 percent were in 2010; 60.3 percent were in 2013. The average homeowning family lost over one-quarter of the equity in its home over those six years.

The validity of these figures depends on the ability of homeowners to estimate the current market value of their home. The principal balance on their mortgage is typically reported at least annually, along with the amount of mortgage interest paid during the previous year, which is tax-deductible. Other relevant data is available is available from private firms and government agencies. RealtyTrac, a real estate information company, publishes monthly and annual reports on the number of homes that are in the process of foreclosure, using information from county government records. These are homes whose owners are unable or perhaps unwilling to make their monthly mortgage payments. The annual “Year-End U.S. Foreclosure Market Report,” contains the number of homes on which at least one foreclosure notice has been filed during the year.48 In 2007, there were about 1.3 million homes (1.03 percent of the housing stock) on which at least one notice was filed – an 80 percent increase over 2006. In 2010, there were almost 2.9 million homes (2.23 percent of the stock); this was the peak year for foreclosure notices. By 2013, the number of homes was down to about 1.4 million (1.04 percent of the stock). These data do not directly measure the change in homeowners’ equity from year to year, but they correlate with the changes reported in the SCF. Foreclosures and homes with negative equity (as judged by their owners) both increased sharply from 2007 to 2010, and then declined more modestly from 2010 to 2013.

