Japan Energy Profile: World’s Largest LNG Importer – Analysis

By EIA

Japan has limited domestic energy resources that have met less than 10% of the country’s total primary energy use each year since 2012. Japan’s domestic energy resources met more than 20% of the country’s total primary energy use before the removal of nuclear power following the Fukushima plant accident.1 Japan is the third largest oil consumer and net importer in the world behind the United States and China. Furthermore, Japan also ranks as the world’s largest importer of liquefied natural gas (LNG) and the third-largest importer of coal behind India and China.

The country’s lack of sufficient domestic hydrocarbon resources has led Japanese energy companies to actively participate in upstream oil and natural gas projects overs as by providing engineering, construction, financial, and project management services for energy projects around the world. Japan is one of the major exporters of energy-sector capital equipment and has a strong energy research and development (R&D) program supported by the government. This program pursues domestic energy efficiency measures to increase the country’s energy security and to reduce carbon dioxide (CO2) emissions.

In March 2011, a 9.0 magnitude earthquake struck off the coast of Sendai, Japan, triggering a tsunami and causing serious damage at the Fukushima-Daiichi nuclear reactors. The damage to Japan’s energy infrastructure resulted in an immediate shutdown of about 10 gigawatts (GW) of nuclear electric generating capacity. The plants that were not immediately damaged were gradually shut down as a result of scheduled maintenance and lack of government approvals to return to operation. For nearly two years between mid-2013 and mid-2015, Japan suspended nuclear power generation for the first time in more than 40 years. Starting at the end of 2015, electric utilities received the necessary approvals to recommission a few reactors. Public opposition to nuclear power post-Fukushima and delays in the approval process create uncertainty as to the timing and degree to which Japan can revive its nuclear sector and the role nuclear power generation will play in the long-term future of the country.2

Nuclear power generation in Japan represented about 27% of the power generation prior to the 2011 earthquake, and it was one of the country’s least expensive sources of electric power. Japan replaced the significant loss of nuclear power with generation from imported natural gas, low-sulfur crude oil, fuel oil, and coal. This substitution of more expensive fossil fuels led to higher electricity prices for consumers, higher government debt, and revenue losses for electric utilities.

Japan imports virtually all its fossil fuels. Japan spent an additional annual average of approximately $30 billion for fossil fuel imports in the three years following the Fukushima accident. The yen’s depreciation against the U.S. dollar and soaring natural gas and oil import costs resulting from a greater reliance on fossil fuels and sustained high international oil prices through the first half of 2014 continued to deepen Japan’s trade deficit. The trade balance reversed from a 30-year trade surplus, which was $65 billion in 2010, to a deficit that reached a record $116 billion (12.8 trillion yen) in 2014. The low oil and natural gas price environment since late 2014 has helped to ease the trade deficit to $22 billion (2.8 trillion yen) in 2015 and has provided some financial relief for Japanese utilities.3

Japan’s current government intends to resume using nuclear energy as a baseload power source with necessary safety measures. The government believes the use of nuclear energy is necessary to reduce current energy supply strains and high energy prices faced by Japan’s industries and end users. The government’s new energy policy, issued in April 2014, emphasizes energy security, economic efficiency, emissions reduction, and safe use of nuclear power. Key goals and plans to balance the country’s fuel portfolio include strengthening the share of renewable and alternative energy sources, diversifying from oil to reduce dependence in the transportation sector, and developing advanced and efficient generation technologies for fossil fuel use.4 These efforts occur in the context of the government’s goal to reverse more than two decades of economic stagnation in Japan and its goal to provide economic revitalization through public infrastructure spending, monetary easing, labor market reform, and business investment.

Total primary energy consumption

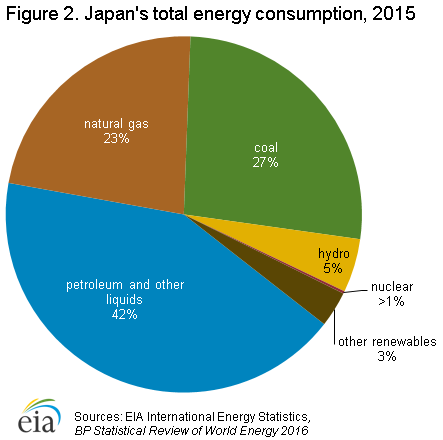

In the wake of the Fukushima nuclear incident, Japan’s energy fuel mix shifted as natural gas, oil, and renewable energy now provide larger shares and supplant some of the nuclear fuel. Oil remains the largest source of primary energy in Japan, although its share of total energy consumption has declined from about 80% in the 1970s to 42% in 2015. The decline in oil use occurred as a result of increased energy efficiency and the increased use of other fuels. Coal continues to account for a significant share of total energy consumption, although natural gas is increasingly important as a fuel source and has been the preferred fuel of choice to replace the nuclear shortfall. The share of natural gas was 23% of total primary consumption in 2015.5 Before the 2011 earthquake, Japan was the third-largest consumer of nuclear power in the world, after the United States and France, and nuclear power accounted for about 13% of the country’s total energy in 2010. By 2013, the country used virtually no nuclear energy. Hydroelectric power and other renewable energy sources comprise a relatively small portion of total energy consumption in the country, although renewable energy, particularly solar power, is growing as an alternative fuel source.

The Japanese government’s policy has emphasized increased energy conservation and efficiency and a lower dependency on oil imports. The government generally aims to reduce the share of oil consumed in its primary energy mix. Among the large developed world economies, Japan has one of the lowest energy intensities, as high levels of investment in R&D of energy technology since the 1970s have substantially increased energy efficiency.

Petroleum and other liquids

Japan was the fourth-largest petroleum consumer and third-largest net petroleum importer in the world in 2016. The country relies almost solely on imports to meet its oil consumption needs because Japan’s oil resources are limited.

Japan has limited domestic proved oil reserves, totaling 44 million barrels as of January 2016, according to the Oil & Gas Journal (OGJ).6 Japan’s domestic oil reserves are concentrated primarily along the country’s western coastline. Offshore areas surrounding Japan, such as the East China Sea (ECS), also contain oil and natural gas deposits. However, development of these zones is held up by competing territorial claims with China. The two countries reached an accord in 2008 to jointly explore four natural gas fields and equally invest in the development of two fields—Chunxiao/Shirakaba and Longjing/Asunaro. Since the agreement was signed, the countries have continued unilateral actions in attempts to develop the natural gas fields.

Tensions escalated with territorial claims by Japan in 2012, with Chinese ships entering in the contested area, and with China’s unilateral declaration of an air defense zone covering much of the ECS in 2013. These disputes have continued through 2016 as China increased the number of vessels in Japanese-claimed waters and as Japan formally complained to China about its recent activities.7

As a result of its significant supply and demand gap, Japan relies almost entirely on imports to meet its oil consumption needs. Japan maintains government-controlled oil stocks to guard against a supply interruption. According to the International Energy Agency, Japan has more than 412 million barrels of total strategic crude oil stocks as of October 2016. About 74% of this amount consisted of government stocks, and 26% were commercial stocks.8 Japan has also signed agreements with oil-producing countries including Saudi Arabia and the United Arab Emirates in recent years that involve Japan lending crude oil storage to these countries, with Japan having a priority to purchase the oil in the event of a serious supply disruption.9

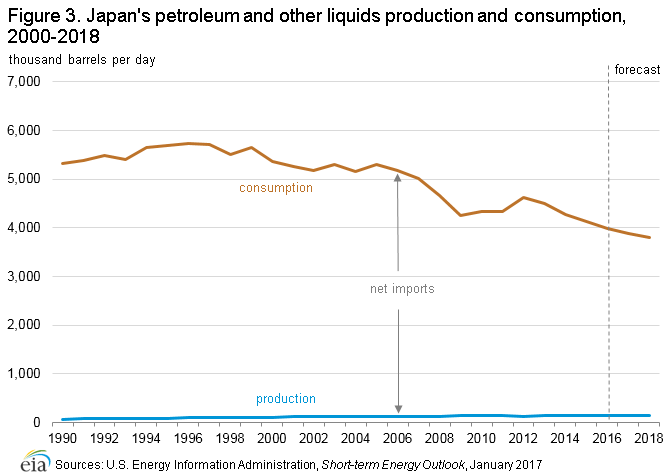

Japan consumed an estimated 4 million barrels of oil per day (b/d) in 2016, making it the fourth-largest petroleum consumer in the world, behind the United States, China, and India. However, oil demand in Japan has declined by 23% overall since 2006. This decline results from structural factors, such as fuel substitution, a declining and an aging population, and energy efficiency measures.

