US-China Trade War And The High Technology Sector – Analysis

By Manohar Parrikar Institute for Defence Studies and Analyses (MP-IDSA)

By Munish Sharma*

On May 15, 2019, the Donald Trump administration issued an Executive Order (EO) entitled “Securing the Information and Communications Technology and Services Supply Chain”. While it does not specifically mention the Chinese telecommunications major, Huawei, the EO does bring to an end speculation over the future of the Chinese company’s presence and operations in the United States. Pursuant to the International Emergency Economic Powers Act and the National Emergencies Act, the EO declares “a national emergency with respect to the threats against information and communications technology and services in the United States.”1 It does not name any country or company per se, but describes the threat as “information and communications technology or services designed, developed, manufactured, or supplied by persons owned by, controlled by, or subject to the jurisdiction or direction of foreign adversaries.”2 The EO comes in the wake of serious allegations against Chinese telecommunications equipment suppliers, Huawei in particular, on account of malicious cyber-enabled actions, including spying, economic and industrial espionage and close ties to the Chinese government.

Earlier, based on the recommendations of the House Intelligence Committee made way back in 2012, the Trump administration had blacklisted Huawei and ZTE Corporation from supplying equipment for sensitive systems. The 2018 National Defense Authorization Act forbade government agencies from procuring telecommunications equipment or services produced or provided by Huawei and ZTE Corporation.3 For some years now, the US intelligence community, some private sector companies and think tanks have openly voiced espionage concerns arising from the equipment supplied by Chinese companies. The latest EO comes in the midst of an escalating trade war between the US and China, as part of which both sides have imposed tariffs on the import of goods from the other country.

The EO authorises the Secretary of Commerce to, in consultation with heads of other agencies as appropriate, prohibit transactions involving information and communications technology or services from “adversaries”. For its part, the Bureau of Industry and Security (BIS) of the Department of Commerce has placed Huawei Technologies Co. Ltd. and 68 of its non-US affiliates on its ‘Entity List’.4 Exports, re-exports and transfer of all items subject to Export Administration Regulations (EAR) to Huawei and the listed affiliates from the US will be put under review. BIS imposes a licence requirement for all items subject to the EAR and a license review policy of presumption of denial – which clearly means that license applications for export to Huawei and affiliates will be outright denied. Under category 3 (Electronics) and 5 (Telecommunications) of the Commerce Control List, semi-conductor integrated circuits, semi-conductor technology, equipment, devices or material manufacturing equipment, telecommunications equipment, bridges, gateways and routers are controlled items. Items under these categories have significant importance in US-China trade.

Huawei has the largest share (28 per cent) in the global cellular base station market.5 The company supplies telecom products and solutions to some 1500 networks in 170 countries.6 In the wake of the May 15 EO, the US probably seeks to address the issue of its rising trade imbalance with respect to China as well as curtail Huawei’s aggressive expansion in the global telecommunications trade, especially when 5G deployment is also around the corner.

US-China High Technology Trade and Trade Imbalance

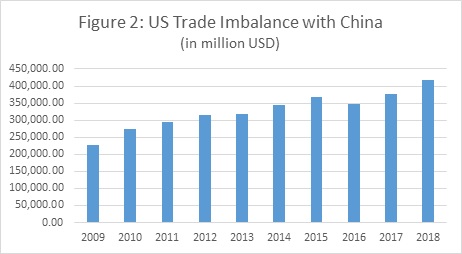

US-China trade, at around USD 660 billion in 2018, has increased by 80 per cent since 2009. China has gained substantially from this bilateral trade, with a balance of USD 419 billion in its favour. The trade imbalance itself has grown by 85 percent, from USD 227 billion to 419 billion between 2009 and 2018 (Figures 1 and 2).