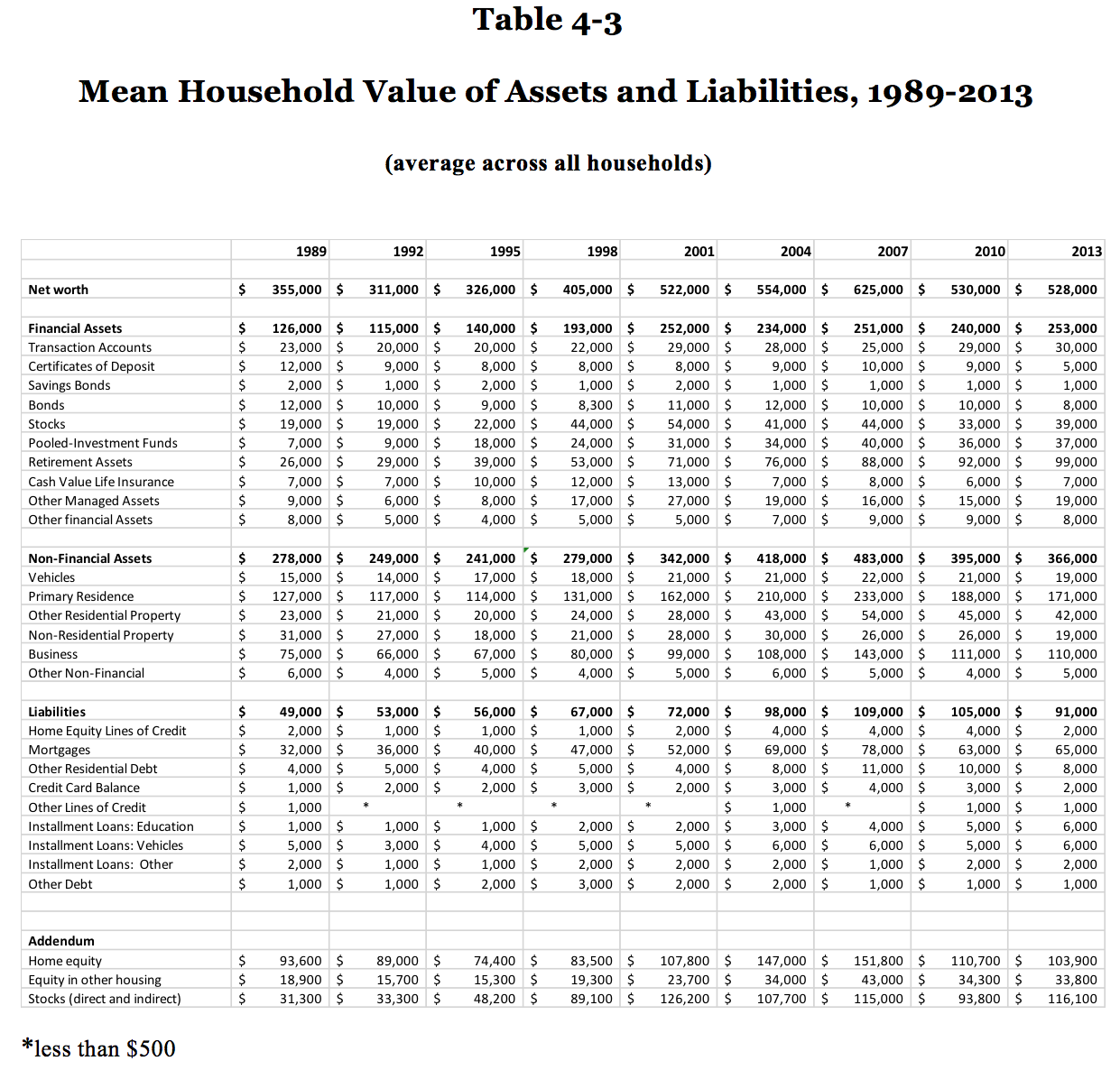

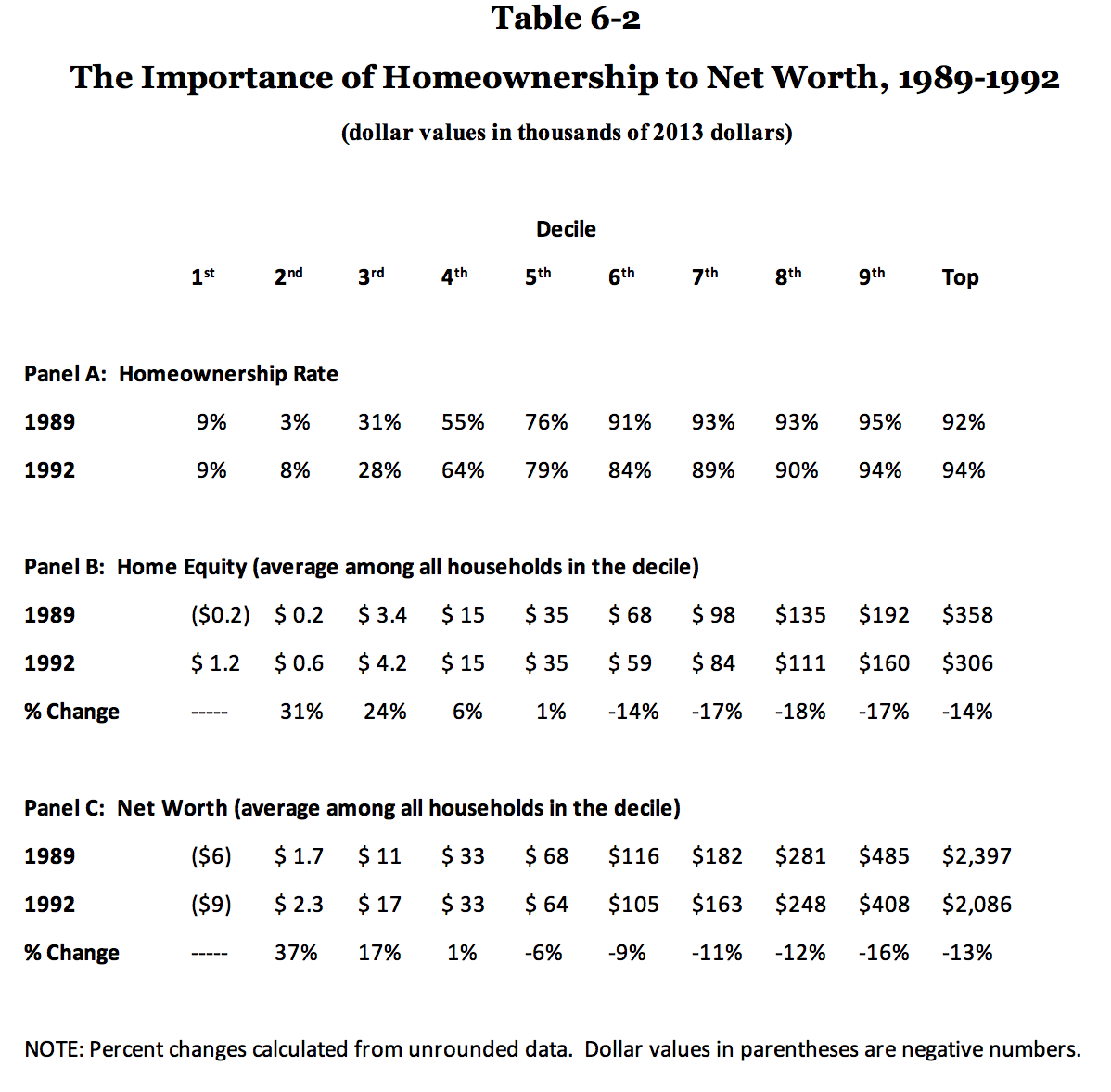

Changes in Household Assets and Debts, 1983-1992

The 1990-1991 recession interrupted some trends. Equity in owner-occupied homes rose by almost 25 percent between 1983 and 1989, but then dropped by over 10 percent through 1995; most of the decline occurred between 1989 and 1992. Similarly, transaction account balances rose by one-third, declined by about 15 percent through 1995, and then began rising again. The same pattern occurred for the values of unincorporated business and vehicles, and on the liability side, for loans to buy vehicles.

In general, however, the changes in assets and debts were not pronounced, either during the 1980s or during the 1989-1992 recessionary period – particularly in the light of what happened after 2007.

“Other” Assets and Debts

The SCF attempts to measure total household net worth, whatever form it may take. To this end, it asks questions about holdings of assets and debts which are held by a small number of households. These are combined in the published categories of “other” assets (separating financial and nonfinancial assets) and debts.

Other Financial Assets. The SCF analysts define “other financial assets” as “a heterogeneous category including such items as oil and gas leases, futures contracts, royalties, proceeds from lawsuits or estates in settlement, and loans made to others.”49

“Other financial assets” as a whole were consistently less than $10,000. In 1989 they amounted to six percent of financial assets and 1.7 percent of net worth. There were the high water marks. By 2013 they amounted to 1.7 percent of financial assets (the lowest value in any survey) and less than one percent of net worth.