Japan consumes most of its oil in the transportation and industrial/chemical sectors (about 43% and 30% of petroleum products, respectively, in 2013), and it is also highly dependent on naphtha and liquefied petroleum gases (LPG) imports.10 Demand for naphtha has fallen as ethylene production is gradually being displaced by petrochemical production in other Asian countries. Japan has imported more LPG from the United States in the past few years to diversify its supply sources, and consumption will remain strong as the country blends LPG with lean LNG (liquefied natural gas with a lower heating value and higher methane content than rich natural gas) from the United States and Australia. In addition to the shift to natural gas in the industrial sector, fuel substitution is occurring in the residential sector as high prices have decreased demand for kerosene in home heating.11

Japan’s oil consumption rose by nearly 260,000 b/d between 2011 and 2012, the first significant annual jump in nearly two decades. Demand for low-sulfur fuel oil and the direct use of crude oil rose substantially in 2012 as these fuels replaced some nuclear electric power generation and supported post-disaster reconstruction. However, oil consumption in the power sector began declining in 2013 as Japan relied more on natural gas and coal as nuclear power substitutes, and as electricity demand declined overall. In addition, an overall consumption tax hike implemented in April 2014, the first in 17 years, and a weaker yen, which lowers purchasing power for imported products, have put downward pressure on oil consumption. Oil demand has fallen by more than 600,000 b/d between 2012 and 2016, and the U.S. Energy Information Administration (EIA) assumes that Japan’s oil consumption will continue declining through 2018 as nuclear capacity comes back online.

Sector organization

Although Japan is a minor oil-producing country, it has a robust oil sector comprised of various state-run, private, and foreign companies. Until 2004, Japan’s oil sector was dominated by the Japan National Oil Corporation (JNOC), which was formed by the Japanese government in 1967 and was charged with promoting oil exploration and production domestically and overseas. In 2004, JNOC’s profitable business units were spun off into new companies to introduce greater competition into Japan’s energy sector. Many of JNOC’s activities were taken over by the Japan Oil, Gas and Metals National Corporation (JOGMEC), a state-run enterprise responsible for aiding Japanese companies involved in oil and gas exploration and production overseas and in the promotion of domestic stockpiling. The largest of the new companies formed were Inpex and Japan Petroleum Exploration Company (Japex).

Private Japanese firms dominate the country’s large and competitive downstream sector, as foreign companies have historically faced regulatory restrictions. But over the past several years, these regulations have been eased, which has led to increased competition in the petroleum-refining sector. Chevron, BP, Shell, and BHP Billiton are among the foreign energy companies involved in providing products and services to the Japanese market as well as joint venture (JV) partnerships in many of Japan’s overseas projects.

Domestic exploration and supply

In 2016, Japan’s production of petroleum and other liquids was an estimated 138,000 b/d, of which only about 15,000 b/d was from light crude oil and condensates associated with natural gas fields. Most of Japan’s domestic oil production comes from of refinery gain, resulting from the country’s large petroleum refining sector. Although Japan continues exploring offshore for oil and gas sources, their resources are limited.

Overseas exploration and production

The Japanese government’s energy strategy encourages Japanese companies to increase energy exploration and development projects around the world to secure a stable supply of oil and natural gas.

Japanese oil companies have sought participation in exploration and production projects overseas with government backing because of the country’s lack of domestic oil resources. The government’s energy strategy plan encourages Japanese companies to increase energy exploration and development projects around the world to secure a stable supply of oil and natural gas. The Japan Bank for International Cooperation supports upstream companies by offering loans at favorable rates, thereby allowing Japanese companies to bid competitively for projects in key hydrocarbon-producing countries. Such financial support helps Japanese companies purchase stakes in oil and natural gas fields around the world, reinforcing national energy security while also guaranteeing their own financial stability.

As a result of the 2011 earthquake and because of a pressing need to secure energy supplies, Japan is promoting even more investment in overseas oil and natural gas operations. Japanese companies participated in more than 140 oil and gas projects worldwide that are in various stages of development, including about half that are in the production phase as of 2014. Japan also participates in technology exchanges with various countries.12

Japan’s overseas oil projects are primarily located in the Middle East, Southeast Asia, and Australia, although companies have recently invested in shale oil and oil sands projects in North America. Japanese oil companies involved in exploration and production projects overseas include: Inpex, Cosmo Oil, Idemitsu Kosan Company, Japan Energy Development Corporation, Japex, Mitsubishi, Mitsui, Nippon Oil, and others. Many of these companies are involved in small-scale projects that were originally set up by JNOC. However, several have invested in high-profile overseas upstream projects in recent years.

Oil imports

Japan, the third-largest global net oil importer, is highly dependent on the Middle East for most of its supply. The country is seeking to diversify its supply sources in Russia, Southeast Asia, and West Africa.

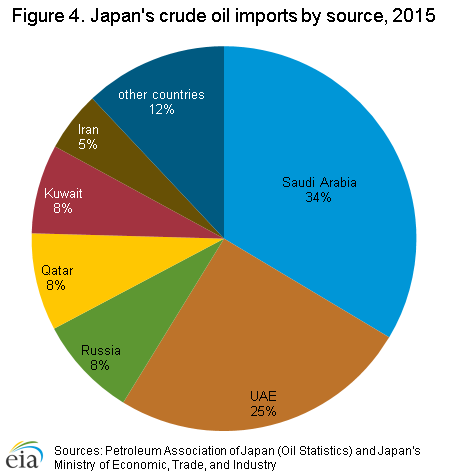

Japan was the third-largest net importer of total crude oil and petroleum products in the world after the United States and China in 2016. Net imports of total liquids (crude oil and petroleum product consumption less production) were 3.8 million b/d.13 Japan increased imports of crude oil for direct burn in power plants immediately following the Fukushima incident. However, crude oil imports have declined since 2012 as other fuels replaced oil use in the power industry and as the economy remained sluggish. Japan imported 3.4 million b/d of crude oil in 2015. The country is primarily dependent on the Middle East for its crude oil imports. Roughly 82% of Japanese crude oil imports originated from this region, and Saudi Arabia is the largest source of Japan’s crude oil imports, making up 34% of the import portfolio, or 1.1 million b/d of crude oil in 2015.14

Japan reduced its imports of crude oil and condensate from Iran in recent years as a result of the U.S. and European Union sanctions targeting Iran’s oil exports and the desire to maintain good relations with major Western countries. Japanese refiners replaced Iranian oil with other Middle Eastern supplies. Japanese imports from Iran were about 170,000 b/d in 2015, down from more than 313,000 bbl/d in 2011. Iran represented only 5% of Japanese crude oil imports in 2015, compared to 9% in 2011. The nuclear agreement signed by Iran and major countries in January 2016 removed sanctions on Iran’s oil exports, effectively allowing importing countries to resume their purchases of Iranian oil. These import levels are expected to increase, although issues remain including the insurance coverage of oil carriers from Iran still being held under sanctions and the price-competitiveness of Iranian oil in the current low-priced environment.15

Japan is leveraging its nuclear capabilities to secure nuclear cooperation and technology transfer deals with Middle Eastern countries in exchange for long-term crude oil supplies and upstream contracts. For instance, Japan signed a technology transfer deal with the UAE in 2013.16

