ECB Blames Inflation On Everything But Itself – OpEd

By MISES

By Louis Rouanet*

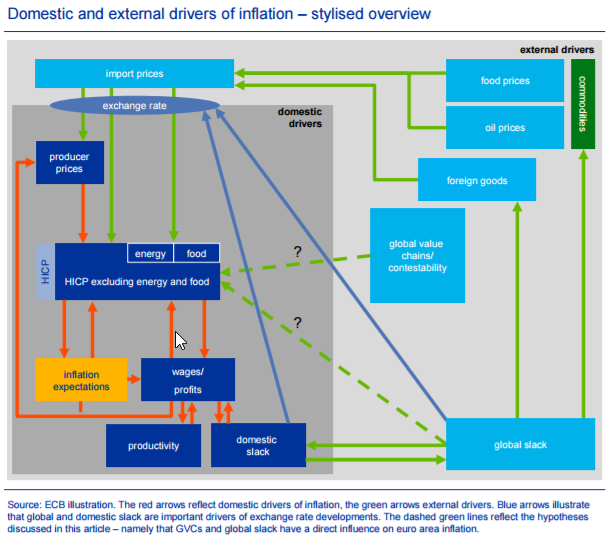

Unsurprisingly, central banks are reluctant to claim credit for inflation. In their latest bulletin, the European Central Bank (ECB) published the graph below explaining what causes inflation.

See the problem? Neither the money supply nor the ECB are mentioned. While there are many factors that influence the purchasing power of money, inflation is still inherently a monetary phenomenon and the role central banks play simply can’t be ignored.

Instead, the ECB prefers to do what all central banks did just before the 2009 great recession: blame inflation on rising food and energy prices. But large central banks like the ECB have a strong and disproportionate effect on energy prices, as predicted by Austrian business cycle theory.

The rise in oil prices in 2007, for example, was triggered by the end of the euphoric monetary boom initiated by the Fed and the ECB in the years prior. As investment in energy production was fueled, in part, by credit expansion instead of real savings.

The quantity of producer’s goods — or at least of some of them — revealed themselves to be insufficient to complete the plans of entrepreneurs, thus generating a sharp increase in their prices.

Therefore the ECB has some responsibility in the so-called external drivers of inflation.

Another problem worth noting is that the ECB seems eager to revive the old myth of cost push inflation. The author of the ECB bulletin writes that: “Domestic price pressures result mainly from wage and price-setting behaviour, which is closely linked to the domestic business cycle.”

But it is the values of the first order goods which are imputed back to productive factors, rather than the other way around. As Henry Hazlitt puts it:

The other rival theory is that inflation and the rise of prices are caused by higher wage demands — by a “cost push.” But this theory reverses cause and effect. “Costs” are prices. An increase in wages above marginal productivity, if it were not preceded, accompanied, or quickly followed by an increase in the supply of money, would not cause inflation; it would merely cause unemployment. It is not true, as so often assumed, that a wage increase in a given firm or industry can be simply “added on to the price.” Without an increased money supply, prices cannot be raised without reducing demand and sales, and hence production and employment. We can stop the “cost push” if we halt the increase in the money supply and repeal the labor laws that confer irresponsible private powers on union leaders.

With a constant demand for money, it is possible for some prices to go up but it is impossible for all prices to go up. For all prices to go up, a central bank must exist and pump more money into the economy. If, in a free market, the cost for oil increases for whatever reason, other prices, ceteris paribus, must fall.

Of course, the ECB is right to argue that global commodity prices affect the domestic price level. Nonetheless, the bulletin deliberately understates the impact the ECB has on the movement of prices. To simply chalk it up to international pressure will, for sure, become a handy justification for the ECB if they fail to maintain inflation under 2%.

But don’t be fooled, central banks, not oil, are responsible for the debasement of the currency.

About the author:

*Louis Rouanet is currently a student at the Paris Institute for Political Studies.

Source:

This article was published by the MISES Institute