Other Nonfinancial Assets. The SCF analysts define “other nonfinancial assets” as “a broad category of tangible assets including artwork, jewelry, precious metals, and antiques.”50 Some other nonfinancial assets are included. As a onetime philatelist, I have noticed that postage stamps are part of the survey, for example, and are in the category of “other.” The same is true of coins. As with “other financial assets,” this category has declined in importance, from 2.2 percent of nonfinancial assets in 1989 to 1.3 percent in 2013, and from 1.5 percent of net worth in 1989 to 0.8 percent in 2013.51

Other Debt. The SCF analysts define “other debt” as “loans on insurance policies, loans against pension accounts, borrowings on a margin account, and other unclassified loans.”52 “Other debt” so defined accounted for 2.3 percent of total debt in 1989 and just over one percent in 2013.53

5. Changes in the Distribution of Wealth, 1983-2013

Measures of Distribution

The distribution of economic well-being is commonly measured in two different ways: measures describing the entire distribution, and measures describing the concentration at one end of the distribution, typically the high end. Each type of measure has strengths and limitations.

The Gini Coefficient

The most common quantitative measure of the entire distribution is the Gini coefficient. It is regularly reported as a measure of the distribution of income in the U.S.; the Census Bureau publishes a Gini coefficient for the distributions of household income and family income each year as part of an annual report on income and poverty, and has been since 1967.54

