The Coronavirus Won’t Be The Cause Of The Next Bust, But It Will Make It Worse – Analysis

By MISES

By Frank Shostak*

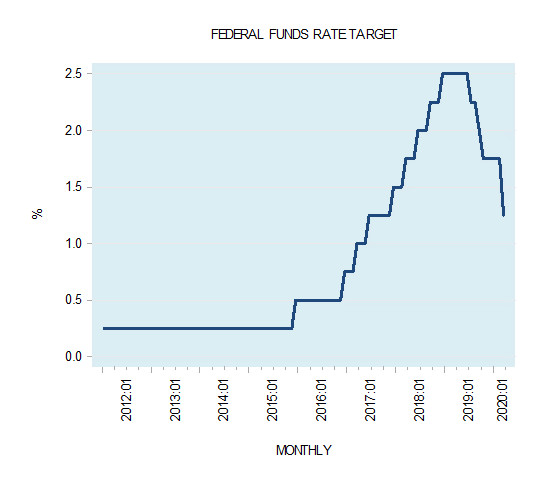

Global policymakers moved to ease public anxiety over the coming economic hit from the coronavirus as analysts warned of a severe slowdown in growth and a possible recession if the virus continues to spread. The US Federal Reserve cut interest rates on Tuesday, March 3, in an emergency move designed to shield the world’s largest economy from the impact of the coronavirus. The central bank said it was cutting rates by a half percentage point to a target range of 1.00 to 1.25 percent.

“The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity. In light of these risks and in support of achieving its maximum employment and price stability goals, the Federal Open Market Committee decided today to lower the target range for the federal funds rate,” the Fed said in a March 4 statement.

The World Bank and International Monetary Fund signaled that they were also ready to assist, particularly poor nations. Monetary policymakers from Japan to Europe pledged to act as needed to stem any economic fallout as infections spread.

The Organization for Economic Co-operation and Development (OECD) said that global growth could plummet to just 1.5 percent in 2020, far less than the 3 percent it projected before the virus surfaced, should the outbreak sweep through the Asia-Pacific, Europe, and North America. If things get bad enough, Japan and Europe could plunge into recession, the OECD warned. Predictions for the United States were nearly as bad: Most analysts expect zero or negative growth in the second quarter, with some forecasting a potential recession before year’s end.

The coronavirus is seen as inflicting both supply and demand shocks, which economists hold makes it difficult for policymakers to handle.

Economic Shocks: The Mainstream View

From the Great Depression of the 1930s until the early 1970s, most economists viewed economic fluctuations as the outcome of shocks to aggregate demand. Sudden changes in consumer preferences were said to cause a fall in aggregate demand, which would drag the entire economy below a path of stable economic growth. In contrast, a sudden increase in optimism was said to lead to excessive consumer expenditure, which would push the economy above a stable growth path.

Economists regarded these deviations from stable growth paths as failures of the market economy to coordinate demand and supply. Consequently, it was seen as necessary for the government and central bank to interfere in order to bring the economy onto a stable growth path.

This way of thinking views the economy as an object that moves along a path of stable economic growth and which is occasionally pushed off course by shocks. Whenever a shock pushes the economy above the path, in this view, it sets in motion an unsustainable economic boom. Likewise, a shock or a sequence of shocks that push the economy below a trajectory of stable economic growth results in an economic bust.

According to this way of thinking, a major source of disturbances is a sudden change in people’s psychology. Hence, if “out of the blue” consumers and businesspeople become optimistic and embark on a buying spree, this pushes the economy above the stable trajectory and sets in motion an economic boom. Likewise, recessions or economic busts are set in motion if people suddenly change their psychology and stop spending.

Since deviations from the path of stable economic growth are costly, it is held that the government and the central bank must always be on guard to introduce policies that will offset these deviations. For instance, if people become pessimistic the central bank must offset this by accelerating the money supply growth rate and by lowering interest rates and vice versa. In addition, the government must raise its expenditure in order to offset their sudden unwillingness to spend. Similarly, it is the role of government authorities to be vigilant to various other shocks such as the coronavirus spread and counter their effects by means of suitable policies.

Although it is held that one can devise a set of rules that would enable authorities to keep the economy on a stable trajectory, in reality it is not that simple. Because of variable lags between policy changes and their effect on various parts of the economy, it is not possible, so it is argued, to establish the correct timing of various policy measures. It is also maintained that a lack of sufficient knowledge regarding the strength of the economy makes it very hard to decide on the required degree of monetary and fiscal measures.

Consequently, in many instances various monetary and fiscal policies rather than stabilizing the economy have become a major source of instability.

The Market Economy Does Not Move along a Trajectory

A market economy cannot be compared to an object that moves along a particular trajectory. In a market economy, producers exchange among themselves various goods and services. Through the production of goods and services a producer acquires means that enables him to secure the goods and services of other producers. A producer exchanges things he has produced for things he prefers more.