Japan is eager to diversify its sources of oil imports and reduce its reliance on Middle Eastern supplies. Russia’s Eastern Siberia-Pacific Ocean (ESPO) 2,900-mile pipeline runs from Taishet, Siberia, to the Kozmino Bay Oil Terminal on the Pacific Ocean, where crude oil is loaded on tankers. ESPO began sending crude oil to Japan in 2009 via ships from the port. Since then, Japan significantly increased its crude oil imports from Russia, which now accounts for about 9% of Japan’s total imports. In mid-2011, Japan replaced some of the lost nuclear power generation with low-sulfur, heavy crudes from sources in West Africa (Gabon, Angola, and Nigeria) and Southeast Asia (Vietnam, Indonesia, and Malaysia). However, when crude oil burn for power in Japan began declining in 2013 as power utilities favored natural gas and coal as feedstock, some of these imports dwindled as well. After the United States lifted its long-term ban on crude oil exports in 2015, Japan began importing cargoes.17

Refining

According to the Petroleum Association of Japan (PAJ), Japan had 3.8 million b/d of crude oil refining capacity at 22 facilities as of October 2016. Japan has the fourth-largest refining capacity globally, behind the United States, China, and India.18 JX Holdings is the largest of eight oil refinery companies in Japan, and other key operators include Idemitsu Kosan, Cosmo Oil, TonenGeneral Sekiyu, and Showa Shell Group. In recent years, the refining sector in Japan has encountered excess capacity because domestic petroleum product consumption has declined. This decline is a result of the contraction of industrial output, the mandatory blending of ethanol into transportation fuels, more fuel-efficient vehicles, and shifting demographics leading to less driving each year. In addition to declining domestic demand for oil products, Japanese refiners now must compete with new, sophisticated refineries in emerging Asian markets.

The Japanese government seeks to promote operational efficiency in the refining sector, including increasing refinery competitiveness, which may lead to further refinery closures in the future. As a result, Japan has scaled back refining capacity from about 4.7 million b/d less than a decade ago.19 In 2010, METI announced an ordinance that would raise refiners’ mandatory cracking-to-crude distillation capacity ratio from 10% to 13% or higher by March 2014. To adhere to METI’s directive, some refiners reduced capacity by nearly 20% between April 2010 and April 2014 by closing plants entirely or by consolidating facilities. METI initiated a second phase of refinery restructuring, which involved improving the overall processing capacity to 50% from a current overall processing capacity of 45% and affected a broader range of processing units. The government calls for this phase to be implemented by March 2017, with a goal that an estimated 400,000 bbl/d of capacity will be curtailed through further reductions in refining operations and facility closures.20

There has been discussion that METI could issue a third phase to further consolidate the number of refiners and the total capacity, although no details about this phase are available.21 These capacity reductions come at a time when the country’s oil demand continues to decline as a result of an aging population, energy conservation measures, expectations of nuclear facilities returning to serve the power sector, and financial burdens of companies having to upgrade and maintain Japan’s old refining plants.

In 2015, two large mergers of refining corporations were proposed, one between JX Holdings and TonenGeneral and the other between Idemitsu Kosan and Showa Shell Group. JX Holdings and TonenGeneral plan to reduce their combined refinery capacity in the Chiba area, to share infrastructure, and to gain a majority share of the country’s gasoline retail market.22 Final approval and completion of this merger is expected by April 2017. The Idemitsu/Showa Shell merger has been held up by recent resistance from the Idemitsu founding family, who claims that the two companies have different corporate cultures.23 This potential merger block could delay further refining capacity reduction in Japan.

Natural gas

Japan relies on LNG imports for nearly all of its natural gas supply and ranks as the world’s largest LNG importer.

According to the OGJ, Japan had 738 billion cubic feet (Bcf) of proved natural gas reserves as of January 2017, which is small compared to other natural gas-producing countries. Because Japan is one of the top global natural gas consumers and has minimal amounts of production, the country relies on imports to meet nearly all of its natural gas demand.

Sector organization

Similar to Japan’s oil sector, Inpex and other companies created from the former Japan National Oil Company are the primary participants in Japan’s domestic natural gas sector. Inpex, Mitsubishi, Mitsui, and various other Japanese companies are actively involved in domestic as well as overseas natural gas exploration and production. Osaka Gas, Tokyo Gas, Toho Gas are Japan’s largest retail natural gas companies accounting for about 70% of city gas sales.24 In addition, more than 200 city gas utilities operate in Japan. Japanese retail gas and electric companies participate directly in overseas upstream liquefied natural gas (LNG) projects to assure reliability of supply.

Although Japan is a large natural gas consumer, it has a relatively limited domestic natural gas pipeline transmission system for a consumer of its size. This is partly a result of geographical constraints caused by the country’s mountainous terrain, but it is also the result of previous regulations that restrained investment in the sector. Japan imports LNG through a number of regasification terminal that are owned by both natural gas and electric utilities.

Reforms, that began in 1995, helped open the natural gas sector to greater competition for larger customers. Several new private companies entered the natural gas industry after the reforms were enacted. Currently, about 63% of the natural gas retail market is deregulated. The government is fully deregulating the retail sector for smaller users, and the residential sector will be open by April 2017. The final phase of natural gas market reform includes the unbundling of pipeline operations by 2022. Little to no third-party access is available at LNG terminals because of the lack of competitors and regulatory hurdles.25

Exploration and production

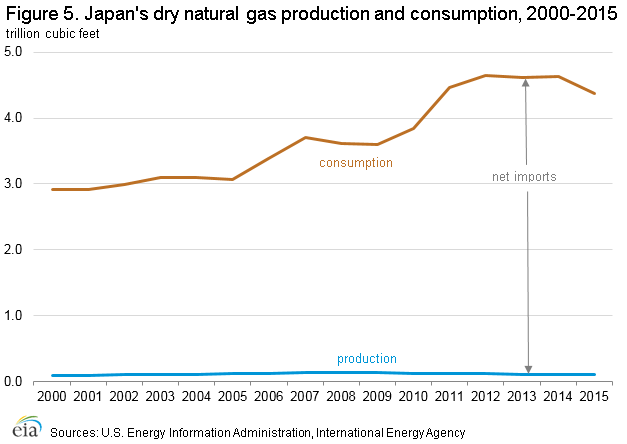

Japan’s natural gas production has been limited for more than a decade as a result of declining reserves. In 2015, production was about 100 Bcf, down from a high of about 140 Bcf in 2007, according to the International Energy Agency.26 Most of Japan’s natural gas fields are located along the western coastline. The Minami-Nagaoka natural gas field, operated by INPEX, on the western coast of Japan’s main island, is one of the country’s largest natural gas fields. The natural gas produced from this field is transported via an 870-mile pipeline network that crosses to the Tokyo metropolitan area.27 Japex, Japan’s other major upstream oil and natural gas company, has been involved in locating new domestic reserves in the Niigata, Akita, Yamagata, and Hokkaido regions of Japan, targeting areas near existing oil and natural gas fields.28

Japanese companies are using innovative methods to produce hydrocarbons and have discovered methane hydrates (natural gas deposits trapped within crystalized ice structures). In March 2013, JOGMEC conducted the first successful testing of offshore methane hydrates in the Nankai Trough on the southeast coast and is planning a second test in March 2017. Japan hopes to begin commercial production by 2023. A joint venture of eleven Japanese companies formed in late 2014 to advance the production and commercialization of methane hydrates.29 However, the high cost of these developments could delay production plans.

Consumption

In 2015, Japan’s natural gas consumption reached 4.4 trillion cubic feet of natural gas per year (Tcf/y), rising about 42% from a decade ago. Virtually all of Japan’s natural gas demand is met by LNG imports, with the exception of a very small portion of domestic production and stocks. After economic recovery following the 2008 global financial crisis and the March 2011 earthquake and nuclear outages, Japan’s natural gas demand rose dramatically between 2009 and 2012. Then economic and electricity demand weakened, coal prices dropped, renewable energy production rose, and natural gas demand plateaued for a few years before falling in 2015.

