Getting Back To Growth – Analysis

By Lone Christiansen, Ashique Habib, Margaux MacDonald and Davide Malacrino

Producing and consuming more goods and services for the same amount of work sounds too good to be true. In fact, it’s entirely possible. Higher productivity is one of the key ingredients to higher economic growth and incomes. It’s all about how workers become more productive.

For many of us, the COVID-19 pandemic has changed the way we work and spend. The question is how these changes will affect our productivity, both now and into the future.

While it’s difficult to forecast long-run productivity, particularly in the current environment, there are two key channels through which the pandemic might influence productivity: accelerated digitalization and a reallocation of workers and capital (e.g. machines and digital technologies) between different firms and industries. Our recent note examines how all this works.

Productivity boost

The pandemic accelerated the shift toward digitalization and automation, including through e-commerce and remote-work—and these trends seem unlikely to reverse.

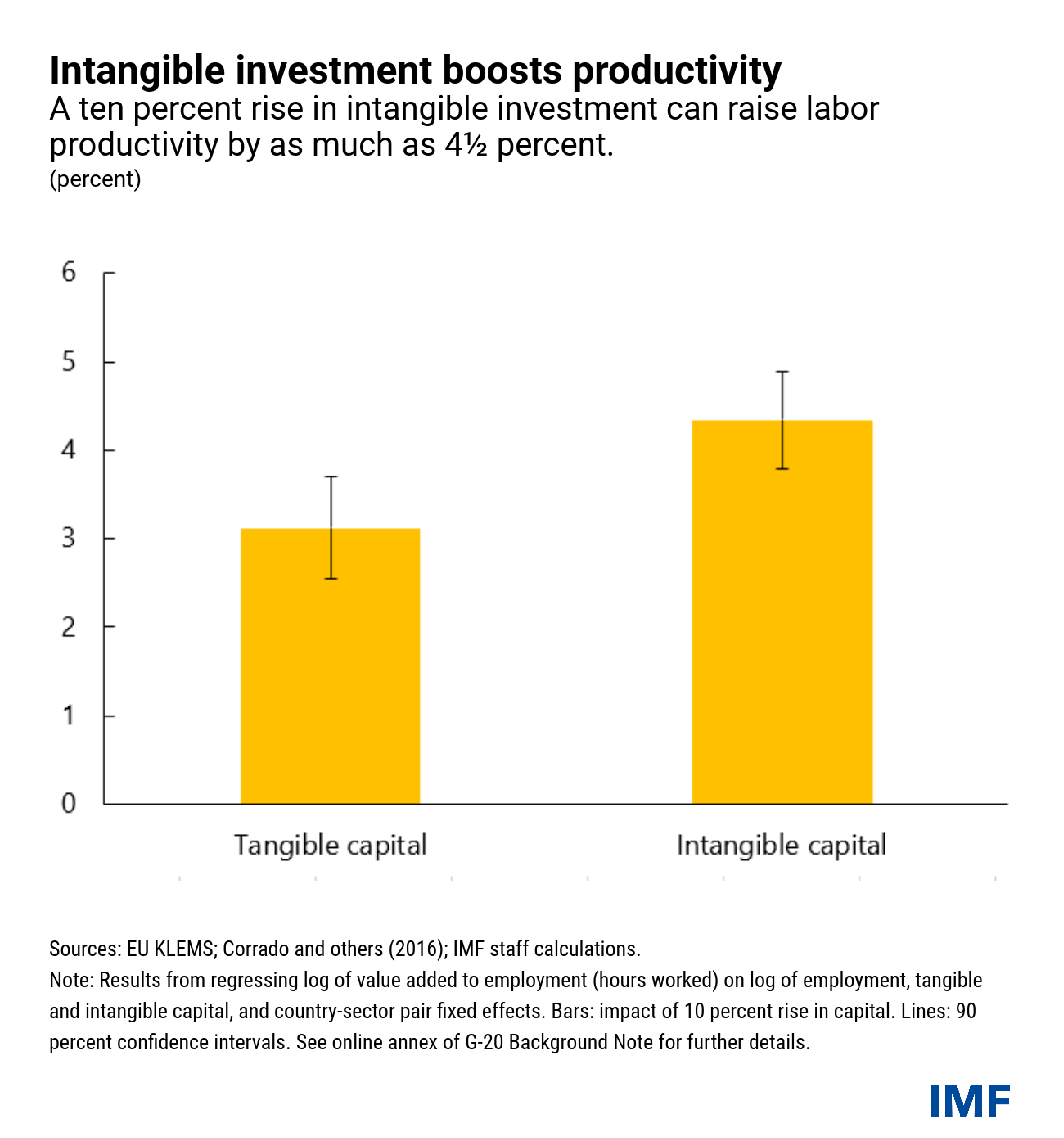

These changes are likely to impact productivity. Recent investments in digital tools—ranging from video conferencing and file sharing applications to drones and data-mining technologies—can make us more efficient at our work. As shown in the chart below, for a sample of 15 countries over 1995–2016, a ten percent rise in intangible capital investment (which is where assets like digital technologies are captured in the national statistics) is associated with about a 4½ percent rise in labor productivity—likely reflecting the role of intangible capital in improving efficiency and competencies.

In comparison, a boost in tangible capital (such as buildings and machinery) is associated with a slightly smaller rise in productivity. As COVID-19 recedes, the firms which invested in intangible assets, such as digital technologies and patents may see higher productivity as a result.

However, the benefits will likely not accrue evenly to everyone. Because investment in intangibles is sensitive to credit conditions, intangible investment may decelerate if financial conditions tighten or firms’ balance sheets worsen as a result of the crisis. Such developments, along with the fact that many large, dominant firms (especially in digital services sectors) performed better than peers during the crisis, could contribute to a rise in market power, which could stifle innovation over time.

Additionally, some jobs vulnerable to automation may never come back, which could mean job losses, prolonged unemployment, and workers having to search for work in different sectors where their existing skills may not be well-suited. This would be the other, darker side of the coin of productivity gains through further digitalization.

Reallocation during the pandemic

With sectors impacted very differently by the pandemic, some degree of ‘resource reallocation’ is likely occurring—for example, shifts in workers across firms as they are laid off or hired. This is occurring for at least two (possibly related) reasons: (i) the churn of businesses entering and exiting the market and (ii) changes in consumer demand.

