Rising Rents And Cheap Money Flowing: Apartment Prices Are Soaring – OpEd

By MISES

By Doug French*

Fannie Mae announced last week that it provided nearly $70 billion in multifamily financing last year. The government lender crowed about $9.6 billion of the total being for affordable housing projects and $13.5 billion financing projects deemed “green and sustainable” units. This helped Fannie “grow its Multifamily Green MBS (mortgage backed securities) issuance to more than $100 billion last year,” according to the press release.

Fannie Mae apartment loan pricing and terms are attractive: the five-year fixed rate starts at 2.74 percent to the thirty-year fixed starting at 3.81 percent. Thirty-year amortizations are available and in some cases interest-only loans can be negotiated, as well as nonrecourse loans. The larger point is that with the Consumer Price Index at 7 percent in December, the real interest rate on these Fannie Mae loans is negative.

According to Multi-Housing News, “On an annual basis through December, rents increased by double-digit percentages in 26 of the top 30 metros, six of which posted gains of 20 percent or more: Phoenix (25.3 percent), Tampa (24.6 percent), Miami (23.5 percent), Orlando (22.7 percent), Las Vegas (22.2 percent) and Austin (20.9 percent).”

So with rents rising and cheap money flowing, the prices of apartment projects are soaring. The latest Las Vegas multifamily announced sale is Ideal Capital Group’s purchase of the 287-unit Jade project near the Rio hotel and casino for $124.5 million. That is a whopping $433,798 per unit.

The covid shutdown in 2020 slowed project sales as many renters lost their jobs. But “Las Vegas’ rental market has since heated up with fast-rising rents and shrunken availability, in part as people sought more space amid widespread work-from-home arrangements, and investor sales have rebounded,” reports Eli Segall for the Las Vegas Review-Journal.

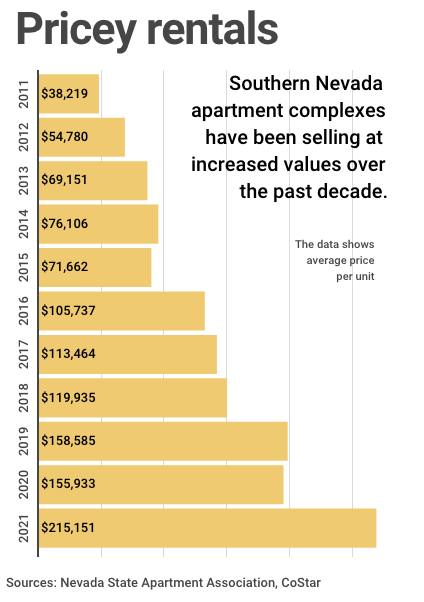

Jade went for double 2021’s average sales price per unit, $215,151. Average apartment sales per unit have risen over 460 percent, from $38,219 in 2011 to last year’s price.

Wolf Richter writes on his site, wolfstreet.com, that working people are harmed by inflation because their wages never catch up, while people with assets, inflated in value by low interest rates, reap the benefit. He writes, “[T]he wealth of the wealthiest 1% of households spiked, creating the biggest and worst wealth disparity ever to the bottom 50% and even to the bottom 99%, based on the Fed’s own wealth distribution data.”

Over lunch recently I expressed my astonishment over the $400,000-per-unit sales to a developer (and apartment project owner) I used to bank. He told me units would be selling for $500,000 by the end of this year.

I said rents would have to jump even more or capitalization rates would have to go to virtually nil for that to happen. He said emphatically, “Rents are going up.” People moving in from California believe rents in Vegas are cheap.

Not for long.

*About the author: Douglas French is President Emeritus of the Mises Institute, author of Early Speculative Bubbles & Increases in the Money Supply, and author of Walk Away: The Rise and Fall of the Home-Ownership Myth. He received his master’s degree in economics from UNLV, studying under both Professor Murray Rothbard and Professor Hans-Hermann Hoppe.

Source: This article was published by the MISES Institute