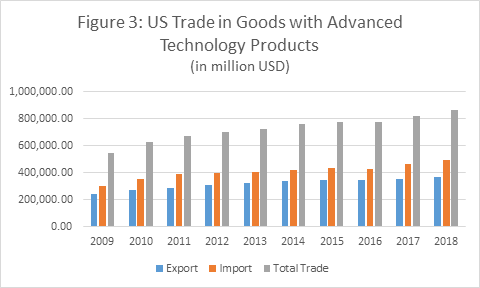

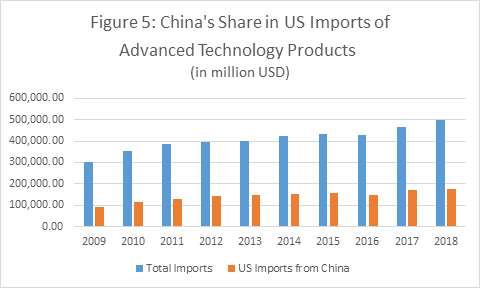

Out of 22,000 commodities that the US trades globally, 500 products from high technology fields such as biotechnology, Information and Communication Technology (ICT), electronics, aerospace and advanced materials are classified as Advanced Technology Products (ATP). These products represent leading edge technology. In this category, the percentage of exports and imports in US global trade has remained steady at around 45 and 55 per cent, respectively, over the last decade. Imports, for instance, were 57 per cent of global ATP trade in 2018 (Figure 3). Nevertheless, US exports of ATP to China have consistently remained marginal; it was seven per cent in 2009 and had increased to only 10 per cent by 2018 (Figure 4). In contrast, China had around a 30 per cent share in global US imports of ATP in 2008, which increased to 35 per cent in 2018 with a value of USD 173 billion (Figure 5). The US, despite managing to maintain a balance between its exports and imports in the global ATP trade, has failed to do this in its ATP trade with China.

The skewed character of bilateral ATP trade between US and China explains the present US apprehensions clearly. During the years 2008 to 2019, US imports of ATP from China total 80 percent of its bilateral ATP trade with China (Figure 6). Under the ATP category, the US imported around USD 157 billion worth of ICT products from China in 2018, while it exported only close to USD 4 billion worth. US imports of ICT products have increased around 50 per cent in these years, from USD 79 billion in 2009. At the same time, US ICT exports to China during these years have remained rather low hovering between 4.5 and 2.5 per cent of its total ICT trade with China (Figure 7).

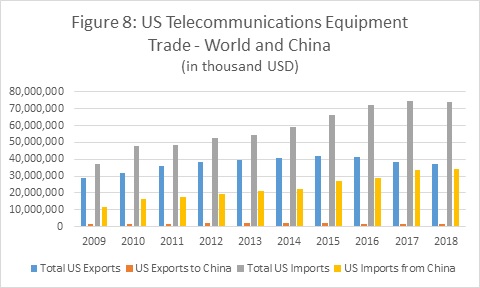

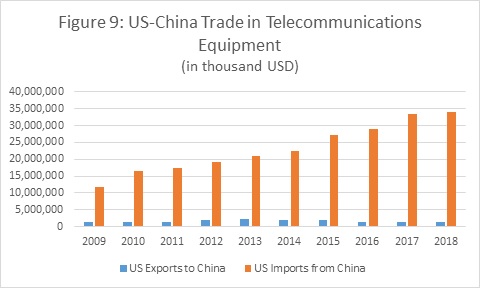

Nor do the trade figures in telecommuincations equipment paint a bright picture for the US. In 2018, China accounted for only four per cent of global US exports of telecommuincations equipment. But, for the same year, China had a whopping 45 per cent share in total telecommuincations equipment imported by the US (Figure 8). US-China telecommuincations equipment trade heavily favours China. At USD 34 billion in 2018, imports from China accounted for 96 per cent of bilateral trade in this segment. US telecommuincations equipment exports were worth only USD 1.43 billion in 2018. From 2009 to 2018, such imports from China increased by 188 per cent – from USD 11.7 billion to 33.9 billion (Figure 9). US telecommuincations equipment exports to China for the same period have grown by just 4.25 per cent.

Technology is a key factor in US economic strength. An upper hand in ATP signifies technological leadership. Its consistent increase in exports in this segment has helped

China to penetrate markets in both developing and developed countries. The US appears to be caving in to the competition from China, as it is unable to arrest its falling share of exports in ICT and telecommunication equipment trade. Global US exports of telecommunication equipment, for instance, has grown by 30 per cent over the last one decade, but its imports have almost doubled (Figure 8). The gap between exports and imports is widening and transforming the US into a market for such products rather than an exporter.

Implications for the US

The May 15 EO aims to correct this imbalance in the midst of the escalating US-China trade war. It will not only adversely impact upon US companies and citizens but also have global ramifications. Chinese-made ICT products are much cheaper than their Western counterparts. Consumers of ICT products are generally individuals and businesses. If companies of Chinese origin are forbidden or restricted from carrying out their business in the US or with their American counterparts, the costs of ICT products will certainly rise. There are no replacement products either, as no other country can match China in this regard.

