Lessons From India For The Power Sector In Sub-Saharan Africa – Analysis

By Observer Research Foundation

The GreenCo model represents a practical solution that recognises and supports the development of the regional power pools.

By Ana Hajduka

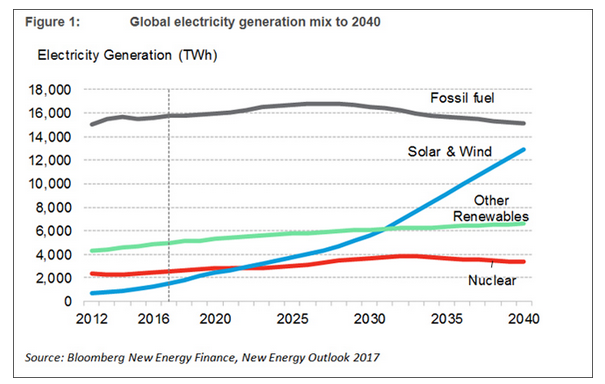

Sub-Saharan African (SSA) countries, and Southern African Power Pool (SAPP) countries in particular, are in an excellent position to benefit from the momentum of the global paradigm shift towards a cleaner, more sustainable energy future, in which “the greening of the world’s electricity system is unstoppable.” [1] The standardised cost of renewables and a central metric that measures affordability has decreased significantly and continuously over the past decade. While already cost competitive in many countries, and even cheaper than fossil-based generation options in some, costs are predicted to continue declining in the future; for this reason and others, renewables are well positioned to play a major role in the electrification of SSA. These developments present the African energy sector with unprecedented opportunities to leapfrog in to an energy future dominated by renewable sources.

The African and international development community and others seeking to support the deployment of grid-connected renewable energy in SSA is addressing how to best convert this staggering potential into operational projects. This conversion can, in turn, provide dependable and affordable electricity sources at the scale required for economic and social development in the region.

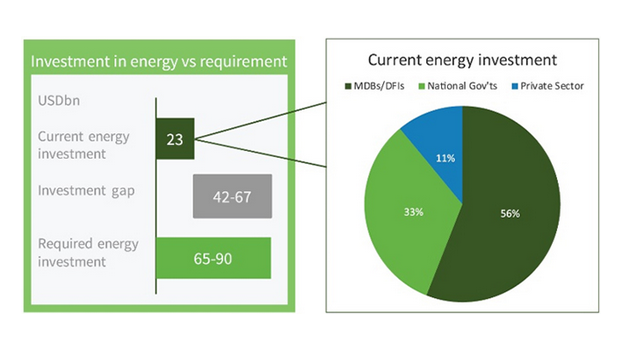

The African Development Bank estimates that there is a funding gap of USD 42-67 billion per year that must be bridged in order to achieve universal access to electricity in Africa by 2025. This target will not be reached unless private sector capital is mobilised.

Currently, the lack of creditworthy offtakers in the SSA is one of the key factors deterring investment in the African renewable energy sector. Weak balance sheets and poor payment track records of many national utilities is one of the reasons why commercial banks have been unwilling to fund Independent Power Projects (“IPPs”), which has resulted in limited competition, and consequently, a higher cost of capital.

New business models are required through which the lack of creditworthiness in the power sector in SSA can be overcome. One such model is the Africa GreenCo which is designed to tackle this creditworthiness constraint by establishing an independently managed, creditworthy intermediary offtaker, and a power services provider to mediate between renewable electricity generation companies on the one hand, and both state owned and private sector off-takers on the other. GreenCo will operate as a member of the African regional power pools, aggregate offtaker credit risk, and diversify both supply and demand side risks on a regional basis. In case of a utility defaulting, GreenCo will rely on various risk mitigation tools including the right to sell power to other utilities/bulk power purchasers via the power pool.

The GreenCo model represents a practical solution that recognises and supports the development of the regional power pools. It is focused on enabling a sustainable market through which there can be a shift from supporting isolated investments to catalysing systemic change in the energy markets. This solution will attract significant volumes of private sector finance.

GreenCo aims to emulate the success of comparable independent power intermediaries and aggregators in developing markets. These pioneering interventions have demonstrated the financial feasibility and transformative market-making impacts of intermediaries on local power markets.

The most applicable case study to the GreenCo model is the PTC India Limited (PTC), formerly known as Power Trading Corporation of India Ltd. PTC was established under the Government of India in 1999 as a PPP. Its primary focus was to develop a commercially vibrant power market in India. PTC was mandated to act as an entity for credit risk mitigation.

The evolution of the Indian power market up until the PTC’s creation closely mirrors that of the African power markets. India had five regional grids, each governed by a Regional Electricity Board (REB), comprising of the Heads of the member State Electricity Boards (SEBs). These acted as each state’s public sector power utility, while each regional area was minimally interconnected. During the 1990s, privately financed and operated IPPs were allowed to support the growing demand for power. IPPs contracted directly with SEBs, with a guarantee from the State Government. In some cases, counter-guarantees were provided by the Central Government. Investment decisions in power generation and transmission infrastructure were not coordinated and inefficient: there was limited inter-state and almost no inter-region power trading.

