EIA Projects Lower US Gasoline Prices Despite Recent Demand Growth – Analysis

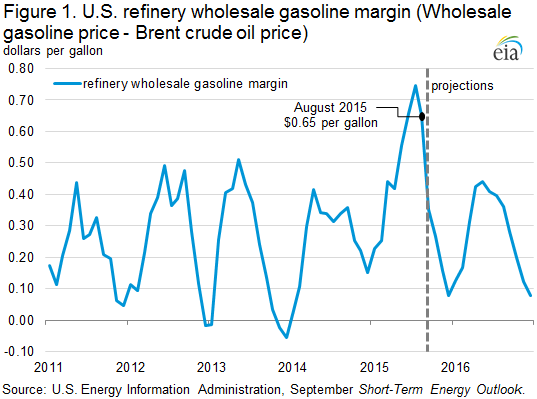

Global gasoline demand in the first half of 2015 was higher than expected, at a time when crude oil prices were falling, which contributed to very strong refinery wholesale gasoline margins. However, EIA does not project the same pattern to continue next year.

The Short-Term Energy Outlook (STEO), which was released on September 9, forecasts slowing gasoline demand growth. While gasoline margins are projected to show their typical seasonal trend, falling from their 2015 peak to a low point at the end of the year, then rising through spring 2016, next year’s forecast margins are closer to those experienced over the 2011-14 period than to the higher wholesale margins in 2015. In addition to lower expected gasoline demand growth, the outlook for lower margins reflects a forecast rise in Brent crude oil prices during 2016 and the expectation that refinery outages in 2016 will not be as significant for gasoline markets as those experienced in 2015.

The most recent data from the U.S. Federal Highway Administration show Americans drove a record 1.54 trillion miles during the first half of 2015, compared with the previous high of 1.50 trillion miles driven in the first half of 2007, contributing to higher demand for gasoline in the United States. Monthly data show gasoline consumption in the United States increased by 3% during the first half of 2015 compared with the first half of 2014.

U.S. motor gasoline consumption, which rose by 80,000 b/d in 2014, is projected to increase by 210,000 b/d (2.3%) in 2015 as the effects of employment growth and lower gasoline prices outweigh increases in vehicle fleet efficiency. However, gasoline consumption is forecast to remain flat in 2016, as a long-term trend toward vehicles that are more fuel-efficient offsets the effects of other factors.

The spurt in domestic consumption in 2015 and strong demand from abroad contributed to high refinery wholesale gasoline margins (the difference between the wholesale price of gasoline and the price of Brent crude oil). U.S. average wholesale gasoline margins averaged 65 cents per gallon (gal) in August, 31 cents/gal higher than in August 2014 and 34 cents/gal higher than the five-year average (2010-14) for August (Figure 1).

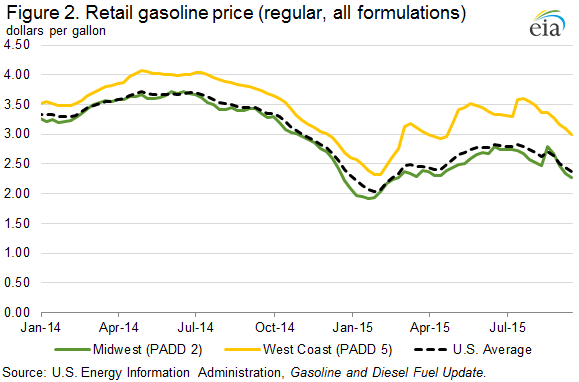

Refinery outages in the Midwest and on the West Coast have contributed to gasoline prices in those regions rising by more than the U.S. average over the past few months, and have resulted in significant price fluctuations. In Petroleum Administration for Defense District (PADD) 2 (Midwest), retail regular gasoline prices rose by 32 cents/gal during the week of August 17 to an average of $2.79/gal, 7 cents/gal higher than the U.S. average, following a temporary unplanned refinery outage at BP’s Whiting, Indiana, refinery. The outage at Whiting, caused by leaks within the larger of two crude distillation units, has since ended, and PADD 2 retail gasoline prices fell to $2.28/gal on September 14, 10 cents/gal below the U.S. average. After reaching a 2015 peak of $3.60/gal on July 20, regular gasoline prices in PADD 5 (West Coast) have since fallen to $2.99/gal as of September 14, but remain 62 cents/gal above the U.S. average as a result of tight gasoline supplies that reflect the ongoing outage at the fluid catalytic cracking unit at ExxonMobil’s Torrance, California refinery (Figure 2).

In August, U.S. retail regular gasoline prices averaged $2.64/gal. EIA expects monthly average prices to decline in the coming months as refineries continue to produce high levels of gasoline, as demand begins to decrease following the peak in the summer driving season, and as the market transitions to lower-cost winter-grade gasoline. EIA projects regular gasoline retail prices to average $2.11/gal in the fourth quarter of 2015.

The U.S. regular gasoline retail price, which averaged $3.36/gal in 2014, is projected to average $2.41/gal in 2015 and $2.38/gal in 2016. The 2015 forecast is unchanged from the August STEO, and the 2016 forecast is 2 cents/gal lower.

U.S. average retail regular gasoline and diesel fuel prices decrease

The U.S. average retail price for regular gasoline decreased six cents from the previous week to $2.38 per gallon as of September 14, 2015, $1.03 per gallon lower than at the same time last year. The West Coast price fell 10 cents to $2.99 per gallon. The Midwest price decreased seven cents to $2.28 per gallon. The East Coast, Gulf Coast, and Rocky Mountain prices each declined five cents, to $2.26 per gallon, $2.09 per gallon, and $2.68 per gallon, respectively.

Propane inventories gain

U.S. propane stocks increased by 1.1 million barrels last week to 97.7 million barrels as of September 11, 2015, 20.3 million barrels (26.2%) higher than a year ago. East Coast, Midwest and Rocky Mountain/West Coast inventories each increased by 0.3 million barrels. Gulf Coast inventory increased by 0.2 million barrels. Propylene non-fuel-use inventories represented 4.5% of total propane inventories.

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!