The Conquest Of Israeli Inflation, Its Benefits And Current Policy Dilemmas – Analysis

By VoxEU.org

Central banks are there to ensure price stability, and economists generally agree that politics and central banking don’t mix well. This column takes us through the inflationary and more controlled history of Israel’s central bank, highlighting the current policy dilemmas facing the country.

By Alex Cukierman*

There is currently a wide consensus that, excluding episodes of financial crisis, the main objective of a modern central bank is price stability and that, to achieve this objective, the central bank should be sufficiently independent from political authorities. The Bank of Israel was founded in 1954 and was dominated by political authorities at least during its first 30 years of its existence. In parallel, the first four to five decades following the Bank’s foundation were characterised by inflation rates above the current 2% international norm, at times very much above.

Following a successful heterodox stabilisation programme in July 1985, and after a prolonged gradual stabilisation that followed, Israel finally reached the current 2% price stability benchmark at the beginning of the 21st century. From 1985 the actual independence of the Bank of Israel gradually increased. During those years, legal independence lagged behind actual independence (Cukierman 2007). This gap was finally closed by a substantial increase in the legal independence of the Bank in 2010.

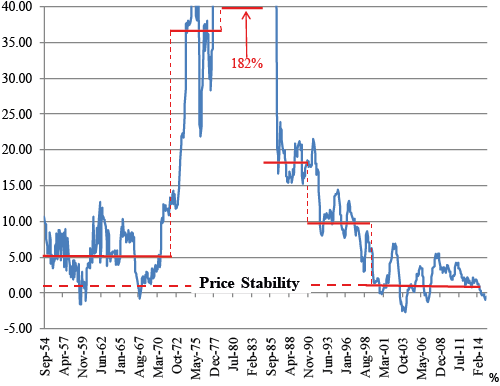

During the first 45 years of the Bank’s existence, both the average level and the variability of inflation went through dramatic changes in both upward and downward directions. For the entire period the average 12-month inflation rate (measured each month as the 12-month rate of inflation since the same month in the previous year) was 31%. It fluctuated between a maximum of 486% just prior to the 1985 cold turkey stabilisation and a minimum of almost minus 3%. However, those summary statistics hide very different inflation environments.

Figure 1 provides a bird’s eye view of inflation in Israel from the creation of the Bank until April 2015. The blue line shows actual inflation each month at yearly rates. The Figure divides the 61 years between the creation of the Bank of Israel and April 2015 into six sub-periods, in line with the nature of the inflationary process. Within each sub-period the rate of inflation fluctuates around a sub-period mean marked by a horizontal red line. Eyeballing of the figure suggests that those means differ substantially across sub-periods. Three of those are prior to the July 1985 inflation stabilisation and the remaining three after it.1 It appears that the 1985 stabilisation constitutes a watershed in the sense that prior to it sub-periods’ inflation means are increasing over time while, after it, they are decreasing.

Changes in the real effects and costs of inflation across sub-periods

Fischer and Modigliani (1978), Leijonhufvud (1977) and others have stressed the costs and consequences of inflation through its effects on various real variables. The variety of inflation experiences since the establishment of the Bank of Israel provides a natural laboratory for the investigation of changes in the real effects and costs of inflation across different inflation environments. The evidence shows that there are substantial differences between the five inflationary sub-periods and the more recent price stability period. Among those are dramatic changes in the anchoring of inflation expectations, in the pass-through from changes in the exchange rate to domestic inflation, in inflation uncertainty, the speed of price adjustments, relative price variability, the (rather late) disappearance of dollarisation in the real estate market, and the benefits induced by price stability for financing of the public debt. There also are significantly positive relationships across sub-periods between inflation on one hand and each of the following: inflation variability, inflation uncertainty and relative price variability.2 Price stickiness is negatively related to inflation inducing a positive relationship between inflation and the pass-through from changes in the exchange rate and domestic inflation. Between the triple digit inflation of the early eighties and the price stability period of the twenty first century the pass-through coefficient decreased from around 1.0 to 0.1.