In 2015, the power sector was the largest consumer of natural gas, with about 63% of the mix, followed by the industrial sector (21%), residential (9%), commercial (4%), and other sectors (3%).30 The share of power generation grew as the sector significantly increased its imports of natural gas following the loss of nuclear power capacity more than five years ago. Tokyo Electric Power Company (Tepco) is Japan’s largest electric utility and natural gas importer. The company purchased an estimated 1.1 Tcf/y, or 27% of Japan’s LNG imports, in 2015.31 Tepco and Japan’s third-largest power company, Chubu Electric, formed a joint venture (Jera Company) to purchase LNG and to make upstream gas and downstream power plant investments starting in 2016. Tepco and Chubu Electric are seeking to leverage their combined market power to lower import prices, improve contract flexibility, share technology, and create more market efficiencies. Other firms such as Tokyo Gas, the country’s largest natural gas supplier, and Kansai Electric have formed a partnership to cooperate on LNG procurement and technological expertise. Japanese utilities are forming these partnerships to leverage optimize their competitive advantage as natural gas and electricity sector deregulation occurs and as new LNG contract terms become more flexible.32

Liquefied natural gas imports

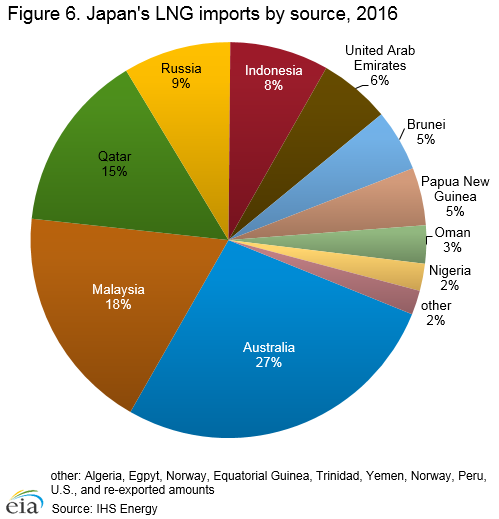

Japan accounted for about 32% of global LNG purchases in 2016 and reached record-high imports in 2014 as the Fukushima disaster spurred greater demand for LNG in the power sector. More than a third of the country’s LNG imports are from Southeast Asia, but Japan has a diverse portfolio of supply sources.

Because of its limited natural gas resources, Japan must rely on imports to meet nearly all of its natural gas needs. Japan began importing LNG from Alaska in 1969 and became a pioneer in the global LNG trade. Japan, the world’s largest LNG importer, accounted for 32% of the global market share of LNG demand in 2016. LNG imports jumped in 2012 after Fukushima and reached a record high of 4.3 Bcf/y in 2014 before retreating to 4 Bcf/y in 2016. Lower electricity demand and competition with other fuels have resulted in reduced natural gas imports since 2014.33

Because of environmental concerns, the Japanese government has encouraged natural gas consumption over the past several decades. The government chose LNG as its primary fuel of choice for power generation to substitute for the lost nuclear generation immediately following the Fukushima nuclear accident. Current government carbon abatement policies and the government’s pledge to lower greenhouse gas emissions in 2030 by 26% from 2013 levels support natural gas as the cleanest fossil fuel to replace lost nuclear capacity.34 However, the high cost of LNG in 2013 and 2014 led to increased coal use.

Japan operates more than 30 LNG import terminals, including expansions and satellite terminals, with a total natural gas send-out capacity of 9.7 Tcf/y as of 2016. Soma LNG, which has 75 Bcf/y of capacity, is the only terminal under construction, and it is slated to come online by 2018.35 The present regasification capacity exceeds the country’s demand, and the average terminal utilization rate is below 50%.36 Japan also has the largest LNG storage tank capacity in the world, holding 590 MMcf, which serves as a buffer during seasons of higher LNG demand. Most of the LNG terminals, which are located in the main population centers and near major urban and manufacturing hubs of Tokyo, Osaka, and Nagoya, are owned by local power companies, either alone or in partnership with natural gas companies. Japan lacks extensive gas pipeline infrastructure and relies on LNG imports in many coastal demand centers and uses LPG in other areas.

Asian LNG prices traditionally have been linked to international crude oil prices, which rose sharply between 2008 and 2014. Japan’s higher natural gas demand for power, a tighter LNG global supply market, and higher oil prices led to a significant increase in Japan’s LNG import prices, climbing from an average of $10/MMBtu before the Fukushima crisis to more than $17/MMBtu in 2012. International oil prices have decreased by more than half since the first half of 2014, and oil-linked Asian LNG prices followed the trend. Japan’s average LNG import price plummeted to below $7/MMBtu by 2016.37

After the Fukushima incident, Japan replaced lost nuclear capacity with natural gas-fired power from short-term and spot purchases of LNG. Subsequently, Japanese companies signed several medium- and long-term LNG purchase agreements with both existing and new suppliers to hedge against higher rates. Japanese importers began negotiating lower prices and greater flexibility in LNG contracts. Oil prices remained at sustained high levels through mid-2014, causing Japanese utilities, particularly those affected by the Fukushima accident, to incur serious costs from higher natural gas and oil purchases, resulting in net revenue losses. In response to the higher fuel acquisition costs and attendant power price increases, Japanese companies signed some LNG contracts based on U.S. natural gas market prices, which are lower, rather than being tightly linked to crude oil prices. The recent decline in international oil prices at the end of 2014 has provided some relief for Japanese LNG customers. Japanese utilities are also seeking to renegotiate some of their existing long-term contracts that restrict the resale of any LNG volumes to provide more flexibility in the face of an oversupplied market and lower electricity demand. Several recently-signed long-term contracts, primarily for LNG supply from new terminals in the United States and Australia, have flexible destination clauses. Osaka Gas also recently announced that it does not plan to sign any further long-term LNG contracts and intends to resell a portion of their contracted volumes since they are oversupplied through 2020.38

LNG supplies from Malaysia and Indonesia are becoming more constrained, and Japan is seeking to diversify its contracts and investments in other LNG ventures. About 36% of Japan’s LNG imports originated from regional suppliers in Southeast Asia, and 27% originated from Australia in 2016, although the country has a fairly balanced portfolio with supplies coming from other regions.39 Qatar, the world’s largest supplier of LNG, made up 15% of Japan’s LNG trade. Russia became a new source of natural gas for Japan when it commissioned the Sakhalin-2 liquefaction terminal, located just north of Japan, in 2009. TEPCO and Osaka Gas hold long-term agreements with Papua New Guinea LNG, which began exporting natural gas in 2014. Japanese electric and natural gas companies and trading houses have signed long-term supply contracts with various large LNG projects in Australia, most notably the Chevron-led Gorgon project, Wheatstone LNG, and Ichthys LNG, all of which are scheduled to come online by 2018. Australia is expected to remain a key source of LNG supply to Japan over the next decade.

Overseas exploration and production

Japanese companies, especially JX Nippon Group, Inpex, and Mitsubishi, have actively sought participation in overseas natural gas exploration and production projects that are typically linked to export facilities. The Japanese trading company, Mitsubishi, a key natural gas supplier to Japanese utilities, has owned capacity in liquefaction terminals, mostly in Southeast Asia, Australia, and Oman, for four decades. JX Nippon and Inpex are developing several production and export projects throughout Southeast Asia, Australia, and the UAE, and more recently, in North America. In the past few years, Japanese utilities have also acquired small stakes in the upstream supply and operations of LNG projects to secure LNG contracts from emerging and growing LNG markets such as Australia, the United States, Canada, and Russia.

The advent of North American shale gas production and anticipated natural gas exports have attracted investment by Japanese companies in North American natural gas developments linked to planned LNG projects. JOGMEC announced in 2013 that it will guarantee 75% of the bank loans to Japanese companies involved in developing LNG projects that help reduce Japan’s import fuel cost.40 In May 2013, Mitsubishi and Mitsui, Japan’s two largest trading companies, first ventured into the U.S. shale gas export market by purchasing a combined 33% equity share in the Cameron LNG project located in the Gulf of Mexico. The companies have agreements to purchase two-thirds of the terminal’s export capacity that is expected to come online by 2017. Mitsubishi and Inpex are also participating in upstream ventures in oil and shale gas developments in western Canada. Mitsui and Sumitomo, another large Japanese trading company, are involved in large upstream shale gas ventures in the United States.