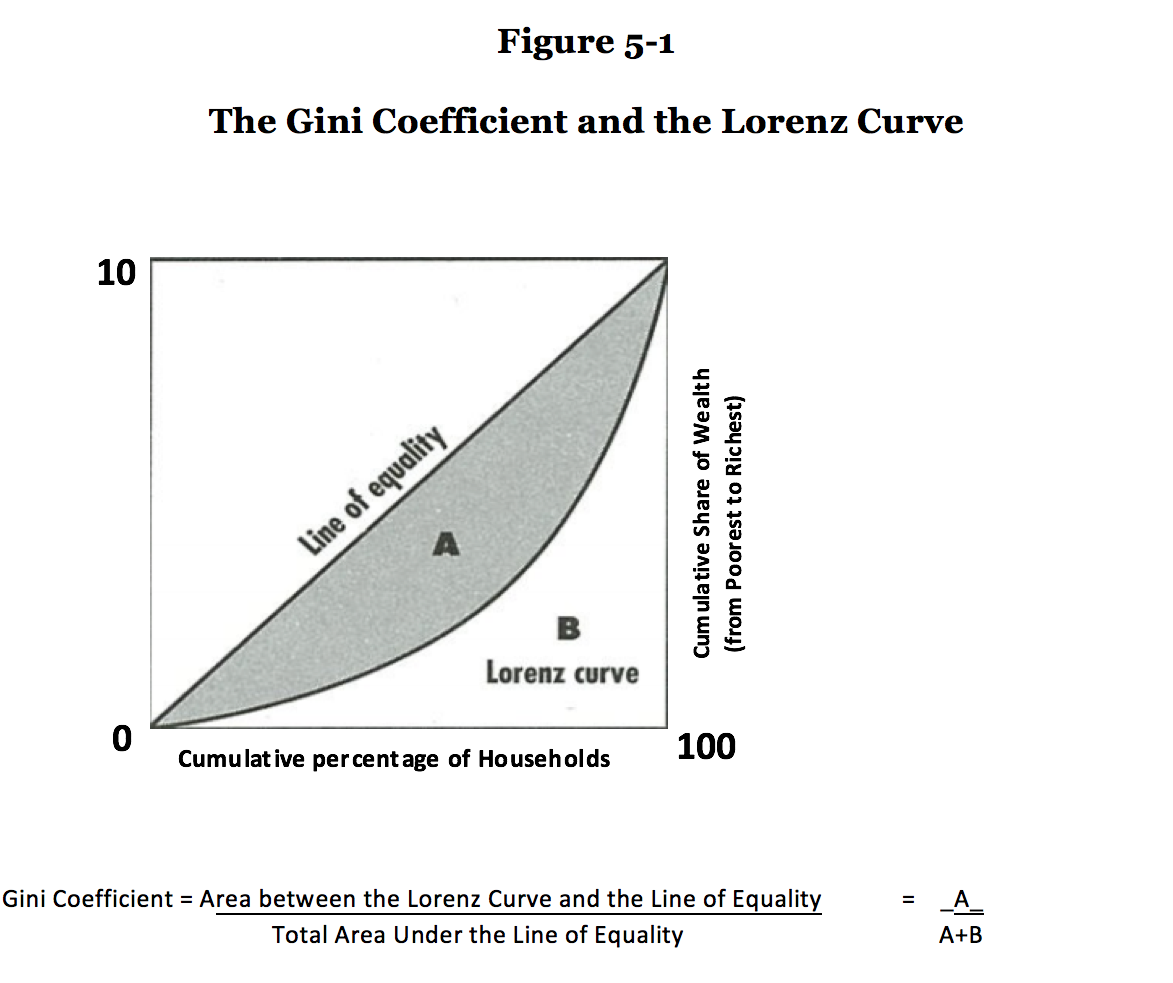

In calculating a Gini coefficient, households or individuals are ranked from the lowest income or wealth to the highest. The cumulative share of total income or wealth is measured against the cumulative share of the population. Figure 5-1 illustrates this ranking. The cumulative share of population is measured along the horizontal axis; the corresponding cumulative share of total income or wealth is measured along the vertical axis.55 The Gini coefficient is measured as the ratio of the area between the diagonal line – indicating a perfectly equal distribution – and the Lorenz curve to the total area under the diagonal line.

The Gini coefficient has a range of 0 to 1. If the distribution of wealth is perfectly equal, the coefficient is zero; if all the wealth in the society is owned by one single household, the coefficient is unity. The greater the concentration of wealth, the closer the Gini coefficient is to unity.