Two types of stabilisations: A cold turkey followed by a gradual stabilisation programme

Price stability was achieved through two very different types of stabilisations. The triple-digit inflation of the early 1980s was reduced to the low double-digit range in one shot in July 1985. The remaining low double-digit inflation was stabilised gradually during the last decade of the twentieth century.

The difference between the pre- and post-1985 nature of the inflationary process cannot be overemphasised. The first era was dominated by the needs of the new state of Israel to absorb large waves of immigration, to maintain effective defences against hostile neighbours, and to provide the funds necessary to finance capital formation against the background of an underdeveloped private capital market. As a consequence, the price stability objective took a back seat and fiscal policy dominated aggregate demand policies. By contrast, following the 1985 cold turkey stabilisation, the price stability objective rose into prominence. After the correction of the fundamental fiscal imbalances as a key component of the 1985 stabilisation programme, fiscal dominance was substantially curtailed, controls over international capital flows were gradually dismantled, and the exchange rate was gradually flexibilised, culminating in a fully floating exchange rate in 2005.3

The stabilisation of the remaining low double-digit inflation gradually replaced the previous exchange rate anchor with an inflation target anchor over the 1990s. The target was initially set at relatively modest (high inflation) levels so as to avoid the need to create large recessions in order to build up the credibility of the target. When the pre-announced target was achieved a more ambitious, lower target was jointly announced by government and the central bank. The monetary measures of the 1990s fit well into the mould of the ‘opportunistic approach to disinflation’. This approach is succinctly summarised by Blinder (1994) as follows:

“Proponents of this approach hold that when inflation is moderate but still above the long-run objective, the Fed should not take deliberate anti-inflation action, but rather should wait for external circumstances such as favourable supply shocks and unforeseen recessions to deliver the desired reduction in inflation. While waiting for such circumstances to arise, the Fed should aggressively resist incipient increases in inflation“.4

The large Russian immigration of the early 1990s provided the Bank of Israel with a positive supply shock it could take advantage of in order to effectively reduce the target, as well as actual inflation, by maintaining the real rate at a sufficiently high level.

Consequences of price stability for dollarisation and government finances

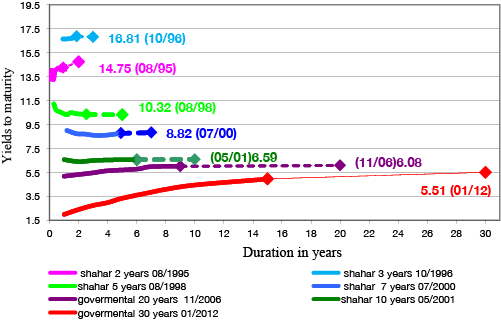

During all five inflationary sub-periods, prices in the rental and real estate markets were quoted in US dollars. Interestingly, high levels of dollarisation in this market prevailed for a good number of years after the onset of price stability at the beginning of the 21st century. But dollarisation virtually disappeared within a couple of years once the domestic currency started to appreciate vis-a-vis the dollar and Israel entered a period of persistent increases in the real estate prices in 2007. The arrival of price stability was highly beneficial for government finances. For the first time since its creation the state of Israel was able to issue unindexed long-term debt (known as ‘Shahar’ bonds) at gradually increasing maturities and decreasing nominal and real interest rates.

An early un-indexed nominal government bond with a maturity of two years (Shahar) was issued in August 1995, soon to be followed by the issuance of a three-year Shahar bond in October 1996. As the drive toward price stability gathered momentum and credibility, the maturity of new issues gradually became longer and the yields to maturity on new issues gradually went down. Figure 2 documents this process. It shows the yield curves on the dates of first issues of successively longer term nominal government bonds and their yields to maturity on the day of issue. The first five-year Shahar bond was issued in October 1998, followed by a seven-year bond in July 2000. The first ten-year nominal bond was issued in May 2001 and the first 20-year bond in November 2006. After ten years of price stability, the Israeli treasury even issued a 30-year bond in January 2012. Those tendencies were reinforced by the decrease in rates in the US and in Europe following the onset of the global financial crisis.