The PTC was developed in response to the Government’s decreasing appetite and capacity to sign sovereign and state-level guarantees for IPPs. There was also recognition that there was scope for more efficient power trading, which would ultimately de-link power purchases from direct fiscal impact.

The two core components to PTC’s operating model are below:

- Acting as an intermediary PPA offtaker for IPPs that are creating transparent and standardised negotiation and contracting practices, while also selling power to SEBs under PSAs. The PTC directly addressed IPP concerns about creditworthiness by limiting exposure to specific utilities and payment securities and through its ability to divert power to alternative buyers in case of default. The PTC’s risks were to be mitigated by a planned deduction from Central to State government grants.

- Trading power from regions/utilities with a surplus to regions/utilities with a power deficit on a short-term basis. The PTC was a pioneer in the Indian market for differentiated peak and off-peak power trading, and introduced the ‘Day Ahead Market.’ In addition to utilities, the PTC works with more than 400 industrial/bulk consumers directly.

The PTC management believed that the following conditions needed to be satisfied in order to be seen to be creditworthy:

- It must have sufficient net worth to collateralise PPA obligations;

- It must have a higher profile in the market;

- Investors must understand and accept the PTC’s capacity to trade in case of default

- It had to ensure timely payment by the off-taker/buyer SEB under the PSA.

Using its capital base, the PTC India has been able to act as a creditworthy PPA counterparty for 7,000MW of installed capacity from a pipeline of 14,000MW. This has unlocked well over USD 5 billion of private investment even by a conservative estimate of capital costs for new IPPs. As planned, the PTC’s involvement as an off-taker since 2004 has resulted in a shift from government guarantees.

The PTC’s role in developing the Indian and regional cross-border power markets has been an unqualified success. The following information supports this:

- It has helped grow overall traded volumes from 1.6 TWh in 2001 to 37 TWh in 2015.

- It has a 30-40% market share.

- Total short term traded volumes have increased from 2% of total generation to approximately 10% from 2005 to 2015.

- It has demonstrated the viability of cross-border power trading.

- It ahs increased investor confidence in supporting IPP.

- Suppliers’ fixed costs per unit of power fell as capacity utilisation increased.

- Supplier/power plant revenues increased as they were able to maximise capacity utilisation.

- Areas of power deficit moved closer to supply/demand equilibrium.

The PTC acts as an indicator of the potential impact and financial feasibility of an intermediary model; for GreenCo the key questions are then how this model can be adapted to fit African power markets. While the Indian and African contexts are clearly different, and operating across multiple countries presents additional challenges when compared to operating in a single country, the PTC’s former management offered the following insights to consider when looking at the similarities between the India and Africa:

- Fragmented State (India) and National (Africa) utilities and transmission infrastructure.

- Growing collaboration and coordination across regional power pools (5 in India, 4 in sub-Saharan Africa).

- Low average creditworthiness of off-taker utilities.

- Desire to eliminate sovereign guarantees for PPAs.

- High growth in/latent demand for power.

- Focus on renewable energy versus fossil fuels.

The PTC India therefore provides a concrete example of the significant role a renewable energy intermediary offtaker, aggregator and power trader can play in increasing power generation and trade and stimulating the power market. GreenCo is a model of a more context relevant South-South collaboration which aims to achieve systemic impacts in the way power markets are developed in sub-Saharan Africa.

Africa GreenCo is working closely with the Government of Zambia on the operationalisation of its business model by Q4 2019 — i.e. the establishment of a new creditworthy intermediary renewable energy power purchaser: GreenCo Power Services Limited (GreenCo), which will be a PPP entity between the Government of Zambia, the international development community, and the private sector.

GreenCo will act as:

- A renewable energy creditworthy power buyer and seller: GreenCo buys power from small to medium sized IPPs, on-selling through long-term contracts to utilities and private buyers; it also executes shorter-term trades on the SAPP.

- An aggregator of Risk and Risk Capital: Strongly capitalised, GreenCo assumes credit risk of utilities and private buyers, resulting in reduced tariffs.

- An operational Aggregator of renewable energy supply.

- Downside Support: Where buyers fail to pay, GreenCo sells to alternative buyers, or through SAPP markets; where termination scenarios arise, GreenCo uses its capital structure to cover outstanding commercial project debt in affected IPPs.

- A champion of new renewable energy services and innovations for the region in partnership with the public sector.

GreenCo will be embedded in the local and regional electricity sector and will be able to take practical steps to diversify and mitigate risk. This will catalyse sustainable structural market change and support the growth of national and regional electricity markets. GreenCo will operate as a member of regional power pools and will mitigate both demand-side and supply-side risks. GreenCo will help unlock the private capital required to meet Sustainable Development Goals at reduced cost, with less reliance on host Government support, and at lower generation tariff to utilities.

While GreenCo will start operations in Zambia, it will provide regional market support and become a renewable energy offtaker in neighbouring countries.

[1] Bloomberg New Energy Finance