The advantage of the Gini coefficient is that it takes into account changes that occur in any part of the distribution. Its main drawback is that it has no intuitive interpretation, except at the extreme points. A Gini coefficient of 0.5, for example, does not necessarily mean that the society is “halfway between” a perfectly equal and perfectly unequal distribution of wealth, and indeed it is not clear what such a statement means. A coefficient of 0.5, or any other value between the theoretical limits, is consistent with a number of different distributions. Nor is it possible to explain the meaning of a Gini coefficient in terms of any other measure. All that can be said is that higher coefficients indicate greater inequality.56

Concentration Ratios

Measures of concentration have become more common in recent years, for several reasons. The ownership of wealth is highly skewed, compared to income or other measures of economic well-being, so the shares held by the richest one percent or ten percent of all households attract attention. Such concentration ratios are easy to calculate and intuitively easy to understand.

The main limitation of concentration ratios is that they only describe part of the distribution of wealth. Changes in net worth for “the wealthy” may not correspond to changes in the opposite direction for any other particular subset of the population (for example, “the poor”), and conversely changes may occur for these groups without any corresponding changes among the rich. Nor is there anything inherently significant in any particular concentration ratio: the highest one percent, five percent, ten percent, or any other share.

The SCF provides information about all households, not only about the wealthy. It can therefore be used to measure both the overall distribution of wealth and the share held by “rich” or “poor” (however defined) American households.