Chinese telecommunication manufactures have been at the epicentre of conflicts, be it related to espionage earlier or trade wars now. It is important to note that Huawei is closely knit with the global technology supply chains. Its presence in the US entity list will send ripples through these supply chains, disrupting not just American but global markets as well. US companies also gain significantly from Huawei — out of USD 70 billion that Huawei spent on procuring components in 2018, close to USD 11 billion went to US firms. 7 Flex, Broadcom, Qualcomm, Intel, Microsoft and Texas Instruments are all suppliers of components and technology to Huawei. These US companies would now require a licence to continue doing business with Huawei or they will probably be proscribed from engaging in any business activity. Further, a disruption in the manufacturing process owing to the loss of suppliers from the US will escalate costs for Huawei’s global clients, which also includes US allies. This can potentially derail or further increase the costs of the 5G roll-out plans of many countries who have roped in Huawei for this purpose.

Major telecom players in the US do not use Huawei equipment in their networks. But, surprisingly, the smaller ones, especially rural carriers (fewer than 100,000 subscribers) depend on Huawei and ZTE to an extent.8 If the ban on Huawei persists and these carriers are forced to replace the company’s equipment, their costs will skyrocket. Moreover, Huawei will most certainly be kept out of 5G deployment in US. Smaller carriers, who count on low-cost equipment from Chinese manufacturers, might not be able to bear the costs of 5G deployment. It may either leave rural consumers devoid of 5G technology, or simply increase the costs substantially for consumers.

The grant of a temporary 90-day general export licence from the US Department of Commerce to Huawei indicates that the US has not yet reached the point of no return. Huawei could be removed from the entity list. Nonetheless, as evident from the trade figures, the US is a lot more dependent on Chinese ICT products and telecommunication equipment. American firms have close business relationships with their Chinese counterparts, be it is Apple iPhones assembled in Shenzen or Qualcomm supplying smartphones or cellular modem chipsets to Chinese manufacturers. In this era of complex interdependence, such sudden disruptions in supply chains will not only hurt Chinese businesses in the US and elsewhere, but also damage the US economy as well as its reputation as a business destination. It is after all a vicious circle.

Views expressed are of the author and do not necessarily reflect the views of the IDSA or of the Government of India.

*About the author: Munish Sharma is Consultant at the Institute for Defence Studies and Analyses, New Delhi

Source: This article was published by IDSA

- 1. “Statement from the Press Secretary”, The White House, May 15, 2019, at https://www.whitehouse.gov/briefings-statements/statement-press-secretary-56/, accessed May 16, 2019.

- 2. “Executive Order on Securing the Information and Communications Technology and Services Supply Chain”, The White House, May 15, 2019, at https://www.whitehouse.gov/presidential-actions/executive-order-securing-information-communications-technology-services-supply-chain/, accessed May 16, 2019.

- 3. U.S. Government Publishing Office, “H.R.2810 – National Defense Authorization Act for Fiscal Year 2018”, December 12, 2017, at https://www.congress.gov/bill/115th-congress/house-bill/2810/text, accessed May 17, 2019.

- 4. Federal Register, Vol., 84, No. 98, May 21, 2019, at https://www.bis.doc.gov/index.php/documents/regulations-docs/2394-huawei-and-affiliates-entity-list-rule/file, accessed May 22, 2019.

- 5. Isao Horikoshi, Takashi Kawakami and Kosei Fukao, “Huawei blacklisting bites 5G carriers in the wallet”, Nikki Asian Review, February 05, 2019, at https://asia.nikkei.com/Economy/Trade-war/Huawei-blacklisting-bites-5G-carriers-in-the-wallet, accessed May 17, 2019.

- 6. Huawei, “Corporate Introduction”, at https://www.huawei.com/en/about-huawei/corporate-information, accessed May 16, 2019.

- 7. Sijia Jiang, Michael Martina, “Huawei’s $105 billion business at stake after U.S. broadside”, Reuters, May 16, 2019, https://www.reuters.com/article/us-usa-trade-china-huawei-analysis/huaweis-105-billion-business-at-stake-after-us-broadside-idUSKCN1SM123, accessed May 17, 2019.

- 8. Zak Doffman,” Trump Signs Executive Order That Will Lead to U.S. Ban on Huawei”, Forbes, May 15, 2019, at https://www.forbes.com/sites/zakdoffman/2019/05/15/trump-expected-to-sign-executive-order-leading-to-ban-on-huawei-this-week/#1c3259d668d9, accessed May 17, 2019.