Electricity

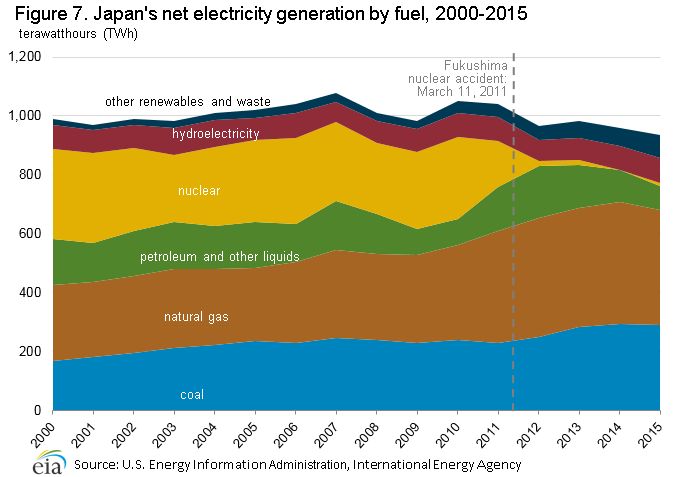

Japan was the world’s third-largest producer of nuclear power, after the United States and France, prior to the Fukushima Daiichi nuclear power plant accident in March 2011. After the Fukushima disaster, the composition of fuel used for power generation shifted heavily to fossil fuels, particularly LNG, which became the primary substitute for nuclear power.

Although Japan has the third-highest demand for electricity in Asia, it has one of the lowest electricity demand growth rates in the region. Net electricity generation, which hovered around 1,000 Terawatthours (TWh) for more than a decade, was estimated at 935 TWh in 2015. Because Japan depends heavily on fuel imports to meet its generation needs, the country seeks to ensure an optimal combination of sources based on cost efficiency, energy security, and environmental stability. Before most nuclear power generation was removed from service after 2011, Japan had one of the most balanced portfolios of fuels used for power generation of the world’s major power consumers.41

Prior to the Fukushima disaster and the displacement of much of the nuclear-generated power, Japan did not rely on any particular fuel source for more than one-third of its total generation. However, nuclear generation played a pivotal role in Japan’s electricity generation mix and represented 27% of net generation in the two years prior to Fukushima. In 2010, natural gas and coal were the primary fossil fuels used in Japan’s electricity portfolio and constituted about 30% and 23%, respectively. Oil, which was expensive and one of the least-clean fuels to burn, accounted for just 8% of power generation in 2010. Renewable energy made up almost 12%, mostly from hydroelectricity.

Once Japan began to remove its nuclear generation capacity from operation starting in 2011, other fuels such as LNG, oil, and coal displaced it. Financial incentives for clean energy projects prompted renewable energy growth. This shift has markedly altered the power generation portfolio. Despite the uncertainty about the role nuclear fuel will play in Japan’s future energy landscape, the government intends to include it in the fuel mix to balance economic costs, environmental concerns, and safety measures.42 Current targets for fuel use in the electricity mix in 2030 have LNG at 27%, coal at 26%, renewable energy at 22-24%, nuclear at 20-22%, and oil at 3%.43

Japan’s total installed electricity generating capacity in 2014 was 313 gigawatts (GW). Fossil fuel-fired power plants accounted for most of this capacity, with 193 GW (62% of the total capacity). Nuclear capacity was 42 GW in 2014, constituting 13% of the capacity, although operational capacity is expected to drop another 2 GW by 2017 as several more reactors are scheduled for decommissioning. Hydroelectric facilities held 16% of the capacity and have been a steady source of power supply for Japan for several years. The remaining capacity came from wind, solar, geothermal, and small biomass-fired facilities.44

Sector organization

Japan’s electricity industry is controlled by 10 privately-owned, integrated power companies that act as regional monopolies, accounting for nearly 80% of the country’s total installed electricity generating capacity. The remaining electricity is generated by industrial facilities or independent power producers. The largest power company in Japan is TEPCO, which accounted for 20% of total power generation in the country in 2014.45 The large companies also control the country’s regional transmission and distribution infrastructure. Japan’s electricity policies are managed by the Agency for Natural Resources and Environment, part of METI. Japan has two power grids with virtually no interconnections and two different power line frequencies.

Other significant operators in the electricity market include the Japan Atomic Power Company, the first Japanese company to build a nuclear reactor (in 1960), and the Electric Power Development Company (J-Power), formerly a state-owned enterprise that was privatized in 2004. The Japan Atomic Power Company operates four nuclear power plants, with a combined capacity of 2.6 GW, and sells electricity to the local power companies. J-Power operates 16 GW of hydroelectric and fossil fuel-fired power plants. J-Power has also been involved in consulting services for electricity production and environmental protection in 63 countries, mainly in the developing world, since 1960.

Japan established the Nuclear Regulatory Authority (NRA) in September 2012 to replace two other nuclear agencies—the Nuclear Safety Commission and METI’s Nuclear and Industrial Safety Agency. The NRA was established to provide a more independent assessment of nuclear safety. The NRA adopted more stringent nuclear safety guidelines and procedures in July 2013 after the Fukushima earthquake and ensuing damage. The NRA is also in charge of enforcing these nuclear safety guidelines, and all nuclear facilities must submit applications to restart operations to the NRA.

These safety guidelines are designed to ensure facilities can withstand all natural disasters and require reactors to be located far from active earthquake fault lines. The guidelines require installation of larger seawalls, air vents, and safety control rooms. Also, the new standards include the decommissioning of any reactors older than 40 years, with a possible 20-year extension. Ultimately, this standard will result in a long-term decline in Japan’s nuclear capacity unless new reactors are constructed.

Electricity price reform

Deregulation of Japan’s electricity sector began in 1995 by giving industrial and commercial customers a choice of electric suppliers, although the country has been slow to fully separate its generation, transmission, and distribution sectors from the regional companies. Following the Fukushima incident, Japan encountered power supply shortages because the regional monopolies could not transmit electricity outside of their regions, and power costs rose following the loss of nuclear generation.

Recent electricity reforms aim to achieve greater competition and lower electricity prices for consumers based on more efficient power sector operations and investments. The government’s goals of the current electricity reforms are for end-users to be able to choose their power generation suppliers and to unbundle the regional monopolies that are vertically integrated. The first phase, implemented in 2015, involved establishing the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) to manage electricity flows across Japan’s regions and to enhance supply security by strengthening overall transmission capacity on the national grid during both normal and emergency circumstances. Japan’s two electricity frequencies (50 hertz and 60 hertz) are not compatible and that allow only 1.2 GW of electricity to be connected or transferred between the frequencies. This incompatibility of electricity frequencies complicates moving to a fully interconnected system. The second phase, which began in April 2016, included a full deregulation of electricity to the retail sector and opened the residential sector to competition. The third phase involves divesting of transmission and distribution divisions from generating companies and replacing a fuel cost-recovery scheme with a market-based pricing system by April 2020.46

Because of higher electricity generation costs from higher fossil fuel purchases, Japan’s electric utilities have sought to increase the electricity tariffs paid by end users to help cover the companies’ generation costs. Subsequently, METI approved tariff increases for several utilities following the Fukushima accident. Retail electricity prices rose about 20% and 30% for residential and industrial customers, respectively, since Fukushima.47

Electricity generation

All of Japan’s nuclear power generation capacity was removed from service between September 2013 and August 2015 as a result of new, stringent safety inspections and several levels of regulatory approval required to restart facilities. Oil and natural gas replaced all of the lost nuclear generation immediately after the Fukushima incident, and coal generation began to supplant oil-fired power after 2013. As nuclear capacity gradually resumes operation following government approval of facilities, Japan anticipates reducing the current share of fossil fuel generation.

