Coronavirus Panic Fuels A Surge In Cash Demand – Analysis

By VoxEU.org

Despite regular reports in the media over the past decade on the imminent death of cash amid rapid innovation in payment technologies, cash in circulation has actually been growing strongly in many countries. Perhaps unsurprisingly given coronavirus-related health concerns, there have recently been renewed calls to abandon cash and some observers have argued the virus will accelerate its demise. This column argues that the data so far indicate that currency in circulation has actually surged in a number of countries. While the economic shutdowns and increased use of online retailing have recently been diminishing cash’s traditional function as a medium of exchange, it seems that this has been more than offset by panic-driven hoarding of banknotes.

By Jonathan Ashworth and Charles Goodhart*

When it first became realised that Covid-19 would have a significant and deleterious effect on economic activity, there was a ‘dash for cash’, as emphasised by Andrew Hauser in a recent speech (Hauser 2020); this ‘dash for cash’ quite naturally involved a surge in demand for both cash/currency and bank deposits.

Perhaps unsurprisingly, though, given fears that Covid-19 can be transmitted over surfaces and via objects, there have been calls by some governments and various institutions for consumers to use electronic payments instead of cash (Cohn and Megaw 2020) and former US Commerce Secretary Gary Cohn argued in the Financial Times that the Covid-19 was speeding up the disappearance of cash (Cohn 2020). Indeed, it is notable that signs have sprung up in many open shops either giving preference for other means of payment or even refusing to accept currency at all.

With a reasonable amount of data now available, we have examined the latest trends in cash in circulation in a number of countries affected by Covid-19 to see what was going on (Ashworth and Goodhart 2020). We had thought that there might be a subsequent reversal of the initial surge but, so far at any rate, there has been very little sign of that; rather, the increase in currency usage has continued. The surge in cash in circulation has been particularly notable in the US, Canada, Italy, Spain, Germany, France, Australia, Brazil, Mexico, India and Russia, to name but a few.

In the US, cash in circulation increased by 0.9% in the week to 23 March, which was the third largest increase on record after the surges in late December 1999 and January 2000 amid Y2K bug fears. After increasing by 1.1% over March, currency in circulation increased by approximately 2% in each of April, May and June – on a par with previous record gains in December 1999 and January 2000. As a result, the year-on-year percentage increase in currency in circulation has surged to over 12% on the latest weekly reading, above the peak from the panic driven surge in cash demand around the time of the Great Financial Crisis (GFC) (see Figure 1). Elsewhere in North America, Canadian weekly currency in circulation has accelerated from around 3%Y towards the end of February to almost 12%Y (above its GFC peak) and in Mexico currency in circulation has surged from 6%Y in January-February to 18%Y at present.

Figure 1 US weekly currency in circulation (%Y)

Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of St. Louis (FRED)

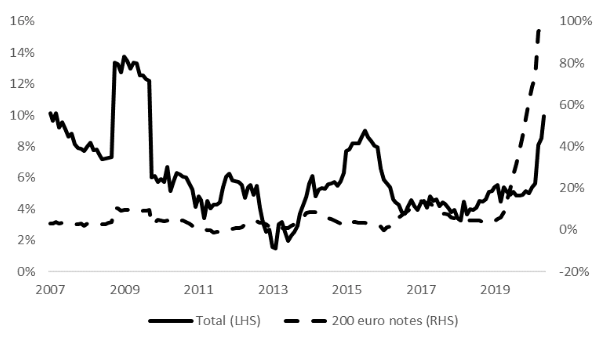

The euro area has also seen huge surges in currency in circulation. In the week to 16 March, it increased by 1.5%, which was the largest gain since December 2008, and the monthly percentage increases of 2.8%, 1.5% and 1.4% in March, April and May were two-to-three times the comparable average monthly increase over the previous decade. The large denomination €200 note has been an important driver of gains, consistent with the panic hoarding of notes. Despite representing 7% of the value of the stock of banknotes in circulation, it represented almost 30% of the increase over March-May. The year-on-year rate of gain in currency in circulation has risen to around 10% (see Figure 2). This is still below the peak of around 15% in the aftermath of the GFC though. The growth in €200 notes in circulation had already soared after the ECB deposit rate cut to -0.5% in September 2019 and has accelerated from 74%Y in February to 94%Y in May (see Figure 2). France, Germany, Spain and Italy all registered huge monthly gains of currency in circulation of around 3% in March, with the German figure at 3.6% – broadly equivalent to the gain over the previous nine months to the end of February! All four countries recorded solid monthly gains in April and May.