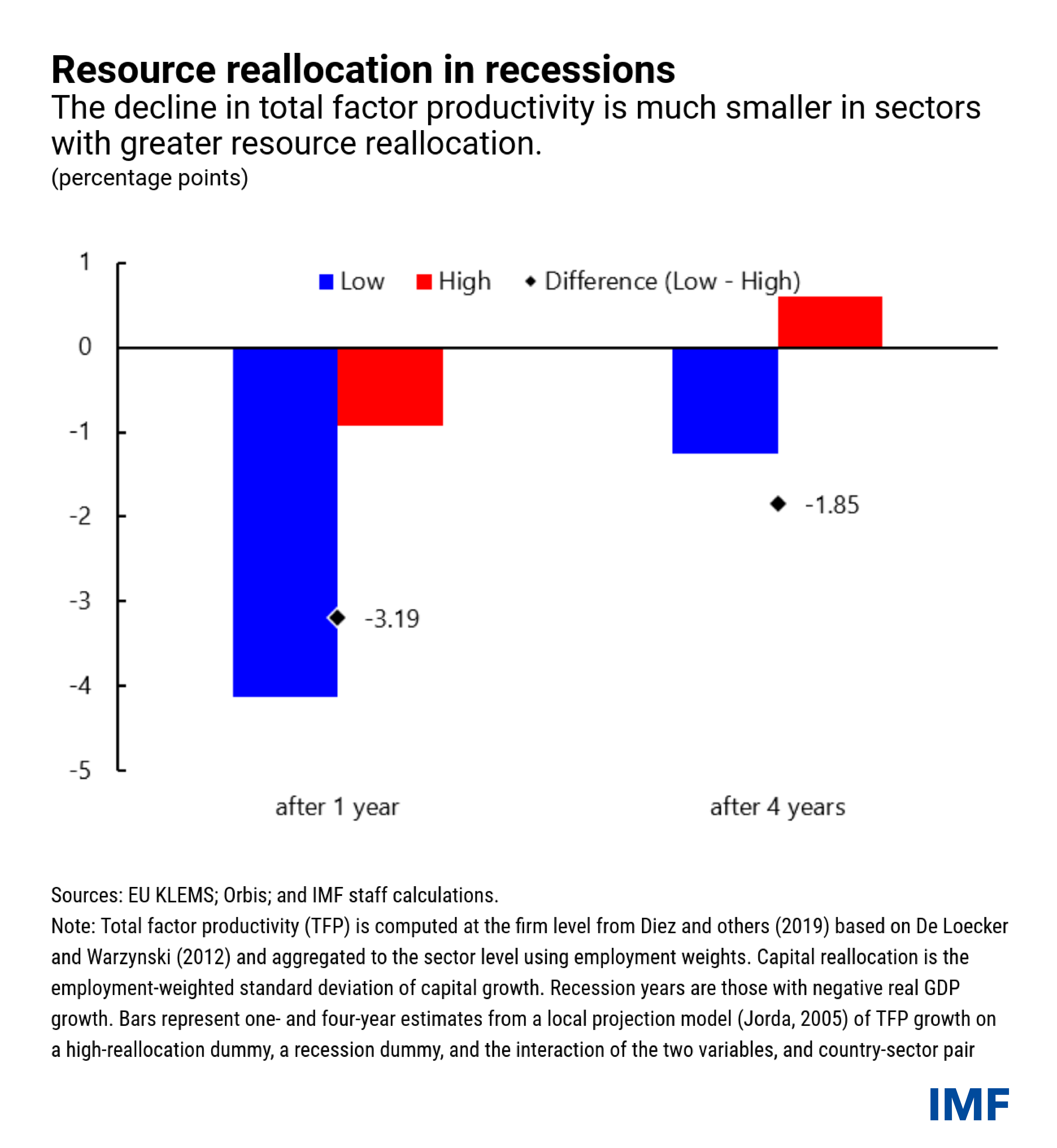

First, the flow of labor and capital toward more productive firms normally lifts productivity and can help cushion the blow of a recession (for example, if laid-off workers are re-hired by more productive firms). As shown in the chart below, an analysis based on firm-level data from 19 countries over 20 years shows that sectors with greater resource reallocation tend to experience a significantly smaller decline in total factor productivity during recessions and recover faster.

Policy actions may influence how much reallocation there is between firms, and thus productivity growth, but the direction is uncertain. For instance, broad-based fiscal support during a crisis could support productivity if it helps firms with the most potential to survive. However, it may also keep resources locked in less productive firms, which could hold back overall productivity growth. The degree to which these forces offset one another is not yet known and depends on how much labor and capital flow to firms that are most productive.

Second, the shift in demand away from in-person services where output per worker tends to be relatively low (e.g. restaurants, tourism, brick-and-mortar retail) toward digital solutions and sectors where output per worker is higher (e.g. e-commerce, remote work) suggests that resource reallocation across sectors may have lifted overall productivity. Yet, the lasting effects of all the shifts that have taken place during the pandemic are highly uncertain, with some sectors likely to rebound (e.g. tourism) and others likely to see more permanent changes (e.g. retail).

Policies can help

