2023 Economic Policy In China: Insights From The Government Work Report – Analysis

By Anbound

By He Jun

On the morning of March 5th, Chinese Premier Li Keqiang delivered the government work report to the National People’s Congress, which was also the last report after his ten-year premiership. Although the major economic policies for 2023 had already been set at the end of last year, researchers at ANBOUND believe that the report presented by Li remains an important window to better understand the economic goals and policies of China for 2023.

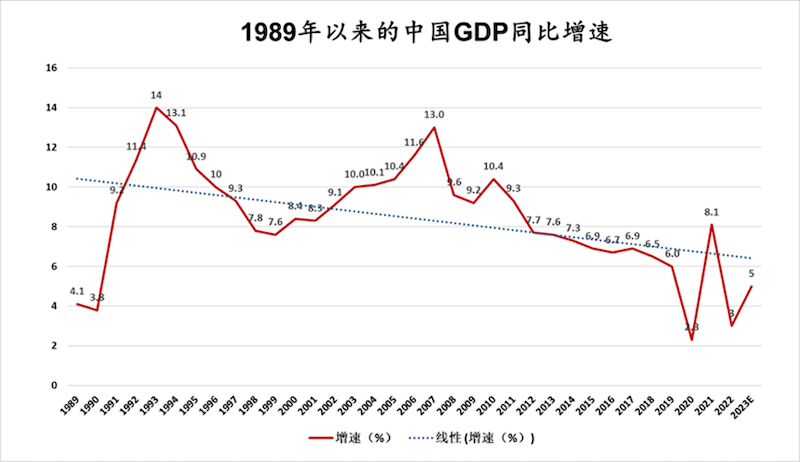

First of all, with regard to the main economic development goals this year, it is expected that the domestic gross domestic product (GDP) will increase by around 5%. The report also mentions that urban employment will increase by about 12 million, with an urban surveyed unemployment rate of around 5.5%. The increase in consumer prices will be around 3%; household income growth will be basically synchronized with economic growth. It also states that imports and exports will be stabilized, with a basic balance of international payments. Energy consumption and major pollutant emissions per unit of GDP will continue to decrease, with a focus on controlling fossil energy consumption.

We believe that the 5% economic growth target for this year is relatively conservative and cautious, considering the low base from last year. On the one hand, this shows that the Chinese government recognizes the increasing difficulties and challenges of the domestic and international economic environment. On the other hand, a relatively conservative target can avoid the embarrassment of failing to achieve the economic growth target, as was the case in 2022, and provide more room for economic policies. Furthermore, setting such a target can also maintain a steady pace and more or less achieve relatively stable economic growth in the last three years of the 14th Five-Year Plan. It should be pointed out that the 5% national economic growth rate is lower than the economic growth targets of most provincial-level regions. According to the weighted average calculation of GDP proportions, the average GDP growth target for provinces in 2023 is 5.6%, and the gap between the national target set in the government work report is similar to that of previous years.

Secondly, fiscal policy will continue to play a major role in the country’s macroeconomic policy for 2023. The report proposes that an active fiscal policy should be strengthened for more effective results. The fiscal deficit rate for this year is expected to be set at 3%, an increase of 0.2 percentage points from the previous year. Plans are in place to issue special local government bonds of RMB 3.8 trillion this year, an increase of RMB 0.15 trillion from the previous year’s RMB 3.65 trillion. The report also mentions that tax and fee preferential policies will be improved, and measures such as fee reduction, tax refund, and tax deferment will be continued, while certain measures will be tweaked. Furthermore, efforts will be made to ensure the basic livelihood of people at the grassroots level, especially the “three guarantees”: access to medical services, safe housing with basic amenities, and basic free education.

As “stable economy” has become the policy tone, the consensus is that the fiscal policy in 2023 will be more proactive. However, due to increasing government debt pressure, the expansion of fiscal policy in 2023 also faces significant constraints. China generally regards a deficit ratio of 3% as the psychological bottom line of fiscal security risk. Before the outbreak of the COVID-19 pandemic in 2020, its deficit ratio had never exceeded 3%. In response to the pandemic’s impact, the deficit ratio in 2020 was raised to a historic high of 3.7%, then lowered to 3.2% in 2021 and further to 2.8% in 2022. This time, returning to a deficit ratio of 3% for stabilizing the economy appears to be a limited fiscal expansion. It is worth noting that this year’s tax and fee preferential policies are facing adjustments. Under fiscal pressure, many such policies are facing difficulty in sustainability, but as the report implies, the power of policy adjustment is actually given to the finance and taxation department and local governments. Local governments will then need to determine which policies should be continued and which ones should be tweaked based on the local business situation and the recovery of the real estate market.

Thirdly, regarding the target of grain production, the report proposed to maintain grain production at more than 1.3 trillion jin (650 billion kg) in 2023. This target is also a relatively realistic and conservative one. China’s grain production in 2022 has reached 1.37 trillion jin (685 billion kg), and the target for this year means that the policy for grain production is mainly to ensure stability, with increasing production as a secondary consideration. However, it is also important to note that the government work report also emphasizes “stabilizing the sowing area of grain, promoting oilseed production, and implementing a new round of action to increase grain production by 100 billion jin (50 billion kg)”, which means that efforts should still be made to increase grain production as much as possible. Due to factors such as limited cultivated land area, limited seed resources, the impact of climate change, and natural disasters, there is an increase in the difficulty for grain production growth in the country, until there is a significant breakthrough in agricultural technology.