Fossil fuels Fossil fuels accounted for an estimated 764 TWh of Japan’s net electricity generation in 2015, representing about 82% of the total generation, up from 62% in 2010. The share of fossil fuel-powered generation rose substantially for the first time in several decades in the wake of the Fukushima disaster when electric utilities turned to hydrocarbons as substitutes for the lost nuclear power generation.

According to Japan Electric Power Information Center, there are currently more than 60 major thermal power plants owned by the top 10 electric utilities and J-Power. Several combined-cycle LNG-fired or coal-fired plants are under construction or are in the planning stages.48 The country’s aging oil-fired power plants are used primarily to meet peak demand. Some facilities have dual-fuel (coal/oil or natural gas/oil) capabilities to provide more flexibility in fuel sources that have been useful during the loss of nuclear generation capacity.

Coal, typically used as a baseload source for power generation, remains an important fuel source for generating electricity in Japan. Domestic coal production dwindled to virtually nothing by 2002, and Japan began importing all of its coal, primarily from Australia. Coal imports grew to 210 million short tons of coal in 2015 from 193 million short tons in 2011, after more coal-fired generation capacity came online.49 Japan, which was the world’s top coal importer for decades, dropped to the third-largest importer in 2015, just below China and India because of the rapid coal consumption growth in these countries.50

Some coal-fired power plants located near the earthquake epicenter off the coast of Fukushima experienced significant damage following the 2011 earthquake. As a result, coal use declined slightly in 2011 when the country relied heavily on natural gas and oil for power generation to replace lost nuclear capacity. Once new coal-fired capacity was commissioned in 2013 and international coal prices plummeted, electric utilities increased coal purchases for power generation. Coal’s share in the power sector was an estimated 23% before Fukushima and rose to 31% by 2015. The government plans for coal to account for 26% of the market share by 2030, maintaining the fuel’s importance as a baseload for power generation.51

Japan has the highest efficiency rate of coal-fired technology in the world. The country is installing new, clean coal plant technologies, such as ultra-supercritical units or integrated gasification combined-cycle technology, to meet environmental targets and to replace some of the decades-old coal power plants. Although no significant coal-fired capacity is expected to come online before 2020, Japanese companies plan to develop about 45 additional coal power plants, adding more than 20 GW of capacity in the next decade. Coal is expected to displace some of the expensive oil-fired power generation. The pace of development depends on how many nuclear units can return to service and whether the government will grant environmental approvals to each coal-fired power plant in light of Japan’s commitment to reduce its greenhouse gas emission levels by 2030.52

Natural gas has increased its role in the power sector, particularly after nuclear power was removed from service starting in 2011. Natural gas, which accounted for 30% of Japan’s electricity generation in 2010, increased its share to 42% in 2015.53 Post-Fukushima, natural gas has been the first choice of nuclear fuel substitution for utilities because of the cleaner-burning nature of natural gas compared to other fossil fuels. Japan is replacing many of its older, less efficient natural gas-fired power plants with more efficient combined-cycle units. Currently, there are three natural gas-fired power plants with a combined 4.8 GW of capacity under construction and scheduled to come online by 2020.54 The expected return to operation of some nuclear reactors in 2016 and beyond and the growing role of renewable energy in the country’s energy portfolio are likely to depress LNG imports and natural gas use in the power sector. By 2030, LNG is expected to provide 27% of the country’s power generation.

Before the 2011 earthquake, Japanese utilities began removing oil-fired generation capacity because of the higher operational costs, aging units, and environmental downsides. Some utilities brought back mothballed oil generation facilities to compensate for lost nuclear power. Total oil demand for power, primarily from residual fuel oil and direct crude oil burn, climbed sharply from an estimated 175,000 b/d in 2010 to 590,000 b/d in 2012 when oil produced 18% of power generation. Overall power consumption declined, and the other less-expensive fuels began to fill the gap. Oil use in the power sector retreated to 270,000 b/d and a 9% share of electricity production by 2015.55 Any nuclear power generation that returns to service will continue to replace oil supply for electricity in Japan, and some oil-fired facilities are once again being mothballed.

Nuclear

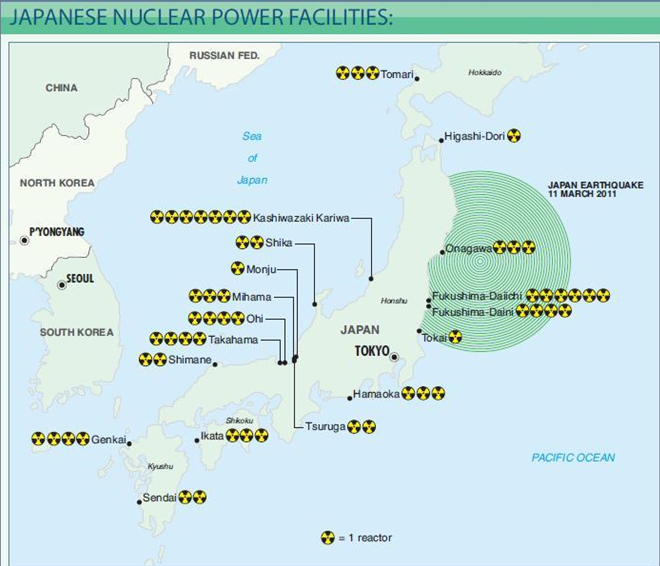

Before the Fukushima accident, Japan was the third-largest nuclear power generator in the world behind the United States and France. However, the country lost all of its operating nuclear generation capacity by 2013 as its facilities were removed from service because of earthquake damage or for regular maintenance.

By the end of 2017, Japan will have 42 operable nuclear reactors with a total installed net generating capacity of about 40 GW, down from 54 reactors with 47 GW of capacity in 2010.56 More than 10 GW of nuclear capacity at the Fukushima, Onagawa, and Tokai facilities ceased operations immediately following the earthquake and tsunami. Other reactors were permanently damaged from emergency seawater-pumping efforts and are not scheduled to return to service. The government officially decommissioned all six reactors at the Fukushima Daiichi nuclear plant, which had a combined capacity of 4.6 GW. By 2017, another 2.6 GW of capacity is slated for decommissioning from small reactors that are at least 40 years old. The cost to upgrade these facilities to comply with the new regulations and extend their lifespan outweigh the cost of closing them.57

General maintenance standards in Japan require nuclear facilities to come offline every 13 months for inspections. Following the Fukushima disaster, the Japanese government required facilities to pass stress tests and receive local government approval. As reactors were removed from operation, they remained offline. By May 2012, Japan did not have any nuclear generation for the first time in more than four decades. The government returned two reactors, Kansai Electric’s Ohi Units 3 and 4, to service in July 2012, leaving Japan with only 2.4 GW of capacity for about a year. These two reactors were again removed from service in September 2013 for scheduled maintenance, leaving Japan without operational nuclear capacity for another two years.

Japan’s current government under Prime Minister Abe and industrial interests in Japan favor re-commissioning nuclear power plants to lower energy costs. However, interested parties are considering safety concerns and resistance from anti-nuclear government factions and the public. Japan’s most recent 2014 Strategic Energy Plan stated that nuclear power is an important source of baseload power, but that dependence on nuclear generation will be offset as much as possible by improved efficiency and by the acceleration of renewable energy supplies.58

As of December 2016, restart applications for 25 reactors and an application for the new Ohma plant, representing more than half of Japan’s remaining operable capacity, had been filed with the NRA.59 Seven of the facilities, with a combined capacity of 5.8 GW, have received approvals from the NRA, and three are currently operating. Kyushu Electric’s Sendai 1 and 2 units in southwestern Japan restarted service in late 2015,60 and Shikoku Electric’s Ikata 3 reactor began operating in August 2016.61 Kansai Electric’s Takahama Units 3 and 4 started operations in early 2016, although local public opposition resulted in a district court immediately issuing an injunction to stop the operations at both facilities. Kansai Electric has filed an objection, and the restart of these reactors is delayed until there is legal resolution. The NRA extended the life of the much older Takahama Units 1 and 2 reactors, pending necessary upgrades, and these facilities are expected to return to service in 2019.

