A Bank Crisis Was Predictable: Was The Fed Lying Or Blind? – OpEd

By MISES

By Tho Bishop*

Welcome to Whose Economy Is It, Anyway?, where the rules are made up and the dollars don’t matter. Or at least that seems to be the view of the Yellen regime.

As Doug French noted last week, Silicon Valley Bank (SVB) was the canary in the coal mine. Over the weekend, Signature Bank became the third-largest bank failure in modern history, just weeks after both firms were given a stamp of approval by KPMG, one of the Big Four auditing firms.

While some in the crypto community are suggesting that the closure of Signature Bank has more to do with a larger war on crypto, the regulatory action was enough to push coordinated action from the Federal Reserve, Federal Deposit Insurance Corporation (FDIC), and the Treasury to do what they do best, ignore clearly established rules to flood a financial crisis with liquidity.

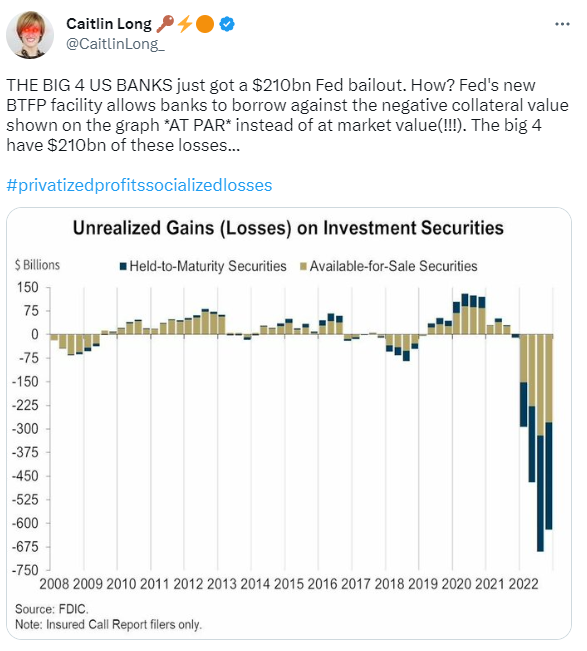

Out: FDIC insurance limits on bank deposits lower than $250,000, haircuts for the largest bank depositors, and Walter Bagehot’s golden rule to lenders of last resort, “Lend freely, at a high rate of interest, against good collateral.” In: emergency financing to secure all deposits, accepting collateral at face value (rather than its current diminished market value) with no fee.

Don’t worry, the government promises this is only a year-long program. It definitely won’t become a standing policy. They promise.

It is poetic that Barney Frank was serving as the director of Signature Bank at the time of its capture. This emergency action from the feds signals the failure of Frank’s key legislative accomplishment, the 2010 Dodd-Frank Act. The bill designated large financial institutions as “systemically important financial institutions,” with an additional layer of regulatory scrutiny as a means to end “too big to fail.”

Instead, the bill consolidated community banks into larger regional banks and empowered financial regulators that have now proven to be blind to the underlying risks of the banks. After all, it was state bank regulators, not the feds, that raised the flag on both SVB and Signature. Meanwhile, the hyper-fragile environment of the post-2008 financial crisis has created an environment where most financial institutions are treated as too big to fail, with no one too small to bear the costs.

Federal bank regulators and KPMG auditors aren’t the only ones blind to the underlying problems facing these large regional banking institutions. Just last week, Jerome Powell said that he saw no systemic risk in the banking sector from the Fed’s aggressive rise in interest rates and signaled confidence that they would continue in the near future. Less than a week later, few buy Powell’s projection.

While Powell deserves a level of credit for his willingness to take inflation risks more seriously than many of his peers, the instability we’re witnessing was predictable. As is repeated regularly on the Mises Wire, the decade-plus reign of low interest rates didn’t only incentivize financial risk but necessitated it. The benefactors were tech firms, the real estate market, and a variety of other financial markets. The consequence has been corporate consolidation and the creation of numerous overly leveraged, unprofitable zombie companies that depend upon refinancing at low interest rates to function. The Fed’s rising interest rates have always been a threat to these parts of the economy.

In defense of Powell, lying about the state of the economy is a necessary part of the modern financial system. Regardless of one’s opinion about the virtues of free banking, state intervention has created a fractional reserve banking system saturated with risk and moral hazard. Since no bank is equipped to deal with a significant increase in demand for deposits, even relatively conservative banks can be brought down by a confidence crisis fueled by the instantaneous communication of social media.

The feds have signaled a bailout for all because everyone is at risk.

It doesn’t have to be this way. Caitlin Long has been fighting the financial regime for years in her quest to create Custodia Bank, a full-reserve bitcoin bank in Wyoming. There has been a coordinated attempt to stop her efforts, ironically including voicing concerns that Custodia could fuel “systemic risk.” Honk honk.

The short-term question is whether the efforts of the Fed and the Treasury are enough to prop up confidence and prevent escalating pressure on financial institutions. However, these are not solutions to the underlying systemic problems that these bodies have created.

Unfortunately, the consequence of the complete politicization of the economy is that financial policies are necessarily focused on the short term at the expense of the long term.

There is no serious solution until there is the political will to deal with our monetary hedonism.

About the author: Tho is an assistant editor for the Mises Wire, and can assist with questions from the press. Prior to working for the Mises Institute, he served as Deputy Communications Director for the House Financial Services Committee. His articles have been featured in The Federalist, the Daily Caller, and Business Insider.

Source: This article was published by the MISES Institute