The Groundhog And US Heating Oil Bills – Analysis

Last Thursday (February 2) was Groundhog Day. Punxsutawney Phil, the Nation’s most famous groundhog, saw his shadow that day when peeking out of his burrow. According to legend (and the promoters of the yearly Groundhog Day event in Punxsutawney, Pennsylvania) this means that there will be six more weeks of winter weather.

However, as a very wise person once noted, “Prediction is very difficult, especially about the future.” Although it sounds like something Yogi Berra might have said, the observation has been attributed to the eminent physicist Niels Bohr. U.S. Energy Information Administration (EIA) staff knows from its own experience that this is true, and we suspect that Phil, who has not had a very accurate record over the last 5 years, would also agree with Bohr.1

Despite warmer-than-usual weather so far this heating season, winter heating oil expenditures for the average U.S. household heating with oil (about six percent of all U.S. households) are expected to be historically high. Temperature is only one of the two main factors driving heating oil expenditures, the other being price.

Despite warmer-than-usual weather so far this heating season, winter heating oil expenditures for the average U.S. household heating with oil (about six percent of all U.S. households) are expected to be historically high. Temperature is only one of the two main factors driving heating oil expenditures, the other being price.

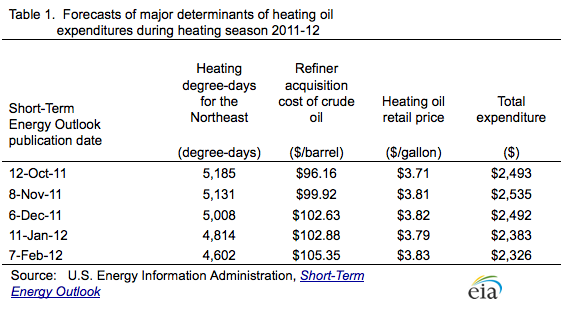

The U.S. Energy Information Administration (EIA) had expected big heating oil expenses since the beginning of the heating season. EIA defines the heating season as running from the beginning of October through the end of March. Last October, in the Short-Term Energy and Winter Fuels Outlook (STEO), EIA projected that winter heating oil expenditures for the average household in the United States were likely to be the highest on record, at about $2,500. EIA made only minor changes to that forecast in the subsequent November and December editions of its outlook. In each of the first three STEOs of the current heating season, total heating oil expenditures were forecast to exceed the previous record high of about $2,300 posted last winter (Table 1).

With 17 percent warmer-than-normal weather in the Northeast 2 (where over 80 percent of U.S. households that heat with heating oil are located) in October through December 2011, EIA cut its per-household heating oil expenditures projection by $110 in the January 2012 STEO compared with the initial October forecast, yet still predicted record expenditures, as heating oil prices remained high. While unseasonably warm weather has continued (January 2012 was about 19 percent warmer-than-normal in the Northeast), winter heating oil expenditures for the average household are nevertheless likely to remain the highest on record due to continued seasonal record high heating oil prices. The current update for heating expenditures (Short-Term Energy Outlook (STEO), February 7, 2012 release) lowers them to $2,326, still a record (Table 2).

With 17 percent warmer-than-normal weather in the Northeast 2 (where over 80 percent of U.S. households that heat with heating oil are located) in October through December 2011, EIA cut its per-household heating oil expenditures projection by $110 in the January 2012 STEO compared with the initial October forecast, yet still predicted record expenditures, as heating oil prices remained high. While unseasonably warm weather has continued (January 2012 was about 19 percent warmer-than-normal in the Northeast), winter heating oil expenditures for the average household are nevertheless likely to remain the highest on record due to continued seasonal record high heating oil prices. The current update for heating expenditures (Short-Term Energy Outlook (STEO), February 7, 2012 release) lowers them to $2,326, still a record (Table 2).