Ensuring an efficient reallocation of resources while protecting vulnerable groups can support a strong recovery. This can be achieved in multiple ways, including by:

- Ensuring that capital in failed firms is quickly put to more efficient use, through policies such as improved insolvency and restructuring procedures.

- Promoting competition to enable the exit and entry of firms to help curb market power.

- Supporting displaced workers, by gradually refocusing policy support from retention to reallocation, to facilitate adjustment to the new normal as the recovery gains speed. Efforts to reskill workers, including through on-the-job training, will also help support inclusiveness as well as boost human capital and strengthen potential growth.

Finally, to reap the benefits for productivity of investment in intangibles, ensuring adequate access to financing for viable firms is essential.

Despite the economic damage caused by the COVID-19 pandemic, investments in technology and know-how could help lift productivity. However, for this to materialize and be broadly shared, policies have a key role to play.

*About the authors:

- Lone Christiansen is a Deputy Division Chief in the Multilateral Surveillance Division of the IMF’s Research Department. Previously, she has worked as an economist in the IMF’s Strategy, Policy, and Review Department and in the European Department.

- Ashique Habib is an Economist in the Research Department of the IMF where he works in the Multilateral Surveillance Division.

- Margaux MacDonald is an Economist in the Research Department of the IMF where she works in the Multilateral Surveillance Division.

- Davide Malacrino is an Economist in the Research Department of the IMF.

Source: This article was published by IMF Blog