In a free market economy, every producer pays for his consumption, or funds it, by means of the goods and services he has produced. It is, however, the availability of final goods and services that ultimately determine people’s well-being. The stock of these goods is what the pool of real savings is all about.

Although shocks can disrupt the pace of economic activity, they have nothing to do with the phenomenon of recurrent boom-bust cycles. This phenomenon requires a mechanism that persistently and systematically feeds and supports it. The only mechanism that does this is central bank monetary policy.

Monetary Policies and Cycles

While in a free, unhampered market economy there is a tendency toward harmony between production and consumption, this is not so once we introduce to our discussion the central bank, which disrupts this harmony.

In a free unhampered market economy, money facilitates the exchange of one producer’s production for the production of another. By means of money, something is exchanged for something else. However, this is not so when the loose monetary policies of the central bank set in motion the creation of money out of “thin air.”

The newly generated money gives rise to consumption that is not supported by the production of real wealth. Money out of “thin air” gives rise to various activities that would not emerge in a free market environment. The emergence of these nonproductive activities constitutes an economic boom. During an economic boom, real savings are diverted from productive activities to nonproductive activities by way of money out of “thin air,” weakening the production of wealth.

Whenever the central bank tightens its stance, i.e., raises interest rates and curtails monetary pumping, this undermines the existence of various nonproductive activities and threatens their existence. This is the essence of an economic bust, or recession. Observe that a tighter monetary stance slows down the diversion of real savings to nonproductive activities, which helps wealth generating activities.

It follows that an economic bust is nothing more than the liquidation of nonproductive activities that have emerged with the support of previous loose monetary policy. Note that the reason recurring boom-bust cycles is that central bank authorities continuously pursue so-called monetary policies that are aimed at navigating the economy toward a path of stability and prosperity.

So, if recessions are about the liquidation of nonproductive activities how do we categorize an event such as the coronavirus? What is the contribution of a virus to a recession? The answer is that the coronavirus has nothing to do with the phenomenon of a recurrent boom-bust cycle. However, it does have the potential to paralyze production activity, which undermines the pool of real savings and therefore future prospects for economic growth. This could especially be worse if the lagged money supply growth was declining too, which would mean that we would also be observing a decline in nonproductive activities. In this case the impact could be profound.

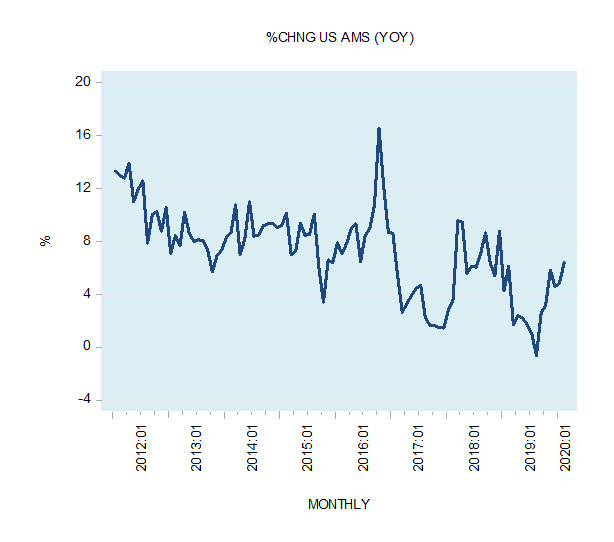

This means that the economic bust is likely to emerge because of the fall in the growth momentum of money. (The coronavirus is likely to amplify the bust). Is this what we are observing currently in the money supply? In the shorter term from a monetary perspective, the slight pickup in the growth rate in the AMS at the beginning of 2018 indicates that we may see a slight improvement in the economic picture for at least the first half of this year before reverting to slowing down. It is also worth noting that over the long term the yearly growth rate of the AMS fell from 13.9 percent in April 2012 to –0.6 percent by August 2019 (see chart).

The coronavirus can only make things much worse as far as the pool of real savings is concerned. It is questionable how the loosening of the monetary stance by the central bank can defend an economy from the coronavirus. All that such policies are going to generate is a further depletion of the pool of real savings. Loose monetary policy cannot speed up the development of the necessary vaccine to fight the coronavirus, for example. Such a policy is going to damage further the pool of real savings, delaying any future economic revival.

The Coronavirus Will Not Be the Cause of a Bust

The likely emergence of an economic bust is due to the coronavirus, as suggested by popular thinking, but is rather the outcome of the Fed’s monetary policy. Boom-bust cycles are not caused by shocks such as the coronavirus. The mechanism that is responsible for the them is central bank monetary policy. The coronavirus shock is likely to weaken the pool of real savings, thereby amplifying the economic bust, but it has nothing to do with the boom-bust cycle as such.

*About the author: Frank Shostak‘s consulting firm, Applied Austrian School Economics, provides in-depth assessments of financial markets and global economies. Contact: email.

Source: This article was published by the MISES Institute