Fourthly, the report proposed that industrial policies should prioritize development and safety. It aims to promote the transformation and upgrading of traditional industries, cultivate and expand strategic emerging industries, and focus on strengthening the weak links of industrial chains. When it comes to science and technology policies, self-reliance is emphasized. It also mentioned the government’s organizational role in key core technology research, as well as highlighted the main position of enterprise innovation in science and technology. The report stated the need to accelerate the construction of a modern industrial system, focus on the key industrial chains of manufacturing and concentrate high-quality resources in this regard, for instance, the development and storage of crucial energy and mineral resources in the country. Other than that, it also discussed hastening the digital transformation of traditional industries and small and medium-sized enterprises, with a focus on improving the level of high-end, intelligent, and green development. The improvement of the logistics system is mentioned as well. On the other hand, concerning the digital economy, it stated to “enhance the level of normalized supervision”, and “support the development of platform economy”.

Against the backdrop of emphasizing the development of the real economy and strengthening the security of the industrial and supply chains, there will be some changes in China’s industrial policies in the future. First, there will be more emphasis on the independent controllability of key technologies and increasing domestic substitution efforts in some areas; Second, under the new national system, it is expected that there will be an increase of R & D efforts in the key core technology fields; Third, more attention will be paid to the industrial chains, clusters, and ecology, with focus given to “domestic circulation” of the industrial sector. However, at the same time, China’s industrial policies should not become a closed system. Maintaining openness in the industrial and technological sectors will still be an important principle for its industrial policies.

Fifthly, regarding employment goals, while lowering the economic growth target, the report raised the employment target for 2023, with new urban employment in 2023 being approximately 12 million, and the surveyed urban unemployment rate around 5.5%. The target for new urban employment in 2022 was more than 11 million, and the surveyed urban unemployment rate of that year was within 5.5%. By comparison, both targets for 2023 have been raised. The reason for this is related to the employment situation in 2022. Affected by the repeated impact of the novel coronavirus outbreaks, China’s surveyed urban unemployment rate fluctuated significantly in 2022, reaching a high of 6.1% in April, and remaining high in March, May, and November, all of which exceeded the target of 5.5%, and only fell to 5.5% in December last year. The new urban employment in 2022 was 12.06 million, which not only achieved the expected target but also provided a benchmark for employment work in 2023.

Sixthly, regarding the policy of opening up to the outside world and foreign trade, the report proposed to attract and utilize foreign investment with greater intensity, expand market access, and increase openness in the modern service industry, as well as implement national treatment of foreign enterprises. It also makes mention of promoting the joining of high-standard economic and trade agreements such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). At the same time, it talked about the importance of improving imports and exports in supporting the economy. Again, the term “stability” is mentioned when it discusses import and export.

Noticeably, China has not changed its fundamental principle of opening-up. Yet, whether the increasingly deteriorating international geopolitical environment still permits China to achieve openness, and whether foreign capital agrees with its opening-up policy and market openness, would be another matter. Looking objectively, the environment and conditions that attract foreign investment in China are deteriorating, and the prospects are not quite optimistic. In terms of foreign trade, the report proposes the goal of “promoting stability and improving quality”, which lowers the requirements for foreign trade to drive the economy, indicating that the unfavorable situation of China’s foreign trade environment and the global supply chain shift has already been anticipated.

Lastly, the work report does not mention specific defense spending, but the report on the implementation of the central and local budgets for 2022 and the draft central and local budgets for 2023, released by the Ministry of Finance on March 5, stated that China’s defense spending in 2023 will be RMB 1.5537 trillion, an increase of 7.2%.

It can be seen that the expected growth rate of defense spending is 2.2 percentage points higher than that of the economy during the same period. Some organizations believe that China’s defense spending in 2022 had increased by 7.1% year-on-year. Although this year’s increase is only 0.1 percentage point higher than last year, last year’s defense spending increase of 7.1% was based on a target GDP growth rate of 5.5%, while this year’s 7.2% increase is based on a GDP growth rate of 5%. Therefore, the defense budget target for 2023 is relatively positive. Taking into account the current international situation, many countries are increasing their defense budgets. In December 2022, the U.S. Congress passed a 2023 defense budget totaling USD 857.9 billion, an increase of 13.93% from 2022. In December 2022, the Japanese cabinet approved a record-high defense budget for 2023, totaling JPY 6.8 trillion (equivalent to USD 51 billion), a significant increase of 26.3% from 2022, and it plans to double defense spending within five years. Germany plans to establish a fund in 2023 with a total of EUR 100 billion to improve its weapon and equipment level. The EU Defense Ministers also stated that they will increase defense spending by EUR 70 billion in three years. It can be expected that China’s defense spending will continue to grow steadily in the future.

Final analysis conclusion:

Overall, China’s government work report for 2023 has set realistic expectations for economic development this year. It reflects a shift towards pragmatic domestic policy goals following the economic impact of 2022, as well as anticipates the deterioration of the external economic environment. 2023 is a crucial year for the country’s 14th Five-Year Plan and for the new government. The situation facing China’s economic and social development, both domestic and international, will remain to be challenging.

He Jun is a researcher at ANBOUND