The impact of stabilisation on the anchoring of inflation expectations

During the decade from the mid-1990s to 2004/5 inflation declined from the 13% range to the 2% range. As we have seen, this process was partly achieved through the establishment and strengthening of the IT regime. At the outset the target was relatively high reflecting the view that, within this range of inflation rates, gradual stabilisation of inflation is preferable to cold turkey. But once the central bank managed to maintain inflation sufficiently close to the target for some time the target was gradually adjusted downward. Between 1994 and 1998 the target was at least 8%. It was reduced to 4% at the beginning of 1999. From the beginning of 2000, the target was reduced further in small steps of half a percent, finally converging to the current long-term target of 2% at the beginning of 2003.

An important function of a pre-announced inflation target is to affect inflation expectations up-front in order to reduce the real costs of stabilisation. Once the long-term inflation target is reached, the main function of the pre-announced inflation target is to anchor inflation expectations tightly to the target. The extent to which expectations are well-anchored depends on the credibility of the pre-announced target. The credibility of the target depends, in turn, on how well the central bank has done in keeping actual inflation near the target in the past. Tight anchoring of inflationary expectations to the target is essential for the efficiency of monetary policy since expectations have a first order effect on actual inflation.

To examine empirically the extent to which the anchoring of expectations to the target has changed upon the onset of price stability we postulate that, in each month, the one-year ahead expected inflation is a weighted average (with weights that sum up to one) of the existing target and of actual inflation over the previous 12 months.5 When the pre-announced target is fully credible expectations are equal to the target. When it has no credibility at all expectations are based only on actual past inflation developments. Between those two extremes there is a whole range of partial credibility/anchoring cases in which the public forms its expectation based on both the pre-announced target and actual past inflationary developments.6 The coefficient on the inflation target characterises the credibility of the target. The closer it is to one the higher is credibility and the better is the anchoring of inflationary expectations. It is therefore referred to in the sequel as the ‘anchoring parameter’.

Regressions analysis reveals that the anchoring parameter increases dramatically from 0.50 to 0.84 between the last inflationary sub-period and the price stability era. As a matter of fact, since the end of 2003 the anchoring parameter is not significantly different from one – the full anchoring benchmark. This can be rightly considered as one main payoff for the high interest rate policies maintained during a large part of the 1990s. It is consistent with the view that credibility cannot be earned by simply preannouncing a target. Credibility is established only after demonstration of the fact that actual inflation is held close to the target for a sufficient length of time.

Current monetary policy dilemmas

Israel is a highly open small economy with strong dependence on foreign trade. Its forex market is small in comparison to world forex markets.7 As a consequence, short- and medium-term capital flows motivated by developments abroad, interest rate differentials and geopolitical events, even if small by world standards, have substantial effects on the effective exchange rate. This, along with the fact that inflation differentials between Israel and its major trading partners have been negligible since the onset of price stability, implies that capital flow-induced changes in the exchange rate may translate into substantial fluctuations in the real exchange rate.

This is rather disruptive for foreign trade in general and for the competitiveness and viability of Israeli exports and employment. This tendency has been reinforced by the recent low interest rate policies of the US and of Europe, which are Israel’s main trading partners. This forced the Bank of Israel to gradually reduce its key interest rate to the vicinity of the zero lower bound and to occasionally intervene in the forex market.

In parallel this policy encouraged mortgage borrowing and reinforced a continuous trend of rising real estate prices that had started in 2007. This trend is undesirable for both systemic stability and equity reasons. This dilemma has been a central issue in monetary policy in recent years. To alleviate those problems, the Bank has been relying on various macro-prudential instruments.