Two nuclear reactors (Ohma Unit 1 and Shimane Unit 3), with a combined capacity of 2.7 GW, are under construction and nearly complete, but work was suspended on these plants following Fukushima. Both units must be approved under the new standards before they can begin operations. The reactors that were in the planning phase before Fukushima are currently cancelled or delayed indefinitely as the country focused on bringing back some of the operational reactors. The timeline for restarting many of these reactors is uncertain because of the more stringent regulations and the need to overcome political opposition and restore public confidence in several provinces.

Japan has a full nuclear fuel cycle, including enrichment and reprocessing of used plutonium and uranium fuel. This process provides Japan with greater energy security and resource conservation, and it reduces Japan’s reliance on imported fuels. Historically, Japan has promoted nuclear electricity as a means of diversifying its energy sources and reducing carbon emissions, emphasizing safety and reliability. According to the FEPC, nuclear power has made a great contribution to Japan’s energy security by reducing its energy imports by reducing its carbon dioxide emissions. Overall, carbon emissions have risen substantially since Japan’s operating nuclear capacity was reduced. Japan’s commitment to lower greenhouse gas emissions by 2030 is also driving the country to optimize its fuel slate and to promote nuclear use for power generation.62

Hydroelectricity and other renewables

Japan’s installed hydroelectric generating capacity was 50 GW in 2014, accounting for about 16% of total electricity capacity.63 About half of the installed capacity consists of large power plants. Like nuclear power, hydropower is a source for baseload generation in Japan because of the low generation costs and a relatively stable supply. Net hydroelectric generation was 84 TWh in 2015, making up about 8% of Japan’s total net generation mix. The Japanese government has invested in small hydropower projects to serve local communities, and the capacity of pumped storage facilities is growing. However, the potential for hydroelectricity growth in Japan is limited.64

As part of the revised energy policy plan, Japan is trying to encourage increased use of renewable energy for power generation from sources such as solar, wind, geothermal, and biomass. Renewable energy, apart from hydroelectricity, made up slightly more than 3% of Japan’s total energy consumption and about 8%, or 79 TWh, of the country’s total electricity generation in 2015.65 Japan wants to boost generation from both hydroelectricity and other renewables to 22—24% by 2030. The Japanese legislature approved generous feed-in tariffs (FIT) for renewable sources in July 2012, obligating electric utilities to purchase electricity generated by renewable fuel sources, including small hydroelectricity projects, at fixed prices for up to 20 years. The costs are shared by government subsidies and by end users.

Most renewable capacity growth since 2012 has occurred in solar energy as a result of heavy investment in large-scale PV units. Japan’s solar generation capacity reached 34 GW at the end of 2015, which is more than five times higher than capacity in 2012.66 Although solar capacity climbed sharply in the past two years, many projects have encountered problems connecting to the grid and challenges selling the electricity to the regional utility firms, slowing the process for actual generation increases.67 Japan’s government revised the FIT subsidy levels down and modified the FIT policy for project tendering in 2016 to reduce the backlog of large-scale solar projects. Japan has one of the largest biomass markets for power generation in the world, and the government is providing financial incentives to promote more biomass projects.68 The potential for geothermal power in Japan is significant, but strict regulations have kept geothermal power from growing in the country. After Fukushima, Japan lifted restrictions on geothermal development in national parks.69

Source: Financial Times via Petroleum Economist.

Notes:

- Data presented in the text are the most recent available as of February 2, 2017.

- Data are EIA estimates unless otherwise noted.

Endnotes:

1EIA International Energy Statistics and BP Statistical Review of World Energy, 2016 for 2015 data.

2International Energy Agency, Medium-Term Gas Market Report 2014, Box 1: “Three years after the Fukushima accident, how is Japan coping in the absence of nuclear”, page 23; World Nuclear News, “Japan’s post-Fukushima nuclear shutdown ends,” August 11, 2015.

3Japan’s Ministry of Economy, Trade, and Industry, Energy Situation in Japan, October 2015, page 2 (used average annual exchange rate based on U.S. Internal Revenue Service); Japan’s Ministry of Finance, Trade Statistics of Japan, Value of Exports and Imports, Calendar Year 2015 (accessed January 2017); Newsbase AsianOil: “In the Shadow of Fukushima”, July 30, 2014 and “LNG Imports Push Japan’s Trade Deficit to Record High”, July 30, 2014.

4Japan’s Ministry of Economy, Trade, and Industry: FY2013 Annual Report on Energy (Energy White Paper 2014) Outline, June 2014 and Fourth Strategic Energy Plan, April 2014.

5BP Statistical Review of World Energy 2016.

6Oil & Gas Journal, Worldwide Look at Reserves and Production, December 7, 2015.

7Reuters, “Exclusive: China in $5 billion drive to develop disputed East China Sea gas“, July 17, 2013; Rigzone, “Roller Coaster Year in Territorial Disputes in East, South China Seas“, December 26, 2014; Bloomberg, “China-Japan Tensions Rise Around Disputed East China Sea Isles,” August 8, 2016.

8International Energy Agency, Monthly Oil Database (accessed January 2017).

9International Energy Agency, Oil Market Report, April 11, 2014 “OECD Asian Economies Building Storage to Take Advantage of Globalized Trade”, page 33 and Bloomberg, “Japan Expands, Extends Oil Storage Lease Contract With Abu Dhabi”, November 9, 2014.

10Petroleum Association of Japan, Petroleum Industry in Japan 2015, page 9; FGE, Asia-Pacific Databook 1, Spring 2016, page 57.

11FGE, Asia-Pacific Databook 1, Spring 2016, page 54-57, S&P Global Platts, “Interview: Japan’s Gyxis to triple overseas LPG trade, double VLGC fleet in 3 years,” May 15, 2015.

12Reuters, “Japan’s JOGMEC says could accelerate investment in oil, gas”, June 19, 2014; Petroleum Association of Japan, Petroleum Industry in Japan 2015, page 25.

13EIA, data based on Short-term Energy Outlook, January 2017.

14Petroleum Institute of Japan, Oil Statistics, Crude Oil Import by Countries and by Source (accessed January 2017) (via Japan’s Ministry of Economy, Trade, and Industry data).

15Nikkei Asian Review, “Japan oil companies not thirsty for Iran crude,” July 8, 2016; S&P Global Platts, “Japan’s Iran oil imports seen rising in 2016 with record shipping insurance,” March 30, 2016.

16Japan’s Ministry of Foreign Affairs, “Exchange of Diplomatic Notes for the Entry into Force of the Japan-United Arab Emirates (UAE) Nuclear Cooperation Agreement“, June 11, 2014.

17Reuters, “Japan to import U.S. crude in May, second cargo since export ban lifted: sources,” March 16, 2016.

18Petroleum Association of Japan, Oil Statistics, Location of Crude Distillation Capacity in Japan (as of October 2016) and FGE, Energy Insights, Issue #237, “What’s Next for Japan’s Oil Refining Industry?,” April 26, 2016; BP Statistical Review of World Energy 2016.

19BP Statistical Review of World Energy 2016.

20International Energy Agency: Oil Market Report, July 11, 2014. “METI Outlines New Plans for Japanese Refinery Industry Rationalisation”, page 55; S&P Platts, “Japan refiners urged to promptly cut nameplate capacity in line with regulation,” November 5, 2014; FACTS Asia Pacific Databook 2, Fall 2016, pages 40-44.

21Reuters: “Japan refiners headed towards consolidation after 2017 – analysts”, November 20, 2014.

22Newsbase AsianOil. “Japanese Refining Sector Faces Further Consolidation”, November 26, 2014; FACTS Global Energy, Energy Insights, Issue #233, “JX/TonenGeneral Merger: The Final Step Towards Japan’s Refining Industry Consolidation” January 14, 2016.

23Reuters, “Japan’s Idemitsu family issues fresh call for management to end Showa Shell merger,” August 9, 2016; Reuters, “Idemitsu family, in fight with management, buys Showa Shell shares to block acquisition,”August 3, 2016; FGE, Energy Insights, Issue #237, “What’s Next for Japan’s Oil Refining Industry?,” April 26, 2016; FGE, “Idemitsu-Showa Shell Stalemate to Delay Japan’s Refining Industry Consolidation,” July 12, 2016.