Changes in the Distribution of Wealth, 1989-2013

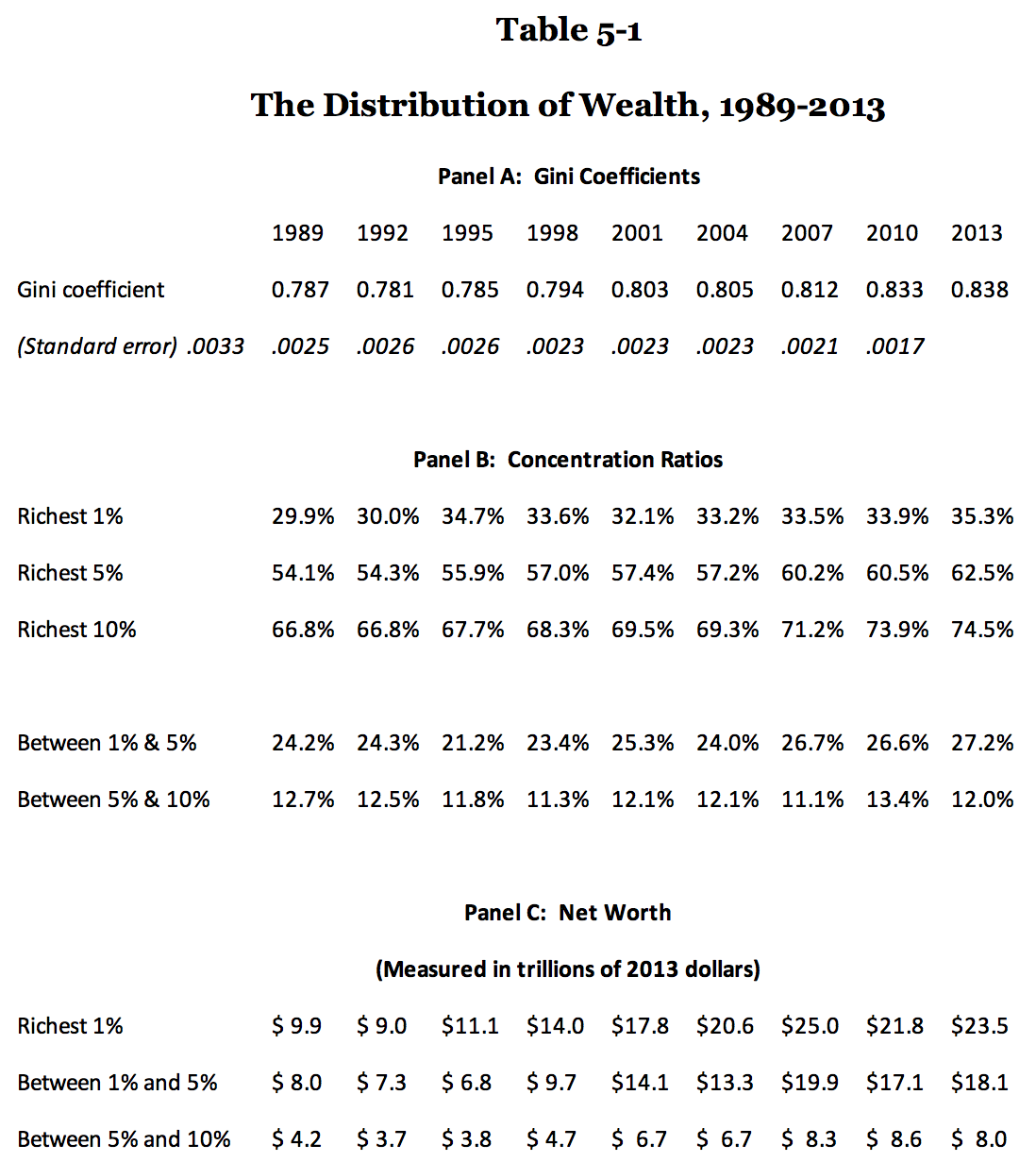

Table 5-1 reports the changes in the overall distribution of wealth and in the share held by the richest households between 1989 and 2013. The Gini coefficient declined slightly from 1989 to 1992, then increased in each three-year period through 2013. The table also shows the standard errors for the coefficients. The largest and most statistically significant increase occurred between 2007 and 2010 – covering the onset of the Great Recession through the first stages of the subsequent recovery. There were also statistically significant – but much smaller – increases in 1995-1998, 1998-2001, and 2010-2013. Otherwise, the change in inequality was smaller and not significant from one survey to the next. Over longer periods, however, the changes were significant.57

The table also shows the concentration of wealth among the richest households, by several criteria: the richest one percent, the richest five percent, and the richest 10 percent, and also for the households between these cutoffs: between one percent and five percent, and between five percent and 10 percent. These all show little or no increase from 1989 to 1992. After 1992 the shares for the richest one percent, five percent, and 10 percent generally increased, with the largest increase for the richest one percent occurring between 1992 and 1995. Through 2007, the share of the richest one percent tended to increase more than the shares of those between one percent and 10 percent, and for that matter more than the share of the rest of the population. But around the end of in the Great Recession, between July and December 2009, the Federal Reserve conducted a follow-up survey of those households that had been interviewed in 2007. In a report on the changes between 2007 and 2009, Kennickell noted that “the share of the wealthiest one percent of households has shown no significant change since 1995,” in comparison to 2007; and added that between 2007 and 2009 the share of total wealth owned by the richest one percent of households had declined by four percentage points, from 33 percent of total wealth to 29 percent.58

The richer got richer between 1992 and 2007, but the poor did not get poorer. In 1992, the total real wealth for the lower half of U.S. families was about $860 billion; in 2007, their total real wealth was about $1.6 trillion.59 Real mean wealth per family increased from about $18,000 to about $28,000. Their share did not increase, rather the reverse – they held 3.3 percent of total net worth in 1992, compared to 2.5 percent in 2007 – but their actual wealth did.

Between 2007 and 2013, this pattern changed. The poor became poorer, but so did the rich and the people in between. The rich were less affected, however. The top 10 percent lost a smaller share of their 2007 wealth than the remainder of the population. The richest 10 percent of households lost about seven percent of their net worth – $3.6 trillion out of $52.2 trillion. The remaining 90 percent of households lost about 22 percent of their net worth – $4.3 trillion out of $19.4 trillion. Indeed, as these figures show, the top 10 percent lost a smaller amount, not just a smaller share, than the remaining 90 percent.60 As of 2010, the share of wealth owned by the richest one percent had risen to 34 percent. share of the richest 1% show that two of the four 1983-1989 increases and one of the two 1989-1992 decreases were statistically significant. For the full period, one comparison shows an insignificant increase in concentration and the other shows a decrease that is almost significant.61

Changes in the Distribution of Wealth, 1983-1992