What Determines A Currency Exchange Rate? – Analysis

By Frank Shostak*

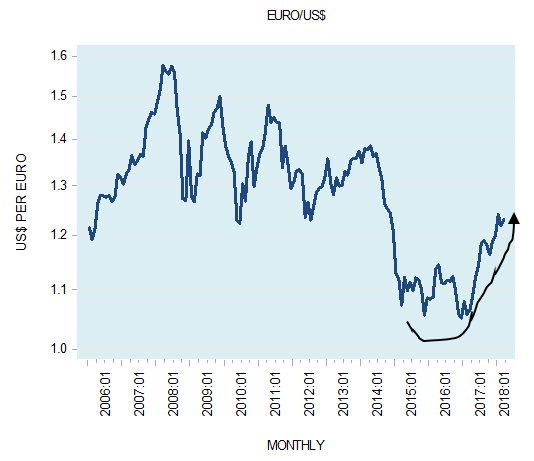

After closing at 1.051 at the end of December 2016, the price of the Euro in US dollar terms settled at 1.2321 at the end of March this year – an increase of 17.2%.

But, a currency exchange rate appears to be moving in response to so many factors that it makes it almost impossible to ascertain where the exchange rate is likely to be headed.

Rather than paying attention to the multitude of variables, it is more sensible to focus on the essential variable.

As far as the currency exchange rate determination is concerned, the essential variable is the relative changes in the purchasing power of various monies. The relative purchasing power of various monies sets the underlying exchange rate.

As far as the currency exchange rate determination is concerned, the essential variable is the relative changes in the purchasing power of various monies. The relative purchasing power of various monies sets the underlying exchange rate.

A price of a basket of goods is the amount of money paid for the basket. We can also say that the amount of money paid for a basket of goods is the purchasing power of money with respect to the basket of goods.

If in the US, the price of a basket of goods is one dollar and in Europe, an identical basket of goods sold for two euros, then the rate of exchange between the US dollar and the euro must be two euros per one dollar.

The Money Supply

An important factor in setting the purchasing power of money is the supply of money. If over time the growth rate in the US money supply exceeds the growth rate of European money supply, all other things being equal, this will put downward pressure on the US dollar versus the euro.

Since a price of a good is the amount of money per good, this now means that the prices of goods in dollar terms will increase faster than prices in euro terms, all other things being equal.

As a result, an identical basket of goods is priced now; let us say at two dollars, as against 2.5 euro. This would imply that the exchange rate between the US dollar and the euro would be now 1.25 euros per one dollar.

Note the fact that changes in a local money supply affect its general purchasing power with a time lag means that changes in relative money supply affect the currency exchange rate also with a time lag.

When money injected into the economy it starts with a particular market before it goes to other markets – this is the reason for the time lag.

When it enters a particular market, it pushes the price of a good in this market higher – more money spent on given goods than before.

This in turn means that past and present information about money supply can be employed in ascertaining likely future moves in the currency exchange rate.

The Demand for Money

Another important factor in driving the purchasing power of money and the currency exchange rate is the demand for money. For instance, with an increase in the production of goods the demand for money will follow suit.

The demand for the services of the medium of exchange is going to increase since more goods are going to be now exchanged. As a result, for a given supply of money, the purchasing power of money is going to increase. Less money will be chasing more goods now.

Likewise, the demand for money is going to increase because of a general increase in prices of goods and services.

Interest Rates

Various factors, such as the interest rate differential, can cause a deviation of the currency rate of exchange from the level dictated by relative purchasing power. Such deviations, however, will set corrective forces in motion.

Let us say that the Fed raises its policy interest rate while the European central bank keeps its policy rate unchanged.

We have seen that if the price of a basket of goods in the US is one dollar and in Europe two euros, then according to the purchasing power framework the currency exchange rate should be one dollar for two euros.

As a result of a widening in the interest rate differential between the US and the Euro zone an increase in the demand for dollars pushes the exchange rate in the market toward one dollar for three euros.

This means that the dollar is now overvalued as depicted by the relative purchasing power of the dollar versus the euro.

In this situation it will pay to sell the basket of goods for dollars then exchange dollars for euros and then buy the basket of goods with euros — thus making a clear arbitrage gain.

For example, individuals will sell a basket of goods for one dollar, exchange the one dollar for three euros, and then exchange three euros for 1.5 basket, gaining 0.5 of a basket of goods.

The fact that the holder of dollars will increase his/her demand for euros in order to profit from the arbitrage will make euros more expensive in terms of dollars — pushing the exchange rate in the direction of one dollar for two euros. An arbitrage will always be set in motion if the exchange rate deviates, for whatever reasons, from the underlying exchange rate.

We have seen that the interplay between the supply and the demand for money sets a currency purchasing power, which in turn determines its exchange rate against the other currency.

The interplay between the supply and the demand for money can be depicted by the excess money growth differential. This differential is established as the difference between the yearly growth rate of money supply and the yearly growth rate of nominal economic activity.

The difference between the excess money growth differential of the US and the EMU sets the underlying exchange rate of the euro in terms of the US dollar.

For example, after closing at 12.5% in August 2011 the difference between the excess AMS growth differential of the US and the EMU settled at minus 8% by February this year.

A visible downtrend in the difference implies a relative underlying strengthening in the purchasing power of the US dollar against the euro. (Relatively to demand for money the growth rate of money supply in the US is much weaker than in the EMU). This in turn raises the likelihood that as time goes by the US dollar should strengthen against the euro.

About the author:

*Frank Shostak‘s consulting firm, Applied Austrian School Economics, provides in-depth assessments of financial markets and global economies. Contact: email.

Source:

This article was published by the MISES Institute.

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!