Figure 2 Euro area currency in circulation (%Y)

Source: European Central Bank

We have also seen very noticeable surges in cash demand in a number of other countries such as Russia, Brazil, India, and Australia. In Russia, the year-on-year percentage increase in cash in circulation increased from 6.5% in February to 21% in May, whilst in Brazil it accelerated from 7-8% in January/February to 35% in May. In India, the growth of cash in circulation increased from around 11%Y at the end of February to 21% on the latest reading. In Australia, the 3.4% seasonally adjusted monthly jump in cash demand in April was the joint second largest on record after the 5% jump in October 2008 amid the GFC, and there was another 3.1% jump in May. The gains over April and May were equivalent to the previous seventeen months and the year-on-year percentage increase has soared from a 4-5% recent trend to over 11%.

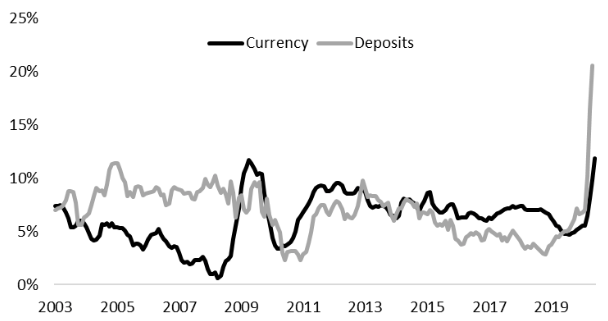

In contrast to typical panic driven surges in cash demand, however, currency-to-deposit ratios – a metric used by economists to gauge the magnitude of the shift from bank deposits into cash (e.g. Ashworth and Goodhart 2015) – may not necessarily have risen, and could actually have fallen. This reflects the fact that due to the enforced shutdowns of major parts of most economies, deposits at commercial banks have also been growing sharply as businesses and households have refrained from spending, or been unable to spend, money on some of their usual activities. As Figure 3 highlights for the US, the value of commercial bank deposits is currently growing at a year-on-year rate of 21% on the latest available data. This has resulted in a declining currency-to-deposit ratio.

Figure 3 Growth in US currency and commercial bank deposits (%Y)

Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of St. Louis (FRED)

The surge in cash demand has not been quite as consistent and pronounced across all major countries, although even some of the initial laggards are now seeing material rises. In the UK, currency in circulation on a seasonally adjusted basis was basically flat over the first four months of the year, suggesting little Covid-related impact. However, there were surprisingly large jumps of 1.4% and 2.4% in May and June – the latter being the largest increase since the Y2K surge and the second largest increase since the late 1970s. Why such belated jumps occurred is less clear. It may reflect the re-opening of the economy and pent-up demand in cash-intensive sectors where online retailing had not been a substitute. Given the weak prior trend, the acceleration of the year-on-year pace of increase to 4.1% has been more modest than elsewhere. In Japan, base effects perhaps related to the extended Golden Week holiday in 2019 resulted in the year-on-year rate of increase of currency in circulation falling to just 0.4% in April 2020 after a steady 2% trend over the previous six months. However, the monthly changes in April, May and June this year have been materially larger than average when compared with comparable months over the previous decade and the year-on-year rate of increase accelerated to over 5%Y in June. In China, the year-on-year rate of increase in currency in circulation has accelerated from around 5%Y in the fourth quarter of last year to over 10%Y in April. However, such an increase does not look particularly remarkable by the standards of recent years.

All in all, only time will tell if the experience of Covid-19 becomes an additional factor alongside technological advances in payment systems in reducing cash usage. Thus far, the economic shutdowns in most countries and increased use of online retailing have clearly diminished, at least temporarily, one of cash’s main traditional functions, namely, as a medium of exchange. However, the data actually suggest that cash in circulation has surged in a number of countries affected by Covid-19. Even after the initial March jumps in some countries, subsequent gains have been large. The rise likely reflects the use of cash for one of its other traditional functions – panic-driven hoarding – although some of the belated increases could also reflect the opening up of cash intensive sectors where internet retailing had not been a substitute.

*About the authors:

- Jonathan Ashworth, Independent Economist

- Charles Goodhart, Emeritus Professor in the Financial Markets Group, London School of Economics

References

Arnold, M (2020), “Banknote virus fears won’t stop Germans hoarding cash”, Financial Times.

Arnold, M and O Storbeck (2020), “European consumers stockpile savings, adding to economic drag”, Financial Times.

Ashworth, J and C A E Goodhart (2015), “Measuring public panic in the Great Financial Crisis”, VoxEU.org, 28 April.

Ashworth, J and C A E Goodhart (2020), “Coronavirus panic fuels a surge in cash demand”, CEPR Discussion Paper 14910.

Cohn, G (2020), “Coronavirus is speeding up the disappearance of cash”, Financial Times.

Hauser, A (2020), “Seven Moments in Spring: Covid-19, financial markets and the Bank of England balance sheet operations”, speech at the Bank of England speech, 4 June.

Thomas, D and N Megaw, (2020), “Coronavirus accelerates shift away from cash”, Financial Times.