Of the two drivers of heating oil expenditures, the heating oil price and the volume of heating oil consumed by the average household, the latter is directly related to heating degree-days (the average of a day’s high and low temperature minus 65 degrees Fahrenheit). Projections of heating degree-days, and therefore of consumption, have declined with each issue of the STEO since the beginning of the heating season. The difference between the high (October 2011 STEO) and low (February 2012, STEO) forecasts for heating degree-days projections is almost 583 days, or a 13-percent difference. EIA’s winter heating oil price forecasts, on the other hand, having started in October at a record high of $3.71 per gallon, have since risen by a further 12 cents per gallon, or 3.2 percent. The primary driver for this winter’s high heating oil expenditures has been heating oil prices, not consumption.

High heating oil prices reflect high crude oil prices worldwide and the strength of the global distillate fuel market, which includes both heating oil and diesel fuel. Although heating oil has been declining as a share of total distillate consumption, global diesel fuel demand has been growing and will likely continue to grow, assuming strong economic activity in developing countries such as China, India, and Brazil. EIA’s expectation of increasing global petroleum demand, especially transportation fuels, over the next few years results not only in high world oil prices in general, but also in rising distillate prices in particular. In the February 2012 STEO, the projection for retail heating oil prices for next winter (October 2012-March 2013) is $3.97 per gallon, 15 cents per gallon higher than the current projection for this winter. This implies that average household heating oil expenditures for next winter will most likely exceed those of the current winter.

Groundhog Day arrives too late during the heating season to provide any significant choices for the heating oil customer. In these times of high heating oil prices, even better news from Punxsutawney Phil would have provided only very limited relief for consumers coping with high heating oil expenditures.

Gasoline price increases four cents per gallon

The U.S. average retail price of regular gasoline increased just over four cents to $3.48 per gallon. The average price is about $0.35 per gallon higher than last year at this time. Prices were up across all regions with the largest increase occurring in the Midwest, where prices increased six cents to $3.41 per gallon. Gulf Coast prices rose almost six cents to $3.35 per gallon. East Coast prices increased three cents per gallon, while Rocky Mountains prices were up four cents per gallon. West Coast prices rose two cents per gallon (the smallest regional increase), but prices there remain the highest in the Nation at $3.67 per gallon.

The national average diesel price increased less than one cent to $3.86 per gallon. The diesel price is $0.34 per gallon higher than last year at this time. Prices on the East Coast, Gulf Coast, Rocky Mountains, and West Coast all changed by less than a penny per gallon, but the Gulf Coast was the only major region that showed a price decrease. Midwest prices were up less than two cents to $3.75 per gallon. West Coast prices, which are the highest in the Nation, remained above the $4 per gallon mark for the fifth week in a row at $4.04 per gallon.

U.S. average residential and wholesale heating oil prices increase

The U.S. residential heating oil price increased by $0.02 per gallon during the week ending February 6, 2012 to $3.97 per gallon. This price is nearly $0.40 per gallon higher than the same time last year. The wholesale heating oil price increased by $0.05 per gallon over the same period to $3.21 per gallon, $0.40 per gallon higher than last year at this time.

The average residential propane price decreased by less than $0.01 per gallon during the week ending February 6 to reach a price of almost $2.86 per gallon, $0.03 per gallon higher than last year. The average wholesale propane price decreased by $0.03 per gallon to $1.20 per gallon. This was a decrease of about $0.21 per gallon when compared with the February 7, 2011 price of $1.41 per gallon.

Propane stocks dip again

Last week, U.S. propane stocks continued the seasonal draw by falling 2.3 million barrels to a total of 46.7 million barrels. The sharpest stock draw occurred in the Midwest with a weekly decline measuring 1.1 million barrels. Elsewhere, Gulf Coast stocks fell 0.7 million barrels, East Coast stocks dipped 0.4 million barrels, and Rocky Mountain/West Coast inventories were down 0.1 million barrels. Propylene non-fuel use inventories represented 10.6 percent of total propane inventories.

1 Comparing actual heating-degree-days in the Northeast for February and March with Phil’s predictions from 2007 through 2011, shows he was wrong 4 out of 5 years.

2 The Northeast comprises PADD 1A New England and PADD 1B Central Atlantic.

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!