24International Energy Agency, Medium-Term Gas Market Report 2016, page 24. FACTS Global Energy, Energy Insights, Issue #234, “Japan’s Power/Gas Sector Deregulations: Part 1- Overview,” page 3.

25International Energy Agency, Medium-Term Gas Market Report 2016, pages 24-25.

26International Energy Agency, Natural Gas Information 2016.

27INPEX Corporation, Our Business webpage (accessed January 2017).

28JAPEX Annual Report 2015, page 15.

29Japan Oil, Gas, and Metals National Corporation, “Gas Production from Methane Hydrate Layers Confirmed“, March 12, 2013; Financial Times, “Methane Hydrates Could be Energy of the Future“, January 17, 2014; Rigzone, “Japan Progresses Methane Hydrate Project, Ignores Industry Downturn,” July 11, 2016.

30IHS Energy, Japan LNG Market Profile, November 1, 2016, page 17.

31IHS Energy, Japan LNG Market Profile, November 1, 2016, page 16 and IHS Energy, Japan LNG Data Sheet, January 4, 2017.

32Reuters, “Japan’s Tepco, Chubu Electric name fuel venture Jera“, April 15, 2015; FACTS Global Energy, Energy Insights, Issue #238, “Japan’s Power/Gas Sector Deregulation: Part 3-Alliances”, April 28, 2016; Nikkei Asian Review, “Kansai Electric, Tokyo Gas form united front to tackle market deregulation“, April 12, 2016.

33IHS Energy, Historical LNG Trade Data, December 5, 2016 and IHS Energy Market Trade Data Sheet: Japan, January 4, 2017.

34The Federation of Electric Power Companies of Japan, Electricity Review Japan 2016, page 10.

35IHS Energy, Historical LNG Trade Data, December 5, 2016 and IHS Energy Market Trade Data Sheet: Japan, January 4, 2017.

36IHS Energy, Japan LNG Market Profile, November 1, 2016, pages 10-13; IHS Energy Market Trade Data Sheet: Japan, January 4, 2017; International Gas Union, IGU World LNG Report – 2016 edition, page 47.

37IHS Energy, LNG Market Data Sheet: Japan, January 4, 2017; Japan’s Ministry of Economy, Trade, and Industry, Statistics: Spot LNG Prices webpage (accessed January 2017) and Newsbase NRG, “Japan India Will See Lower LNG Prices, Just Not Through Consortium”, September 2014.

38FACTS Global Energy, Gas/LNG Flash Alert, “An Overcommitted Osaka Gas and its Plans to Resell LNG”, September 23, 2016.

39IHS Energy Market Trade Data Sheet: Japan, July 5, 2016.

40S&P Global Platts, “Jogmec to guarantee 75% of loans to LNG projects that lower Japan’s import costs“, June 21, 2013.

41The Federation of Electric Power Companies of Japan Electricity Review Japan 2014, page 20.

42Japan’s Ministry of Economy, Trade, and Industry, FY2013 Annual Report on Energy (Energy White Paper 2014) Outline, June 2014.

43FACTS Global Energy, Energy Insights, Issue #219, Japan’s Official Power Generation Mix Target for 2030″, May 21, 2015.

44U.S. Energy Information Administration; World Nuclear Association, Nuclear Power in Japan (updated December 28, 2016); International Atomic Energy Agency, Power Reactor Information System Country Statistics for Japan (accessed January 2017).

45Japan Electric Power Information Center, Inc. Operating and Financial Data (accessed January 2017).

46FACTs Global Energy, Energy Insights, Issue #234 and #236, “Japan’s Power/Gas Sector Deregulation: Part 1-Overview,” January 15, 2016 and “Japan’s Power/Gas Sector Deregulation: Part 2- Nationalization of the Nuclear Sector is Under Consideration,” April 18, 2016; METI, “Electricity Market Reform in Japan,” October 2014; METI, “Japan’s Electricity Market Deregulation,” June 2015.

47World Nuclear News, “Japan Continues to Count Cost of Idled Reactors“, June 17, 2014; The Federation of Electric Power Companies of Japan, Electricity Review Japan 2016, page 3; Forbes, “Five Years After Fukushima, Japan Launches Massive Electric Sector Deregulation,” April 4, 2016.

48Japan Electric Power Information Center, Inc. Operating and Financial Data (accessed January 2017).

49United Nations Comtrade Database, International Trade Centre (accessed January 2017).

50U.S. Energy Information Administration; United Nations Comtrade Database, International Trade Centre (accessed January 2017); World Coal Association, Coal Statistics webpage (accessed January 2017).

51FACTS Global Energy, Energy Insights, Issue #219, Japan’s Official Power Generation Mix Target for 2030″, May 21, 2015.

52FACTS Global Energy, Energy Insights, Issue #219, Japan’s Official Power Generation Mix Target for 2030″, May 21, 2015; Reuters, “FACTBOX-Japan’s construction plans for new coal-fired power stations,” April 22, 2016; Reuters, “Japan doubles down on coal power as trading houses curb investment“, June 16, 2016.

53EIA estimates derived from International Energy Agency electricity data (2016).

54Japan Electric Power Information Center, Inc. Operating and Financial Data (accessed January 2017).

55International Energy Agency, Statistics: Japan, Oil for 2010; International Energy Agency, Oil Market Report, August, 11, 2016, page 9; Federation of Electric Power Companies of Japan, Electricity Generated and Purchased (Bulletin), FY 2010.

56U.S. Energy Information Administration; International Atomic Energy Agency, Power Reactor Information System, Country Statistics, Japan (accessed January 2017); World Nuclear Association, Nuclear Power in Japan (updated December 28, 2016); FACTS Global Energy, East of Suez Gas Service, LNG Market Report, Issue #80, May 25, 2016, pages 1-4; Federation of Electric Power Companies of Japan, Electricity Review Japan 2016, page 17.

57World Nuclear Association, Country Profiles, Nuclear Power in Japan (updated December 28, 2016).

58Japan’s Ministry of Economy, Trade, and Industry, Fourth Strategic Energy Plan, April 2014.

59World Nuclear Association, Country Profiles, Nuclear Power in Japan (updated December 28, 2016).

60Reuters, “Japan restarts second reactor at Sendai nuclear plant,” October 14, 2015.

61World Nuclear News, “Fifth Japanese power reactor restarted,” August 12, 2016; Nuclear Energy Institute, Japan Nuclear Update (accessed January 2017).

62The Federation of Electric Power Companies of Japan, Electricity Review Japan 2016, pages 8 and 10; World Nuclear Association, “Climate Targets Blown in Japan“, August 1, 2013.

63U.S. Energy Information Administration.

64The Federation of Electric Power Companies of Japan, Electricity Review Japan 2016, page 6.

65BP Statistical Review of World Energy, 2016; EIA estimates derived from International Energy Agency electricity data (2016).

66Bloomberg, “Japan’s Solar Boom Showing Signs of Deflating as Subsidies Wane“, July 5, 2016; PV Magazine, “Japan clears up uncertainty over its renewable energy FIT“, May 31, 2016; Japan Renewable Energy Foundation: A Statement of the Basic Energy Plan of Japan, April 21, 2014.

67Bloomberg, “Solar’s $30 Billion Splurge Proves Too Much for Japan“, October 9, 2014, and The Economist, “Solar Shambles: Japan has failed to learn from Germany’s renewable energy mess“, November 29, 2014.

68Japan External Trade Organization (JETRO), “Japan’s Biomass Market Overview“, November 2015.

69JOGMEC, “Current Situation of Geothermal Power Generation in Japan“; Geothermal Energy Association, 2013 Geothermal Power: International Market Overview, November 2013. Geothermal Potential and Resource Assessments in Japan, IGA Workshop in Essen, November 14, 2013, National Institute of Advanced Industrial Science and Technology, Japan.