Since roughly the beginning of 2014, inflation has been lower than the lower bound of the inflation target range (the target range is between 1 and 3%). During the last year it even was mostly in negative territory, though due primarily to supply shocks that are expected to have a temporary effect on inflation. The recent emergence of negative inflation rates raised an issue that has been dormant during the entire existence of the Bank of Israel – given the state of the real economy, should the Bank lean against inflation rates below the lower bound of the IT range with the same determination and speed that it applies to leaning against inflation when the latter is above the upper bound of the target range? There are differing opinions on this issue. My own feeling is that the optimal policy response to a given deviation of inflation below the lower bound of the target range may well be smaller than the optimal response to an a similar (in absolute values) upward deviation of inflation from the upper bound of the target range.

About the author:

*Alex Cukierman, Professor emeritus, Tel Aviv University; Professor of Economics, Interdisciplinary Center; CEPR Research Fellow

References:

Bai, J and P Perron (1998), “Estimating and testing linear models with multiple structural changes”, Econometrica 66(1): 47–78.

Blinder, A S (1994), “Prepared Statement”, nominations of Alan S Blinder, Steven M H Wallman and Phllip Diehl, Hearing before Committee on Banking, Housing, and Urban Affairs.

Cukierman, A (2007), “De jure, de facto, and desired independence: the Bank of Israel as a case study” in N Liviatan, H Barkai (eds.), The Bank of Israel, Vol. II: Selected Topics in Israel’s Monetary Policy, Oxford University Press, Oxford, pp. 3–45.

Cukierman, A and N Liviatan (1991), “Optimal accommodation by strong policymakers under incomplete information”, Journal of Monetary Economics 27: 99–127.

Cukierman A and R Melnick (2015), “The Conquest of Israeli Inflation and Current Policy Dilemmas”, CEPR DP 10955, November.

Fischer S and F Modigliani (1978), “Towards an understanding of the real effects and costs of inflation”, Weltwirtschaftliches Archiv, Band 114, pp. 810–833.

Leijonhufvud, A (1977), “Costs and consequences of inflation” in G Harcourt (ed.) Microeconomic Foundations of Macroeconomics, Proceedings of an IEA conference, London.

Melnick R and T Strohsal (2015), “From Galloping Inflation to Price Stability in Steps: Israel 1985–2013”, SFB 649 Discussion Paper 2015-009, Freie Universität Berlin, Germany.

Orphanides A and D W Wilcox (2002), “The opportunistic approach to disinflation”, International Finance, 5(1): 47–71.

Endnotes:

1 With an average inflation of 182% the subperiod just preceding the 1985 stabilisation is way outside Figure’s 1 scale. This fact is marked by a vertical red arrow pointing up. Using a statistical methodology suggested by Bai and Perron (1998), Melnick and Strohsal (2015) characterise the three post-July 1985 periods as inflation ‘steps’. One formal requirement from an inflation step is that there be no serial correlation between the deviations of actual inflation from the mean inflation of the step.

2 Inflation variance and inflation uncertainty are distinct concepts since part of future inflation variability is generally anticipated in advance. Correspondingly inflation variance is measured as the mean square deviation of actual inflation from its mean whereas inflation uncertainty is measured as the mean square deviation of actual inflation from its ex ante forecasted value.

3 Most of this flexibilisation had already been achieved by 1998.

4 An early formal treatment of this strategy appears in Orphanides and Wilcox (2002).

5 The empirical measure of inflationary expectations is the difference between the yield to maturity on a one year nominal bond and a one year ahead indexed bond also known as a ‘breakeven expectation’

6 This is an empirical adaptation of a partial credibility/anchoring model from Cukierman and Liviatan (1991). Further details appear in Cukierman and Melnick (2015).

7 Since the early twenty first century Israel has a persistent surplus in the current account of the balance of payments